You might also like

- Control Accounts GuideDocument4 pagesControl Accounts GuideTeresa ManNo ratings yet

- Handout - CONTROL ACCOUNTSDocument4 pagesHandout - CONTROL ACCOUNTSDominique MillerNo ratings yet

- Control accounts streamline accountingDocument14 pagesControl accounts streamline accountingXue YikNo ratings yet

- Chapater 7 Books of Accounts and Double Entry SystemDocument9 pagesChapater 7 Books of Accounts and Double Entry SystemAngellouiza MatampacNo ratings yet

- Lecture 5 - Books of Accounts and Double Entry SystemDocument7 pagesLecture 5 - Books of Accounts and Double Entry SystemmallarilecarNo ratings yet

- Control AccountDocument6 pagesControl AccountPranitha RaviNo ratings yet

- Mgt101-11 - Control AccountsDocument52 pagesMgt101-11 - Control AccountsKamran ArshafNo ratings yet

- As Level Accounting NotesDocument77 pagesAs Level Accounting NotesRoHan ChooramunNo ratings yet

- As Level Accounting Notes.Document75 pagesAs Level Accounting Notes.SameerNo ratings yet

- CH 14 Audit of Sales and Collection Cycle Tests of Controls and Substantive Tests of TransactionsDocument11 pagesCH 14 Audit of Sales and Collection Cycle Tests of Controls and Substantive Tests of TransactionsAldwin CalambaNo ratings yet

- Audit of Sales and Collection CycleDocument4 pagesAudit of Sales and Collection Cyclenadxco 1711No ratings yet

- Control AccountsDocument3 pagesControl AccountsLilian OngNo ratings yet

- Trial Balance and Rectification of ErrorsDocument7 pagesTrial Balance and Rectification of Errorsakshaya ammuNo ratings yet

- Financial AccountingDocument53 pagesFinancial Accountingnikhil100% (1)

- Financial AccountingDocument161 pagesFinancial AccountingAbdulqadir Al-Emad100% (1)

- Financial Accounting and Reporting (FAR) - Part 5Document3 pagesFinancial Accounting and Reporting (FAR) - Part 5Malcolm HolmesNo ratings yet

- B215 AC03 Ibiz Software Solutions - 6th Presentation - 30apr2009Document34 pagesB215 AC03 Ibiz Software Solutions - 6th Presentation - 30apr2009tohqinzhiNo ratings yet

- Books of Accounts and Double-Entry SystemDocument9 pagesBooks of Accounts and Double-Entry SystemLacson DennisNo ratings yet

- Lecture Note F3 - Part 1Document45 pagesLecture Note F3 - Part 1mai linhNo ratings yet

- The Accounting Cycle Study GuideDocument9 pagesThe Accounting Cycle Study Guidetoma hawkNo ratings yet

- The Accounting Cycle of a Trading CompanyDocument10 pagesThe Accounting Cycle of a Trading CompanyNhim Muzt NhimuztNo ratings yet

- Jan Marie Valencia Kharla Baladjay Recca Anna Laranan Rex Martin GuceDocument46 pagesJan Marie Valencia Kharla Baladjay Recca Anna Laranan Rex Martin GuceElsie AdornaNo ratings yet

- CONTROL ACCOUNT NotesDocument2 pagesCONTROL ACCOUNT Notesndumiso100% (2)

- ISR 111 - Chapter 7 MaterialsDocument9 pagesISR 111 - Chapter 7 MaterialsTrisha Nicole FajardoNo ratings yet

- Chapter Two Audit of Receivables and Sales: Page - 1Document20 pagesChapter Two Audit of Receivables and Sales: Page - 1mubarek oumer100% (1)

- Acct For Mgrs Chapter ThreeDocument29 pagesAcct For Mgrs Chapter ThreeAbdiNo ratings yet

- Control Acc F5Document15 pagesControl Acc F5Tinevimbo NdlovuNo ratings yet

- Finacco Module 2Document18 pagesFinacco Module 2obtuse anggelNo ratings yet

- A Review of The Accounting CycleDocument46 pagesA Review of The Accounting CycleRNo ratings yet

- Chapter Two - Fundamentals of AcctDocument14 pagesChapter Two - Fundamentals of AcctGedionNo ratings yet

- Accounting Cheat SheetDocument6 pagesAccounting Cheat SheetTrisha Mae LandichoNo ratings yet

- Fund W1-3Document55 pagesFund W1-3Edren LoyloyNo ratings yet

- Sectional and Self Balancing SystemDocument7 pagesSectional and Self Balancing SystemBhupender Singh Kaushal78% (9)

- Module 001: Review of The Basic Accounting Concepts and PrinciplesDocument18 pagesModule 001: Review of The Basic Accounting Concepts and PrinciplesHo Ming LamNo ratings yet

- Accounting Equation and Double Entry BookkeepingDocument29 pagesAccounting Equation and Double Entry BookkeepingArvin ToraldeNo ratings yet

- Lecture 2 Audit of The Sales and Collection Cycle Tests of ControlsDocument46 pagesLecture 2 Audit of The Sales and Collection Cycle Tests of ControlsShiaab Aladeemi100% (1)

- GuidetoBookkeepingConcepts PDFDocument18 pagesGuidetoBookkeepingConcepts PDFSarah HlordjiNo ratings yet

- FA1 1 3 Chapters PDFDocument35 pagesFA1 1 3 Chapters PDFJerlin PreethiNo ratings yet

- General Ledger and SubledgersDocument2 pagesGeneral Ledger and SubledgersCharielle Esthelin BacuganNo ratings yet

- A Review of The Accounting CycleDocument44 pagesA Review of The Accounting CycleBelle PenneNo ratings yet

- Chapter 2Document23 pagesChapter 2Genanew AbebeNo ratings yet

- Merchandise: Periodic Inventory MethodDocument11 pagesMerchandise: Periodic Inventory MethodLav Casal CorpuzNo ratings yet

- Acc. ReceivableDocument11 pagesAcc. ReceivableUswatun HsnNo ratings yet

- Lesson 1 and 2 - Single Entry System, Correction of ErrorsDocument8 pagesLesson 1 and 2 - Single Entry System, Correction of ErrorsThe Brain Dump PHNo ratings yet

- AccountingDocument2 pagesAccountingazazelrallosNo ratings yet

- Ccounting Nformation YstemDocument37 pagesCcounting Nformation YstemafridaNo ratings yet

- Arens - Chapter14 AuditingDocument39 pagesArens - Chapter14 AuditingtableroofNo ratings yet

- AIS Chapter 4 Revenue CycleDocument6 pagesAIS Chapter 4 Revenue CycleKate Alvarez100% (1)

- Basic Accounting For IT Part IIDocument4 pagesBasic Accounting For IT Part IImailbag6No ratings yet

- Basic AccountingDocument2 pagesBasic AccountingBea RoseNo ratings yet

- Financial Management Development Financial Accounting Basic AccountingDocument8 pagesFinancial Management Development Financial Accounting Basic AccountingPururaja AjsNo ratings yet

- CHP 14 NotesDocument22 pagesCHP 14 NotesDhruvit DadNo ratings yet

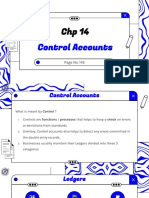

- Chapter 4 Control Account & Their ReconciliationDocument13 pagesChapter 4 Control Account & Their ReconciliationSyed MunibNo ratings yet

- Control Accounts: Summarize Receivables & PayablesDocument4 pagesControl Accounts: Summarize Receivables & Payablesfurqan100% (1)

- Control Final o LevelDocument18 pagesControl Final o Levelparwez_0505No ratings yet

- ch15Document29 pagesch15xxxjungxzNo ratings yet

- Grdae 9 - Ems - Financial Literacy SummaryDocument17 pagesGrdae 9 - Ems - Financial Literacy SummarykotolograceNo ratings yet

- Bookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursFrom EverandBookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- Week 1 - Exercises (S)Document9 pagesWeek 1 - Exercises (S)Teresa ManNo ratings yet

- Profit For The Year (W1) 58 625 41 875Document5 pagesProfit For The Year (W1) 58 625 41 875Teresa ManNo ratings yet

- Week 02 - Ratios - SDocument6 pagesWeek 02 - Ratios - STeresa ManNo ratings yet

- Week 2 - In-Sessional PracticeDocument2 pagesWeek 2 - In-Sessional PracticeTeresa ManNo ratings yet

- Fact Sheet - Financial Statements For Sole TradersDocument5 pagesFact Sheet - Financial Statements For Sole TradersTeresa ManNo ratings yet

- Valuation of Inventory Methods and Their ImpactDocument4 pagesValuation of Inventory Methods and Their ImpactTeresa ManNo ratings yet

- Week 1 - AssignmentDocument27 pagesWeek 1 - AssignmentTeresa ManNo ratings yet

- Course OutlineDocument1 pageCourse OutlineTeresa ManNo ratings yet

- Week 1 - DepreciationDocument8 pagesWeek 1 - DepreciationTeresa ManNo ratings yet

- Week 1 - Correction of ErrorsDocument16 pagesWeek 1 - Correction of ErrorsTeresa ManNo ratings yet

- Answer To Q2Document3 pagesAnswer To Q2Teresa ManNo ratings yet

- Blindness Theme Wheel visualizes themes in the novelDocument1 pageBlindness Theme Wheel visualizes themes in the novelTeresa ManNo ratings yet

- International Advanced Level Accounting worksheet errors and partnership accountsDocument6 pagesInternational Advanced Level Accounting worksheet errors and partnership accountsTeresa ManNo ratings yet

- Blindness Theme Wheel VisualizationDocument1 pageBlindness Theme Wheel VisualizationTeresa ManNo ratings yet

- Blank Symbol Analysis OrganizerDocument1 pageBlank Symbol Analysis OrganizerTeresa ManNo ratings yet

- 開立發票與結帳Document12 pages開立發票與結帳Teresa ManNo ratings yet

- Completed Theme WheelDocument1 pageCompleted Theme WheelTeresa ManNo ratings yet

- Blindness and Symbols in Saramago's NovelDocument7 pagesBlindness and Symbols in Saramago's NovelTeresa ManNo ratings yet

- Symbol Analysis OrganizersDocument4 pagesSymbol Analysis OrganizersTeresa ManNo ratings yet

- Blank Theme Wheel With Blank ThemesDocument1 pageBlank Theme Wheel With Blank ThemesTeresa ManNo ratings yet

- 索取產品目錄和價目表Document14 pages索取產品目錄和價目表Teresa ManNo ratings yet

- Analyze Blindness with LitCharts Teacher EditionDocument3 pagesAnalyze Blindness with LitCharts Teacher EditionTeresa ManNo ratings yet

- CH11 CartaDocument13 pagesCH11 CartaTeresa ManNo ratings yet

- Blindness LitChartDocument71 pagesBlindness LitChartTeresa ManNo ratings yet

- A Powerful Graphic Liquid Crystal Display: Column #47, March 1999 by Lon GlaznerDocument16 pagesA Powerful Graphic Liquid Crystal Display: Column #47, March 1999 by Lon GlaznerVijay P PulavarthiNo ratings yet

- Recording of Dying DeclarationDocument6 pagesRecording of Dying DeclarationsarayusindhuNo ratings yet

- NBCC Green ViewDocument12 pagesNBCC Green Views_baishyaNo ratings yet

- OsteoporosisDocument57 pagesOsteoporosisViviViviNo ratings yet

- Impacts of Gmos On Golden RiceDocument3 pagesImpacts of Gmos On Golden RiceDianna Rose Villar LaxamanaNo ratings yet

- Unit 1 Advanced WordDocument115 pagesUnit 1 Advanced WordJorenn_AyersNo ratings yet

- Consumer Perception of Digital Payment Modes in IndiaDocument14 pagesConsumer Perception of Digital Payment Modes in Indiakarthick50% (2)

- EasyGreen ManualDocument33 pagesEasyGreen ManualpitoupitouNo ratings yet

- QRT1 WEEK 8 TG Lesson 22Document5 pagesQRT1 WEEK 8 TG Lesson 22Bianca HernandezNo ratings yet

- Waiters' Training ManualDocument25 pagesWaiters' Training ManualKoustav Ghosh90% (51)

- Document Application and Review FormDocument1 pageDocument Application and Review FormJonnel CatadmanNo ratings yet

- List of Registered Non Govt and Govt Secondary SchoolDocument200 pagesList of Registered Non Govt and Govt Secondary SchoolDennisEudes78% (9)

- Integrate Payments Direct Post APIDocument31 pagesIntegrate Payments Direct Post APIAnjali SharmaNo ratings yet

- 6 Fsiqiatria-1524041346Document48 pages6 Fsiqiatria-1524041346მირანდა გიორგაშვილიNo ratings yet

- Sivas Doon LecturesDocument284 pagesSivas Doon LectureskartikscribdNo ratings yet

- Indigo CaseDocument13 pagesIndigo Caseharsh sainiNo ratings yet

- Criteria For Judging MR and Ms UNDocument9 pagesCriteria For Judging MR and Ms UNRexon ChanNo ratings yet

- Fasader I TraDocument56 pagesFasader I TraChristina HanssonNo ratings yet

- Policy Based Routing On Fortigate FirewallDocument2 pagesPolicy Based Routing On Fortigate FirewalldanNo ratings yet

- 7) Set 3 Bi PT3 (Answer) PDFDocument4 pages7) Set 3 Bi PT3 (Answer) PDFTing ShiangNo ratings yet

- Tsu m7 Practice Problems Integral CalculusDocument1 pageTsu m7 Practice Problems Integral CalculusJAMNo ratings yet

- IELTS2 Video ScriptsDocument5 pagesIELTS2 Video ScriptskanNo ratings yet

- g6 Sws ArgDocument5 pagesg6 Sws Argapi-202727113No ratings yet

- Reported SpeechDocument2 pagesReported SpeechlacasabaNo ratings yet

- A-7 Longitudinal SectionDocument1 pageA-7 Longitudinal SectionarjayymerleNo ratings yet

- Use VCDS with PC lacking InternetDocument1 pageUse VCDS with PC lacking Internetvali_nedeleaNo ratings yet

- Water As A Weapon - Israel National NewsDocument11 pagesWater As A Weapon - Israel National NewsJorge Yitzhak Pachas0% (1)

- Down Syndrome Research PaperDocument11 pagesDown Syndrome Research Paperapi-299871292100% (1)

- Edited General English Question Paper Part 1Document12 pagesEdited General English Question Paper Part 1Utkarsh R MishraNo ratings yet

- The Merchant of Venice QuestionsDocument9 pagesThe Merchant of Venice QuestionsHaranath Babu50% (4)