You might also like

- E-Marketing and Online BankingDocument8 pagesE-Marketing and Online BankingAnonymous CwJeBCAXpNo ratings yet

- E-banking study comparing SBI and HDFC BankDocument11 pagesE-banking study comparing SBI and HDFC BankAbhinav VermaNo ratings yet

- E BankingDocument10 pagesE BankingAbhimita GaineNo ratings yet

- Dissertation On Internet Banking in IndiaDocument8 pagesDissertation On Internet Banking in IndiaOrderAPaperBillings100% (1)

- Mobile and Online Banking Services in IndiaDocument99 pagesMobile and Online Banking Services in IndiaPrakshi PunmiyaNo ratings yet

- E-Banking in India: Division: C PRN: 16010324225 Program: BBALLB Semester-8thDocument16 pagesE-Banking in India: Division: C PRN: 16010324225 Program: BBALLB Semester-8thGurava reddyNo ratings yet

- Case Study FinanceDocument15 pagesCase Study Financesarah IsharatNo ratings yet

- My Main ProjectDocument29 pagesMy Main ProjectRahul VermaNo ratings yet

- Comparative Study of Sbi & IciciDocument4 pagesComparative Study of Sbi & Icicikamal paridaNo ratings yet

- National Seminar New Frontiers Business Management TechnologyDocument4 pagesNational Seminar New Frontiers Business Management Technologyhằng phạmNo ratings yet

- Dharani e BankDocument10 pagesDharani e Bankmohammed khayyumNo ratings yet

- Essay # 1. Meaning of Internet Banking:: ContentsDocument8 pagesEssay # 1. Meaning of Internet Banking:: ContentsdfgsgfywNo ratings yet

- IJCRT2105956Document5 pagesIJCRT2105956Suny PaswanNo ratings yet

- Brijesh Project All Set To PrintDocument59 pagesBrijesh Project All Set To Printv raviNo ratings yet

- Comparative Study of E-Banking Facilities of ICICI and HDFC BankDocument34 pagesComparative Study of E-Banking Facilities of ICICI and HDFC BankRevati santosh salapNo ratings yet

- NANA VISHNU - e BankDocument10 pagesNANA VISHNU - e BankMOHAMMED KHAYYUMNo ratings yet

- Gouse SnyopsisDocument14 pagesGouse Snyopsisdanbaig096No ratings yet

- Digital Payments Methods in India A Study of Problems and ProspectsDocument8 pagesDigital Payments Methods in India A Study of Problems and ProspectsNandanNo ratings yet

- An Analysis Satisfaction Level of Consumer Through E-Banking and M-BankingDocument3 pagesAn Analysis Satisfaction Level of Consumer Through E-Banking and M-BankingJay ParmarNo ratings yet

- Icici BANK PROJECT Pradeep 2Document73 pagesIcici BANK PROJECT Pradeep 2Marketing HydNo ratings yet

- A Study On Customer S Perception TowardsDocument8 pagesA Study On Customer S Perception TowardsPrabhu SahuNo ratings yet

- 13 Growth of e Banking Challenges and Opportunities in IndiaDocument5 pages13 Growth of e Banking Challenges and Opportunities in IndiaAyesha Asif100% (1)

- E Banking ReportDocument28 pagesE Banking ReportJagwinder SekhonNo ratings yet

- Consumer Perception of E-banking ServicesDocument46 pagesConsumer Perception of E-banking ServicesWwe MomentsNo ratings yet

- E BankingDocument62 pagesE BankingShraddha Yellattikar89% (19)

- Banking Law ProjectDocument12 pagesBanking Law ProjectAYUSHI TYAGINo ratings yet

- Shubham Kumar Chachan CIA - 1Document12 pagesShubham Kumar Chachan CIA - 1AYUSH TREHAN 20215023No ratings yet

- Banking Law AssignmnetDocument11 pagesBanking Law Assignmnetvinay kumarNo ratings yet

- BAAANKDocument6 pagesBAAANKHassenNo ratings yet

- Digital Banking in India: Recent Trends, Advantages and DisadvantagesDocument4 pagesDigital Banking in India: Recent Trends, Advantages and DisadvantagesAmazing VideosNo ratings yet

- E - BankingDocument32 pagesE - BankingSanoj Kumar Yadav0% (1)

- Measuring Customer Satisfaction of Internet Banking ServicesDocument11 pagesMeasuring Customer Satisfaction of Internet Banking ServicesMOHAMMAD ALAMNo ratings yet

- The Impact of E Banking On The Use of Banking Services and Customers SatisfactionDocument4 pagesThe Impact of E Banking On The Use of Banking Services and Customers SatisfactionEditor IJTSRDNo ratings yet

- Digital Banking The Future of BankingDocument25 pagesDigital Banking The Future of BankingHIMANSHU RAWATNo ratings yet

- Banking and Operation Assignment: Submitted By: Prashant Ghimire 17021141125 Batch: 2017-19Document10 pagesBanking and Operation Assignment: Submitted By: Prashant Ghimire 17021141125 Batch: 2017-19Prashant GhimireNo ratings yet

- E Banking ProjectDocument59 pagesE Banking ProjectSurbhi Singhal0% (1)

- Explore SBI's Internet Banking ServicesDocument63 pagesExplore SBI's Internet Banking ServicesHiteshwar Singh Andotra82% (22)

- Customer Perception On E-Banking Services - A Study With Reference To Private and Public Sector BanksDocument12 pagesCustomer Perception On E-Banking Services - A Study With Reference To Private and Public Sector BanksVenkat 19P259No ratings yet

- Banking risksDocument14 pagesBanking risksKaran TolaniNo ratings yet

- 13 Growth of E - Banking Challenges and Opportunities in IndiaDocument5 pages13 Growth of E - Banking Challenges and Opportunities in IndiaPARAMASIVAN CHELLIAHNo ratings yet

- The Role of Internet Banking and Society: C.A.Mahesh Kumar, Y.Lokesh Kumar Reddy, B.SreenivasuluDocument9 pagesThe Role of Internet Banking and Society: C.A.Mahesh Kumar, Y.Lokesh Kumar Reddy, B.SreenivasuluPavan PaviNo ratings yet

- Submitted By: Project Submitted in Partial Fulfillment For The Award of Degree OFDocument21 pagesSubmitted By: Project Submitted in Partial Fulfillment For The Award of Degree OFMOHAMMED KHAYYUMNo ratings yet

- D Sneha e BankDocument16 pagesD Sneha e BankMOHAMMED KHAYYUMNo ratings yet

- Executive Synopsis Internet BankingDocument8 pagesExecutive Synopsis Internet BankingSweta PandeyNo ratings yet

- e Banking ReportDocument40 pagese Banking Reportleeshee351No ratings yet

- Challenges and Opportunities OF E-BankingDocument13 pagesChallenges and Opportunities OF E-BankingNithya NandNo ratings yet

- Top Popularity of Internet Banking at Shri Ram College of CommerceDocument20 pagesTop Popularity of Internet Banking at Shri Ram College of CommerceSaheb DasNo ratings yet

- Bob Internet BankingDocument12 pagesBob Internet BankingSweta PandeyNo ratings yet

- A B C D of E-BankingDocument75 pagesA B C D of E-Bankinglove tannaNo ratings yet

- Olympus Case: Presented byDocument11 pagesOlympus Case: Presented bymageshNo ratings yet

- 1.1 Executive Summary: The Ever Increasing Speed of Internet Enabled Phones & Personal AssistantDocument59 pages1.1 Executive Summary: The Ever Increasing Speed of Internet Enabled Phones & Personal AssistantTejas GohilNo ratings yet

- A Study On Banking System in India - IciciDocument7 pagesA Study On Banking System in India - IcicikizieNo ratings yet

- A Study of Awareness Related To Various Banking FraudsDocument50 pagesA Study of Awareness Related To Various Banking FraudsSakshi SinghNo ratings yet

- Report of Internet BankingDocument40 pagesReport of Internet BankingFILESONICNo ratings yet

- Role of Internet Banking in IndiaDocument14 pagesRole of Internet Banking in IndiapraveenembassyNo ratings yet

- Evaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersFrom EverandEvaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersNo ratings yet

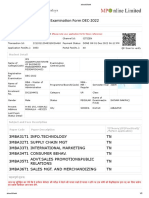

- Examina On Form DEC-2022: Transaction DetailsDocument2 pagesExamina On Form DEC-2022: Transaction DetailsYash BhattNo ratings yet

- Effective Communication Requires Listening and UnderstandingDocument6 pagesEffective Communication Requires Listening and UnderstandingYash BhattNo ratings yet

- Information Technology Presentation On Types of Information Process SystemDocument13 pagesInformation Technology Presentation On Types of Information Process SystemYash BhattNo ratings yet

- Exam Form 2022Document2 pagesExam Form 2022Yash BhattNo ratings yet

- Deva Crop Science Private LimitedDocument1 pageDeva Crop Science Private LimitedYash BhattNo ratings yet

- Brand Management PPT by YASHDocument24 pagesBrand Management PPT by YASHYash BhattNo ratings yet

- Shivam N PDFDocument53 pagesShivam N PDFYash BhattNo ratings yet

- Brand ManagementDocument24 pagesBrand ManagementYash BhattNo ratings yet

- Brand ManagementDocument12 pagesBrand ManagementYash BhattNo ratings yet

- Need For Effective CommunicationDocument4 pagesNeed For Effective CommunicationYash BhattNo ratings yet

- Study On DTH Service ProviderDocument56 pagesStudy On DTH Service ProviderYash BhattNo ratings yet

- Marketing Strategy of Airtel: A Case StudyDocument69 pagesMarketing Strategy of Airtel: A Case StudyYash BhattNo ratings yet

- Wa0033.Document2 pagesWa0033.Yash BhattNo ratings yet

- Volume 5 SFMDocument16 pagesVolume 5 SFMrajat sharmaNo ratings yet

- SY B.Com (Hons) C - Group 5Document27 pagesSY B.Com (Hons) C - Group 5Riya GuptaNo ratings yet

- VP Mortgage Default Servicing in Dallas TX Resume Robert WarrenDocument3 pagesVP Mortgage Default Servicing in Dallas TX Resume Robert WarrenRobertWarrenNo ratings yet

- Sample Personal Statement 2 0Document4 pagesSample Personal Statement 2 0Ly Hoang100% (1)

- Tev - Mrsia Final (Aleiah)Document20 pagesTev - Mrsia Final (Aleiah)Aleiah Jean LibatiqueNo ratings yet

- Water BillDocument1 pageWater BillAlex R0% (1)

- Holding Summary:: Account Name: TARUN JOSHIDocument2 pagesHolding Summary:: Account Name: TARUN JOSHIArshil KhanNo ratings yet

- Foundations of Risk ManagementDocument173 pagesFoundations of Risk ManagementTrà Mi NguyễnNo ratings yet

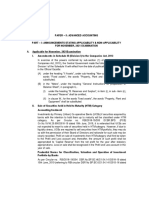

- HI 5020 Corporate Accounting: Session 8a Intra-Group TransactionsDocument15 pagesHI 5020 Corporate Accounting: Session 8a Intra-Group TransactionsFeku RamNo ratings yet

- Overnight Indexed SwapDocument2 pagesOvernight Indexed Swaptimothy454No ratings yet

- FAR 09 Income Tax 1 PDFDocument5 pagesFAR 09 Income Tax 1 PDFAnnalyn AlmarioNo ratings yet

- Case Study On Horniman HorticultureDocument2 pagesCase Study On Horniman Horticulturesanthosh rameshNo ratings yet

- Exercise 6 - 1 Multiple Choice QuestionsDocument3 pagesExercise 6 - 1 Multiple Choice QuestionsYrica100% (1)

- M and N 1Document1 pageM and N 1DDdNo ratings yet

- ACCT4110 Advanced Accounting PRACTICE Exam 2 KEY v2Document14 pagesACCT4110 Advanced Accounting PRACTICE Exam 2 KEY v2accounts 3 lifeNo ratings yet

- Chapter 6-Exercise SetDocument23 pagesChapter 6-Exercise SetNatalie JimenezNo ratings yet

- Chap - 1 IAS 37 Provisions and ContingenciesDocument12 pagesChap - 1 IAS 37 Provisions and ContingenciesSandyNo ratings yet

- PPT Advanced Accounting 7e Hoyle Chapter 2Document42 pagesPPT Advanced Accounting 7e Hoyle Chapter 2Ayimere Dagne FentaNo ratings yet

- #2482 April 2023Document5 pages#2482 April 2023annie janeNo ratings yet

- INSTRUCTION: Please Answer All The Problems That Will Be Found in Your Textbook. Put Your Answers OnDocument6 pagesINSTRUCTION: Please Answer All The Problems That Will Be Found in Your Textbook. Put Your Answers OnMary Ann F. MendezNo ratings yet

- Home Loan Options Ebook EnglishDocument21 pagesHome Loan Options Ebook EnglishAbdul Wadood GharsheenNo ratings yet

- Bajaj Allianz General Insurance Company LTD.: Declaration by The InsuredDocument1 pageBajaj Allianz General Insurance Company LTD.: Declaration by The InsuredArtiNo ratings yet

- T1 - YAL - Qns (12-5-2011Document9 pagesT1 - YAL - Qns (12-5-2011Jennifer EdwardsNo ratings yet

- Advanced Accounting RTP N21Document39 pagesAdvanced Accounting RTP N21Harshwardhan PatilNo ratings yet

- Bookkeeping NC Iii - Core CompetenciesDocument33 pagesBookkeeping NC Iii - Core CompetenciesRonyla EnriquezNo ratings yet

- On January 1Document3 pagesOn January 1Jude Santos0% (1)

- RTP Accounting CA Foundation May 18Document35 pagesRTP Accounting CA Foundation May 18kanishk bahetiNo ratings yet

- LI - 06 - Release of Advise Format Version ABB - Aibb.v50223Document14 pagesLI - 06 - Release of Advise Format Version ABB - Aibb.v50223Asyraf WajdiNo ratings yet

- ABC - PFRS 3 Final Exam ReviewDocument17 pagesABC - PFRS 3 Final Exam ReviewCristel TannaganNo ratings yet

- Financial Analysis of SBI Bank PROJECT (MANSI)Document110 pagesFinancial Analysis of SBI Bank PROJECT (MANSI)manan88% (8)