You might also like

- Solutions To Week 3 Practice Text ExercisesDocument6 pagesSolutions To Week 3 Practice Text Exercisespinkgold48No ratings yet

- Case Study 1 Muhammad JanjuaDocument6 pagesCase Study 1 Muhammad JanjuaAmeer Hamza JanjuaNo ratings yet

- M09 Berk0821 04 Ism C091Document15 pagesM09 Berk0821 04 Ism C091Linda VoNo ratings yet

- Case 7-20 Contact Global Our Analysis-FinalsDocument11 pagesCase 7-20 Contact Global Our Analysis-FinalsJenny Malabrigo, MBANo ratings yet

- 2016 AccountingDocument16 pages2016 AccountingAlison JcNo ratings yet

- D. A Period Cost Under Variable CostingDocument14 pagesD. A Period Cost Under Variable CostingSweet EmmeNo ratings yet

- Fma Past Papers 1Document23 pagesFma Past Papers 1Fatuma Coco BuddaflyNo ratings yet

- Mcgraw QnADocument7 pagesMcgraw QnAGGNo ratings yet

- Acc564 HW 3Document4 pagesAcc564 HW 3Aaryan PatelNo ratings yet

- 102 Test No. 3 Solutions KeeperDocument17 pages102 Test No. 3 Solutions KeepergirlyserendipityNo ratings yet

- Reviewer Acctg 11Document9 pagesReviewer Acctg 11ezraelydanNo ratings yet

- Acst6003 Week11 Tutorial SolutionsDocument5 pagesAcst6003 Week11 Tutorial Solutionsyida chenNo ratings yet

- Cpa Questions Part XDocument10 pagesCpa Questions Part XAngelo MendezNo ratings yet

- F2 Test First 8 ChaptersDocument5 pagesF2 Test First 8 ChaptersAmaara ZafarNo ratings yet

- Cat/fia (Ma2)Document12 pagesCat/fia (Ma2)theizzatirosli50% (2)

- Prepared By: Jilly Boy G. Bruno Jr. and Jerome Marquez (Set A) - 1Document8 pagesPrepared By: Jilly Boy G. Bruno Jr. and Jerome Marquez (Set A) - 1BSIT 1A Yancy CaliganNo ratings yet

- Prelims Ms1Document6 pagesPrelims Ms1ALMA MORENANo ratings yet

- Food Costs Supervisory SalariesDocument11 pagesFood Costs Supervisory SalariesJames CrombezNo ratings yet

- Sample Questions FinalDocument11 pagesSample Questions FinaldunyaNo ratings yet

- Mock 1stDocument8 pagesMock 1stLalan JaiswalNo ratings yet

- SQ - Cost Accounting - Chap 3 Raiborn Part II (Ans)Document8 pagesSQ - Cost Accounting - Chap 3 Raiborn Part II (Ans)Anonymous 7m9SLrNo ratings yet

- Unit - 2 - Financial Statement and RatioDocument37 pagesUnit - 2 - Financial Statement and Ratiodangthanhhd7967% (6)

- Prelim/Advisory Exam: ACC 311 Managerial Accounting 1Document3 pagesPrelim/Advisory Exam: ACC 311 Managerial Accounting 1Dexter Joseph CuevasNo ratings yet

- MCDocument7 pagesMCJMNo ratings yet

- Pset 3Document4 pagesPset 3Assassin Panda14No ratings yet

- F5 QuestionsDocument10 pagesF5 QuestionsDeanNo ratings yet

- Tutorial 2 - Student AnswerDocument6 pagesTutorial 2 - Student AnswerDâmDâmCôNươngNo ratings yet

- Saa Group Cat TT7 Mock 2011 PDFDocument16 pagesSaa Group Cat TT7 Mock 2011 PDFAngie NguyenNo ratings yet

- Latihan Soal DirectDocument7 pagesLatihan Soal Directpadjajaran conferenceNo ratings yet

- Financial Statement Analysis: 7.1.A. Accounting Income and Assets: The Accrual ConceptDocument6 pagesFinancial Statement Analysis: 7.1.A. Accounting Income and Assets: The Accrual ConceptKrishna PrasadNo ratings yet

- S P A C eDocument3 pagesS P A C eAdanechNo ratings yet

- Mock Exam Part 1 Essay September 07, 2018Document13 pagesMock Exam Part 1 Essay September 07, 2018bernard cruzNo ratings yet

- QS07 - Class Exercises SolutionDocument8 pagesQS07 - Class Exercises Solutionlyk0texNo ratings yet

- On Tap Ke Toan Quan Tri 1 Quiz Ke Toan Quan TriDocument45 pagesOn Tap Ke Toan Quan Tri 1 Quiz Ke Toan Quan TriPhan HieuNo ratings yet

- Answers Homework # 6 - BudgetingDocument6 pagesAnswers Homework # 6 - BudgetingRaman ANo ratings yet

- Prelims Ms1Document6 pagesPrelims Ms1ALMA MORENANo ratings yet

- P2 - Performance ManagementDocument11 pagesP2 - Performance Managementmrshami7754No ratings yet

- Finals Answer KeyDocument13 pagesFinals Answer Keymarx marolinaNo ratings yet

- Fma Past Paper 3 (F2)Document24 pagesFma Past Paper 3 (F2)Shereka EllisNo ratings yet

- Finals SolutionsDocument9 pagesFinals Solutionsi_dreambig100% (3)

- MA1 First Test UpdatedDocument14 pagesMA1 First Test UpdatedHammad KhanNo ratings yet

- 2 Points: Clear SelectionDocument8 pages2 Points: Clear SelectionKimmy ShawwyNo ratings yet

- Module 5 Case Accounting For Decision and Transfer PricingDocument14 pagesModule 5 Case Accounting For Decision and Transfer PricingSamuel NderituNo ratings yet

- Bill French - Eve - Version 2Document28 pagesBill French - Eve - Version 2Joanne LazaretoNo ratings yet

- Section C Part 2 MCQDocument344 pagesSection C Part 2 MCQSaiswetha BethiNo ratings yet

- BA213 Test3 Review AnswersDocument27 pagesBA213 Test3 Review AnswersnwuodiopdNo ratings yet

- TheoryDocument9 pagesTheoryprettyNo ratings yet

- Pendants Plus Company CaseDocument4 pagesPendants Plus Company CaseShuo LuNo ratings yet

- Manegiral Accounting Unit 4 5 Test BankDocument8 pagesManegiral Accounting Unit 4 5 Test BankJean NestaNo ratings yet

- Chapter 1: Answers To Questions and Problems: Chapter 01 - The Fundamentals of Managerial EconomicsDocument7 pagesChapter 1: Answers To Questions and Problems: Chapter 01 - The Fundamentals of Managerial EconomicstellmewhourNo ratings yet

- MD&ADocument14 pagesMD&AGraziella CathleenNo ratings yet

- Group 7 Group AssignmentDocument16 pagesGroup 7 Group AssignmentAZLINDA MOHD NADZRINo ratings yet

- Cost & Managerial Accounting II EssentialsFrom EverandCost & Managerial Accounting II EssentialsRating: 4 out of 5 stars4/5 (1)

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Achievements and Skills Showcase Made Easy: The Made Easy Series Collection, #4From EverandAchievements and Skills Showcase Made Easy: The Made Easy Series Collection, #4No ratings yet

- Implementing Results-Based Budget Management Frameworks: An Assessment of Progress in Selected CountriesFrom EverandImplementing Results-Based Budget Management Frameworks: An Assessment of Progress in Selected CountriesNo ratings yet

- Fixed Vs Variable CostDocument9 pagesFixed Vs Variable Costapi-643732098No ratings yet

- Two Leaders Interview PaperDocument9 pagesTwo Leaders Interview Paperapi-643732098No ratings yet

- Ulo Updated GridDocument6 pagesUlo Updated Gridapi-643732098No ratings yet

- Power and Leadership Case Study and Reaction PaperDocument5 pagesPower and Leadership Case Study and Reaction Paperapi-643732098No ratings yet

- Ethical Issues in AccountingDocument11 pagesEthical Issues in Accountingapi-643732098No ratings yet

- Reflection PaperDocument4 pagesReflection Paperapi-643732098No ratings yet

- Final PaperDocument12 pagesFinal Paperapi-643732098No ratings yet

- Financial Analysis Power PointDocument14 pagesFinancial Analysis Power Pointapi-643732098No ratings yet

- Financial Analysis - KHCDocument9 pagesFinancial Analysis - KHCapi-643732098No ratings yet

- Leadership and Personality AssessmentDocument7 pagesLeadership and Personality Assessmentapi-643732098No ratings yet

- Short Paper 5Document3 pagesShort Paper 5api-643732098No ratings yet

- Term PaperDocument5 pagesTerm Paperapi-643732098No ratings yet

- Yayoi Kusama PDFDocument1 pageYayoi Kusama PDFapi-643732098No ratings yet

- Social Justice LetterDocument2 pagesSocial Justice Letterapi-643732098No ratings yet

- The Gospel According To Nicole SavindaDocument3 pagesThe Gospel According To Nicole Savindaapi-643732098No ratings yet

- Approaching The QuranDocument7 pagesApproaching The Quranapi-643732098No ratings yet

- Braveheart Hospital "3 Big Data Sources": Memorandum Report 6.1 AssignmentDocument6 pagesBraveheart Hospital "3 Big Data Sources": Memorandum Report 6.1 Assignmentapi-643732098No ratings yet

- Nicole Savinda PPDocument10 pagesNicole Savinda PPapi-643732098No ratings yet

- Individual Assignment# 02: Course: International Business BUS685, Section-03Document5 pagesIndividual Assignment# 02: Course: International Business BUS685, Section-03AREFIN FERDOUSNo ratings yet

- Catálogo 2022 Indoor - FaroDocument390 pagesCatálogo 2022 Indoor - FaroALESSANDRA MARIA VASQUEZ DIAZNo ratings yet

- Recuenco, Ass4, Basic MacroeconomicsDocument3 pagesRecuenco, Ass4, Basic Macroeconomicskyle RecuencoNo ratings yet

- Certificate On Distribution of Physical Acknowledgements of Kharif 2022 and Rabi 2022-23Document1 pageCertificate On Distribution of Physical Acknowledgements of Kharif 2022 and Rabi 2022-23John StephenNo ratings yet

- Hamachandru S Infosys Technologies Limited, Hyderabad: Name CompanyDocument6 pagesHamachandru S Infosys Technologies Limited, Hyderabad: Name CompanyreenajoseNo ratings yet

- NYSF Walmart Solutionv2Document41 pagesNYSF Walmart Solutionv2Vianna NgNo ratings yet

- MathDocument2 pagesMathJessel Ann MontecilloNo ratings yet

- Revised Road Safety Design Manual - June 1, 2011Document165 pagesRevised Road Safety Design Manual - June 1, 2011gabemzaman100% (1)

- This Study Resource Was: Correct!Document5 pagesThis Study Resource Was: Correct!Angelie De LeonNo ratings yet

- W1L3 - Lecture 3 - The Global North and The Global SouthDocument12 pagesW1L3 - Lecture 3 - The Global North and The Global Southaakriti VermaNo ratings yet

- Statement of AccountDocument1 pageStatement of Accountsneha1299sharmaNo ratings yet

- Understanding The 2007-2008 Global Financial Crisis: Lessons For Scholars of International Political EconomyDocument23 pagesUnderstanding The 2007-2008 Global Financial Crisis: Lessons For Scholars of International Political EconomyFred DuhagaNo ratings yet

- Bank Chapter OneDocument8 pagesBank Chapter OnebikilahussenNo ratings yet

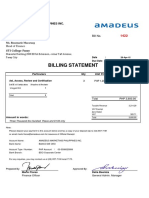

- Bill No. 1422 STI College - PasayDocument1 pageBill No. 1422 STI College - PasayKristel BelenNo ratings yet

- Document 4Document14 pagesDocument 4xipoucrettallu-2379No ratings yet

- Journal of Air Transport Management: Jan K. Brueckner, Chrystyane AbreuDocument8 pagesJournal of Air Transport Management: Jan K. Brueckner, Chrystyane AbreuNicolas KaramNo ratings yet

- MFRS 133 Earnings Per Share Tuto 5Document3 pagesMFRS 133 Earnings Per Share Tuto 5LAVINNYA NAIR A P PARBAKARANNo ratings yet

- 555W Datasheet - Vertex - DE19M (II) - EN - 2020 - PA1 - WebDocument2 pages555W Datasheet - Vertex - DE19M (II) - EN - 2020 - PA1 - WebRoyroute 999No ratings yet

- دريد آل شبيب ، عبد الرحمان الجبوري ، أهمية تطوير هيئة الرقابة على الأوراق المالية لرفع كفاءة السوق المالي حالة شركة وورلدكم الأمريكية PDFDocument17 pagesدريد آل شبيب ، عبد الرحمان الجبوري ، أهمية تطوير هيئة الرقابة على الأوراق المالية لرفع كفاءة السوق المالي حالة شركة وورلدكم الأمريكية PDFKrimo DzNo ratings yet

- A Queen Dies Slowly - The Rise and Decline of Iloilo CityDocument17 pagesA Queen Dies Slowly - The Rise and Decline of Iloilo CityJohn Feil JimenezNo ratings yet

- Economic Impact of Tourism in Greater Palm Springs 2023 CLIENT FINALDocument15 pagesEconomic Impact of Tourism in Greater Palm Springs 2023 CLIENT FINALJEAN MICHEL ALONZEAUNo ratings yet

- Smart-Money Multiplier CourseDocument5 pagesSmart-Money Multiplier CourseTarun ChoudharyNo ratings yet

- Market Failure Response QuestionsDocument4 pagesMarket Failure Response QuestionsSammy PearceNo ratings yet

- Tien Te ReviewDocument3 pagesTien Te ReviewViết BảoNo ratings yet

- Recent Bank Written Math Solution: Prepared By: Musfik AlamDocument9 pagesRecent Bank Written Math Solution: Prepared By: Musfik AlamAbdullah Al NomanNo ratings yet

- Latin America Gri Real Estate 2023Document22 pagesLatin America Gri Real Estate 2023Tiago Pedroso FonsecaNo ratings yet

- Deed of Absolute Sale TemplateDocument2 pagesDeed of Absolute Sale TemplatetataNo ratings yet

- Chapter 9 Treasury FunctionDocument22 pagesChapter 9 Treasury FunctionlostNo ratings yet

- Notice 123Document69 pagesNotice 123Gaming's WarthNo ratings yet

- Galápagos SyndromeDocument4 pagesGalápagos SyndromeDummy1 AccountNo ratings yet