You might also like

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- November Compliance Calendar 2023Document4 pagesNovember Compliance Calendar 2023Astik Dubey ADNo ratings yet

- Indirect Tax Laws 1Document10 pagesIndirect Tax Laws 1GunjanNo ratings yet

- 37th GSTC Meeting - 02Document2 pages37th GSTC Meeting - 02Sahil ShahNo ratings yet

- 37 Meeting of The GST Council, Goa 20 September, 2019 Press ReleaseDocument2 pages37 Meeting of The GST Council, Goa 20 September, 2019 Press ReleasePranay SaxenaNo ratings yet

- 37th GST Council Meet Final Press Release GSTPW 20092019Document2 pages37th GST Council Meet Final Press Release GSTPW 20092019AVASTNo ratings yet

- Unit 5 GSTDocument3 pagesUnit 5 GSTNishu KatiyarNo ratings yet

- 1 Latest GSTR 9 and 9C TaxbykkDocument73 pages1 Latest GSTR 9 and 9C TaxbykkjitendraktNo ratings yet

- Action For Difference in ITC Between 3B and 2ADocument46 pagesAction For Difference in ITC Between 3B and 2Aphani raja kumarNo ratings yet

- Satish Pradhan Dnyanasadhana College: Department of BMS Sample MCQ Questions Subject: Indirect TaxDocument5 pagesSatish Pradhan Dnyanasadhana College: Department of BMS Sample MCQ Questions Subject: Indirect TaxSallu SaleemNo ratings yet

- Circular No.60Document4 pagesCircular No.60Hr legaladviserNo ratings yet

- GST LatestAmendments Issues 01072023Document85 pagesGST LatestAmendments Issues 01072023Selvakumar MuthurajNo ratings yet

- Aino Communique 111th Edition Jan 2023 PDFDocument14 pagesAino Communique 111th Edition Jan 2023 PDFSwathi JainNo ratings yet

- Answer Sheet of Mock Test Paper 31.3.2020Document19 pagesAnswer Sheet of Mock Test Paper 31.3.2020Babu GupthaNo ratings yet

- Returns GSTDocument25 pagesReturns GSTRahul RockzzNo ratings yet

- Section: A MCQ 20X1 20 Marks: A. B. C. DDocument12 pagesSection: A MCQ 20X1 20 Marks: A. B. C. DSarath KumarNo ratings yet

- CompliancecalendarjanDocument24 pagesCompliancecalendarjanDsp VarmaNo ratings yet

- Asmt 10 1920Document69 pagesAsmt 10 1920Prashant ZawareNo ratings yet

- Record Notebook Faculty of Arts & Commerce Department of Cost & Management Accounting (Cma)Document16 pagesRecord Notebook Faculty of Arts & Commerce Department of Cost & Management Accounting (Cma)Sha dowNo ratings yet

- Standardised PPT On GST: Indirect Taxes Committee The Institute of Chartered Accountants of IndiaDocument29 pagesStandardised PPT On GST: Indirect Taxes Committee The Institute of Chartered Accountants of IndiaManjunathreddy SeshadriNo ratings yet

- Latest Updates in GST - NovDocument6 pagesLatest Updates in GST - NovVishwanath HollaNo ratings yet

- 03 WP GST - Ipsum - v2Document47 pages03 WP GST - Ipsum - v2noorensaba01100% (1)

- Standardised PPT On GST: Indirect Taxes Committee The Institute of Chartered Accountants of IndiaDocument28 pagesStandardised PPT On GST: Indirect Taxes Committee The Institute of Chartered Accountants of Indiaatanu karmakarNo ratings yet

- Cir 174 06 2022 CGSTDocument5 pagesCir 174 06 2022 CGSTNM JHANWAR & ASSOCIATESNo ratings yet

- 25-7-21 611 nf-8175 GST QueDocument4 pages25-7-21 611 nf-8175 GST QueJignesh NagarNo ratings yet

- Ram NameDocument2 pagesRam NameStock PsychologistNo ratings yet

- Corporate Compliance Calendar For September, 2022 - Taxguru - inDocument25 pagesCorporate Compliance Calendar For September, 2022 - Taxguru - inSubhash VishwakarmaNo ratings yet

- Annual Return - Salem BranchDocument23 pagesAnnual Return - Salem BranchSureshkumarNo ratings yet

- Registration in GST NovDocument8 pagesRegistration in GST Novvinod.sale1No ratings yet

- Returns: FAQ'sDocument25 pagesReturns: FAQ'smun1barejaNo ratings yet

- GST Unit VDocument29 pagesGST Unit VMani Maran123No ratings yet

- Hc-Allows-Errros in ITC Availment in Tax Head - Rectification-Of-Gstr-3b-After-Expiry-Of-Statutory-Time-LimitDocument3 pagesHc-Allows-Errros in ITC Availment in Tax Head - Rectification-Of-Gstr-3b-After-Expiry-Of-Statutory-Time-LimitychichghareNo ratings yet

- GST Invoice Rules, GST Tax Invoice, Download GST Invoice FormatDocument6 pagesGST Invoice Rules, GST Tax Invoice, Download GST Invoice Formatiiftgscm batch2No ratings yet

- Unit 2 - Part III - Returns Under GST - 30!07!2021Document4 pagesUnit 2 - Part III - Returns Under GST - 30!07!2021Milan ChandaranaNo ratings yet

- Form No. 16A: From ToDocument2 pagesForm No. 16A: From ToRajesh AntonyNo ratings yet

- Recommendations of GST Council Related To Law &procedureDocument2 pagesRecommendations of GST Council Related To Law &procedurePunit AroraNo ratings yet

- Introduction To GST Unit 1 8 Mark Questions.Document4 pagesIntroduction To GST Unit 1 8 Mark Questions.manoharchary157No ratings yet

- GST Returns: BackgroundDocument3 pagesGST Returns: BackgroundPrakash PalanisamyNo ratings yet

- 2023721217646921CircularNo 1of2023-2024Document4 pages2023721217646921CircularNo 1of2023-2024krebs38No ratings yet

- Compliance Calendar NovDocument23 pagesCompliance Calendar NovDsp VarmaNo ratings yet

- Statement of FactsDocument32 pagesStatement of FactsThe Ultra IndiaNo ratings yet

- DR - MGR E & RI - Chennai - 28.05.2021-1Document21 pagesDR - MGR E & RI - Chennai - 28.05.2021-1Sha dowNo ratings yet

- Attachment 1Document2 pagesAttachment 1khabrilaalNo ratings yet

- Anspg5953f 2018-19Document3 pagesAnspg5953f 2018-19virajv1No ratings yet

- Swiggy DFDocument2 pagesSwiggy DFhemanth1234No ratings yet

- IDT Corrigendum For Nov 22 ExamsDocument8 pagesIDT Corrigendum For Nov 22 Examspreeti sinhaNo ratings yet

- Compliance Chart FormatDocument2 pagesCompliance Chart FormatSmeet ShahNo ratings yet

- Signed SCN of PP PlasticsDocument4 pagesSigned SCN of PP PlasticsADARSH TIWARINo ratings yet

- Refund Forms For Centre and StateDocument20 pagesRefund Forms For Centre and StateShail MehtaNo ratings yet

- Indirect Tax Newsletter - July 2023Document15 pagesIndirect Tax Newsletter - July 2023ELP LawNo ratings yet

- Monthly Round-Up - August 2019: Editor'S NoteDocument15 pagesMonthly Round-Up - August 2019: Editor'S NoteSabrina CanoNo ratings yet

- GST MCQS - 2 Without AnswerDocument9 pagesGST MCQS - 2 Without AnswerSpidy MacNo ratings yet

- Final New Indirect Tax Laws Test 3 Detailed May Solution 1617180255Document17 pagesFinal New Indirect Tax Laws Test 3 Detailed May Solution 1617180255CAtestseriesNo ratings yet

- Due Date Calendar Oct 22Document1 pageDue Date Calendar Oct 22Kushal DabhadkarNo ratings yet

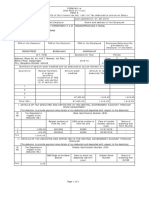

- Form 16 Part A Name and Address of The Employer Name and Designation of The EmployeeDocument3 pagesForm 16 Part A Name and Address of The Employer Name and Designation of The EmployeeishaqmdNo ratings yet

- Chapter 13 - Returns Under GSTDocument11 pagesChapter 13 - Returns Under GSTJay PawarNo ratings yet

- GSTR 9 and 9CDocument4 pagesGSTR 9 and 9Cnitin01.snetNo ratings yet

- Form No. 16A: From ToDocument1 pageForm No. 16A: From ToShail MehtaNo ratings yet

- (See Rule 31 (1) (A) ) : Form No. 16Document8 pages(See Rule 31 (1) (A) ) : Form No. 16Amol LokhandeNo ratings yet

- Reply Letter - Lawyer NoticeDocument3 pagesReply Letter - Lawyer Noticemeghan googlyNo ratings yet

- Ts 129060v150300pDocument191 pagesTs 129060v150300pKing KiteNo ratings yet

- Ijmerr v2n4 8Document15 pagesIjmerr v2n4 8King KiteNo ratings yet

- VETTED Website PublicationDocument2 pagesVETTED Website PublicationKing KiteNo ratings yet

- Application FormDocument7 pagesApplication FormKing KiteNo ratings yet

- Why and Where To Set Up A Foreign Trust For Asset Protectionffjqr PDFDocument3 pagesWhy and Where To Set Up A Foreign Trust For Asset Protectionffjqr PDFshirticicle02No ratings yet

- IOERJTraceable File 57 F 4 F 22858 F 72Document1 pageIOERJTraceable File 57 F 4 F 22858 F 72helio_bacNo ratings yet

- Demand PerformaDocument12 pagesDemand PerformaMuhammad Asif LillaNo ratings yet

- Kepco Ilijan Corp v. CIRDocument4 pagesKepco Ilijan Corp v. CIRPatrick ManaloNo ratings yet

- CIR Vs Fortune TobaccoDocument6 pagesCIR Vs Fortune TobaccoJohnde MartinezNo ratings yet

- CASE DOCTRINES - 2020 Jurisprudence Updates (SC and CTA Cases)Document12 pagesCASE DOCTRINES - 2020 Jurisprudence Updates (SC and CTA Cases)Carlota VillaromanNo ratings yet

- Deductions: Philippines Gross Estate World Gross Estate Deductible LITDocument3 pagesDeductions: Philippines Gross Estate World Gross Estate Deductible LITMaria LopezNo ratings yet

- Od 123941656293759000Document1 pageOd 123941656293759000MANORANJAN BEHERANo ratings yet

- Medical PolicyDocument1 pageMedical PolicyAshok Dangwal100% (4)

- Difference Between Trust and SocietyDocument2 pagesDifference Between Trust and SocietyNancy GirdherNo ratings yet

- Business Finance: Management of Working Capital AccountsDocument17 pagesBusiness Finance: Management of Working Capital AccountsNicole Ann RamosNo ratings yet

- Obillos Vs CirDocument2 pagesObillos Vs CirjessapuerinNo ratings yet

- Annex E - TCC-GOCC - Sworn ApplicationDocument1 pageAnnex E - TCC-GOCC - Sworn ApplicationanabuaNo ratings yet

- FR Revision Video Links FinalDocument2 pagesFR Revision Video Links FinalwipeyourassNo ratings yet

- Books AmazonDocument1 pageBooks AmazonmohitNo ratings yet

- Invoice TableauDocument1 pageInvoice Tableauameen9956No ratings yet

- College Savings Plan ComparisonDocument2 pagesCollege Savings Plan Comparisoncharanmann9165No ratings yet

- Idt 1Document10 pagesIdt 1manan agrawalNo ratings yet

- Ahmedabad Municipal Corporation Mahanagar Sewa SadanDocument1 pageAhmedabad Municipal Corporation Mahanagar Sewa SadanVaghasiyaBipinNo ratings yet

- DTC Agreement Between Ukraine and BelgiumDocument34 pagesDTC Agreement Between Ukraine and BelgiumOECD: Organisation for Economic Co-operation and Development100% (1)

- Mothersonsumi Infotech & Designs Limited: Monthly Leave StatusDocument1 pageMothersonsumi Infotech & Designs Limited: Monthly Leave StatusswabhiNo ratings yet

- Assignment 1 Public BudgetDocument18 pagesAssignment 1 Public BudgetNur IzzatiNo ratings yet

- Cor Clearing LLC The Landmark Center 1299 Farnam Street SUITE 800 OMAHA, NE 68102Document10 pagesCor Clearing LLC The Landmark Center 1299 Farnam Street SUITE 800 OMAHA, NE 68102luisNo ratings yet

- LSB2605 Assignment 2 762303 FINALDocument2 pagesLSB2605 Assignment 2 762303 FINALGift MatoaseNo ratings yet

- Press Release Template 01Document2 pagesPress Release Template 01mkb07No ratings yet

- Volume 1 - 50 Pages MN23Document52 pagesVolume 1 - 50 Pages MN23Kajal KanduNo ratings yet

- C7021-22-2717923 30-03-2023 30-03-2023 Sold by (Pharmacy) Bill To / Ship To (Patient) Healthsaverz Medical LLP UshaDocument1 pageC7021-22-2717923 30-03-2023 30-03-2023 Sold by (Pharmacy) Bill To / Ship To (Patient) Healthsaverz Medical LLP UshaViraj DobriyalNo ratings yet

- Premium Receipt: Personal DetailsDocument1 pagePremium Receipt: Personal Detailskathik MNo ratings yet

- Client Letter ExamplesDocument4 pagesClient Letter ExamplesOh Oh OhNo ratings yet

- Tan v. Del RosarioDocument6 pagesTan v. Del RosarioKlyza Zyra Kate E. AndrinoNo ratings yet