You might also like

- Unit II Supplemental Practice ProblemsDocument5 pagesUnit II Supplemental Practice Problemsgunna4liphNo ratings yet

- Self-test 5 FN 211 matrices and regressionsDocument5 pagesSelf-test 5 FN 211 matrices and regressionsRaiNz SeasonNo ratings yet

- Calculate Expected Returns and Risk of Stock, Bond, and Mixed PortfoliosDocument2 pagesCalculate Expected Returns and Risk of Stock, Bond, and Mixed PortfoliosBijoy SalahuddinNo ratings yet

- Buhlmann Credibility Homework SolutionsDocument11 pagesBuhlmann Credibility Homework Solutionschitechi sarah zakiaNo ratings yet

- ANSWERS Expected Return and Standard Deviation For Individual Stocks and PortfoliosDocument3 pagesANSWERS Expected Return and Standard Deviation For Individual Stocks and PortfoliosKashifNo ratings yet

- Ch 5: Risk Return Portfolio Theory Assets PricingDocument4 pagesCh 5: Risk Return Portfolio Theory Assets PricingMukul KadyanNo ratings yet

- Practice 1Document3 pagesPractice 1bo chian chynNo ratings yet

- Probability distributions and expectationsDocument10 pagesProbability distributions and expectationsthemangoburnerNo ratings yet

- Portfolio Management Handout 1 - AnswersDocument13 pagesPortfolio Management Handout 1 - AnswersPriyankaNo ratings yet

- Chapter Eight End of Chapter Useful Questions and SolutionsDocument18 pagesChapter Eight End of Chapter Useful Questions and SolutionsAbhinav AgarwalNo ratings yet

- AEM 3e Chapter 06Document6 pagesAEM 3e Chapter 06AKIN ERENNo ratings yet

- Chapter 5: Risk and Return: Portfolio Theory and Assets Pricing ModelsDocument3 pagesChapter 5: Risk and Return: Portfolio Theory and Assets Pricing ModelsMukul KadyanNo ratings yet

- Quantitative Methods MM ZG515 / QM ZG515: L6: Probability DistributionsDocument22 pagesQuantitative Methods MM ZG515 / QM ZG515: L6: Probability DistributionsROHIT SINGHNo ratings yet

- Chapter 6 - Problem Solving (Risk)Document5 pagesChapter 6 - Problem Solving (Risk)Shresth KotishNo ratings yet

- Financial Management - Assignment Ch8 - Abdullah Bin Amir - Section ADocument2 pagesFinancial Management - Assignment Ch8 - Abdullah Bin Amir - Section AAbdullah AmirNo ratings yet

- ANSWERS Calculate Expected Return and Standard Deviation For Individual Stocks and PortfoliosDocument3 pagesANSWERS Calculate Expected Return and Standard Deviation For Individual Stocks and PortfoliosKashifNo ratings yet

- Chapter 7Document3 pagesChapter 7YINN YEE TANNo ratings yet

- Answer For Q4 Case Study 1 ExcelDocument5 pagesAnswer For Q4 Case Study 1 ExcelKyounosuke YuiNo ratings yet

- Problem Set 1 SolutionsDocument32 pagesProblem Set 1 Solutionsale.ili.pauNo ratings yet

- Practice Exam1 2021Document9 pagesPractice Exam1 2021silNo ratings yet

- Solution To Chapter 11 Assigned ProblemsDocument4 pagesSolution To Chapter 11 Assigned ProblemsBombitaNo ratings yet

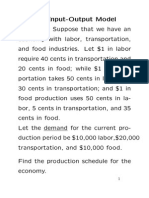

- Leontief 1Document24 pagesLeontief 1Tara BhusalNo ratings yet

- IM - Chapter 2 AnswersDocument4 pagesIM - Chapter 2 AnswersEileen WongNo ratings yet

- Solutions Manual Chapter 22 Estimating Risk Return AssetsDocument13 pagesSolutions Manual Chapter 22 Estimating Risk Return AssetsRonieOlarteNo ratings yet

- Accounts Receivable Management Set A SolutionsDocument20 pagesAccounts Receivable Management Set A Solutions김우림No ratings yet

- Worksheet # 4 - SolutionDocument7 pagesWorksheet # 4 - Solutionahmed wahshaNo ratings yet

- Standard Deviation on Individual Security = σ = √σ: Risk Return Problems Problem 1Document3 pagesStandard Deviation on Individual Security = σ = √σ: Risk Return Problems Problem 1jakia yasminNo ratings yet

- Quiz 7Document3 pagesQuiz 7朱潇妤No ratings yet

- LinPro 2.7.5 structural analysis resultsDocument13 pagesLinPro 2.7.5 structural analysis resultsEdin MuratovicNo ratings yet

- D - Tutorial 4 (Solutions)Document12 pagesD - Tutorial 4 (Solutions)AlfieNo ratings yet

- Finance 261 Portfolio Standard DeviationDocument4 pagesFinance 261 Portfolio Standard DeviationManuel BoahenNo ratings yet

- Microeconomics Assignment 1: I 2i 3i 4iDocument5 pagesMicroeconomics Assignment 1: I 2i 3i 4iYash AgarwalNo ratings yet

- Assignmnt AccountingDocument14 pagesAssignmnt AccountingAqsa AnumNo ratings yet

- Results:: A) Experimental Shear CentreDocument4 pagesResults:: A) Experimental Shear Centrekaram bawadiNo ratings yet

- Questions - Risk and Return - IIDocument3 pagesQuestions - Risk and Return - IIRuchitha PrakashNo ratings yet

- Risk and Return: Portfolio Theory and Assets Pricing Models: Problem 1Document3 pagesRisk and Return: Portfolio Theory and Assets Pricing Models: Problem 1anubha srivastavaNo ratings yet

- Practice Problem 2Document7 pagesPractice Problem 2Austin AzengaNo ratings yet

- ProbabilityDocument3 pagesProbabilityK214662 Abdul RehmanNo ratings yet

- Session 3 DistribtionDocument61 pagesSession 3 DistribtionSriya Aishwarya TataNo ratings yet

- Business Statistics Topic 3 Tutorial Solutions (Q1-Q10)Document4 pagesBusiness Statistics Topic 3 Tutorial Solutions (Q1-Q10)Beryl ChanNo ratings yet

- Latihan Soal Sesi 3 - Nastiti Kartika DewiDocument26 pagesLatihan Soal Sesi 3 - Nastiti Kartika DewiNastiti KartikaNo ratings yet

- GARCH (1,1) : Relatives WeightsDocument14 pagesGARCH (1,1) : Relatives WeightsPritam Kumar GhoshNo ratings yet

- Ch06 Tool KitDocument36 pagesCh06 Tool KitRoy HemenwayNo ratings yet

- Tutorial 5 - SolutionDocument6 pagesTutorial 5 - SolutionNg Chun SenfNo ratings yet

- Unit 4 FMDocument47 pagesUnit 4 FMAlexis ParrisNo ratings yet

- NA - Ma Roki Fajri Aulia Rahma Putri Ahmad Habibie Matkul Manajemen KeuanganDocument2 pagesNA - Ma Roki Fajri Aulia Rahma Putri Ahmad Habibie Matkul Manajemen Keuangankota lainNo ratings yet

- Lecturer Name: MR Moyo: Radreck U. Maenzanise 01182038512Document4 pagesLecturer Name: MR Moyo: Radreck U. Maenzanise 01182038512Morris AloqrothNo ratings yet

- Business Data Final Exam June 2022Document13 pagesBusiness Data Final Exam June 2022Fungai MajuriraNo ratings yet

- ch06 Tool KitDocument36 pagesch06 Tool KitBrandon FrancomNo ratings yet

- Tutorial Set 9 SolutionsDocument8 pagesTutorial Set 9 SolutionsRabinNo ratings yet

- FI4007 Investments: Analysis and Management Week 6-7 Tutorial: Questions and SolutionsDocument6 pagesFI4007 Investments: Analysis and Management Week 6-7 Tutorial: Questions and SolutionsIlko KacarskiNo ratings yet

- Expected Returns, Variance & Correlation of Two-Stock PortfolioDocument8 pagesExpected Returns, Variance & Correlation of Two-Stock PortfolioPuneet MeenaNo ratings yet

- Name:Emmanuel Morgan Tembo NUMBER:201702046 Program:Accounting and Finance Course:Financial Management and Risk AppraisalDocument11 pagesName:Emmanuel Morgan Tembo NUMBER:201702046 Program:Accounting and Finance Course:Financial Management and Risk AppraisalEmmanuel Ēzscod TemboNo ratings yet

- Research AssignmentDocument8 pagesResearch AssignmentAbdusalam IdirisNo ratings yet

- Examples and SolutionsDocument9 pagesExamples and Solutions2002.pawandeepsinghNo ratings yet

- Mean, Variance, Standard DeviationDocument3 pagesMean, Variance, Standard DeviationCielo DimayugaNo ratings yet

- Statistics and Probability Module 2Document3 pagesStatistics and Probability Module 2Cielo DimayugaNo ratings yet

- Chapter 3 Part 3Document30 pagesChapter 3 Part 3Aditya GhoshNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Practice 3Document4 pagesPractice 3bo chian chynNo ratings yet

- Practice 1Document3 pagesPractice 1bo chian chynNo ratings yet

- Investment Utility and Expected ReturnsDocument1 pageInvestment Utility and Expected Returnsbo chian chynNo ratings yet

- Fund Performance Measures X YDocument1 pageFund Performance Measures X Ybo chian chynNo ratings yet

- Inverse Trigo and Functions BansalDocument28 pagesInverse Trigo and Functions BansalYagyank ChadhaNo ratings yet

- Theosophical Quarterly v23 1925-1926Document424 pagesTheosophical Quarterly v23 1925-1926Joma SipeNo ratings yet

- Panasonic Phone System KXT308Document6 pagesPanasonic Phone System KXT308Kellie CroftNo ratings yet

- Evolution of Crops - D.Tay-2Document27 pagesEvolution of Crops - D.Tay-2liam peinNo ratings yet

- Fabric in ArchitectureDocument28 pagesFabric in ArchitecturesubalakshmiNo ratings yet

- Ficha Tecnica SpikaDocument2 pagesFicha Tecnica SpikaJosé Luis RubioNo ratings yet

- Career PlanDocument1 pageCareer Planapi-367263216No ratings yet

- Curriculum Vitae Eldy PDFDocument2 pagesCurriculum Vitae Eldy PDFFaza InsanNo ratings yet

- First Principle Applications in RoRo-Ship Design PDFDocument7 pagesFirst Principle Applications in RoRo-Ship Design PDFFerdy Fer DNo ratings yet

- Nakshatra Revati: According To Prash TrivediDocument8 pagesNakshatra Revati: According To Prash TrivediazzxdNo ratings yet

- Ophelia SyndromeDocument10 pagesOphelia SyndromeJulioroncal100% (1)

- Aplac TR 001 Issue 2Document48 pagesAplac TR 001 Issue 2gaunananguyenNo ratings yet

- Alexandrite: Structural & Mechanical PropertiesDocument2 pagesAlexandrite: Structural & Mechanical PropertiesalifardsamiraNo ratings yet

- Study PDFDocument10 pagesStudy PDFDaniel Cano QuinteroNo ratings yet

- Urban Form FactorsDocument56 pagesUrban Form FactorsEarl Schervin CalaguiNo ratings yet

- University of Oxford, Financial Statements 2017-2018 PDFDocument120 pagesUniversity of Oxford, Financial Statements 2017-2018 PDFRano Digdayan MNo ratings yet

- Assignment 1 Gene30Document7 pagesAssignment 1 Gene30api-533399249No ratings yet

- 21b Text PDFDocument47 pages21b Text PDFyoeluruNo ratings yet

- Selection and Characterisation of The Predominant Lactobacillus Species As A Starter Culture in The Preparation of Kocho, Fermented Food From EnsetDocument12 pagesSelection and Characterisation of The Predominant Lactobacillus Species As A Starter Culture in The Preparation of Kocho, Fermented Food From EnsetHelen WeldemichaelNo ratings yet

- Notes From - The Midnight LibraryDocument10 pagesNotes From - The Midnight LibrarySiddharth ToshniwalNo ratings yet

- Care Sheet - Halloween CrabsDocument2 pagesCare Sheet - Halloween CrabsJohn GamesbyNo ratings yet

- Introduction To Psychological Assessment and PsychodiagnosisDocument75 pagesIntroduction To Psychological Assessment and PsychodiagnosisNishesh AcharyaNo ratings yet

- Helve Tic ADocument9 pagesHelve Tic AwemeihNo ratings yet

- Arguments in Ordinary LanguageDocument5 pagesArguments in Ordinary LanguageStephanie Reyes GoNo ratings yet

- D/S Dokmoka LoringthepiDocument1 pageD/S Dokmoka LoringthepiManupriya KapleshNo ratings yet

- Mosfet 100 VoltDocument9 pagesMosfet 100 Voltnithinmundackal3623No ratings yet

- TSO C69bDocument28 pagesTSO C69btotololo78No ratings yet

- Pakistan Exams Cie o A Reg Form Oct09Document13 pagesPakistan Exams Cie o A Reg Form Oct09shamsulzamanNo ratings yet

- De Bono 6 Action Shoesdoc - CompressDocument12 pagesDe Bono 6 Action Shoesdoc - CompressHazel RománNo ratings yet

- IMP Workshop ManualDocument336 pagesIMP Workshop Manualsyllavethyjim67% (3)