You might also like

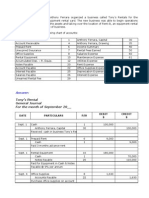

- Tony's Rentals General Journal For September 20Document17 pagesTony's Rentals General Journal For September 20Rehan Mehmood63% (8)

- Betty's Balloon Boutique - AnswerDocument5 pagesBetty's Balloon Boutique - AnswerMG Moana100% (1)

- Bank Statment Wells FargoDocument7 pagesBank Statment Wells FargoYu ShilohNo ratings yet

- Valued Added TaxDocument5 pagesValued Added TaxCharles Reginald K. Hwang100% (6)

- Fundamentals of Accountancy, Business and Management 1 (FABM 1)Document12 pagesFundamentals of Accountancy, Business and Management 1 (FABM 1)trek boiNo ratings yet

- Computing Gross Taxable Income and Tax DueDocument21 pagesComputing Gross Taxable Income and Tax DuepearlNo ratings yet

- 12ENTREP Q2 Module 8 Terminal Report of Business OperationsDocument10 pages12ENTREP Q2 Module 8 Terminal Report of Business OperationsJM Almaden AbadNo ratings yet

- G12 Buss Finance W4 LASDocument18 pagesG12 Buss Finance W4 LASEvelyn DeliquinaNo ratings yet

- Business Finance12 Q3 M4Document20 pagesBusiness Finance12 Q3 M4Chriztal TejadaNo ratings yet

- Grade11 Fabm1 Q2 Week6Document19 pagesGrade11 Fabm1 Q2 Week6Mickaela MonterolaNo ratings yet

- Fabm 2: Quarter 3 - Module 2 Statement of Comprehensive Income For Service & Merchandising BusinessDocument23 pagesFabm 2: Quarter 3 - Module 2 Statement of Comprehensive Income For Service & Merchandising BusinessMaria Nikka GarciaNo ratings yet

- Senior High School: Organization & Management Quarter IIDocument12 pagesSenior High School: Organization & Management Quarter IICipher Amoz100% (1)

- Melc Grade 12 Abm1Document4 pagesMelc Grade 12 Abm1Neniel DumanjogNo ratings yet

- QA SIPACKS in Business Finance Q3 W1 7Document91 pagesQA SIPACKS in Business Finance Q3 W1 7Roan DiracoNo ratings yet

- Apply Business Math in Water Refilling StationDocument22 pagesApply Business Math in Water Refilling StationsdfdsfNo ratings yet

- 4th FABM 2Document2 pages4th FABM 2Keisha MarieNo ratings yet

- Gen005 - Quiz 3 Answer KeyDocument3 pagesGen005 - Quiz 3 Answer KeyELLE WOODSNo ratings yet

- Fundamentals of ABM1 - Q4 - LAS2 DRAFTDocument10 pagesFundamentals of ABM1 - Q4 - LAS2 DRAFTSitti Halima Amilbahar AdgesNo ratings yet

- Organization and Management Grade 11, Quarter 2, Week 8: Weekly Learning Activity SheetDocument8 pagesOrganization and Management Grade 11, Quarter 2, Week 8: Weekly Learning Activity SheetJessebel Dano AnthonyNo ratings yet

- SHS ABM BF Q1 Mod-11 RISK-RETURN-TRADE-OFF FINAL-1Document11 pagesSHS ABM BF Q1 Mod-11 RISK-RETURN-TRADE-OFF FINAL-1Kimberly LagmanNo ratings yet

- Module Abm1 FinalDocument69 pagesModule Abm1 FinalLANY T. CATAMINNo ratings yet

- Math 12-ABM BESR-Q2-Week-6Document14 pagesMath 12-ABM BESR-Q2-Week-6Jomar BenedicoNo ratings yet

- FABM2 1st QTR Exam (2022)Document2 pagesFABM2 1st QTR Exam (2022)Noel CalicdanNo ratings yet

- Fourth Quarter Week 3 and Week 4 Module in Business FinanceDocument15 pagesFourth Quarter Week 3 and Week 4 Module in Business FinanceRojane L. AlcantaraNo ratings yet

- Lesson 11 Income and Business TaxationDocument51 pagesLesson 11 Income and Business TaxationGelai BatadNo ratings yet

- FABM2 Q2 Mod10Document16 pagesFABM2 Q2 Mod10Fretty Mae AbuboNo ratings yet

- Fabm2 Law q1 Week 1 To 9Document21 pagesFabm2 Law q1 Week 1 To 9Karen, Togeno CabusNo ratings yet

- Las q2 Fabm 2 Week 4Document10 pagesLas q2 Fabm 2 Week 4Mahika BatumbakalNo ratings yet

- FABM2 Module 7 SLMDocument30 pagesFABM2 Module 7 SLMMarjeanetteAgpaoaReyesNo ratings yet

- Philippine High School Weekly Learning PlanDocument3 pagesPhilippine High School Weekly Learning PlanJessie Rose Tamayo100% (1)

- MODULE 09 FABM2 Bank ReconciliationDocument9 pagesMODULE 09 FABM2 Bank ReconciliationJm JuanillasNo ratings yet

- Business Mathematics: Quarter 2, Week 8 - Module 16: Kinds of Graph and Its PartDocument17 pagesBusiness Mathematics: Quarter 2, Week 8 - Module 16: Kinds of Graph and Its Partkurlstine joanne aceronNo ratings yet

- Business Finance Module Week1 6Document80 pagesBusiness Finance Module Week1 6Stefany SorianoNo ratings yet

- (FABM1) Module 2 Accounting Concepts and PrinciplesDocument8 pages(FABM1) Module 2 Accounting Concepts and PrinciplesYvonne Alyanna LunaNo ratings yet

- Fundamentals of ABM2 NADocument45 pagesFundamentals of ABM2 NASheena DumayNo ratings yet

- JpegDocument15 pagesJpegMae Joy EscanillasNo ratings yet

- Business Finance: Basic Long-Term Financial ConceptsDocument29 pagesBusiness Finance: Basic Long-Term Financial ConceptsJanna GunioNo ratings yet

- Fabm1 Summative ExamDocument8 pagesFabm1 Summative ExamAbegail PanangNo ratings yet

- Financial Statement Analysis Part 2Document10 pagesFinancial Statement Analysis Part 2Kim Patrick VictoriaNo ratings yet

- HandoutsDocument2 pagesHandoutsJoshuaMolinoPanambitanNo ratings yet

- School Business Organization TypesDocument5 pagesSchool Business Organization TypesMarilyn Nelmida TamayoNo ratings yet

- Merchandising QuizzerDocument1 pageMerchandising QuizzerjadeNo ratings yet

- Acc106 Rubrics For Assignment - For Student RefDocument2 pagesAcc106 Rubrics For Assignment - For Student RefItik BerendamNo ratings yet

- Chapter 07Document23 pagesChapter 07Liko Pah TuafNo ratings yet

- Abm Fidp 2023Document9 pagesAbm Fidp 2023Ms. Jhallaine MauricioNo ratings yet

- Weekly Home Learning Plan Fabm1Document2 pagesWeekly Home Learning Plan Fabm1Charly Mint Atamosa Israel100% (2)

- Daily-Lesson LogDocument3 pagesDaily-Lesson LogFaith Tulmo De Dios100% (1)

- Adjusting EntriesDocument35 pagesAdjusting EntriesEliyah CalucagNo ratings yet

- Bank ReconcilationDocument9 pagesBank ReconcilationJohnpaul FloranzaNo ratings yet

- Fundamentals of Accountancy, Business and Management IIDocument12 pagesFundamentals of Accountancy, Business and Management IILee Arne BarayugaNo ratings yet

- Statement of Changes in EquityDocument4 pagesStatement of Changes in EquityWella LozadaNo ratings yet

- Business Finance: Quarter 3 - Module 3: Sources and Uses of Short-Term and Long-Term FundsDocument19 pagesBusiness Finance: Quarter 3 - Module 3: Sources and Uses of Short-Term and Long-Term FundsDENNIS AUJERONo ratings yet

- PDF Teaching Guide Business Ethics and Social Responsibility Module - CompressDocument34 pagesPDF Teaching Guide Business Ethics and Social Responsibility Module - CompressSAMSON ALBERT SALASNo ratings yet

- Organization and Management Essentials for Effective Business PlanningDocument13 pagesOrganization and Management Essentials for Effective Business PlanningJaslor LavinaNo ratings yet

- Quiz and Performance Tasks For 2nd QTR 21 22Document22 pagesQuiz and Performance Tasks For 2nd QTR 21 22Cipher Amoz100% (1)

- Detailed Lesson Plan in Fundamentals of AccountancyDocument5 pagesDetailed Lesson Plan in Fundamentals of AccountancyKrisha Joy CofinoNo ratings yet

- FUNDAMENTALS OF ABM1, Q2-WEEKS 3 & 4 FinalDocument17 pagesFUNDAMENTALS OF ABM1, Q2-WEEKS 3 & 4 FinalMichelJoy De GuzmanNo ratings yet

- Accounting Cycle of A Service Business-ExerciseDocument50 pagesAccounting Cycle of A Service Business-ExerciseHannah GarciaNo ratings yet

- 3 RdquarterDocument7 pages3 RdquarterRylan Yani OlshpNo ratings yet

- BusinessFinance12 Q2 Mod1 Type-of-Investments V5Document20 pagesBusinessFinance12 Q2 Mod1 Type-of-Investments V5Anna May Serador CamachoNo ratings yet

- Adjusting Entries Company A ExercisesDocument19 pagesAdjusting Entries Company A ExercisesRodolfo CorpuzNo ratings yet

- Work Immersion Portfolio RubricDocument2 pagesWork Immersion Portfolio RubricRomeo Pilongo100% (1)

- Fabm2 - Q2 - M5Document13 pagesFabm2 - Q2 - M5Christopher AbundoNo ratings yet

- Kanban SizingDocument102 pagesKanban Sizingsribalaji22No ratings yet

- Bank StatmentDocument28 pagesBank Statmentmanish.singh655No ratings yet

- Supply Chain Management - DR V K GuptaDocument9 pagesSupply Chain Management - DR V K GuptacgvcNo ratings yet

- Reviewer For PrelimsDocument6 pagesReviewer For PrelimsJerric CristobalNo ratings yet

- PT. HOT & COLD JURNAL PEMBELIAN DESEMBER 2017Document21 pagesPT. HOT & COLD JURNAL PEMBELIAN DESEMBER 2017Epon NopiantiNo ratings yet

- Brant Freezer Company warehouse performance analysisDocument3 pagesBrant Freezer Company warehouse performance analysisThanh MaiNo ratings yet

- Week 03 - Bank ReconciliationDocument6 pagesWeek 03 - Bank ReconciliationPj ManezNo ratings yet

- Managerial MidtermDocument6 pagesManagerial MidtermIqtidar KhanNo ratings yet

- Copy Alaska Usa Federal Credit Union Statement of AccountDocument37 pagesCopy Alaska Usa Federal Credit Union Statement of AccountВлад АнгелNo ratings yet

- Chapter 01 - DayagDocument16 pagesChapter 01 - DayagPrincessAngelaDeLeon80% (5)

- Supply Chain Strategy in <40 CharactersDocument17 pagesSupply Chain Strategy in <40 CharactersNiña AlfonsoNo ratings yet

- SMCH 05Document73 pagesSMCH 05FratFool100% (1)

- Xacc280 Week3 Reading2Document56 pagesXacc280 Week3 Reading2osharpening9402No ratings yet

- Association of Chartered Certified Accountants Multiple Choice Questions - Paper 1.1Document24 pagesAssociation of Chartered Certified Accountants Multiple Choice Questions - Paper 1.1tahahameed55No ratings yet

- BULATS Standard Test SampleDocument36 pagesBULATS Standard Test SampleThảo Uyên100% (2)

- Exer 1Document15 pagesExer 1Kim OlimbaNo ratings yet

- Account Title Unadjusted Trial Balance Adjustments Adjusted Trial Balance Debit Credit Debit Credit DebitDocument15 pagesAccount Title Unadjusted Trial Balance Adjustments Adjusted Trial Balance Debit Credit Debit Credit DebitTwins VinesNo ratings yet

- 654475993949_e-StatementBRImo_042301005930531_Feb2024_20240301_121426Document3 pages654475993949_e-StatementBRImo_042301005930531_Feb2024_20240301_121426Muhammad Awaludin HasanNo ratings yet

- Rci Bub, 2019Document143 pagesRci Bub, 2019Robert AbelaNo ratings yet

- N CY5 DAwg 4 GQSJ JQuDocument12 pagesN CY5 DAwg 4 GQSJ JQuVinod SharmaNo ratings yet

- Usaa Receipt Sharecd7bcc1f 3817 4d83 Bae5 Bdb429ce1a15Document12 pagesUsaa Receipt Sharecd7bcc1f 3817 4d83 Bae5 Bdb429ce1a15Rohan DuncanNo ratings yet

- Solution Chapter 15Document32 pagesSolution Chapter 15xxxxxxxxx75% (4)

- AccountingDocument19 pagesAccountinggigigiNo ratings yet

- Advance 1Document7 pagesAdvance 1Diana Faye CaduadaNo ratings yet

- Presentation - John LangleyDocument30 pagesPresentation - John LangleyReza GholamiNo ratings yet

- Solution Chapter 15Document33 pagesSolution Chapter 15Sy Him82% (11)

- G_L Register (4)Document18 pagesG_L Register (4)emerzuzonNo ratings yet