You might also like

- Norah Jones PDFDocument2 pagesNorah Jones PDFJuanJoseHerreraBerrio100% (4)

- Goodweek Tires Case Study EBIT ProjectionsDocument4 pagesGoodweek Tires Case Study EBIT ProjectionsEfri DwiyantoNo ratings yet

- Chapter 13 MK 2Document5 pagesChapter 13 MK 2Novelda100% (1)

- Track Software's Financial Performance in 2015Document8 pagesTrack Software's Financial Performance in 2015devanmadeNo ratings yet

- Precast FactoryDocument25 pagesPrecast Factoryamirsh78No ratings yet

- Capital Structure of ENCANADocument6 pagesCapital Structure of ENCANAsujata shahNo ratings yet

- Plate 2Document9 pagesPlate 2MichaelViloria0% (1)

- Mid Term Exam MCQs For 5530Document6 pagesMid Term Exam MCQs For 5530Amy WangNo ratings yet

- Policy and investment guidelines for financial objectivesDocument5 pagesPolicy and investment guidelines for financial objectivesavi dotto100% (1)

- The Investment DetectiveDocument9 pagesThe Investment DetectiveFadhila Nurfida HanifNo ratings yet

- 08 - Chapter 8Document71 pages08 - Chapter 8hunkieNo ratings yet

- Motion To Release Cash Bail BondDocument1 pageMotion To Release Cash Bail BondJamie Tiu100% (2)

- MENG 6502 Financial ratios analysisDocument6 pagesMENG 6502 Financial ratios analysisruss jhingoorieNo ratings yet

- Latin Quotess..Document554 pagesLatin Quotess..donikaNo ratings yet

- THE WHITE SANDS INCIDENT by Daniel Fry Forward by Lucus LouizeDocument72 pagesTHE WHITE SANDS INCIDENT by Daniel Fry Forward by Lucus LouizeLib100% (4)

- Case PPA (SMART) - QuestionDocument9 pagesCase PPA (SMART) - QuestionSekar WiridianaNo ratings yet

- Kota Fibres Case Study: Improving Cash Flow Through Operational ChangesDocument4 pagesKota Fibres Case Study: Improving Cash Flow Through Operational ChangesZhijian HuangNo ratings yet

- Supreme Court of the Philippines upholds constitutionality of Act No. 2886Document338 pagesSupreme Court of the Philippines upholds constitutionality of Act No. 2886OlenFuerteNo ratings yet

- Calveta's Core Values Drive SuccessDocument11 pagesCalveta's Core Values Drive SuccessKartik SharmaNo ratings yet

- Agency Trust & Partnership ReviewerDocument8 pagesAgency Trust & Partnership ReviewerKfMaeAseronNo ratings yet

- Ventures Onsite Market Awards 22062023 64935868dDocument163 pagesVentures Onsite Market Awards 22062023 64935868dhamzarababa21No ratings yet

- Group Task - Investment Detective - Syndicate 2.Xlsx - Sheet1Document2 pagesGroup Task - Investment Detective - Syndicate 2.Xlsx - Sheet1jibrildewantaraNo ratings yet

- Northern Forest ProductsDocument15 pagesNorthern Forest ProductsHương Lan TrịnhNo ratings yet

- Duration GAP analysis: Measuring interest rate riskDocument5 pagesDuration GAP analysis: Measuring interest rate riskShubhash ShresthaNo ratings yet

- Case Study 1Document3 pagesCase Study 1asuvaniNo ratings yet

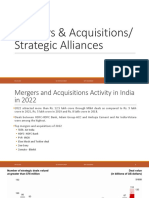

- Mergers Acquisitions and Strategic Alliances - ClassDocument69 pagesMergers Acquisitions and Strategic Alliances - ClassKartik SharmaNo ratings yet

- APO Group-6 Calveta Dining Services IncDocument10 pagesAPO Group-6 Calveta Dining Services IncKartik SharmaNo ratings yet

- SWOT On Philippine Port StateDocument7 pagesSWOT On Philippine Port StateLourisa LorenNo ratings yet

- Case Digests on Violations of Canons 16-18 of the Code of Professional ResponsibilityDocument4 pagesCase Digests on Violations of Canons 16-18 of the Code of Professional ResponsibilityRosana Villordon SoliteNo ratings yet

- Marine CorpDocument11 pagesMarine CorpYazlin Yusof100% (1)

- Jurisdiction definedDocument30 pagesJurisdiction definedJeong100% (1)

- Oasis Hong Kong Case FinalDocument58 pagesOasis Hong Kong Case FinalAtika Siti AminahNo ratings yet

- Final Gitman - pmf13 - PPT 07 GE Stock Valuation To 50Document51 pagesFinal Gitman - pmf13 - PPT 07 GE Stock Valuation To 50asimNo ratings yet

- Appendix - 8A The Maturity ModelDocument10 pagesAppendix - 8A The Maturity ModelAndreea IoanaNo ratings yet

- Fin516 Week5 HW ScribdDocument2 pagesFin516 Week5 HW ScribdmsspellaNo ratings yet

- Neogi Chemical CoDocument10 pagesNeogi Chemical Codpu_bansal83241No ratings yet

- M12 Titman 2544318 11 FinMgt C12Document80 pagesM12 Titman 2544318 11 FinMgt C12marjsbarsNo ratings yet

- TN38 Primus Automation Division 2002Document11 pagesTN38 Primus Automation Division 2002mylittle_pg100% (1)

- Csae Study of FMDocument4 pagesCsae Study of FMAbdul Saqib17% (6)

- Assignment (Management)Document18 pagesAssignment (Management)RSNo ratings yet

- Enhanced cash flow analysis of replacement printing pressesDocument37 pagesEnhanced cash flow analysis of replacement printing pressesRiangelli Exconde100% (1)

- Investment Detective CaseDocument1 pageInvestment Detective CaseJonathan ZhaoNo ratings yet

- Dessler 03Document13 pagesDessler 03Yose DjaluwarsaNo ratings yet

- FICT System Development & Analysis AssignmentDocument3 pagesFICT System Development & Analysis AssignmentCR7 الظاهرةNo ratings yet

- Watawala Plantations PLC Annual Report 2018/19 HighlightsDocument184 pagesWatawala Plantations PLC Annual Report 2018/19 HighlightsThilinaAbhayarathneNo ratings yet

- Financial Statements: Analysis of Attock Refinery LimitedDocument1 pageFinancial Statements: Analysis of Attock Refinery LimitedHasnain KharNo ratings yet

- Calculating IRR Through Fake Payback Period MethodDocument9 pagesCalculating IRR Through Fake Payback Period Methodakshit_vij0% (1)

- Impact of Virtual Advertising in Sports EventsDocument19 pagesImpact of Virtual Advertising in Sports EventsRonak BhandariNo ratings yet

- CC2 - The Financial Detective, 2005Document4 pagesCC2 - The Financial Detective, 2005Aldren Delina RiveraNo ratings yet

- Case Study - Nilgai Foods: Positioning Packaged Coconut Water in India (Cocofly)Document6 pagesCase Study - Nilgai Foods: Positioning Packaged Coconut Water in India (Cocofly)prathmesh kulkarniNo ratings yet

- Hitungan Kuis 6 Bethesda Mining CompanyDocument6 pagesHitungan Kuis 6 Bethesda Mining Companyrica100% (1)

- Swati Anand - FRMcaseDocument5 pagesSwati Anand - FRMcaseBhavin MohiteNo ratings yet

- Asset Quality Management in BankDocument13 pagesAsset Quality Management in Bankswendadsilva100% (4)

- Solved - United Technologies Corporation (UTC), Based in Hartfor...Document4 pagesSolved - United Technologies Corporation (UTC), Based in Hartfor...Saad ShafiqNo ratings yet

- Koehl's Doll Shop Cash Budget and Loan RequirementsDocument3 pagesKoehl's Doll Shop Cash Budget and Loan Requirementsmobinil1No ratings yet

- Cost of Capital (Ch-3)Document26 pagesCost of Capital (Ch-3)Neha SinghNo ratings yet

- Corporate Level Strategy - Types and ExamplesDocument21 pagesCorporate Level Strategy - Types and ExamplesSuraj RajbharNo ratings yet

- Ebit Eps AnalysisDocument11 pagesEbit Eps Analysismanish9890No ratings yet

- Mirr NotesDocument5 pagesMirr NotesSitaKumariNo ratings yet

- Working Capital Management in Reliance Industries LimitedDocument5 pagesWorking Capital Management in Reliance Industries LimitedVurdalack666No ratings yet

- Unit 2 Capital StructureDocument27 pagesUnit 2 Capital StructureNeha RastogiNo ratings yet

- Lesson 5 Tax Planning With Reference To Capital StructureDocument37 pagesLesson 5 Tax Planning With Reference To Capital StructurekelvinNo ratings yet

- Financial Ratios NestleDocument23 pagesFinancial Ratios NestleSehrash SashaNo ratings yet

- Syndicate 1 Nike Cost of Capital FinalDocument2 pagesSyndicate 1 Nike Cost of Capital FinalirfanmuafiNo ratings yet

- Goldstar Example of Ratio AnalysisDocument13 pagesGoldstar Example of Ratio AnalysisRoshan SomaruNo ratings yet

- Shell PakistanDocument92 pagesShell Pakistantalhagujjar2No ratings yet

- This Study Resource Was: Problem 5Document3 pagesThis Study Resource Was: Problem 5Hasan SikderNo ratings yet

- Businessstrategyandcorporateculture 111128195955 Phpapp01Document52 pagesBusinessstrategyandcorporateculture 111128195955 Phpapp01richierismyNo ratings yet

- Schneider Electric Case Study:: Accelerating Global Digital Platform Deployment Using The CloudDocument8 pagesSchneider Electric Case Study:: Accelerating Global Digital Platform Deployment Using The CloudAjaySon678100% (1)

- Financial Statement ManipulationDocument10 pagesFinancial Statement Manipulationssimi137No ratings yet

- Fundamental of FinanceDocument195 pagesFundamental of FinanceMillad MusaniNo ratings yet

- Case Study: Ratios and Financial Planning at S&S AirDocument4 pagesCase Study: Ratios and Financial Planning at S&S AirAstha GoplaniNo ratings yet

- Example 4Document3 pagesExample 4dimash209100% (1)

- Project Cash Flow AnalysisDocument8 pagesProject Cash Flow AnalysisIkhaa AlbashNo ratings yet

- Analyze capital budgeting projects to rank top four investmentsDocument34 pagesAnalyze capital budgeting projects to rank top four investmentsAdnan AliNo ratings yet

- Sales Distribution Channel: 24 February 2023Document50 pagesSales Distribution Channel: 24 February 2023Kartik SharmaNo ratings yet

- IMT Ghaziabad - Ujjawal - 18.02.23Document28 pagesIMT Ghaziabad - Ujjawal - 18.02.23Kartik SharmaNo ratings yet

- Business Strategies - ClassDocument38 pagesBusiness Strategies - ClassKartik SharmaNo ratings yet

- Vision and MissionDocument22 pagesVision and MissionKartik SharmaNo ratings yet

- Session 16Document10 pagesSession 16Kartik SharmaNo ratings yet

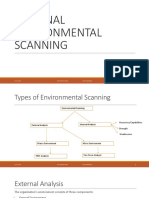

- External Environment Analysis - ClassDocument20 pagesExternal Environment Analysis - ClassKartik SharmaNo ratings yet

- Hygiene QuestionsDocument1 pageHygiene QuestionsAnkitaNo ratings yet

- ForecastingDocument40 pagesForecastingKartik SharmaNo ratings yet

- Targeting Plumbers and Developers for Aqualisa Shower SalesDocument13 pagesTargeting Plumbers and Developers for Aqualisa Shower SalesKartik SharmaNo ratings yet

- Innovation Types and Life Cycle StagesDocument25 pagesInnovation Types and Life Cycle StagesKartik SharmaNo ratings yet

- Corporate Strategy Questions AnsweredDocument33 pagesCorporate Strategy Questions AnsweredKartik SharmaNo ratings yet

- Calculate NPV, IRR, and more for 7 investment projectsDocument12 pagesCalculate NPV, IRR, and more for 7 investment projectsKartik SharmaNo ratings yet

- Role of Management Information System in Tata MotorsDocument13 pagesRole of Management Information System in Tata MotorsKartik SharmaNo ratings yet

- Project Work: Sales & Distribution ManagementDocument24 pagesProject Work: Sales & Distribution Managementraavi84187% (15)

- Aqualisa Case QuestionsDocument3 pagesAqualisa Case Questionspunksta18250% (2)

- Indian Contract Act Key Elements (35Document48 pagesIndian Contract Act Key Elements (35Kartik SharmaNo ratings yet

- Statement of Cash FlowsDocument2 pagesStatement of Cash FlowsKartik SharmaNo ratings yet

- Aqualisa 3rd QuesDocument1 pageAqualisa 3rd QuesKartik SharmaNo ratings yet

- Day 8Document48 pagesDay 8Kartik SharmaNo ratings yet

- Day 7Document33 pagesDay 7Kartik SharmaNo ratings yet

- IoT Lab Task-2Document4 pagesIoT Lab Task-2Kartik SharmaNo ratings yet

- Tata Consumer Products' Genesis and Journey So FarDocument39 pagesTata Consumer Products' Genesis and Journey So FarKartik SharmaNo ratings yet

- Baseband Formatting TechniquesDocument89 pagesBaseband Formatting TechniquesKartik SharmaNo ratings yet

- Indian Contract Act II RecapDocument47 pagesIndian Contract Act II RecapKartik SharmaNo ratings yet

- TARPDA5Document7 pagesTARPDA5Kartik SharmaNo ratings yet

- 18bec0140 VL2020210106999 Ast06Document13 pages18bec0140 VL2020210106999 Ast06Kartik SharmaNo ratings yet

- London Stock ExchangeDocument15 pagesLondon Stock ExchangeZakaria Abdullahi MohamedNo ratings yet

- Ticket(s) Issued : Flight DetailsDocument2 pagesTicket(s) Issued : Flight DetailswinstevenrayNo ratings yet

- The Sun Invincible: Timothy J. O'Neill, FRCDocument4 pagesThe Sun Invincible: Timothy J. O'Neill, FRCC UidNo ratings yet

- View - Print Submitted Form PassportDocument2 pagesView - Print Submitted Form PassportRAMESH LAISHETTYNo ratings yet

- Vietnamese Rice Certificate DetailsDocument2 pagesVietnamese Rice Certificate DetailsNguyễn Thị Trà My100% (1)

- Chap 012Document36 pagesChap 012Shailesh VishvakarmaNo ratings yet

- Basic Finance Module Materials List of Modules: No. Module Title CodeDocument49 pagesBasic Finance Module Materials List of Modules: No. Module Title CodeShaina LimNo ratings yet

- Removing Resigned Employees From SSS, Philhealth, Pag-Ibig, BirDocument3 pagesRemoving Resigned Employees From SSS, Philhealth, Pag-Ibig, BirAlthea Marie AlmadenNo ratings yet

- ITC: Building World-Class Brands For IndiaDocument24 pagesITC: Building World-Class Brands For IndiaVinay GhuwalewalaNo ratings yet

- FS Pimlico: Information GuideDocument11 pagesFS Pimlico: Information GuideGemma gladeNo ratings yet

- Mrs. Pringle's Dinner Party ChaosDocument30 pagesMrs. Pringle's Dinner Party ChaosMatet Recabo MataquelNo ratings yet

- HOLIDAYS IN JAPAN PointersDocument2 pagesHOLIDAYS IN JAPAN PointersAyaNo ratings yet

- New Customer? Start Here.: The Alchemical Body: Siddha Traditions in Medieval India by David Gordon WhiteDocument2 pagesNew Customer? Start Here.: The Alchemical Body: Siddha Traditions in Medieval India by David Gordon WhiteBala Ratnakar KoneruNo ratings yet

- Article Practive Sheet LatestDocument3 pagesArticle Practive Sheet LatestNahian NishargoNo ratings yet

- Syllabus+ +Obligations+and+ContractsDocument10 pagesSyllabus+ +Obligations+and+ContractsEmman KailanganNo ratings yet

- Chapter 1 IntroductionDocument60 pagesChapter 1 IntroductionAndrew Charles HendricksNo ratings yet

- NDMC vs Prominent Hotels Limited Delhi High Court Judgement on Licence Fee DisputeDocument84 pagesNDMC vs Prominent Hotels Limited Delhi High Court Judgement on Licence Fee DisputeDeepak SharmaNo ratings yet

- Attitude StrengthDocument3 pagesAttitude StrengthJoanneVivienSardinoBelderolNo ratings yet