You might also like

- quản trị mar - MOMODocument32 pagesquản trị mar - MOMONguyễn Phương UyênNo ratings yet

- Paytm Case StudyDocument11 pagesPaytm Case StudyShriraj BamneNo ratings yet

- Banks Digital Wallet WhitepaperDocument9 pagesBanks Digital Wallet Whitepaperchandro2007No ratings yet

- Vietnam FinTech Challenge PDFDocument6 pagesVietnam FinTech Challenge PDFVarun MittalNo ratings yet

- Final Nike CaseDocument15 pagesFinal Nike Casehimanshu sahuNo ratings yet

- Nike Vs AdidasDocument4 pagesNike Vs AdidasKlim TurovNo ratings yet

- PMk-T222WSB-2 - Group 1 - VietravelDocument28 pagesPMk-T222WSB-2 - Group 1 - VietravelThien Tri ViNo ratings yet

- Shopee Report - Consumer Behaviour - Group1Document43 pagesShopee Report - Consumer Behaviour - Group1Phuong NghiNo ratings yet

- E-Banking in MoroccoDocument21 pagesE-Banking in Moroccopse100% (1)

- Vietnam Mobile App Market Report 2018 enDocument60 pagesVietnam Mobile App Market Report 2018 enNhung NguyễnNo ratings yet

- One 97 Communications (ONE97 IN) : Too Many Fingers in Too Many PiesDocument56 pagesOne 97 Communications (ONE97 IN) : Too Many Fingers in Too Many PiesSubhro Sengupta100% (1)

- GrabAds Media KitDocument50 pagesGrabAds Media Kittuấn nghĩa nguyễnNo ratings yet

- QSM - USSH - NHÓM 1 - BÀI TẬP 1 - WORD PDFDocument17 pagesQSM - USSH - NHÓM 1 - BÀI TẬP 1 - WORD PDFLinh Nguyen PhuongNo ratings yet

- Fintech Vietnam PDFDocument31 pagesFintech Vietnam PDFLinh Le0% (1)

- Analysis of Canifa'S Marketing Price Policy and Recommendations To Improve Canifa'S Marketing ActivitiesDocument12 pagesAnalysis of Canifa'S Marketing Price Policy and Recommendations To Improve Canifa'S Marketing Activitieshdrth wft100% (1)

- Case Study of Baemin: I/ Base InformationDocument4 pagesCase Study of Baemin: I/ Base InformationJupter NguyễnNo ratings yet

- Public Relation Report: Go-Viet - Increase Brand's AwarenessDocument24 pagesPublic Relation Report: Go-Viet - Increase Brand's AwarenessCyn NguyenNo ratings yet

- Xiaomi Vs Samsung: Marketing Strategies Used in IndiaDocument4 pagesXiaomi Vs Samsung: Marketing Strategies Used in IndiaAlexNo ratings yet

- The Perfect Payment Partner What Merchants Are Looking For From Their PSPs Banking CircleDocument13 pagesThe Perfect Payment Partner What Merchants Are Looking For From Their PSPs Banking CircleRemA YahyaNo ratings yet

- Attitude Towards Drone Food Delivery Services-Role of Innovativeness, Perceived Risk, and Green ImageDocument19 pagesAttitude Towards Drone Food Delivery Services-Role of Innovativeness, Perceived Risk, and Green ImageStella CruzNo ratings yet

- Case Study: Redbus - in - Automating The Bus Travel IndustryDocument3 pagesCase Study: Redbus - in - Automating The Bus Travel IndustryAnand Singh ThakurNo ratings yet

- Bank Neo Commerce: Quickly Scaling UpDocument23 pagesBank Neo Commerce: Quickly Scaling UpAgus SuwarnoNo ratings yet

- Cashify Whitepaper 2020Document28 pagesCashify Whitepaper 2020poorawsiasNo ratings yet

- What Microenvironmental Factors Have Affected Fitbit Since It Opened For Business?Document4 pagesWhat Microenvironmental Factors Have Affected Fitbit Since It Opened For Business?Ubl HrNo ratings yet

- Product Playbook: Who We Are What We Offer How We Can Help MoreDocument34 pagesProduct Playbook: Who We Are What We Offer How We Can Help Morecadesmas techNo ratings yet

- Apollo Tyres CFA ChallengeDocument15 pagesApollo Tyres CFA ChallengeChetanNo ratings yet

- Xiaomi and Huawei ReportDocument2 pagesXiaomi and Huawei ReportSaqib LiaqatNo ratings yet

- State of India Fintech 1694501298Document60 pagesState of India Fintech 1694501298Onkar BhagatNo ratings yet

- Xiaomi Could It Disrupt India's Consumer Electronics MarketDocument13 pagesXiaomi Could It Disrupt India's Consumer Electronics MarketDiya ShahNo ratings yet

- Meesho (C) : Empowering India'S Women EntrepreneursDocument5 pagesMeesho (C) : Empowering India'S Women Entrepreneursrishabh mundhadaNo ratings yet

- CyberSource MPOS Android SDKDocument9 pagesCyberSource MPOS Android SDKSratixNo ratings yet

- Study Id45600 Statista Report FintechDocument142 pagesStudy Id45600 Statista Report FintechOlson Ortiz T.No ratings yet

- Nike and Adidas ArchitectureDocument9 pagesNike and Adidas Architecturefire dragonNo ratings yet

- Open The News Magazine First Edition March 2023Document9 pagesOpen The News Magazine First Edition March 2023Open The NewsNo ratings yet

- Cuvva:: Disrupting The Market For Car InsuranceDocument32 pagesCuvva:: Disrupting The Market For Car InsuranceAkash PayunNo ratings yet

- Fintech Vietnam Startups 151126150047 Lva1 App6891Document59 pagesFintech Vietnam Startups 151126150047 Lva1 App6891Anonymous 45z6m4eE7pNo ratings yet

- Company Failures ResourcesDocument86 pagesCompany Failures ResourcesMehar BhagatNo ratings yet

- 5 Industry and Competitor Analysis - JARD-Fall 2022Document43 pages5 Industry and Competitor Analysis - JARD-Fall 2022Troy CrooksNo ratings yet

- Mobile Payment Usage in Vietnam 2020 Asia Plus IncDocument22 pagesMobile Payment Usage in Vietnam 2020 Asia Plus IncNguyễn LongNo ratings yet

- Vijay Shekhar SharmaDocument21 pagesVijay Shekhar SharmaManan Chandarana100% (1)

- MRe Assignment 3Document23 pagesMRe Assignment 3Jin Bi KwonNo ratings yet

- Q CommerceDocument42 pagesQ CommerceChhavi KhandujaNo ratings yet

- Segasoft CaseDocument10 pagesSegasoft CaseSamrah QamarNo ratings yet

- International Business: Case Study 5 BEER For All: Sabmiller in MozambiqueDocument3 pagesInternational Business: Case Study 5 BEER For All: Sabmiller in Mozambiquesatyapal yadavNo ratings yet

- (POI) GoPay X Pesona SquareDocument16 pages(POI) GoPay X Pesona Squareagiriwanda100% (1)

- 30-07-2022-1659161461-7-IJBGM-2. Reviewed - IJBGM - An Overview - Impact of FinTech in Indian Banking SectorDocument4 pages30-07-2022-1659161461-7-IJBGM-2. Reviewed - IJBGM - An Overview - Impact of FinTech in Indian Banking Sectoriaset123No ratings yet

- Artificial Intelligencein Marketing FinalDocument7 pagesArtificial Intelligencein Marketing FinalGilang KemalNo ratings yet

- Study Id108684 Quick-CommerceDocument81 pagesStudy Id108684 Quick-CommerceJamal NicholsNo ratings yet

- PW Nike Metaverse CaseDocument21 pagesPW Nike Metaverse CaseGabriel Fojas VillorenteNo ratings yet

- ENGPR2022Document156 pagesENGPR2022Trader CatNo ratings yet

- Empowering New Business Innovation With PaymentsDocument19 pagesEmpowering New Business Innovation With PaymentstamlqNo ratings yet

- Emergence of Fintech CompaniesDocument23 pagesEmergence of Fintech CompaniesHIMANSHU RAWATNo ratings yet

- DoorDash Revenue and Usage Statistics (2021) - Business of AppsDocument6 pagesDoorDash Revenue and Usage Statistics (2021) - Business of AppsMarcos Moreira AlvesNo ratings yet

- Bda ProjectDocument19 pagesBda ProjectDevanshi RastogiNo ratings yet

- Pleasure Scooter CaseDocument25 pagesPleasure Scooter CaseKabeer KarnaniNo ratings yet

- Meta Bain Syncsea 2022Document88 pagesMeta Bain Syncsea 2022Gebakken Kibbeling100% (1)

- Competitive Analysis of MyntraDocument15 pagesCompetitive Analysis of MyntraSagnik AdhikaryNo ratings yet

- 2 Kim Prior - FinTechDocument54 pages2 Kim Prior - FinTechSai Charan TejaNo ratings yet

- Vietnam'S Fintech: Shor T Pre Se NtationDocument10 pagesVietnam'S Fintech: Shor T Pre Se NtationNgọcThủyNo ratings yet

- Doolhur 2013Document4 pagesDoolhur 2013bichodavidNo ratings yet

- Forreign Exchange Risks Management For Exporter and ImporterDocument3 pagesForreign Exchange Risks Management For Exporter and ImporterNguyễn Phương UyênNo ratings yet

- University of Ueh Business School Faculty of International Business - MarketingDocument17 pagesUniversity of Ueh Business School Faculty of International Business - MarketingNguyễn Phương UyênNo ratings yet

- QTM FinalDocument39 pagesQTM FinalNguyễn Phương UyênNo ratings yet

- Writing 3 Ex.9 Page. 71Document1 pageWriting 3 Ex.9 Page. 71Nguyễn Phương UyênNo ratings yet

- Digital Mar P2Document3 pagesDigital Mar P2Nguyễn Phương UyênNo ratings yet

- MCQs - Overview of MA and Cost ClassificationsDocument6 pagesMCQs - Overview of MA and Cost ClassificationsĐạt NguyễnNo ratings yet

- Tieu Luan Khoa Hoc Quan Tri (MS)Document26 pagesTieu Luan Khoa Hoc Quan Tri (MS)Nguyễn Phương UyênNo ratings yet

- Assignment - Phung Van HungDocument28 pagesAssignment - Phung Van HungNguyễn Phương UyênNo ratings yet

- Mar Can Ban FinalDocument2 pagesMar Can Ban FinalNguyễn Phương UyênNo ratings yet

- Group HW 8 12oct 9s1 Group ADocument1 pageGroup HW 8 12oct 9s1 Group ANguyễn Phương UyênNo ratings yet

- General Report For GSMDocument14 pagesGeneral Report For GSMNguyễn Phương UyênNo ratings yet

- BEDocument14 pagesBENguyễn Phương UyênNo ratings yet

- Sensitivity Report For Wyndor: 1. Using Excel SolverDocument2 pagesSensitivity Report For Wyndor: 1. Using Excel SolverNguyễn Phương UyênNo ratings yet

- Final ExamDocument3 pagesFinal ExamNguyễn Phương UyênNo ratings yet

- HOMEWORKDocument1 pageHOMEWORKNguyễn Phương UyênNo ratings yet

- Test Comparative - Superlative: Name NGUYỆT HÀ Gr4.1 SmartDocument3 pagesTest Comparative - Superlative: Name NGUYỆT HÀ Gr4.1 SmartNguyễn Phương UyênNo ratings yet

- Teaching PowerPoint Slides - Chapter 16Document36 pagesTeaching PowerPoint Slides - Chapter 16Seo ChangBinNo ratings yet

- Management Case Study Submission Guidelines - (Shuvo - Britterbaire@ymail - Com)Document7 pagesManagement Case Study Submission Guidelines - (Shuvo - Britterbaire@ymail - Com)Shuvo Sultana HasanNo ratings yet

- Independent University, Bangladesh School of Business: Strategic ManagementDocument4 pagesIndependent University, Bangladesh School of Business: Strategic ManagementDevdip ÇhâwdhúrÿNo ratings yet

- CitikeyDocument54 pagesCitikeyJacob PochinNo ratings yet

- SMP A3 PDFDocument6 pagesSMP A3 PDFMarlyn OrticioNo ratings yet

- Business Plan CafeDocument10 pagesBusiness Plan CafeNO NAME100% (1)

- SIP Report Atharva SableDocument68 pagesSIP Report Atharva Sable7s72p3nswtNo ratings yet

- Chapter 9Document12 pagesChapter 9Ruthchell CiriacoNo ratings yet

- Uhura Company Has Decided To Expand Its Operations The BookkeepDocument1 pageUhura Company Has Decided To Expand Its Operations The BookkeepM Bilal SaleemNo ratings yet

- Causes of Low Literacy Rate in PakistanDocument27 pagesCauses of Low Literacy Rate in PakistanSaba Naeem82% (17)

- Press Release JFSL and Blackrock Agree To Form JVDocument3 pagesPress Release JFSL and Blackrock Agree To Form JVvikaskfeaindia15No ratings yet

- GiftDocument6 pagesGiftalive2flirtNo ratings yet

- Oilsafe Identification LabelsDocument12 pagesOilsafe Identification LabelsHesham MahdyNo ratings yet

- Coti GIW Rep 26x28LSA PDFDocument3 pagesCoti GIW Rep 26x28LSA PDFjohan diazNo ratings yet

- 30 Pantry Organization Ideas and Tricks - How To Organize A PantryDocument1 page30 Pantry Organization Ideas and Tricks - How To Organize A PantryCKNo ratings yet

- FLIPKART Research ReportDocument18 pagesFLIPKART Research ReportHabib RahmanNo ratings yet

- IE 317 Case Study 4: Bsie Ii Group 7Document37 pagesIE 317 Case Study 4: Bsie Ii Group 7Chel Armenton100% (1)

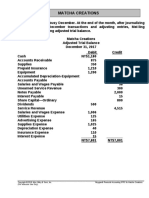

- MC4 Matcha Creations: (For Instructor Use Only)Document2 pagesMC4 Matcha Creations: (For Instructor Use Only)Reza eka PutraNo ratings yet

- Employee Performance Management Literature ReviewDocument6 pagesEmployee Performance Management Literature Reviewea8d1b6nNo ratings yet

- Certificado EGT 20000 MAX G2Document4 pagesCertificado EGT 20000 MAX G2Diego PionaNo ratings yet

- Case Study 3: Fountain Pens LimitedDocument3 pagesCase Study 3: Fountain Pens Limitedtanya singh100% (1)

- Sir Jeff FX GuideDocument143 pagesSir Jeff FX GuideMadafaka MarobozuNo ratings yet

- Typeform Invoice BTLWMgTYQCPq91RjvDocument1 pageTypeform Invoice BTLWMgTYQCPq91RjvAakash vermaNo ratings yet

- Project Cycle Management Report (AEPAM Pub.288)Document64 pagesProject Cycle Management Report (AEPAM Pub.288)Waqar AhmadNo ratings yet

- Branding-Bottled WaterDocument29 pagesBranding-Bottled Watern4b33l100% (1)

- Fringe Benefits Test BankDocument12 pagesFringe Benefits Test BankAB Cloyd100% (1)

- ChatGPT PromptsDocument105 pagesChatGPT PromptsJohn ErichNo ratings yet

- FINAL Morocco FIDE PD DPF P168587 Jan 23 2019 Clean For RVP 1 01282019 636865560830710558Document92 pagesFINAL Morocco FIDE PD DPF P168587 Jan 23 2019 Clean For RVP 1 01282019 636865560830710558Patsy CarterNo ratings yet

- Wbc-Ec 2020Document6 pagesWbc-Ec 2020mrfutschNo ratings yet

- Services Flyer en DEC 2022 FinalDocument35 pagesServices Flyer en DEC 2022 FinalPabloBecerraNo ratings yet