You might also like

- KRA 1. Maternal, Neonatal, Child Health and Nutrition (MNCHN)Document7 pagesKRA 1. Maternal, Neonatal, Child Health and Nutrition (MNCHN)Tmo BosNo ratings yet

- 1619921936223forensic Science UNIT - I PDFDocument86 pages1619921936223forensic Science UNIT - I PDFVyshnav RNo ratings yet

- The Riches of Ra by Michael LeppierDocument18 pagesThe Riches of Ra by Michael LeppierMassimo1083100% (13)

- Pokerole Core Rulebook 2.0Document489 pagesPokerole Core Rulebook 2.0Trey Bachtiger100% (2)

- US ARMY US MARINE CORPS TM 10-4610-215-10 TM 08580A-10/1 TECHNICAL MANUAL OPERATORS MANUAL, WATER PURIFICATION UNIT, REVERSE OSMOSIS, 600 GPH TRAILER MOUNTED FLATBED CARGO, 5 TON 4 WHEEL TANDEM ROWPU MODEL 600-1 (4610-01-093-2380) AND 600 GPH SKID MOUNTED ROWPU MODEL 600-3 (4610-01-113-8651)Document223 pagesUS ARMY US MARINE CORPS TM 10-4610-215-10 TM 08580A-10/1 TECHNICAL MANUAL OPERATORS MANUAL, WATER PURIFICATION UNIT, REVERSE OSMOSIS, 600 GPH TRAILER MOUNTED FLATBED CARGO, 5 TON 4 WHEEL TANDEM ROWPU MODEL 600-1 (4610-01-093-2380) AND 600 GPH SKID MOUNTED ROWPU MODEL 600-3 (4610-01-113-8651)hbpr9999100% (2)

- Principles of AccontingDocument16 pagesPrinciples of AccontingShafqat WassanNo ratings yet

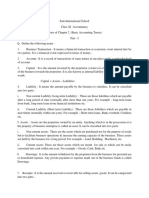

- Chapter 8-Types of Major AccountsDocument2 pagesChapter 8-Types of Major AccountsRichael Ann Delubio ZapantaNo ratings yet

- Balance SheetDocument25 pagesBalance SheetDHANUSHA BALAKRISHNANNo ratings yet

- ACC106 - Chapter 3Document30 pagesACC106 - Chapter 3Nealie100% (1)

- ACC406 - Chapter 3Document32 pagesACC406 - Chapter 3Carol Lesly100% (1)

- Corporate Financial Statements IDocument43 pagesCorporate Financial Statements IArpit SidhuNo ratings yet

- Week 1: Assignment: A Report On What Has Been Learnt by Us Over The Week 1Document9 pagesWeek 1: Assignment: A Report On What Has Been Learnt by Us Over The Week 1Govind GoelNo ratings yet

- CHAPTER 2-Accounting EquationDocument91 pagesCHAPTER 2-Accounting EquationHảo HuỳnhNo ratings yet

- Types of Major AccountsDocument2 pagesTypes of Major Accountscristin l. viloriaNo ratings yet

- FABM1TGhandouts L8 9TypesOfMajAcctsDocument2 pagesFABM1TGhandouts L8 9TypesOfMajAcctsKarl Vincent DulayNo ratings yet

- Session 2 Basic TermsDocument23 pagesSession 2 Basic TermsSagar ParateNo ratings yet

- AccountingDocument35 pagesAccountingJohn Eric Caparros AzoresNo ratings yet

- Accountingnit Jamshedpur NotesDocument47 pagesAccountingnit Jamshedpur NotesSuraj KumarNo ratings yet

- Lesson 1 SFPDocument14 pagesLesson 1 SFPLydia Rivera100% (3)

- 2assets, Liabilities and CapitalDocument5 pages2assets, Liabilities and Capitaldilhani sheharaNo ratings yet

- Lesson 2: General Purpose Financial Statements: Business Resources Amount From Creditors + Amount From OwnersDocument5 pagesLesson 2: General Purpose Financial Statements: Business Resources Amount From Creditors + Amount From OwnersRomae DomagasNo ratings yet

- Chapter - 2 Basic Accounting TermsDocument6 pagesChapter - 2 Basic Accounting TermsChaudhary GaylesabbNo ratings yet

- Basic Accounting TermsDocument7 pagesBasic Accounting TermsKamal SoniNo ratings yet

- Accounting: Basic Terminologies in AccountingDocument24 pagesAccounting: Basic Terminologies in AccountingRoshan JhaNo ratings yet

- Assets Assets Are The Resources Owned and Controlled by The FirmDocument4 pagesAssets Assets Are The Resources Owned and Controlled by The FirmAshaira MangondayaNo ratings yet

- XI Notes of Chapter 2 Part I PDFDocument3 pagesXI Notes of Chapter 2 Part I PDFRoshanNo ratings yet

- Acc1 Lesson Week8 1Document26 pagesAcc1 Lesson Week8 1KeiNo ratings yet

- Fabm2 1Document17 pagesFabm2 1Jacel GadonNo ratings yet

- Type of AccountsDocument35 pagesType of AccountsJennifer0% (1)

- Types of Major AccountsDocument2 pagesTypes of Major AccountsKelsey Sofia RojasNo ratings yet

- FM 101 Chapter 3Document41 pagesFM 101 Chapter 3maryjoymayo494No ratings yet

- LESSON 8 - Types of Major AccountsDocument3 pagesLESSON 8 - Types of Major Accountsdrea.heart29No ratings yet

- EBITDAC - A New Financial Metric?: Earnings Before Interest, Taxes, Depreciation, Amortization, and CoronavirusDocument24 pagesEBITDAC - A New Financial Metric?: Earnings Before Interest, Taxes, Depreciation, Amortization, and Coronavirusks frNo ratings yet

- Chapter # 1 Business TransactionDocument22 pagesChapter # 1 Business TransactionWaleed NasirNo ratings yet

- Account Tiltes HandoutsDocument2 pagesAccount Tiltes HandoutsSean Andreson MabalacadNo ratings yet

- Users of Accounting InformationDocument4 pagesUsers of Accounting InformationWycliffe OgetiiNo ratings yet

- CMBE 2 - Lesson 3 ModuleDocument12 pagesCMBE 2 - Lesson 3 ModuleEunice AmbrocioNo ratings yet

- The Accounting EquationDocument4 pagesThe Accounting EquationjcwimzNo ratings yet

- Basic Accounting TermsDocument16 pagesBasic Accounting TermsKusum MotwaniNo ratings yet

- Basic Terminologies of Accounting: 1. AssetsDocument10 pagesBasic Terminologies of Accounting: 1. AssetsSophiya PrabinNo ratings yet

- ABM ReviewerDocument2 pagesABM Reviewermary christy mantalabaNo ratings yet

- An Introduction To Business and AccountingDocument43 pagesAn Introduction To Business and AccountingKeo VannuthNo ratings yet

- The Five Major Accounts & The Chart of AccountsDocument29 pagesThe Five Major Accounts & The Chart of AccountsPrecious Leigh VillamayorNo ratings yet

- Flow of Costs: Module 2 Introducing The Fin Statements, and Transaction Analysis. Start by Looking atDocument36 pagesFlow of Costs: Module 2 Introducing The Fin Statements, and Transaction Analysis. Start by Looking atLong NguyenNo ratings yet

- Module - 6 Balance SheetDocument67 pagesModule - 6 Balance Sheetlakshmi dileepNo ratings yet

- EC480 Banks Balance Sheet AnalysisDocument110 pagesEC480 Banks Balance Sheet Analysistugrul.kartalogluNo ratings yet

- Statement of Financial PositionDocument8 pagesStatement of Financial PositionKaye LiwagNo ratings yet

- Acconting NotesDocument27 pagesAcconting NotesparinkhonaNo ratings yet

- Chapter 2 HandoutsDocument15 pagesChapter 2 HandoutsBlackpink BtsNo ratings yet

- Accounting: Ankon Gopal BanikDocument9 pagesAccounting: Ankon Gopal BanikAnkon Gopal BanikNo ratings yet

- Chapter 2 NLKTDocument58 pagesChapter 2 NLKTPhan Lê Anh Đào100% (1)

- Short-Questions (Accounts) 1.goodsDocument3 pagesShort-Questions (Accounts) 1.goodsUrvishNo ratings yet

- Chapter 2 FarDocument2 pagesChapter 2 FarAdil KaranNo ratings yet

- Financial Accounting and Analysis: Internal Assignment Applicable For June 2021examinationDocument10 pagesFinancial Accounting and Analysis: Internal Assignment Applicable For June 2021examinationTeChtroNiCS [AK]No ratings yet

- FABM2 - Statement of Financial PositionDocument36 pagesFABM2 - Statement of Financial PositionVron Blatz100% (6)

- Types of Major AccountsDocument30 pagesTypes of Major AccountsEstelle GammadNo ratings yet

- Statement of Financial PositionDocument64 pagesStatement of Financial PositionDaphne Gesto SiaresNo ratings yet

- Accounting Chapter 2. Financial Statements For Decision MakingDocument56 pagesAccounting Chapter 2. Financial Statements For Decision MakingMichenNo ratings yet

- 8011 Topper 21 101 503 550 10598 Basic Accounting Terms Up201904301415 1556613905 1714Document7 pages8011 Topper 21 101 503 550 10598 Basic Accounting Terms Up201904301415 1556613905 1714Madhu SNo ratings yet

- Balance Sheet: Mehwish KiranDocument28 pagesBalance Sheet: Mehwish KiranAlina ZubairNo ratings yet

- UNIT II The Accounting Process Service and TradingDocument22 pagesUNIT II The Accounting Process Service and TradingAlezandra SantelicesNo ratings yet

- MODULE 5-The Five Major AccountsDocument6 pagesMODULE 5-The Five Major Accountsgerlie gabrielNo ratings yet

- Fabm2 02Document24 pagesFabm2 02Alyza Maegan SebastianNo ratings yet

- 2 Elements of AccountingDocument4 pages2 Elements of Accountingapi-299265916No ratings yet

- Unit I IVDocument169 pagesUnit I IVKALAI ARASANNo ratings yet

- CF FormulaesDocument30 pagesCF FormulaesKALAI ARASANNo ratings yet

- Unit IvDocument18 pagesUnit IvKALAI ARASANNo ratings yet

- Sources of FinanceDocument44 pagesSources of FinanceKALAI ARASANNo ratings yet

- Cost of CapitalFM 1.1Document54 pagesCost of CapitalFM 1.1KALAI ARASANNo ratings yet

- Canopy Growth Corporation Final ReportDocument14 pagesCanopy Growth Corporation Final ReportKALAI ARASANNo ratings yet

- Time Value of MoneyDocument78 pagesTime Value of MoneyKALAI ARASANNo ratings yet

- Persuasive EssayDocument8 pagesPersuasive EssayBri GringNo ratings yet

- TLM When To Sit & StandDocument1 pageTLM When To Sit & Standluthien tasadurNo ratings yet

- Iwo Jima Amphibious Ready Group/24TH Marine Expeditionary Unit (IWOARG/24 MEU) NDIA Post-Deployment BriefDocument13 pagesIwo Jima Amphibious Ready Group/24TH Marine Expeditionary Unit (IWOARG/24 MEU) NDIA Post-Deployment Briefthatguy96No ratings yet

- Ainbook Unit6wk2Document10 pagesAinbook Unit6wk2GarrettNo ratings yet

- BS en 14399-3-2015Document32 pagesBS en 14399-3-2015WeldedSplice100% (3)

- Homeless Serving Land Use Overnight Shelter Parcel DataDocument14 pagesHomeless Serving Land Use Overnight Shelter Parcel DataAbhishekh GuptaNo ratings yet

- Trading Legends Million MovesDocument7 pagesTrading Legends Million Movesjoxax95901No ratings yet

- Innovative Practices in HRM at Global LevelDocument5 pagesInnovative Practices in HRM at Global LevelInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- The Goddess Within and Beyond The Three PDFDocument417 pagesThe Goddess Within and Beyond The Three PDFEkaterina Aristova100% (4)

- Intercultural Competence in Elt Syllabus and Materials DesignDocument12 pagesIntercultural Competence in Elt Syllabus and Materials DesignLareina AssoumNo ratings yet

- Purchase Request: Supplies and Materials For Organic Agriculture Production NC IiDocument13 pagesPurchase Request: Supplies and Materials For Organic Agriculture Production NC IiKhael Angelo Zheus JaclaNo ratings yet

- Arjuna Prime FinalDocument27 pagesArjuna Prime FinalTejaswi SaxenaNo ratings yet

- Respondent 2007 - Asia Cup MootDocument31 pagesRespondent 2007 - Asia Cup MootNabilBariNo ratings yet

- SMC vs. Laguesma (1997)Document2 pagesSMC vs. Laguesma (1997)Kimberly SendinNo ratings yet

- Documentary: A War From Another Galaxy: Hoodedcobra666Document2 pagesDocumentary: A War From Another Galaxy: Hoodedcobra666kevin lopes cardosoNo ratings yet

- Ethicalaspectsof FinanciaDocument6 pagesEthicalaspectsof FinanciaVinay RamaneNo ratings yet

- AL-qadim Archetypes: Scimitars Against The DarkDocument33 pagesAL-qadim Archetypes: Scimitars Against The DarkJes100% (14)

- A Beckett Canon PDFDocument433 pagesA Beckett Canon PDFMyshkin100% (1)

- PitchbookDocument6 pagesPitchbookSAMEERNo ratings yet

- Esusu Africa - Digital Cooperative Banking - ProposalDocument6 pagesEsusu Africa - Digital Cooperative Banking - Proposalchristian obinnaNo ratings yet

- Taxation - Constitutional Limitations PDFDocument1 pageTaxation - Constitutional Limitations PDFVicson Mabanglo100% (3)

- Professional Practice Law and Ethics 1st Unit Lecture NotesDocument27 pagesProfessional Practice Law and Ethics 1st Unit Lecture NotesRammohanreddy RajidiNo ratings yet

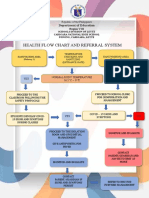

- Health Flow Chart and Referral System: Department of EducationDocument2 pagesHealth Flow Chart and Referral System: Department of EducationWendy TablaNo ratings yet

- Deferred AnnuityDocument10 pagesDeferred AnnuityYoon Dae MinNo ratings yet

- Philip B. Magtaan, Rcrim, Mscrim, CSP: LecturerDocument13 pagesPhilip B. Magtaan, Rcrim, Mscrim, CSP: LecturerPhilip MagtaanNo ratings yet