You might also like

- The ALLTEL Pavilion Case - Strategy and CVP Analysis PDFDocument7 pagesThe ALLTEL Pavilion Case - Strategy and CVP Analysis PDFPritam Kumar NayakNo ratings yet

- Group8-Baldwin Bicycle CompanyDocument9 pagesGroup8-Baldwin Bicycle CompanyChandrachuda SharmaNo ratings yet

- Baldwin PDFDocument14 pagesBaldwin PDFAli Zaigham AghaNo ratings yet

- An Internship Report OnDocument40 pagesAn Internship Report OnRaunak Thapa100% (6)

- Volkswagen - An Offshore CompanyDocument10 pagesVolkswagen - An Offshore CompanyIoana ȚecuNo ratings yet

- Solutions To Chapters 7 and 8 Problem SetsDocument21 pagesSolutions To Chapters 7 and 8 Problem SetsMuhammad Hasnain100% (1)

- AJAX OriginalDocument7 pagesAJAX Originalreva_radhakrish1834No ratings yet

- Excerpt From Antonio Pigafetta - S First Voyage Around TheDocument34 pagesExcerpt From Antonio Pigafetta - S First Voyage Around TheAlff Xui100% (1)

- Case 18-1 Huron Automotive Company StudyDocument4 pagesCase 18-1 Huron Automotive Company StudyEmpress CarrotNo ratings yet

- Baldwin Bicycle CaseDocument10 pagesBaldwin Bicycle CaseAli Zaigham AghaNo ratings yet

- Case ReichardDocument23 pagesCase ReichardDesiSelviaNo ratings yet

- MANAC II - Morrissey Forgings CaseDocument8 pagesMANAC II - Morrissey Forgings CaseKaran Oberoi100% (1)

- Budgeting Activity DanshuiDocument1 pageBudgeting Activity Danshuiptanoy8No ratings yet

- Natureview Case StudyDocument3 pagesNatureview Case StudySachin KamraNo ratings yet

- Nview SolnDocument6 pagesNview SolnShashikant SagarNo ratings yet

- Chapter 26Document32 pagesChapter 26karlosgwapo3No ratings yet

- Marketing AssignmentDocument14 pagesMarketing Assignmentvineel kumarNo ratings yet

- Baldwin Bicycle CaseDocument10 pagesBaldwin Bicycle CaseDhurjati Majumdar100% (1)

- Baldwin Bicycle Company - Ashik AhmedDocument3 pagesBaldwin Bicycle Company - Ashik AhmedAkhilesh UniyalNo ratings yet

- Baldwin Bicycle CompanyDocument5 pagesBaldwin Bicycle CompanyPremal Gangar0% (1)

- Mgt. Acctg, - Case Study - Baldwin BicycleDocument14 pagesMgt. Acctg, - Case Study - Baldwin BicycleCristina Fernandez SanchezNo ratings yet

- Baldwin BicyclesDocument15 pagesBaldwin BicyclesAtul Hegadepatil100% (1)

- Baldwin Bicycle Company - Group8Document8 pagesBaldwin Bicycle Company - Group8Satyendra ShuklaNo ratings yet

- Forner Carpet CompanyDocument7 pagesForner Carpet CompanySimranjeet KaurNo ratings yet

- Sara Lee: A Tale of Another Turnaround: Case Analysis - Strategic ManagementDocument6 pagesSara Lee: A Tale of Another Turnaround: Case Analysis - Strategic ManagementKeerthi PurushothamanNo ratings yet

- Baldwin Bicycle CompanyDocument19 pagesBaldwin Bicycle CompanyMannu83No ratings yet

- Kreative Kasuals - NewDocument10 pagesKreative Kasuals - NewDeep Gandhi100% (1)

- Honda Case - A: Group 8Document9 pagesHonda Case - A: Group 8Shivam ShuklaNo ratings yet

- Baldwin Case Analysis - Kanupriya ChaudharyDocument4 pagesBaldwin Case Analysis - Kanupriya ChaudharyKanupriya ChaudharyNo ratings yet

- BALDWIN Case BarnaliDocument39 pagesBALDWIN Case BarnaliVinay PottiNo ratings yet

- Group 7 - Morrissey ForgingsDocument10 pagesGroup 7 - Morrissey ForgingsVishal AgarwalNo ratings yet

- MA Session 5 PDFDocument35 pagesMA Session 5 PDFArkaprabha GhoshNo ratings yet

- Case - SunAir Boat Builders Part - 2Document3 pagesCase - SunAir Boat Builders Part - 2dhakar_ravi1No ratings yet

- Kreative Kasuals NewDocument11 pagesKreative Kasuals Newdebapriya sarkarNo ratings yet

- Wilkerson Company Case Numerical Approach SolutionDocument3 pagesWilkerson Company Case Numerical Approach SolutionAbdul Rauf JamroNo ratings yet

- Curled Metal IncDocument1 pageCurled Metal IncDeepesh MoolchandaniNo ratings yet

- Management Control Systems, Transfer Pricing, and Multinational Considerations 22Document30 pagesManagement Control Systems, Transfer Pricing, and Multinational Considerations 22Martinus WarsitoNo ratings yet

- Baldwin Bicycle CaseDocument18 pagesBaldwin Bicycle CaseSneha Shenoy100% (2)

- Unitron CorporationDocument7 pagesUnitron CorporationERika PratiwiNo ratings yet

- Hilton Manufacturing CompanyDocument15 pagesHilton Manufacturing CompanySARA SALASNo ratings yet

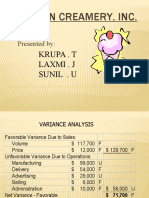

- Boston Creamery CaseDocument9 pagesBoston Creamery Caselion_heart3001100% (1)

- CLV Calculation With No Changes To Brand Strategy: NPV of Expected Cash Flow From Customer (CLV) $378.49Document4 pagesCLV Calculation With No Changes To Brand Strategy: NPV of Expected Cash Flow From Customer (CLV) $378.49killerboyeNo ratings yet

- Boston CreameryDocument11 pagesBoston CreameryJelline Gaza100% (3)

- Group 7 - Excel - Destin BrassDocument9 pagesGroup 7 - Excel - Destin BrassSaumya SahaNo ratings yet

- 3 ManAcc CasesDocument5 pages3 ManAcc CasesalexsophieNo ratings yet

- Case Analysis On Huron Automotive CompanyDocument12 pagesCase Analysis On Huron Automotive CompanyAce ConcepcionNo ratings yet

- Case AnalysisDocument11 pagesCase AnalysisSrinivasan IyerNo ratings yet

- CVPDocument3 pagesCVPRajShekarReddyNo ratings yet

- Fashion - Point SolutionDocument4 pagesFashion - Point SolutionMuhammad JunaidNo ratings yet

- Chemalite Cash Flow StatementDocument2 pagesChemalite Cash Flow Statementrishika rshNo ratings yet

- Midwest Office Products - AHMDocument4 pagesMidwest Office Products - AHMMSINS SDEDNo ratings yet

- CMI Vs Conventional Pads: Curled Metal Inc. Group - 15Document2 pagesCMI Vs Conventional Pads: Curled Metal Inc. Group - 15Malini RajashekaranNo ratings yet

- Reichard Maschinen DocumentDocument5 pagesReichard Maschinen DocumentLucille Ausborn100% (2)

- JHT Case ExcelDocument4 pagesJHT Case Excelanup akasheNo ratings yet

- Clean SpritzDocument2 pagesClean SpritzSaurabh KadamNo ratings yet

- Bill French Case Submitted By: Sourabh Phanase Section: ADocument2 pagesBill French Case Submitted By: Sourabh Phanase Section: AsourabhphanaseNo ratings yet

- Cost-Volume-Profit AnalysisDocument50 pagesCost-Volume-Profit AnalysisMarkiesha StuartNo ratings yet

- Group 2 - Baldwin Bicycle Company (BBC)Document8 pagesGroup 2 - Baldwin Bicycle Company (BBC)wenablesNo ratings yet

- Baldwin Cycles - Group Assignment - SG H Submission ScribdDocument4 pagesBaldwin Cycles - Group Assignment - SG H Submission ScribdDharna KachrooNo ratings yet

- 6 Baldwin+ENG GG100ADocument5 pages6 Baldwin+ENG GG100Av5jssftpwtNo ratings yet

- ACCT 2500 Test 2 Format, Instructions and ReviewDocument17 pagesACCT 2500 Test 2 Format, Instructions and Reviewyahye ahmedNo ratings yet

- Exercise 2 Problems 1 Which of The Following Items Would You Classify in COGS?Document4 pagesExercise 2 Problems 1 Which of The Following Items Would You Classify in COGS?Matthew LiNo ratings yet

- AFD Practice Questions Mock (3399)Document7 pagesAFD Practice Questions Mock (3399)AbhiNo ratings yet

- Baldwin Bicycle CompanyDocument7 pagesBaldwin Bicycle CompanyIndustry ReportNo ratings yet

- Grand Rounds Alumni MagazineSaint Louis University School of MedicineDocument13 pagesGrand Rounds Alumni MagazineSaint Louis University School of MedicineSlusom WebNo ratings yet

- Introduction To Real NumbersDocument4 pagesIntroduction To Real NumbersMuhammad Saad GhaffarNo ratings yet

- Asia Lighterage and Shipping Inc Vs Court of AppealsDocument2 pagesAsia Lighterage and Shipping Inc Vs Court of AppealsCRS CBOS SEC REGISTRATIONNo ratings yet

- PDD Syllabus Anna UniversityDocument41 pagesPDD Syllabus Anna UniversityVenkatakrishnan NatchiappanNo ratings yet

- Canaan Group: Reshaping The Ecs DivisionDocument2 pagesCanaan Group: Reshaping The Ecs Divisionankit0% (1)

- BetaCodex-OrgPhysic Niels PflaegingDocument27 pagesBetaCodex-OrgPhysic Niels PflaegingClaudia TirbanNo ratings yet

- Minstrel GuideDocument14 pagesMinstrel GuideEdith IndekNo ratings yet

- Casual To Committed WorkbookDocument32 pagesCasual To Committed WorkbookNicole Clase CruzNo ratings yet

- Capiz NewsDocument4 pagesCapiz NewsalexNo ratings yet

- A Critical Study of The Theories of Proper NamesDocument211 pagesA Critical Study of The Theories of Proper NamesSirajuddin ANo ratings yet

- Database Management SystemsDocument85 pagesDatabase Management Systemsbogdan2303No ratings yet

- Global Ethics Seminal Essays Thomas PoggDocument2 pagesGlobal Ethics Seminal Essays Thomas Poggvishal tiwariNo ratings yet

- New CV - SalamaDocument3 pagesNew CV - Salamaapi-404126004No ratings yet

- Rail Generic Risk Assessments V8 2014Document10 pagesRail Generic Risk Assessments V8 2014SbitNo ratings yet

- De Report PDFDocument24 pagesDe Report PDFAdarshPatelNo ratings yet

- Syn113/Syn115 Datasheet: (300-450Mhz Ask Transmitter)Document18 pagesSyn113/Syn115 Datasheet: (300-450Mhz Ask Transmitter)mhemaraNo ratings yet

- EXP10MOM1252Document6 pagesEXP10MOM1252Sreevatsan M D 19BME1252No ratings yet

- 1st Semst Result HistologyDocument14 pages1st Semst Result Histologyas adNo ratings yet

- Adjectival Clauses G7Document2 pagesAdjectival Clauses G7Kritika RamchurnNo ratings yet

- Ethymyology of Intelligence Abroad and in UzbekistanDocument4 pagesEthymyology of Intelligence Abroad and in UzbekistanresearchparksNo ratings yet

- English5 Q4 LAS3Document7 pagesEnglish5 Q4 LAS3Marynel ZaragosaNo ratings yet

- Rublic 4 Video Presentation RubricDocument2 pagesRublic 4 Video Presentation RubricYenyen Quirog-PalmesNo ratings yet

- PDF Ef Test - CompressDocument5 pagesPDF Ef Test - CompressNadila AuliaNo ratings yet

- 14.statistics and Porbability Password RemovedDocument43 pages14.statistics and Porbability Password RemovedfameNo ratings yet

- Hein V Chandler Amended ComplaintDocument23 pagesHein V Chandler Amended ComplaintDave BiscobingNo ratings yet

- Matura ŚrodkiDocument76 pagesMatura ŚrodkiKlaudia KasprzakNo ratings yet