You might also like

- UFCW 1776 2012 Financials Wendell YoungDocument38 pagesUFCW 1776 2012 Financials Wendell YoungbobguzzardiNo ratings yet

- AlfaDocument6 pagesAlfaranjeet baghelNo ratings yet

- Basketball Season Tickets 2022-2023 ProjectDocument1 pageBasketball Season Tickets 2022-2023 Projectapi-620442382No ratings yet

- Quickbooks Guide - Chart of AccountsDocument13 pagesQuickbooks Guide - Chart of Accountsjr7mondo7edoNo ratings yet

- CMS Manual System: Pub 100-04 Medicare Claims ProcessingDocument33 pagesCMS Manual System: Pub 100-04 Medicare Claims ProcessingMiguel ÁngelNo ratings yet

- CSG 10Q Sep 10Document226 pagesCSG 10Q Sep 10Shubham BhatiaNo ratings yet

- Company Cash Advance FormDocument1 pageCompany Cash Advance FormFrancisco CatapangNo ratings yet

- Summarized - Invoice - 380231RDocument40 pagesSummarized - Invoice - 380231RPenélope FatimaNo ratings yet

- Form No 10-IaDocument1 pageForm No 10-Iacooldude32166No ratings yet

- Modern Trends in CompensationDocument14 pagesModern Trends in CompensationHardik Kothiyal100% (2)

- Altlifelab: InstructionsDocument1,957 pagesAltlifelab: InstructionsIndira VenkataramanNo ratings yet

- Investor Diary Expert Stock Analysis Excel (V-3) : How To Use This Spreadsheet?Document206 pagesInvestor Diary Expert Stock Analysis Excel (V-3) : How To Use This Spreadsheet?karife3137100% (1)

- Mathematics Quarter 2 - Module 2: Simple, General, and Deferred AnnuitiesDocument17 pagesMathematics Quarter 2 - Module 2: Simple, General, and Deferred AnnuitiesJoseph Mondo�edo100% (1)

- Philippine International Trading Corp PITC Vs Comm. On Audit G.R. No. 205837Document3 pagesPhilippine International Trading Corp PITC Vs Comm. On Audit G.R. No. 205837Bhoxs Joey CelesparaNo ratings yet

- JCL Theory - E Book On JCLDocument4 pagesJCL Theory - E Book On JCLDebanjan SahaNo ratings yet

- Chapter 2-3 SQL queriesDocument3 pagesChapter 2-3 SQL queriesRaistlin Chan Ching KitNo ratings yet

- SCLM ManualDocument340 pagesSCLM ManualpavanrajhrNo ratings yet

- PART B (Annexure) Details of Salary Paid and Any Other Income and Tax Deducted INR Inr InrDocument3 pagesPART B (Annexure) Details of Salary Paid and Any Other Income and Tax Deducted INR Inr InrAshraf KhanNo ratings yet

- Abend Solving (Mine)Document63 pagesAbend Solving (Mine)Thrinadh B JNo ratings yet

- HP LaptopDocument1 pageHP Laptopgudavalli0088No ratings yet

- UBI RFP Integrated Treasury Management System RFP - Itms - Dit - r00000000-0000-0Document148 pagesUBI RFP Integrated Treasury Management System RFP - Itms - Dit - r00000000-0000-0shankar vnNo ratings yet

- Input Table - Master Database: Employee Transaction File: USERID - COBCASE.PS - TRANS Output Report File: Userid - Cobcase.Ps - ReportDocument4 pagesInput Table - Master Database: Employee Transaction File: USERID - COBCASE.PS - TRANS Output Report File: Userid - Cobcase.Ps - ReportHarithaNo ratings yet

- Database Shutdown IssueDocument45 pagesDatabase Shutdown Issuetitamin21100% (3)

- Form No. Aoc-4: Form For Filing Financial Statement and Other Documents With The RegistrarDocument9 pagesForm No. Aoc-4: Form For Filing Financial Statement and Other Documents With The RegistrarHardik KalariaNo ratings yet

- One Mobikwik Systems Limited: (Please Read Section 32 of The Companies Act, 2013)Document411 pagesOne Mobikwik Systems Limited: (Please Read Section 32 of The Companies Act, 2013)manmath91No ratings yet

- Data Warehouse Concepts HandbookDocument27 pagesData Warehouse Concepts HandbookFelipe CordeiroNo ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument53 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceVishal BawaneNo ratings yet

- FAQs GST E-Invoice - IRN SystemDocument14 pagesFAQs GST E-Invoice - IRN SystemAman JainNo ratings yet

- Tracking Results: Corporate Profile Tracking Service Guide Franchisee Corporate Solutions Careers Contact UsDocument1 pageTracking Results: Corporate Profile Tracking Service Guide Franchisee Corporate Solutions Careers Contact UssperoNo ratings yet

- Tatmeen Training Manual For Master Data - v1.0Document42 pagesTatmeen Training Manual For Master Data - v1.0Jaweed SheikhNo ratings yet

- Guardian Programming Ref For CDocument344 pagesGuardian Programming Ref For CdeepaksaneNo ratings yet

- 3 BHK Cost SheetDocument6 pages3 BHK Cost SheetADESHNo ratings yet

- Database DriversDocument314 pagesDatabase DriversRoberto Hernandez AmecaNo ratings yet

- Employee Details For RazorpayX PayrollDocument8 pagesEmployee Details For RazorpayX PayrollDeepak kumar M RNo ratings yet

- CPU-Motherboard Block DiagramDocument49 pagesCPU-Motherboard Block DiagrambizongodNo ratings yet

- TTCL Products Services PPT 2021 Version 2Document84 pagesTTCL Products Services PPT 2021 Version 2Michael BaloshNo ratings yet

- WesleyDocument4 pagesWesleyWesley RajaNo ratings yet

- Solutions For GST Question BankDocument55 pagesSolutions For GST Question BankVarun VardhanNo ratings yet

- SQL Server Database Administrator Resume Example Company Name - Atlanta, GeorgiaDocument7 pagesSQL Server Database Administrator Resume Example Company Name - Atlanta, GeorgiaDocktee GhNo ratings yet

- Guide for Deploying Confidential eOffice SystemDocument22 pagesGuide for Deploying Confidential eOffice Systemsumandas1963No ratings yet

- MDB 3.0 PDFDocument270 pagesMDB 3.0 PDFLiñán Hernández Iván UlisesNo ratings yet

- How to file income tax return in NepalDocument5 pagesHow to file income tax return in NepalnepalcaNo ratings yet

- Invoice 8348010670678820049Document2 pagesInvoice 8348010670678820049e2school e2No ratings yet

- Commodities Account FormDocument43 pagesCommodities Account FormDhirenNo ratings yet

- Decision TablesDocument23 pagesDecision TablesHardik KumarNo ratings yet

- Manipulate Records With DML Unit - Salesforce TrailheadDocument9 pagesManipulate Records With DML Unit - Salesforce TrailheadYURI acerNo ratings yet

- WVD Promo FAQ - PartnerDocument7 pagesWVD Promo FAQ - PartnerKamila CordierNo ratings yet

- Payment Gateway Setup Guide PDFDocument21 pagesPayment Gateway Setup Guide PDFOptimus SolutionsNo ratings yet

- TC Transcontinental Benefits Guide 2020 HourlyDocument31 pagesTC Transcontinental Benefits Guide 2020 HourlyMike SloopNo ratings yet

- Annexure - 1: Mode of RepaymentDocument2 pagesAnnexure - 1: Mode of RepaymentJyoti SharmaNo ratings yet

- AX 2012 Fixed Asset Set Up BlogDocument7 pagesAX 2012 Fixed Asset Set Up BlogSrini Vasan100% (1)

- FTSE4Good Index Series Ground RulesDocument28 pagesFTSE4Good Index Series Ground RulesAdel AdielaNo ratings yet

- Fonepay QR AgreementDocument6 pagesFonepay QR AgreementtrijyaNo ratings yet

- Gajendra PandeyDocument94 pagesGajendra PandeyManjeet SinghNo ratings yet

- ABC Lecture Notes PDFDocument24 pagesABC Lecture Notes PDFJose Ramer MegioNo ratings yet

- In Voice 13096706704484885453Document2 pagesIn Voice 13096706704484885453VISHAL ARORANo ratings yet

- SBI Online Trading User GuideDocument73 pagesSBI Online Trading User Guidenaruka21ravindra100% (1)

- Arjun Emf CVDocument2 pagesArjun Emf CVArjun PrasadNo ratings yet

- Form PDF 337279780310722Document7 pagesForm PDF 337279780310722hitendraNo ratings yet

- Illusion Dental Laboratory: JDID-1920-6928 15/04/2019Document2 pagesIllusion Dental Laboratory: JDID-1920-6928 15/04/2019Sheetal100% (1)

- Employee Central 19Document8 pagesEmployee Central 19AxleNo ratings yet

- TesterDocument16 pagesTesterSiddharth arunNo ratings yet

- Income Tax Guidelines For Financial Year 2021-22: Key PointsDocument13 pagesIncome Tax Guidelines For Financial Year 2021-22: Key PointsBhanuSavarniNo ratings yet

- Investment Declaration Guidelines SummaryDocument1 pageInvestment Declaration Guidelines SummarySunny KhavleNo ratings yet

- Note On Budget Proposals-2020Document4 pagesNote On Budget Proposals-2020Dhananjai SharmaNo ratings yet

- Hotel Holiday Resort - Google SearchDocument1 pageHotel Holiday Resort - Google SearchRajshree SamantrayNo ratings yet

- Quotex An Innovative Platform For Online InvestmDocument1 pageQuotex An Innovative Platform For Online InvestmRajshree SamantrayNo ratings yet

- Make My TripDocument1 pageMake My TripRajshree SamantrayNo ratings yet

- 3 Yearresume - SushriDocument3 pages3 Yearresume - SushriRajshree SamantrayNo ratings yet

- Pinterest login sign up home decor glass doors ideas privacy lightDocument1 pagePinterest login sign up home decor glass doors ideas privacy lightRajshree SamantrayNo ratings yet

- 440 Etched Glass Patterns Ideas in 2022 Door Glass Design, Glass Design, Window Glass DesignDocument1 page440 Etched Glass Patterns Ideas in 2022 Door Glass Design, Glass Design, Window Glass DesignRajshree SamantrayNo ratings yet

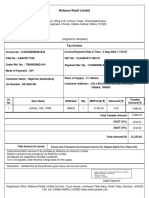

- Reliance Retail Limited: Sr. No. Plan Details SAC Qty MRP/Unit Discount Taxable AmountDocument1 pageReliance Retail Limited: Sr. No. Plan Details SAC Qty MRP/Unit Discount Taxable AmountVijay GuptaNo ratings yet

- Wifi - Invoice - 16 MAY 2022Document2 pagesWifi - Invoice - 16 MAY 2022Rajshree Samantray100% (1)

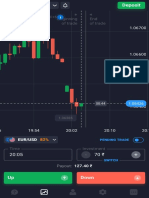

- Live Crypto Trading ResultsDocument1 pageLive Crypto Trading ResultsRajshree SamantrayNo ratings yet

- Reliance Retail Limited: Sr. No. Plan Details SAC Qty MRP/Unit Discount Taxable AmountDocument1 pageReliance Retail Limited: Sr. No. Plan Details SAC Qty MRP/Unit Discount Taxable AmountVijay GuptaNo ratings yet

- CN-829330 Deal Summary Report Version 2Document9 pagesCN-829330 Deal Summary Report Version 2Rajshree SamantrayNo ratings yet

- Cfakepathseleniumc 00206827000000010780219155847Document1 pageCfakepathseleniumc 00206827000000010780219155847Rajshree SamantrayNo ratings yet

- Rent ReceiptDocument1 pageRent ReceiptRajshree SamantrayNo ratings yet

- Reliance Retail Limited: Sr. No. Plan Details SAC Qty MRP/Unit Discount Taxable AmountDocument1 pageReliance Retail Limited: Sr. No. Plan Details SAC Qty MRP/Unit Discount Taxable AmountVijay GuptaNo ratings yet

- Reliance Retail Limited: Sr. No. Plan Details SAC Qty MRP/Unit Discount Taxable AmountDocument1 pageReliance Retail Limited: Sr. No. Plan Details SAC Qty MRP/Unit Discount Taxable AmountVijay GuptaNo ratings yet

- HRA Tax Benefit Self DeclarationDocument1 pageHRA Tax Benefit Self DeclarationRajshree SamantrayNo ratings yet

- Reliance Retail Limited: Sr. No. Plan Details SAC Qty MRP/Unit Discount Taxable AmountDocument1 pageReliance Retail Limited: Sr. No. Plan Details SAC Qty MRP/Unit Discount Taxable AmountVijay GuptaNo ratings yet

- Premium Paid Certificate HDFC Life PolicyDocument1 pagePremium Paid Certificate HDFC Life PolicyRajshree SamantrayNo ratings yet

- PPC 03745733 1671523503Document1 pagePPC 03745733 1671523503Rajshree SamantrayNo ratings yet

- Bobby & BettyDocument6 pagesBobby & BettySimon KingNo ratings yet

- Cve427 - Ce Laws - Week 7: Charging For Civil Engineering Services Six MethodsDocument3 pagesCve427 - Ce Laws - Week 7: Charging For Civil Engineering Services Six MethodsDrei ServitoNo ratings yet

- CH 5 - Compensation MGTDocument28 pagesCH 5 - Compensation MGTGetnat BahiruNo ratings yet

- Excess Business Loss and Net Operating Loss NOL 2021Document2 pagesExcess Business Loss and Net Operating Loss NOL 2021Finn KevinNo ratings yet

- In The Maharashtra Administrative Tribunal MumbaiDocument8 pagesIn The Maharashtra Administrative Tribunal MumbaiTanuja Sawant 50No ratings yet

- 2Document45 pages2fdbfbNo ratings yet

- Law of Tort II DamagesDocument4 pagesLaw of Tort II DamagesBrian PetersNo ratings yet

- Features of ICICI Pru Saral Jeevan BimaDocument2 pagesFeatures of ICICI Pru Saral Jeevan BimaKriti KaNo ratings yet

- Project Title: Effectiveness of Recruitment and Training Programs For Sales Force A Case Study of HDFC Standard LifeDocument47 pagesProject Title: Effectiveness of Recruitment and Training Programs For Sales Force A Case Study of HDFC Standard Lifeanon_45072No ratings yet

- Accounting Liability ReportDocument18 pagesAccounting Liability ReportCaren ReasNo ratings yet

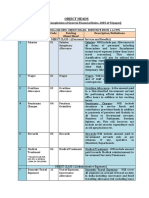

- Object Heads ListingDocument6 pagesObject Heads ListingLal ZahawmaNo ratings yet

- Vanishing DeductionsDocument3 pagesVanishing DeductionsCyrell AsidNo ratings yet

- The Development of Insurance Law: The English & Indian ExperiencesDocument17 pagesThe Development of Insurance Law: The English & Indian ExperiencesTanya RajNo ratings yet

- Labour-PQDocument5 pagesLabour-PQRohaib MumtazNo ratings yet

- Public Sector AccountingDocument394 pagesPublic Sector AccountingUMUHIRE JulienNo ratings yet

- Life Certificate LICIDocument2 pagesLife Certificate LICIChatterjee KushalNo ratings yet

- Covering Sheet For LTADocument1 pageCovering Sheet For LTAsrinath rao P100% (1)

- MODULE 1 Understanding Personal FinanceDocument43 pagesMODULE 1 Understanding Personal FinanceAnore, Anton NikolaiNo ratings yet

- Business Math: Standard DeductionsDocument12 pagesBusiness Math: Standard DeductionsMontenegro Roi Vincent100% (1)

- Corporate Governance: Youchaa KHODR 3 Edition Pearson Prentice HallDocument27 pagesCorporate Governance: Youchaa KHODR 3 Edition Pearson Prentice HallDiana SaidNo ratings yet

- Swot Analysis of The Asset Classes: Real EstateDocument7 pagesSwot Analysis of The Asset Classes: Real EstateMuskan MNo ratings yet

- Direct DepositDocument1 pageDirect DepositMike BelmoreNo ratings yet

- Certfcate No.: NB/01992 Form No. 12 BaDocument7 pagesCertfcate No.: NB/01992 Form No. 12 BaKanishk JamwalNo ratings yet

- Unit 3 Important Questions: BBA 3 Year 5 Semester Subject: Income Tax Law & Accounting Subject Code: BBA N 503Document5 pagesUnit 3 Important Questions: BBA 3 Year 5 Semester Subject: Income Tax Law & Accounting Subject Code: BBA N 503jyoti.singh100% (1)

- R.A. No. 9679 IRRDocument21 pagesR.A. No. 9679 IRRsnhlaoNo ratings yet