You might also like

- Word Note The Body Shop International PLC 2001: An Introduction To Financial ModelingDocument9 pagesWord Note The Body Shop International PLC 2001: An Introduction To Financial Modelingalka murarka100% (2)

- Financial Projections for New Business StartupDocument4 pagesFinancial Projections for New Business StartupShaza ZulfiqarNo ratings yet

- File 19-Class Wrap-Ups 17Document7 pagesFile 19-Class Wrap-Ups 17alroy dcruzNo ratings yet

- File 19-Class Wrap-Ups 16Document7 pagesFile 19-Class Wrap-Ups 16alroy dcruzNo ratings yet

- AVIS CarsDocument10 pagesAVIS CarsSheikhFaizanUl-HaqueNo ratings yet

- Valuation Model1 by Mihir KumarDocument15 pagesValuation Model1 by Mihir KumarMannaNo ratings yet

- Module 1.6 Forecasting Financial Statements Excercise ExcelDocument27 pagesModule 1.6 Forecasting Financial Statements Excercise Excelsachin kambhapuNo ratings yet

- Discounted Cash Flow-Model For ValuationDocument9 pagesDiscounted Cash Flow-Model For ValuationPCM StresconNo ratings yet

- 12008-Dave Tejaskumar Rakeshkumar (Fa&b) PptDocument31 pages12008-Dave Tejaskumar Rakeshkumar (Fa&b) PptAchal SharmaNo ratings yet

- M 16 Forecasting Financial Statements in ExcelDocument12 pagesM 16 Forecasting Financial Statements in ExcelAnrag Tiwari100% (1)

- Macro Economics Aspects of BudgetDocument44 pagesMacro Economics Aspects of Budget6882535No ratings yet

- TMW Co. Ltd Financial ProjectionsDocument15 pagesTMW Co. Ltd Financial ProjectionsgabegwNo ratings yet

- DCF ModelDocument51 pagesDCF Modelhugoe1969No ratings yet

- TechnoFunda Investing Screener Excel Template - NeDocument37 pagesTechnoFunda Investing Screener Excel Template - NeDaknik CutieTVNo ratings yet

- Financial Analysis (Detail)Document68 pagesFinancial Analysis (Detail)Paulo NascimentoNo ratings yet

- Technofunda Investing Excel Analysis - Version 2.0: Watch Screener TutorialDocument37 pagesTechnofunda Investing Excel Analysis - Version 2.0: Watch Screener TutorialVipulNo ratings yet

- 02 WMT 2010 FiveYear SummaryDocument1 page02 WMT 2010 FiveYear SummaryNeha ChoudharyNo ratings yet

- How to use the DCF model tutorialDocument9 pagesHow to use the DCF model tutorialTanya SinghNo ratings yet

- Financial Report Analysis: Mangalore Chemical & Fertilizers LTD and Madras Fertilizers LTDDocument10 pagesFinancial Report Analysis: Mangalore Chemical & Fertilizers LTD and Madras Fertilizers LTDRonit VermaNo ratings yet

- BSY v3 Revenue ModelDocument34 pagesBSY v3 Revenue Modeljazz.srishNo ratings yet

- Pakistan Tobacco Company: A Subsidiary of British American Tobacco (BAT)Document15 pagesPakistan Tobacco Company: A Subsidiary of British American Tobacco (BAT)AbdulRehmanHaschameNo ratings yet

- Portfolio SnapshotDocument63 pagesPortfolio Snapshotgurudev21No ratings yet

- Werner - Financial Model - Final VersionDocument2 pagesWerner - Financial Model - Final VersionAmit JainNo ratings yet

- Team7 FMPhase2 Trent SENIORSDocument75 pagesTeam7 FMPhase2 Trent SENIORSNisarg Rupani100% (1)

- RELAXODocument82 pagesRELAXOFIN GYAANNo ratings yet

- Y-O-Y Sales Growth % 18% 19% 12% 10% 1% 9% 2% 11% 2% - 2%Document7 pagesY-O-Y Sales Growth % 18% 19% 12% 10% 1% 9% 2% 11% 2% - 2%muralyyNo ratings yet

- Ratio Analysis of Colgate PalmoliveDocument19 pagesRatio Analysis of Colgate Palmolivewan nur anisahNo ratings yet

- Technofunda Investing Excel Analysis - Version 2.0: Watch Screener TutorialDocument37 pagesTechnofunda Investing Excel Analysis - Version 2.0: Watch Screener TutorialRaman BajpaiNo ratings yet

- FY 19 Budget Overview 3818Document83 pagesFY 19 Budget Overview 3818Chris SwamNo ratings yet

- Forecasted Volume Sold Direct +0% Volume Sold Direct +1% Volume Sold Direct +2% Volume Sold Direct +3%Document5 pagesForecasted Volume Sold Direct +0% Volume Sold Direct +1% Volume Sold Direct +2% Volume Sold Direct +3%gatorcapital123No ratings yet

- Financial Modelling and Analysis ITCDocument9 pagesFinancial Modelling and Analysis ITCPriyam SarangiNo ratings yet

- Dividend PolicyDocument74 pagesDividend PolicyNithin KsNo ratings yet

- DCF ModelDocument6 pagesDCF ModelKatherine ChouNo ratings yet

- Colgate Ratio Analysis WSM 2020 SolvedDocument17 pagesColgate Ratio Analysis WSM 2020 Solvedabi habudinNo ratings yet

- Titan Company by Anuj GuptaDocument25 pagesTitan Company by Anuj GuptaHIMANSHU RAWATNo ratings yet

- ITC detailed analysis strengths weaknesses forecastsDocument14 pagesITC detailed analysis strengths weaknesses forecastsShivang KalraNo ratings yet

- Laurus Labs Ltd financial analysis and key metrics from 2011 to 2021Document32 pagesLaurus Labs Ltd financial analysis and key metrics from 2011 to 2021Akash GowdaNo ratings yet

- Laurus LabsDocument32 pagesLaurus LabsAkash GowdaNo ratings yet

- Q2FY11 Reliance Communications Result UpdateDocument4 pagesQ2FY11 Reliance Communications Result UpdateVinit BolinjkarNo ratings yet

- Laurus LabsDocument32 pagesLaurus LabsAkash GowdaNo ratings yet

- Ratio Analysis Model - Colgate PalmoliveDocument18 pagesRatio Analysis Model - Colgate PalmoliveAkshataNo ratings yet

- Equity Valuacion (Grupo SBS)Document3 pagesEquity Valuacion (Grupo SBS)Juan José BlesaNo ratings yet

- Financial Model of ACCDocument13 pagesFinancial Model of ACCYash AhujaNo ratings yet

- Financial Model - Colgate Palmolive (Unsolved Template) : Prepared by Dheeraj Vaidya, CFA, FRMDocument35 pagesFinancial Model - Colgate Palmolive (Unsolved Template) : Prepared by Dheeraj Vaidya, CFA, FRMahmad syaifudinNo ratings yet

- P&G Financial Projection Model AssumptionsDocument4 pagesP&G Financial Projection Model AssumptionsHashNo ratings yet

- Project Apraisal Case: The Findings of The Market Research Are As FollowsDocument8 pagesProject Apraisal Case: The Findings of The Market Research Are As FollowsWasif HossainNo ratings yet

- DCF ModellDocument7 pagesDCF ModellVishal BhanushaliNo ratings yet

- DCF TemplateDocument21 pagesDCF TemplateShrikant ShelkeNo ratings yet

- PORTFOLIO_PERFORMANCEDocument51 pagesPORTFOLIO_PERFORMANCEgurudev21No ratings yet

- Adidas/Reebok Merger: Collin Shaw Kelly Truesdale Michael Rockette Benedikte Schmidt SaravanansadaiyappanDocument27 pagesAdidas/Reebok Merger: Collin Shaw Kelly Truesdale Michael Rockette Benedikte Schmidt SaravanansadaiyappanUdipta DasNo ratings yet

- Analisis FinancieroDocument124 pagesAnalisis FinancieroJesús VelázquezNo ratings yet

- 2.11 Duration & ConvexityDocument15 pages2.11 Duration & Convexityshreya2729singhNo ratings yet

- Williamstown Five-Year Revenue Projection 2010Document1 pageWilliamstown Five-Year Revenue Projection 2010iBerkshires.comNo ratings yet

- Green Mountain Coffee Roasters1Document4 pagesGreen Mountain Coffee Roasters1Gary RibeNo ratings yet

- Colgate Financial Model SolvedDocument36 pagesColgate Financial Model SolvedSundara MoorthyNo ratings yet

- Earnings Presentation Q3 FY20Document26 pagesEarnings Presentation Q3 FY20Bruno Enrique Silva AndradeNo ratings yet

- Competitive Intelligence ReportDocument4 pagesCompetitive Intelligence ReportPham TuyenNo ratings yet

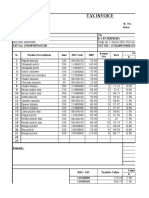

- Tax Invoice: % Rate CGST Sr. Product Description Gms HSN Code MRP Return QtyDocument4 pagesTax Invoice: % Rate CGST Sr. Product Description Gms HSN Code MRP Return QtyJai GaneshNo ratings yet

- Account-Based Marketing: How to Target and Engage the Companies That Will Grow Your RevenueFrom EverandAccount-Based Marketing: How to Target and Engage the Companies That Will Grow Your RevenueRating: 1 out of 5 stars1/5 (1)

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Fugro NV Accounting Review 0311 2013Document3 pagesFugro NV Accounting Review 0311 2013Jean-Louis ThiemeleNo ratings yet

- Ritchie Brothers Auctioneers 04082015 BespokeDocument5 pagesRitchie Brothers Auctioneers 04082015 BespokeJean-Louis ThiemeleNo ratings yet

- RBA Notes March 2015 HighlightsDocument1 pageRBA Notes March 2015 HighlightsJean-Louis ThiemeleNo ratings yet

- Clean Harbors Teaser 0330 2015Document5 pagesClean Harbors Teaser 0330 2015Jean-Louis ThiemeleNo ratings yet

- 5-8 Financial Markets McqsDocument26 pages5-8 Financial Markets McqsdmangiginNo ratings yet

- Lowering Financial Inclusion Barriers With A Blockchain-Based Capital Transfer SystemDocument27 pagesLowering Financial Inclusion Barriers With A Blockchain-Based Capital Transfer Systemoke d4fNo ratings yet

- Retail Selling ProcessDocument17 pagesRetail Selling ProcessAlirezaNNo ratings yet

- Credit Risk - Predictive ModellingDocument47 pagesCredit Risk - Predictive ModellingAldo LealNo ratings yet

- Accounting For ManagersDocument287 pagesAccounting For ManagersmenakaNo ratings yet

- LEARNING MODULE-Financial Accounting and ReportingDocument7 pagesLEARNING MODULE-Financial Accounting and ReportingAira AbigailNo ratings yet

- Book Review - MR Market Miscalculates by James GrantDocument5 pagesBook Review - MR Market Miscalculates by James Grantbillerickson100% (2)

- DJ BANK LTD. BALANCE SHEET AS ON 31-03-2018Document7 pagesDJ BANK LTD. BALANCE SHEET AS ON 31-03-2018jaimin vasaniNo ratings yet

- Financial Statement AnalysisDocument24 pagesFinancial Statement AnalysisDawn Zoleta100% (1)

- Assignment Example May 2019 SubmissionDocument26 pagesAssignment Example May 2019 Submissionmuhammad abdullah janNo ratings yet

- CCGL Asm1 WANG XINRUI 3036128298 2023Document4 pagesCCGL Asm1 WANG XINRUI 3036128298 2023XINRUI WANGNo ratings yet

- Study on Loans and Advances in BankingDocument178 pagesStudy on Loans and Advances in BankingIram Fatmah100% (1)

- Theoretical and Conceptual Framework of Access ToDocument17 pagesTheoretical and Conceptual Framework of Access ToWilliam TabiNo ratings yet

- JANKIDocument47 pagesJANKIJankiNo ratings yet

- Entrepreneurship and Small Business Management 2nd Edition Mariotti Solutions Manual DownloadDocument9 pagesEntrepreneurship and Small Business Management 2nd Edition Mariotti Solutions Manual DownloadRhoda Koester100% (20)

- How Lenderwize is transforming telecom financing with Wiserfunding's rapid risk assessmentsDocument4 pagesHow Lenderwize is transforming telecom financing with Wiserfunding's rapid risk assessmentsAlexander Leanos (Xander)No ratings yet

- Echeverria Motion For Proof of AuthorityDocument13 pagesEcheverria Motion For Proof of AuthorityIsabel SantamariaNo ratings yet

- English Mortgage DefinitionDocument4 pagesEnglish Mortgage DefinitionKiran VenugopalNo ratings yet

- Reducing Balance EMI CalculatorDocument2 pagesReducing Balance EMI CalculatorJamesNo ratings yet

- Conditions Home MortgageDocument77 pagesConditions Home MortgageamfipolitisNo ratings yet

- Pinchhe Tole, Balkumari: Kathmandu University School of ManagementDocument11 pagesPinchhe Tole, Balkumari: Kathmandu University School of ManagementashNo ratings yet

- This Content Downloaded From 154.59.124.214 On Wed, 08 Jun 2022 20:42:36 UTCDocument9 pagesThis Content Downloaded From 154.59.124.214 On Wed, 08 Jun 2022 20:42:36 UTCsalem alkaabiNo ratings yet

- Busana 1 Pe FinalsDocument3 pagesBusana 1 Pe FinalsKim TNo ratings yet

- Ratio Analysis: R K MohantyDocument30 pagesRatio Analysis: R K Mohantybgowda_erp1438No ratings yet

- Merc 2016 Bar Qs and Suggested AnswersDocument10 pagesMerc 2016 Bar Qs and Suggested AnswersedreaNo ratings yet

- OLC Chap 17Document3 pagesOLC Chap 17NeelNo ratings yet

- Indian Mortgages IndustryDocument16 pagesIndian Mortgages IndustryChintan SharmaNo ratings yet

- M8a PDFDocument146 pagesM8a PDFLiz Lee100% (1)

- Genesis Program details innovative private placement trading opportunityDocument2 pagesGenesis Program details innovative private placement trading opportunityunoguru93% (15)

- Proc Docs Safcec JV Agreement 1Document13 pagesProc Docs Safcec JV Agreement 1karri1963No ratings yet