You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Walmart Sample Training ProgramDocument17 pagesWalmart Sample Training ProgramNisha BrosNo ratings yet

- Business ProposalDocument8 pagesBusiness ProposalBraddoriiNo ratings yet

- Tax Midterms Reviwer-CompressedDocument245 pagesTax Midterms Reviwer-Compressedalia fauniNo ratings yet

- Use of Business / Accountancy Models: Annotated Examples of Research and Analysis - Topic 8Document2 pagesUse of Business / Accountancy Models: Annotated Examples of Research and Analysis - Topic 8Reznov KovacicNo ratings yet

- MNM2615 Assignment 2 PDFDocument9 pagesMNM2615 Assignment 2 PDFKefiloe MoatsheNo ratings yet

- Blank 1: Linear - Blank 2: ProgrammingDocument15 pagesBlank 1: Linear - Blank 2: Programmingalia fauniNo ratings yet

- Kahoot 3 LawDocument1 pageKahoot 3 Lawalia fauniNo ratings yet

- Kahoot Part 2Document3 pagesKahoot Part 2alia fauniNo ratings yet

- AIS Chapter 2Document12 pagesAIS Chapter 2alia fauniNo ratings yet

- AIS Chapter 1Document9 pagesAIS Chapter 1alia fauniNo ratings yet

- COSTDocument15 pagesCOSTalia fauniNo ratings yet

- Intermediate Accounting II Computations FlashcardsDocument11 pagesIntermediate Accounting II Computations Flashcardsalia fauniNo ratings yet

- Laboratory Exercise2Document4 pagesLaboratory Exercise2alia fauniNo ratings yet

- Government Agencies Involved in Tax AdministrationDocument2 pagesGovernment Agencies Involved in Tax Administrationalia fauniNo ratings yet

- Computation of Income Tax Due and PayableDocument14 pagesComputation of Income Tax Due and Payablealia fauniNo ratings yet

- Stats SaDocument3 pagesStats Saalia fauniNo ratings yet

- Laboratory Exercise1Document6 pagesLaboratory Exercise1alia fauniNo ratings yet

- Laboratory Exercise 3Document9 pagesLaboratory Exercise 3alia fauniNo ratings yet

- Assessment MLRDocument4 pagesAssessment MLRalia fauniNo ratings yet

- Laboratory Exercise 6Document4 pagesLaboratory Exercise 6alia fauniNo ratings yet

- Laboratory Exercise 5Document5 pagesLaboratory Exercise 5alia fauniNo ratings yet

- Module Reviewer Law ObliDocument183 pagesModule Reviewer Law Oblialia fauniNo ratings yet

- Comprehensive Assessment3Document3 pagesComprehensive Assessment3alia fauniNo ratings yet

- Cost Chapter 4Document10 pagesCost Chapter 4alia fauniNo ratings yet

- EA1 Ia2Document6 pagesEA1 Ia2alia fauniNo ratings yet

- Cost Chapter 1Document10 pagesCost Chapter 1alia fauniNo ratings yet

- The Total Economic Impact of Fortinet NGFW For Data Center and AI-Powered FortiGuard Security Services SolutionDocument29 pagesThe Total Economic Impact of Fortinet NGFW For Data Center and AI-Powered FortiGuard Security Services Solutiontola02000No ratings yet

- Introduction To Mobile Forensics: Full Physical Image AnalysisDocument31 pagesIntroduction To Mobile Forensics: Full Physical Image AnalysisEsteban RamirezNo ratings yet

- Inb 304Document10 pagesInb 304Rebaka Alam KhanNo ratings yet

- Syllabus For Term I Class XI 2023-24Document2 pagesSyllabus For Term I Class XI 2023-24licab58347No ratings yet

- Group Decision Support Systems (GDSS) : Sumit Ghunake (M.B.A.-I) Presented byDocument10 pagesGroup Decision Support Systems (GDSS) : Sumit Ghunake (M.B.A.-I) Presented bySumiit S GhunakeNo ratings yet

- Malunggaling Churros Business PlanDocument10 pagesMalunggaling Churros Business PlanPrincess Elizabeth ArañezNo ratings yet

- 2020dec18 AgendaDocument206 pages2020dec18 AgendanikerNo ratings yet

- MSHEM-02.11-C Level 2 JSA - Veolia - RO Units Pipes Repairing and ReplacementDocument6 pagesMSHEM-02.11-C Level 2 JSA - Veolia - RO Units Pipes Repairing and ReplacementAbdullah AbedNo ratings yet

- Call For Expression of InterestDocument19 pagesCall For Expression of InterestDavid PanNo ratings yet

- City Assessor of Cebu VSDocument6 pagesCity Assessor of Cebu VSLaw StudentNo ratings yet

- Asm 1 BUS3Document11 pagesAsm 1 BUS3Nguyễn Hà Phương100% (1)

- FSUU Board ResolutionDocument2 pagesFSUU Board ResolutionJudeRamos0% (1)

- How To Write Your Performance Objective Statements: Our Top TipsDocument2 pagesHow To Write Your Performance Objective Statements: Our Top TipsShruti KochharNo ratings yet

- GeM Bidding 3335448Document7 pagesGeM Bidding 3335448Bhumi ShahNo ratings yet

- Apple Inc - Research ReportDocument1 pageApple Inc - Research Reportapi-554762479No ratings yet

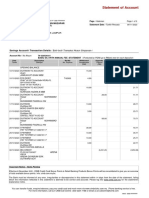

- Statement Cimb NovDocument3 pagesStatement Cimb NovfaqrullhNo ratings yet

- TR2394 - Handover of System From Project To AssetDocument16 pagesTR2394 - Handover of System From Project To Assetmaximusala83No ratings yet

- Sworn Declaration: Annex DDocument3 pagesSworn Declaration: Annex DellamanzonNo ratings yet

- 05q1 Ia1 Dela Cruz, Shiela Jane L (Bsa2a)Document3 pages05q1 Ia1 Dela Cruz, Shiela Jane L (Bsa2a)Alexandra JamesNo ratings yet

- MII BAMC Action ProjectDocument11 pagesMII BAMC Action ProjectAmar Mohamed AliNo ratings yet

- Riyadh Delhi: DLTJPQ CompleteDocument4 pagesRiyadh Delhi: DLTJPQ Completenaimi786No ratings yet

- Research Paper On DominosDocument4 pagesResearch Paper On Dominoshgrmzbikf100% (1)

- A Strategic Management ModelDocument5 pagesA Strategic Management ModelJamine Piper GaitaNo ratings yet

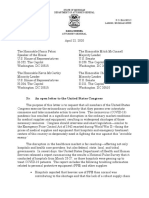

- Letter To U.S. CongressDocument8 pagesLetter To U.S. CongressWWMTNo ratings yet

- Tax Practice Math Solution PDFDocument1 pageTax Practice Math Solution PDFnurulaminNo ratings yet

- Macalit - Top 10 Real Estate Developers in The PhilippinesDocument6 pagesMacalit - Top 10 Real Estate Developers in The Philippinesaira catubagNo ratings yet