You might also like

- Withholding Tax Regime-PaksitanDocument2 pagesWithholding Tax Regime-Paksitanusmansss_606776863No ratings yet

- Ind As 12: Income Taxes: Current Tax Temporary Difference: TaxableDocument2 pagesInd As 12: Income Taxes: Current Tax Temporary Difference: Taxablechandrakumar k pNo ratings yet

- TDS VDS Rate Thorugh FA 2017.pdf 1348997815Document10 pagesTDS VDS Rate Thorugh FA 2017.pdf 1348997815Abu KawcherNo ratings yet

- Scope of TaxDocument12 pagesScope of TaxHajra MalikNo ratings yet

- Cfas - FinalsDocument9 pagesCfas - FinalsawitakintoNo ratings yet

- Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument8 pagesManila Cavite Laguna Cebu Cagayan de Oro DavaoRaymond RosalesNo ratings yet

- Far Eastern University: An Institute of Accounts Business and FinanceDocument5 pagesFar Eastern University: An Institute of Accounts Business and FinanceAcademic StuffNo ratings yet

- Income Taxes Lang HehezDocument8 pagesIncome Taxes Lang HehezDiana Rose BassigNo ratings yet

- Unit 6 - Preparation of Annua ITR BIR Compliance RequirementsDocument13 pagesUnit 6 - Preparation of Annua ITR BIR Compliance RequirementsRomero Joseph AnthonyNo ratings yet

- Referencer For Quick Revision: Intermediate Course Paper-4: TaxationDocument15 pagesReferencer For Quick Revision: Intermediate Course Paper-4: TaxationRamNo ratings yet

- All TaxesDocument9 pagesAll TaxesJv FerminNo ratings yet

- Base Amonut Does Not Exceed-Tk. 50 Lakh/ - 3%. Exceeds 50 Lakh To 2 Crore - 5% Exceeds 2 Crore - 7%Document8 pagesBase Amonut Does Not Exceed-Tk. 50 Lakh/ - 3%. Exceeds 50 Lakh To 2 Crore - 5% Exceeds 2 Crore - 7%Mohammad BaratNo ratings yet

- Income TaxesDocument17 pagesIncome TaxesThomas HutahaeanNo ratings yet

- 2 Index For Withholding TaxDocument16 pages2 Index For Withholding TaxabbelleNo ratings yet

- CH16 Accounting For Income TaxDocument5 pagesCH16 Accounting For Income Taxeyayaya blablablaNo ratings yet

- For ReformatDocument49 pagesFor ReformatCid Benedict PabalanNo ratings yet

- Ias 12Document27 pagesIas 12Kuti KuriNo ratings yet

- Far.119 Income TaxDocument4 pagesFar.119 Income Taxjhon tupagNo ratings yet

- Withholding Income Tax Regime (WHT Rates Card) : Facilitation GuideDocument48 pagesWithholding Income Tax Regime (WHT Rates Card) : Facilitation GuideKamran KhanNo ratings yet

- Tax Inter Quick Referencer by ICAIDocument17 pagesTax Inter Quick Referencer by ICAITushar kumarNo ratings yet

- Income Tax: Full PFRS, Prfs For Smes & Pfrs For SesDocument15 pagesIncome Tax: Full PFRS, Prfs For Smes & Pfrs For SesChara etangNo ratings yet

- Income Tax: Cabria Cpa Review CenterDocument4 pagesIncome Tax: Cabria Cpa Review CenterMaeNo ratings yet

- This Study Resource Was: Cebu Cpar Center Inc. Unit 103, MGA Arcade, A.C. Cortes Ave., Mandaue CityDocument3 pagesThis Study Resource Was: Cebu Cpar Center Inc. Unit 103, MGA Arcade, A.C. Cortes Ave., Mandaue CityNhel AlvaroNo ratings yet

- Chapter 7-Gross IncomeDocument5 pagesChapter 7-Gross Incomesha marananNo ratings yet

- Accounting For Income TaxDocument12 pagesAccounting For Income Taxglrosaaa cNo ratings yet

- 2010 - Consolidated Tax CasesDocument18 pages2010 - Consolidated Tax CasesZairah Nichole PascacioNo ratings yet

- Ias 12 Income TaxesDocument70 pagesIas 12 Income Taxeszulfi100% (1)

- Income-Tax Law: A Capsule For Quick Recap: Chapter 9: Advance Tax and Tax Deduction at SourceDocument5 pagesIncome-Tax Law: A Capsule For Quick Recap: Chapter 9: Advance Tax and Tax Deduction at Sourcem310235No ratings yet

- Budget 2023 Tax GuideDocument2 pagesBudget 2023 Tax GuideMichele RivarolaNo ratings yet

- TAX.3504 Withholding Tax SystemDocument17 pagesTAX.3504 Withholding Tax SystemMarinoNo ratings yet

- DIrect TaxDocument17 pagesDIrect Taxsureshkappe98No ratings yet

- MODULE 5 Final Income Taxation PDFDocument6 pagesMODULE 5 Final Income Taxation PDFJennifer AdvientoNo ratings yet

- Deferred Tax Accounting - Lecture NotesDocument6 pagesDeferred Tax Accounting - Lecture Notesmax pNo ratings yet

- Facilitation Guide: Withholding Tax Regime (Income Tax) Under The Income Tax Ordinance, 2001Document41 pagesFacilitation Guide: Withholding Tax Regime (Income Tax) Under The Income Tax Ordinance, 2001Raza312No ratings yet

- De La Salle Lipa: Intermediate Accounting 3 Income and Expense Items Affecting Deferred TaxesDocument4 pagesDe La Salle Lipa: Intermediate Accounting 3 Income and Expense Items Affecting Deferred TaxesJere Mae MarananNo ratings yet

- Penalty TAX: Ax Distinguished From Other ChargesDocument4 pagesPenalty TAX: Ax Distinguished From Other Chargesmaria cruzNo ratings yet

- Accounting V Tax TreatmentDocument3 pagesAccounting V Tax TreatmentReena MaNo ratings yet

- IAS 12 - Income TaxesDocument1 pageIAS 12 - Income TaxesFeras ShreimNo ratings yet

- Income Tax BocDocument75 pagesIncome Tax BocJenica Anne DalaodaoNo ratings yet

- Eopt Act Comparative SummaryDocument6 pagesEopt Act Comparative Summarybbc.moniqueNo ratings yet

- Adobe Scan Mar 11, 2021Document14 pagesAdobe Scan Mar 11, 2021Jul A.No ratings yet

- Ind AS 12 EIRC 10.10.2022Document44 pagesInd AS 12 EIRC 10.10.2022Abhishek YadavNo ratings yet

- Corporation Returns. - Requirements Final Adjustment ReturnDocument3 pagesCorporation Returns. - Requirements Final Adjustment ReturnDevilleres Eliza DenNo ratings yet

- Income Tax Notes-IAS 12Document11 pagesIncome Tax Notes-IAS 12mehdi.jjh313No ratings yet

- Gross Income 2019Document11 pagesGross Income 2019mysterymieNo ratings yet

- Strategic Tax Management Notes - CMA ReviewerDocument10 pagesStrategic Tax Management Notes - CMA ReviewerAngelly EsguerraNo ratings yet

- TAXATION I - Income Tax (Word)Document24 pagesTAXATION I - Income Tax (Word)Jerald-Edz Tam AbonNo ratings yet

- Income Taxes Far Reviwer NotesDocument15 pagesIncome Taxes Far Reviwer Notesabb.reviewersNo ratings yet

- CLWTAXN Module 4 Principles of Income Taxation (Income Tax Notes) v012024-1Document7 pagesCLWTAXN Module 4 Principles of Income Taxation (Income Tax Notes) v012024-1kdcngan162No ratings yet

- Chpater 5 - Final Income TaxationDocument31 pagesChpater 5 - Final Income TaxationKeziah YpilNo ratings yet

- Last Minute Notes DeductionDocument2 pagesLast Minute Notes DeductionPrincess Helen Grace BeberoNo ratings yet

- Referencer For Quick Revision: Intermediate Course Paper-4: TaxationDocument24 pagesReferencer For Quick Revision: Intermediate Course Paper-4: TaxationHinduja KumarNo ratings yet

- Tax FinalsDocument4 pagesTax FinalsNikki Beverly G. BacaleNo ratings yet

- IAS 12 Income TaxDocument43 pagesIAS 12 Income TaxMinal BihaniNo ratings yet

- M2 - Taxes, Tax Laws and Tax AdministrationDocument31 pagesM2 - Taxes, Tax Laws and Tax AdministrationTERRIUS AceNo ratings yet

- Pas 12Document2 pagesPas 12JennicaBailonNo ratings yet

- FAR.2835 Income Taxes PDFDocument7 pagesFAR.2835 Income Taxes PDFNah HamzaNo ratings yet

- Remedies in TaxationDocument8 pagesRemedies in TaxationabcyuiopNo ratings yet

- Chapter 4 - Accounting For Other LiabilitiesDocument21 pagesChapter 4 - Accounting For Other Liabilitiesjeanette lampitoc0% (1)

- Creating Advertising Programe Message, Headlines, Copy, LogoDocument18 pagesCreating Advertising Programe Message, Headlines, Copy, LogoHiren ShahNo ratings yet

- PHP KF Ma ASDocument32 pagesPHP KF Ma ASEat BestNo ratings yet

- Consolidation Intercompany Sale of Fixed AssetsDocument4 pagesConsolidation Intercompany Sale of Fixed AssetsEdma Glory MacadaagNo ratings yet

- EnrollmentDocument4 pagesEnrollmentJet Boclaras100% (1)

- Presentasi Executive Search Firstasia ConsultantsDocument11 pagesPresentasi Executive Search Firstasia ConsultantsNatasha FebryanaNo ratings yet

- Ifs GMP Checklist Pac enDocument9 pagesIfs GMP Checklist Pac enCevdet BEŞENNo ratings yet

- BBM 115 Introduction To Microeconomics-1Document115 pagesBBM 115 Introduction To Microeconomics-1Kevin KE100% (4)

- The Rampant Case of Unemployment in The PhilippinesDocument3 pagesThe Rampant Case of Unemployment in The PhilippinesTomas DocaNo ratings yet

- Class 13 PDFDocument26 pagesClass 13 PDFNilufar Yasmin AhmedNo ratings yet

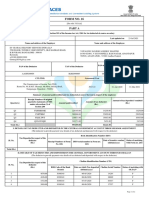

- Form No. 16: Part ADocument6 pagesForm No. 16: Part AVinuthna ChinnapaNo ratings yet

- SMU V500R003C10SPC018T Upgrade GuideDocument9 pagesSMU V500R003C10SPC018T Upgrade GuideDmitry PodkovyrkinNo ratings yet

- Mcdonal's Finanical RatiosDocument11 pagesMcdonal's Finanical RatiosFahad Khan TareenNo ratings yet

- Why You Want To Become An EntrepreneurDocument3 pagesWhy You Want To Become An Entrepreneursiddhant jainNo ratings yet

- 1.1. PNC PRE FO 66 Proposed Student Research Topics 2.1Document9 pages1.1. PNC PRE FO 66 Proposed Student Research Topics 2.1ALWINA CATINDOYNo ratings yet

- ALARP - Demonstration STD - AUSDocument24 pagesALARP - Demonstration STD - AUSMahfoodh Al AsiNo ratings yet

- Homework On Inventories Problem 1 (Borrowing Cost ConceptsDocument3 pagesHomework On Inventories Problem 1 (Borrowing Cost ConceptsJazehl Joy ValdezNo ratings yet

- Jakki Mohr, Sanjit Sengupta, Stanley Slater Marketing of High-Technology Products and InnovationsDocument569 pagesJakki Mohr, Sanjit Sengupta, Stanley Slater Marketing of High-Technology Products and InnovationsArshed Rosales100% (3)

- Test Bank For Financial Management Principles and Applications 10th Edition by KeownDocument19 pagesTest Bank For Financial Management Principles and Applications 10th Edition by KeownPria Aji PamungkasNo ratings yet

- InvestmentDocument3 pagesInvestmentAngelica PagaduanNo ratings yet

- ChackaoDocument13 pagesChackaoChackaNo ratings yet

- Strategic Management ProjectDocument9 pagesStrategic Management ProjectUsama AdenwalaNo ratings yet

- ICSI Guidelines Name Change Name ProprietorshipConcern Firm of PCS 2020Document4 pagesICSI Guidelines Name Change Name ProprietorshipConcern Firm of PCS 2020Nitin CSNo ratings yet

- Scientia L 2023Document244 pagesScientia L 2023john umaru rikkaNo ratings yet

- 1.2 Introduction To Cash ManagementDocument8 pages1.2 Introduction To Cash Managementasmamatha23No ratings yet

- To Update Your Contact Details, Kindly Call 1800-103-2292 (Toll Free)Document9 pagesTo Update Your Contact Details, Kindly Call 1800-103-2292 (Toll Free)Rajesh RamaswamyNo ratings yet

- Infosys-A Case Study Decision SheetDocument3 pagesInfosys-A Case Study Decision SheetRAW STARNo ratings yet

- (FIX) FOH Budget and COGS BudgetDocument26 pages(FIX) FOH Budget and COGS BudgetAlifia Zulfa SalsabilaNo ratings yet

- 2 ABBOT VS. NLRC G.R. No. 76959 October 12, 1987Document2 pages2 ABBOT VS. NLRC G.R. No. 76959 October 12, 1987Kornessa ParasNo ratings yet

- Leadership of Woman President in The Philippine State Universities and CollegesDocument14 pagesLeadership of Woman President in The Philippine State Universities and CollegesAPJAET JournalNo ratings yet

- Price Per Visit Quantity Demanded Quantity SuppliedDocument4 pagesPrice Per Visit Quantity Demanded Quantity SuppliedGrace FranzNo ratings yet