You might also like

- Make Money With Dividends Investing, With Less Risk And Higher ReturnsFrom EverandMake Money With Dividends Investing, With Less Risk And Higher ReturnsNo ratings yet

- Filled Patient & Employee Details - Hospital Details With Stamp and Signatur Is Mandatory. Should Be Compulsare Carry at The Time of Claim SubmissionDocument1 pageFilled Patient & Employee Details - Hospital Details With Stamp and Signatur Is Mandatory. Should Be Compulsare Carry at The Time of Claim SubmissionVaibhav NagarNo ratings yet

- Aerodynamic Design Analysis of A UAV For PDFDocument15 pagesAerodynamic Design Analysis of A UAV For PDFDreamer MakerNo ratings yet

- SALN LONG BlankDocument3 pagesSALN LONG BlankPeache Nadenne LopezNo ratings yet

- Bargi (Rani Avanti Bai Lodhi Sagar) Major Irrigation Project BriefDocument6 pagesBargi (Rani Avanti Bai Lodhi Sagar) Major Irrigation Project BriefGovind M.PNo ratings yet

- ANATOMYDocument7 pagesANATOMYNicole Xyza JunsayNo ratings yet

- HG GRAD 6 MODULE 4 Laid Out FINALDocument13 pagesHG GRAD 6 MODULE 4 Laid Out FINALArlene IgnacioNo ratings yet

- TB SR Implementation Guideline-Clean-FinalDocument64 pagesTB SR Implementation Guideline-Clean-FinalRam GhartiNo ratings yet

- 7.2 Clinical and US Anatomy: 7.2.1 Anterior ArmDocument15 pages7.2 Clinical and US Anatomy: 7.2.1 Anterior ArmLucas GuadaNo ratings yet

- Tutorial 2A - Introduction To Ms ExcelDocument8 pagesTutorial 2A - Introduction To Ms ExcelAMIRAH AWATIF MOHD ZAINNo ratings yet

- ON1 Effects LogDocument46 pagesON1 Effects LogRasol SadiqNo ratings yet

- WWW Slideshare Net Kumar008 Bajaj-ContentsDocument14 pagesWWW Slideshare Net Kumar008 Bajaj-ContentsPRINCE ARYANo ratings yet

- Marketing ProjectDocument31 pagesMarketing ProjectSai KashidNo ratings yet

- Evaluation Models: Viewpoints EducationalDocument18 pagesEvaluation Models: Viewpoints EducationalVLad2385No ratings yet

- Flipkart Labels 09 Sep 2023 01 19Document22 pagesFlipkart Labels 09 Sep 2023 01 19Fungaming ZoneNo ratings yet

- Adobe Host File SampleDocument5 pagesAdobe Host File SampleMax Chu100% (1)

- Outdoor Weekend Opens This Friday: Tri-City TimesDocument26 pagesOutdoor Weekend Opens This Friday: Tri-City TimesWoodsNo ratings yet

- Sub-Project Proposal Batch Iii: Technological and Professional Skills Development Sector Project (TPSDP)Document69 pagesSub-Project Proposal Batch Iii: Technological and Professional Skills Development Sector Project (TPSDP)Berkah Fajar Tamtomo KionoNo ratings yet

- Unicharm - Prospectus 2016-2018Document350 pagesUnicharm - Prospectus 2016-2018re faNo ratings yet

- Beacon Center Healthcare ReportDocument5 pagesBeacon Center Healthcare ReportFOX 17 News Digital StaffNo ratings yet

- Lecture44 - 16827 - A. OpenGLDocument28 pagesLecture44 - 16827 - A. OpenGLsumayya shaikNo ratings yet

- Notice RHQ 06032023Document135 pagesNotice RHQ 06032023Touhidur RahamanNo ratings yet

- Hikcentral Professional Isup Device Accessing Operation Guide v2.1.0Document30 pagesHikcentral Professional Isup Device Accessing Operation Guide v2.1.0Christopher LaputNo ratings yet

- Junos® OS Protocol-Independent Routing Properties Feature GuideDocument524 pagesJunos® OS Protocol-Independent Routing Properties Feature GuideayheytNo ratings yet

- Deloitte Price Forecast Oil & Gas Mar 2022Document28 pagesDeloitte Price Forecast Oil & Gas Mar 2022rodrigo belloNo ratings yet

- CES Scope of Work For Dallas Housing Policy Development Project HOPPE 5.12.22Document5 pagesCES Scope of Work For Dallas Housing Policy Development Project HOPPE 5.12.22April ToweryNo ratings yet

- SDS NITOFLOR SL1000 IndiaDocument29 pagesSDS NITOFLOR SL1000 IndiaMaha MuflehNo ratings yet

- A Constitutive Model For Partially Saturated Soils: Gcotechnique 40, No. 3,405-430Document26 pagesA Constitutive Model For Partially Saturated Soils: Gcotechnique 40, No. 3,405-430Aivy Jinneth CutaNo ratings yet

- Well Known TMDocument4 pagesWell Known TMDrunk funNo ratings yet

- Professional PracticeDocument29 pagesProfessional Practicetanya mohantyNo ratings yet

- MFL67477506 - English + HindiDocument38 pagesMFL67477506 - English + HindiFarhanNo ratings yet

- Curriculum Vitae: Tejas H. PanchalDocument8 pagesCurriculum Vitae: Tejas H. PanchalTejas Panchal100% (1)

- Fdocuments - in - Pre Joining GuidelinesDocument19 pagesFdocuments - in - Pre Joining GuidelinesPrincy poojaNo ratings yet

- HR Policy GgialDocument38 pagesHR Policy GgialAkash ChauhanNo ratings yet

- Ebook DOZEROAOS10Kdeseguidores 2021Document60 pagesEbook DOZEROAOS10Kdeseguidores 2021CamilaBruschNo ratings yet

- Communicating Science - A Practical Guide For Engineers and Physical Scientists (2017)Document284 pagesCommunicating Science - A Practical Guide For Engineers and Physical Scientists (2017)Ahmed LordNo ratings yet

- Sree Rayalseema Alkalies 16 5077530316Document75 pagesSree Rayalseema Alkalies 16 5077530316HitechSoft HitsoftNo ratings yet

- Ford Vehicle RecallDocument4 pagesFord Vehicle RecallNational Content DeskNo ratings yet

- GEO292 Doc 4Document4 pagesGEO292 Doc 4Àlfin FahdiraNo ratings yet

- Ecpg OrlapDocument258 pagesEcpg OrlapNoha Ibraheem HelmyNo ratings yet

- MuskanDocument33 pagesMuskanRishabh TripathiNo ratings yet

- Xerox - History, Products, & Facts - BritannicaDocument8 pagesXerox - History, Products, & Facts - BritannicanguyentuandangNo ratings yet

- A+ Blog - SSLC - Model Theory Questions - 2023 - emDocument37 pagesA+ Blog - SSLC - Model Theory Questions - 2023 - emhadiyxxNo ratings yet

- CellMolBio RevisionDocument11 pagesCellMolBio RevisionChristianAvelinoNo ratings yet

- DB2 Web Query For I The Nuts and BoltsDocument224 pagesDB2 Web Query For I The Nuts and BoltsNicolás TrepinNo ratings yet

- Base Carbon: Initiating Coverage With An Outperform (Speculative) RatingDocument23 pagesBase Carbon: Initiating Coverage With An Outperform (Speculative) RatingJim McIntyreNo ratings yet

- Thinking Beyond PIN CodesDocument9 pagesThinking Beyond PIN CodesSenthil kumar NatarajanNo ratings yet

- Dollar Appreciation Vs Indian Rupee It's Impact On Indian EconomyDocument51 pagesDollar Appreciation Vs Indian Rupee It's Impact On Indian EconomyBharti PunjabiNo ratings yet

- 5.23.2023 School Resource Officers AgreementDocument11 pages5.23.2023 School Resource Officers AgreementJennifer CuevasNo ratings yet

- PROOFED - Press Conference Deck v4Document32 pagesPROOFED - Press Conference Deck v4sameh aboulsoudNo ratings yet

- Aug 22-24,2022 DLLDocument16 pagesAug 22-24,2022 DLLCy DacerNo ratings yet

- KCBS-KCAL EEO Public File Report 8-1-21 To 7-22!22!1Document8 pagesKCBS-KCAL EEO Public File Report 8-1-21 To 7-22!22!1TatyanaNo ratings yet

- Project Monitoring System: in NTPCDocument38 pagesProject Monitoring System: in NTPCTrilok Singh TakuliNo ratings yet

- Solution To Q2Document19 pagesSolution To Q2apurv43No ratings yet

- DP 25179Document504 pagesDP 25179R. NikhithaNo ratings yet

- SOPEPDocument3 pagesSOPEPPOOJA KUMARINo ratings yet

- 1 - Geopraphy Chapter - 1 (With Answer) Natural ResourcesDocument2 pages1 - Geopraphy Chapter - 1 (With Answer) Natural Resourcesshiva nagarNo ratings yet

- Pengaruh Penerapan Sistem Administrasi Perpajakan Modern Terhadap Tingkat Kepatuhan Wajib Pajak Di KPP Pratama Makassar Selatan (3) - 1Document70 pagesPengaruh Penerapan Sistem Administrasi Perpajakan Modern Terhadap Tingkat Kepatuhan Wajib Pajak Di KPP Pratama Makassar Selatan (3) - 1Fitri YurnaningsihNo ratings yet

- ECON163 Example 10Document7 pagesECON163 Example 10Meisy AnjaliNo ratings yet

- Tutorial Review-3Document37 pagesTutorial Review-3Nguyên HoàngNo ratings yet

- Practice 4 - ECON1010Document7 pagesPractice 4 - ECON1010sonNo ratings yet

- Practice 7 - ECON1010Document10 pagesPractice 7 - ECON1010sonNo ratings yet

- Practice 9 - ECON1010Document13 pagesPractice 9 - ECON1010sonNo ratings yet

- SPORT in KOREA History DevelopDocument2 pagesSPORT in KOREA History DevelopsonNo ratings yet

- IEA ReadingDocument314 pagesIEA ReadingsonNo ratings yet

- 11b1-Mid Term 2 - Revision GuidelinesDocument9 pages11b1-Mid Term 2 - Revision GuidelinessonNo ratings yet

- Entry 7-1Document8 pagesEntry 7-1sonNo ratings yet

- Strikingly, Waterproof Mobile Phones Are Quite Common in Japan, As Many Teenagers Use Them Even in TheDocument1 pageStrikingly, Waterproof Mobile Phones Are Quite Common in Japan, As Many Teenagers Use Them Even in ThesonNo ratings yet

- INTERNATIONAL TRADE AND ITS IMPLICATION FOR UGANDA ECONOMY AssignmentDocument14 pagesINTERNATIONAL TRADE AND ITS IMPLICATION FOR UGANDA ECONOMY Assignmentwandera samuel njoyaNo ratings yet

- Hyundai PPT AmitDocument17 pagesHyundai PPT AmitAmit RauniyarNo ratings yet

- Buat PPT Liat Jurnal Eproc, Penerapan Lean Manufacturing (PDF), Bookmark Di ChromeDocument1 pageBuat PPT Liat Jurnal Eproc, Penerapan Lean Manufacturing (PDF), Bookmark Di ChromeJoice MargarethaNo ratings yet

- Jurnal Internasional Nilai Tukar PDFDocument12 pagesJurnal Internasional Nilai Tukar PDFRexalNo ratings yet

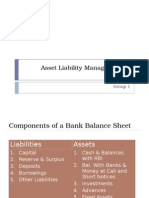

- Asset Liability Management in Banks: Group 1Document29 pagesAsset Liability Management in Banks: Group 1AjDonNo ratings yet

- Project Analysis and EvaluationDocument3 pagesProject Analysis and Evaluationsakibsultan_308No ratings yet

- Decision Making Relevant CostingDocument78 pagesDecision Making Relevant Costingmmattiullah584100% (1)

- MGMT3030-BSG Strategic AuditDocument16 pagesMGMT3030-BSG Strategic AuditKelcey McCuaigNo ratings yet

- MP 102Document238 pagesMP 102shruti1806No ratings yet

- R3 Reports: Fedcoin: A Central Bank-Issued CryptocurrencyDocument30 pagesR3 Reports: Fedcoin: A Central Bank-Issued CryptocurrencyFranco Emilio100% (1)

- Break-Even Analysis Basic Concepts and Linear Profit AnalysisDocument9 pagesBreak-Even Analysis Basic Concepts and Linear Profit AnalysisJelian E. TangaroNo ratings yet

- Nature & Scope of MEDocument13 pagesNature & Scope of MEMr.K.Chandra BoseNo ratings yet

- Lecture 2Document53 pagesLecture 2Siddhartha AgarwalNo ratings yet

- Auditing Derivatives: Middle Office (Valuation)Document4 pagesAuditing Derivatives: Middle Office (Valuation)Jasvinder JosenNo ratings yet

- The Role of Islamic Cooperatives in Developing SocietiesDocument9 pagesThe Role of Islamic Cooperatives in Developing SocietiesdiraNo ratings yet

- Pengantar Ekonomi Mikro - Ten PrinciplesDocument4 pagesPengantar Ekonomi Mikro - Ten PrinciplesAyu AndhyraNo ratings yet

- The Transformation of Contemporary China Studies, 1977-2002Document19 pagesThe Transformation of Contemporary China Studies, 1977-2002annsaralondeNo ratings yet

- D. N. Dwivedi - Microeconomics-I - (2012)Document373 pagesD. N. Dwivedi - Microeconomics-I - (2012)68 Jainam100% (1)

- 0450 s13 QP 13Document12 pages0450 s13 QP 13Pramudith LiyanageNo ratings yet

- ST 4th Qtr. AppliedDocument2 pagesST 4th Qtr. AppliedXian GuzmanNo ratings yet

- CH 9Document17 pagesCH 9muhammadifan2210No ratings yet

- CF Unit 2 Solutions 09-01-2022Document22 pagesCF Unit 2 Solutions 09-01-2022SuganyaNo ratings yet

- NCERT-class 12-Eco-Summary (Part 2) PDFDocument26 pagesNCERT-class 12-Eco-Summary (Part 2) PDFrahul pawarNo ratings yet

- Masters Company Currently Produces Cereal Targeted To Consumers Over 40 Years OldDocument1 pageMasters Company Currently Produces Cereal Targeted To Consumers Over 40 Years OldAbdulla Al MuhairiNo ratings yet

- Participating in The Dynamic Business EnvironmentDocument19 pagesParticipating in The Dynamic Business EnvironmentReader100% (1)

- Module 2 L2 Pest AnalysisDocument2 pagesModule 2 L2 Pest AnalysisBLOCK 8 / TAMAYO / K.No ratings yet

- Class 11 FinalTerm SyllabusDocument5 pagesClass 11 FinalTerm SyllabusMayank Kumar BhagatNo ratings yet

- Master of Business Administration (Mba)Document56 pagesMaster of Business Administration (Mba)s.muthu100% (1)

- Basic Appraisal Principles: Course DescriptionDocument7 pagesBasic Appraisal Principles: Course Descriptionnaren_3456No ratings yet

- Optimum Currency Areas and The European Experience: ECO41 International Economics Udayan RoyDocument57 pagesOptimum Currency Areas and The European Experience: ECO41 International Economics Udayan RoyБежовска СањаNo ratings yet