You might also like

- Managerial Economics Assignment No: 1 Name: Sharada Raut PRN: 09020446006Document6 pagesManagerial Economics Assignment No: 1 Name: Sharada Raut PRN: 09020446006sharadararautNo ratings yet

- Capital GainDocument9 pagesCapital Gainbarakkat72No ratings yet

- Securities Transaction Tax (STT)Document9 pagesSecurities Transaction Tax (STT)koushiki mishraNo ratings yet

- Tax On Mutual FundsDocument7 pagesTax On Mutual FundsPramod KumarNo ratings yet

- NRI Saving GuideDocument4 pagesNRI Saving GuidemeenaNo ratings yet

- Capital GainDocument4 pagesCapital GainrichaNo ratings yet

- 9 Dec... 3 ArticlesDocument9 pages9 Dec... 3 Articlesavinash sharmaNo ratings yet

- Advisorkhoj ICICI Prudential Mutual Fund ArticleDocument6 pagesAdvisorkhoj ICICI Prudential Mutual Fund ArticleBIJAY KRISHNA DASNo ratings yet

- Stocks: Tax Free Government BondsDocument4 pagesStocks: Tax Free Government BondsRavi SinghNo ratings yet

- Direct Tax CodeDocument8 pagesDirect Tax CodeImran HassanNo ratings yet

- Aa TaxDocument22 pagesAa Taxnirshan rajNo ratings yet

- Corrigendum To MFD - WB Version Dec 2019 - Chapter 8 - Effective From 31mar2020Document14 pagesCorrigendum To MFD - WB Version Dec 2019 - Chapter 8 - Effective From 31mar2020Manish MahatoNo ratings yet

- Taxation 12Document13 pagesTaxation 12surajspammsNo ratings yet

- Getting Started With TradingDocument24 pagesGetting Started With TradingmoumonaNo ratings yet

- Capital GainsDocument25 pagesCapital GainsanonymousNo ratings yet

- Taxation Regulations IndiaDocument6 pagesTaxation Regulations IndiaSiddhant WaliaNo ratings yet

- Self Employed: TRN Requirements For Sole ProprietorsDocument14 pagesSelf Employed: TRN Requirements For Sole ProprietorsAnonymous imWQ1y63No ratings yet

- NOTES 5 - Income Tax 601 - BBA-6 SemDocument24 pagesNOTES 5 - Income Tax 601 - BBA-6 Semmkv status100% (1)

- Taxation Matters Relating To Securities and DerivativesDocument60 pagesTaxation Matters Relating To Securities and DerivativesAnjali JainNo ratings yet

- Income Tax Part ADocument23 pagesIncome Tax Part AVishwas AgarwalNo ratings yet

- All About TAX in Financial Year 2009Document44 pagesAll About TAX in Financial Year 2009themeditatorNo ratings yet

- What Are ESOPs and How Are They TaxedDocument3 pagesWhat Are ESOPs and How Are They TaxedDevdatta NaikNo ratings yet

- Tax Capital Gain Mcom Project of 31 OagesDocument33 pagesTax Capital Gain Mcom Project of 31 Oageskarthika kounder50% (6)

- All About TAX in Financial Year 2009 - 2010Document44 pagesAll About TAX in Financial Year 2009 - 2010pradeep mathurNo ratings yet

- Ifp 32 Capital Gain PDFDocument7 pagesIfp 32 Capital Gain PDFMoh. Farid Adi PamujiNo ratings yet

- Income Tax Assessment SemDocument10 pagesIncome Tax Assessment SemB SIBA PRASAD REDDYNo ratings yet

- Value Added Tax Black Book 2 2332Document47 pagesValue Added Tax Black Book 2 2332sanket yelaweNo ratings yet

- Taxation of Debt InstrumentsDocument15 pagesTaxation of Debt InstrumentsPunyak SatishNo ratings yet

- I Have Done IntraDocument4 pagesI Have Done IntraNeeraj KhandelwalNo ratings yet

- Presentation - FINANCIAL INSTRUMENTSDocument12 pagesPresentation - FINANCIAL INSTRUMENTSnareshNo ratings yet

- Taxation in Mutual FundsDocument16 pagesTaxation in Mutual Fundsvineetb553No ratings yet

- Investment Management#2 2010Document34 pagesInvestment Management#2 2010M M PanditNo ratings yet

- Capital Gain in Indian Tax System: Income From Capital GainsDocument3 pagesCapital Gain in Indian Tax System: Income From Capital GainsvikramkukrejaNo ratings yet

- 12 DTC PresentationDocument19 pages12 DTC PresentationPunit BhandariNo ratings yet

- Taxation in Mutual FundsDocument18 pagesTaxation in Mutual Fundsvineetb553No ratings yet

- Tax Reckoner 2011Document3 pagesTax Reckoner 2011Bunuanu SamadNo ratings yet

- 413sol3 04Document17 pages413sol3 04drtoeNo ratings yet

- Deloitte DTC Impact FIIDocument5 pagesDeloitte DTC Impact FIIGs ShikshaNo ratings yet

- Income From Capital Gains (2017 IT Act)Document9 pagesIncome From Capital Gains (2017 IT Act)AjayNo ratings yet

- Tax EfficientDocument22 pagesTax EfficientBrijesh NagarNo ratings yet

- Name: Mehreen Khan ENROLL NO:01-112171-013 Submitted To: Mam Amal Khan Subject: Advance TaxationDocument7 pagesName: Mehreen Khan ENROLL NO:01-112171-013 Submitted To: Mam Amal Khan Subject: Advance TaxationMehreen KhanNo ratings yet

- Income TaxDocument47 pagesIncome TaxSaurabhSinghYadavNo ratings yet

- WM AssignmentDocument5 pagesWM Assignmentvunnam manoharNo ratings yet

- Tax PlanningDocument28 pagesTax PlanningDishaNo ratings yet

- Mutual Funds - NRIDocument3 pagesMutual Funds - NRIsmc.universalNo ratings yet

- How To Calculate Profitability Ratios For BanksDocument5 pagesHow To Calculate Profitability Ratios For BanksMohsin JuttNo ratings yet

- An Introduction To The Enterprise Investment Scheme (EIS) - UKDocument13 pagesAn Introduction To The Enterprise Investment Scheme (EIS) - UKWeAreKopiNo ratings yet

- About The ExpertDocument7 pagesAbout The ExpertAnurag RanbhorNo ratings yet

- NISM Series 5A Chapter 8Document12 pagesNISM Series 5A Chapter 8sachinaman.2016No ratings yet

- 8 SMART Ways To Lower Your Tax LiabilityDocument6 pages8 SMART Ways To Lower Your Tax LiabilityansplanetNo ratings yet

- A Simple Guide To Fixed DepositDocument1 pageA Simple Guide To Fixed DepositchiragdedhiaNo ratings yet

- Author Ayan Ahmed Blog Capital Gain in FranceDocument5 pagesAuthor Ayan Ahmed Blog Capital Gain in FranceAYAN AHMEDNo ratings yet

- Mutual Funds Taxation Rules FY 2020-21 - Capital Gains & DividendsDocument7 pagesMutual Funds Taxation Rules FY 2020-21 - Capital Gains & DividendsSushant ChhotrayNo ratings yet

- Direct Tax Code: Kunal Vora Bhavik BhanderiDocument11 pagesDirect Tax Code: Kunal Vora Bhavik BhanderiBhavik BhanderiNo ratings yet

- Vaishnavi ProjectDocument72 pagesVaishnavi ProjectAkshada DhapareNo ratings yet

- 1tax Planning For Retirees of IOB 1Document34 pages1tax Planning For Retirees of IOB 1mail2ncNo ratings yet

- Basics of Personal FinanceDocument15 pagesBasics of Personal FinanceAnjali TejaniNo ratings yet

- TaxationDocument7 pagesTaxationAkshatNo ratings yet

- DTC - FinalDocument18 pagesDTC - FinalvjranavjNo ratings yet

- Whats NewDocument3 pagesWhats Newphani raja kumarNo ratings yet

- Leelavati Service Tax ReturnDocument6 pagesLeelavati Service Tax Returnphani raja kumarNo ratings yet

- Star Health Assure - One Pager - Version 1.0 - April - 2022Document3 pagesStar Health Assure - One Pager - Version 1.0 - April - 2022Shihb100% (1)

- Test AttachmentDocument1 pageTest Attachmentphani raja kumarNo ratings yet

- ACT Invoice FOR JANDocument2 pagesACT Invoice FOR JANphani raja kumarNo ratings yet

- Practical Aspects of Availing Credit in Respect of Invoices Not Appearing in Form GSTR 2A or GSTR 2BDocument6 pagesPractical Aspects of Availing Credit in Respect of Invoices Not Appearing in Form GSTR 2A or GSTR 2Bphani raja kumarNo ratings yet

- Compendium of MSMEDocument65 pagesCompendium of MSMEChaitra KatragaddaNo ratings yet

- Stampduty For Firm ReconstitutionDocument2 pagesStampduty For Firm Reconstitutionphani raja kumarNo ratings yet

- Vat 112Document2 pagesVat 112phani raja kumarNo ratings yet

- Socieity Registration Required DetailsDocument1 pageSocieity Registration Required Detailsphani raja kumarNo ratings yet

- Affidavit For Society Registration For Own House Amma PremashramDocument1 pageAffidavit For Society Registration For Own House Amma Premashramphani raja kumarNo ratings yet

- Incorporation of CompanyDocument4 pagesIncorporation of Companyphani raja kumarNo ratings yet

- I Disabled HiberfilDocument3 pagesI Disabled Hiberfilphani raja kumarNo ratings yet

- Income Tax Scrutiny NormsDocument6 pagesIncome Tax Scrutiny Normsphani raja kumarNo ratings yet

- Impact of Non Submission of Export Intimation Within The Prescribed Time in Case of ct-3Document6 pagesImpact of Non Submission of Export Intimation Within The Prescribed Time in Case of ct-3phani raja kumarNo ratings yet

- Central Excise Job Work RulesDocument3 pagesCentral Excise Job Work RulesSameer HusainNo ratings yet

- Some Important Aspects of HUF Under Income Tax, 1961Document16 pagesSome Important Aspects of HUF Under Income Tax, 1961phani raja kumarNo ratings yet

- Compensation Under RR Act and Vijayawada Rural DetailsDocument2 pagesCompensation Under RR Act and Vijayawada Rural Detailsphani raja kumarNo ratings yet

- ICSI E-Bulletin MAY - JUNE 2014Document59 pagesICSI E-Bulletin MAY - JUNE 2014phani raja kumarNo ratings yet

- GOODS SOLD ON MRP BASIS IS EXEMPTED FROM SERVICE TAX Circular No.173 - 8 - 2013 - ST, Dated 07-10-2013Document1 pageGOODS SOLD ON MRP BASIS IS EXEMPTED FROM SERVICE TAX Circular No.173 - 8 - 2013 - ST, Dated 07-10-2013phani raja kumarNo ratings yet

- How To Claim Income Tax Refund of TDS For Last Six YearsDocument1 pageHow To Claim Income Tax Refund of TDS For Last Six Yearsphani raja kumarNo ratings yet

- Channels ListDocument2 pagesChannels Listphani raja kumarNo ratings yet

- Verification of Applicant in Case of Form DIN-1 As Per Annexure I of The DIN RulesDocument1 pageVerification of Applicant in Case of Form DIN-1 As Per Annexure I of The DIN Rulesphani raja kumarNo ratings yet

- Central Excise Duty Rates Chapter Wise Changes in Budget 2015-16Document34 pagesCentral Excise Duty Rates Chapter Wise Changes in Budget 2015-16phani raja kumarNo ratings yet

- APPT RegistrationDocument2 pagesAPPT Registrationphani raja kumarNo ratings yet

- Acception of Cforms After Issuing of Assessment Order Godrej Agrovet CaseDocument1 pageAcception of Cforms After Issuing of Assessment Order Godrej Agrovet Casephani raja kumarNo ratings yet

- Rectification ManualDocument25 pagesRectification Manualwww.TdsTaxIndia.comNo ratings yet

- Chapter 61 Central ExciseDocument1 pageChapter 61 Central Excisephani raja kumarNo ratings yet

- Cii1981 2011Document1 pageCii1981 2011Ritesh AgarwalNo ratings yet

- CH 3Document9 pagesCH 3yebegashet67% (3)

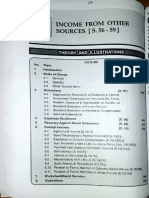

- Income From Other Sources (FA Module)Document22 pagesIncome From Other Sources (FA Module)kalyaniraghuwashiNo ratings yet

- Cir v. Traders Royal BankDocument17 pagesCir v. Traders Royal BankPauline100% (1)

- Anjali Bisht V-ADocument77 pagesAnjali Bisht V-AAnjali BishtNo ratings yet

- Double Taxation AssignmentDocument12 pagesDouble Taxation AssignmentVishal Salwan100% (1)

- Justice and EqualityDocument2 pagesJustice and EqualityLovlesh RubyNo ratings yet

- Benchmarking The Performance of The Duterte Administration Year 1 Full ReportDocument20 pagesBenchmarking The Performance of The Duterte Administration Year 1 Full ReportThe Movement for Good Governance (MGG)No ratings yet

- Unit 1 Online Services Danial AhmedDocument19 pagesUnit 1 Online Services Danial Ahmedapi-567993949No ratings yet

- Mini CooperDocument5 pagesMini CooperzavrisNo ratings yet

- Form 16Document4 pagesForm 16Premeshor LaishramNo ratings yet

- Waller County Appraisal DistrictDocument4 pagesWaller County Appraisal DistrictO'Connor AssociateNo ratings yet

- L2-Characteristics and Importance of Tourism IndustryDocument5 pagesL2-Characteristics and Importance of Tourism Industryraymart fajiculayNo ratings yet

- Bruhat Bengaluru Mahanagara Palike - Revenue Department: Xjdœ LXD - /HZ Eud/ Eĺ Lbx¡E (6 E LDocument1 pageBruhat Bengaluru Mahanagara Palike - Revenue Department: Xjdœ LXD - /HZ Eud/ Eĺ Lbx¡E (6 E LGovinda RajuNo ratings yet

- Delhi 1 - ReportDocument23 pagesDelhi 1 - ReportArjun PradhanNo ratings yet

- Ch08 Property, Plant & EquipmentDocument6 pagesCh08 Property, Plant & EquipmentregenNo ratings yet

- EY Budget Flash 2021Document12 pagesEY Budget Flash 2021Anam IqbalNo ratings yet

- Sai 1484Document4 pagesSai 1484NSPOLY ASHOKNo ratings yet

- Servet Mutlu-Late Ottoman PopulationDocument39 pagesServet Mutlu-Late Ottoman Populationaokan@hotmail.com100% (1)

- TDS ChalanDocument1 pageTDS ChalanRAKHAL BAIRAGINo ratings yet

- Tax Law II Research PaperDocument24 pagesTax Law II Research PaperK.MeghanaNo ratings yet

- 6 Comparing AlternativesDocument49 pages6 Comparing AlternativesTrimar DagandanNo ratings yet

- Swot Analysis - IKEADocument7 pagesSwot Analysis - IKEAAaltu FaltuNo ratings yet

- 2021 Ifrs Coa BasicDocument6 pages2021 Ifrs Coa BasicAnn MayNo ratings yet

- 2007 Summer Great Peninsula Conservancy NewsletterDocument8 pages2007 Summer Great Peninsula Conservancy NewsletterGreat Peninsula ConservancyNo ratings yet

- BSBFIN501 Assessment Manual V2.0Document16 pagesBSBFIN501 Assessment Manual V2.0andrevian600100% (1)

- Project - Impact of GST On Indian Economy - Logistic SectorDocument63 pagesProject - Impact of GST On Indian Economy - Logistic SectorParveen Dsouza50% (4)

- Cir vs. Philam LifeDocument1 pageCir vs. Philam LifeRaquel Doquenia100% (1)

- Principal and Agent: Joseph E. StiglitzDocument13 pagesPrincipal and Agent: Joseph E. StiglitzRamiro EnriquezNo ratings yet

- Cir V Phil American DIGESTDocument3 pagesCir V Phil American DIGESTjannagotgoodNo ratings yet

- Kilosbayan v. Guingona Jr. G.R. No. 113375Document59 pagesKilosbayan v. Guingona Jr. G.R. No. 113375JinyoungPNo ratings yet