You might also like

- Government Accounting NotesDocument24 pagesGovernment Accounting Noteszee abadilla100% (1)

- Government Accounting: Accounting For Non-Profit OrganizationsDocument28 pagesGovernment Accounting: Accounting For Non-Profit OrganizationsDe GuzmanNo ratings yet

- Credit TransactionsDocument8 pagesCredit TransactionsLoyce Grace MorenteNo ratings yet

- ATFX Advantages: Regulated Broker with MT4 PlatformDocument39 pagesATFX Advantages: Regulated Broker with MT4 PlatformNurul Mutmainnah NadarNo ratings yet

- Chapter 2Document19 pagesChapter 2robert matutinaNo ratings yet

- Accounting for Budgetary AccountsDocument63 pagesAccounting for Budgetary Accountselisha mae cardeñoNo ratings yet

- Chapter 1 Acct09Document3 pagesChapter 1 Acct09Joseph LapasandaNo ratings yet

- Government Accounting: Accounting For Non-Profit OrganizationsDocument88 pagesGovernment Accounting: Accounting For Non-Profit OrganizationsDe GuzmanNo ratings yet

- Government Exam Notes 1-3Document8 pagesGovernment Exam Notes 1-3Joseph LapasandaNo ratings yet

- Group 1 Budget ProcessDocument26 pagesGroup 1 Budget ProcessCassie ParkNo ratings yet

- Government Budget ProcessDocument5 pagesGovernment Budget ProcessSteffany RoqueNo ratings yet

- Chapter 1 Acct09Document8 pagesChapter 1 Acct09Joseph LapasandaNo ratings yet

- Government Budget ProcessDocument16 pagesGovernment Budget Processmaria ronoraNo ratings yet

- Copy 7 ACP 313 QuickNotes On Government AccountingDocument10 pagesCopy 7 ACP 313 QuickNotes On Government AccountingRodken VallenteNo ratings yet

- New Government Accounting System (NGAS) OverviewDocument20 pagesNew Government Accounting System (NGAS) OverviewIsiah Jarrett Trinidad Abille100% (1)

- Government Accounting SystemDocument46 pagesGovernment Accounting SystemMeshack NyekelelaNo ratings yet

- Gov Acc 2019 JaaDocument9 pagesGov Acc 2019 JaaGlaiza Lerio100% (1)

- Government Accounting OverviewDocument18 pagesGovernment Accounting OverviewCherrie Arianne Fhaye Naraja100% (1)

- Actgnp Rev.Document11 pagesActgnp Rev.Krizah Marie CaballeroNo ratings yet

- Diaz Haidie R Assessment 1Document3 pagesDiaz Haidie R Assessment 1Christel OrugaNo ratings yet

- Government Accounting PunzalanDocument5 pagesGovernment Accounting PunzalanN Jo88% (17)

- Government AccountingDocument7 pagesGovernment AccountingErica EgidaNo ratings yet

- NOTESDocument2 pagesNOTESJñelle Faith Herrera SaludaresNo ratings yet

- Chapter 1 - New Government Accounting System (Ngas)Document28 pagesChapter 1 - New Government Accounting System (Ngas)MA ValdezNo ratings yet

- Lesson 1,2 and 3 1 and 2: Introduction To Government AccountingDocument5 pagesLesson 1,2 and 3 1 and 2: Introduction To Government Accountingyen claveNo ratings yet

- Overview of Government AccountingDocument2 pagesOverview of Government Accountingwhin LimboNo ratings yet

- Government Accounting Auditing & ProcurementDocument97 pagesGovernment Accounting Auditing & Procurementjamie c100% (1)

- Task Performance-Gov T Acctg - PrelimDocument5 pagesTask Performance-Gov T Acctg - PrelimAnonymouslyNo ratings yet

- Chapter 1 - Overview of Government AccountingDocument4 pagesChapter 1 - Overview of Government AccountingChris tine Mae MendozaNo ratings yet

- Chapter 1 - Nature and Scope of NGASDocument26 pagesChapter 1 - Nature and Scope of NGASJapsNo ratings yet

- Why Accounting is Essential for Government: A 40-Character SummaryDocument14 pagesWhy Accounting is Essential for Government: A 40-Character SummaryJoanna TiuzenNo ratings yet

- Prelim-ExaminationDocument8 pagesPrelim-Examinationshi shiiisshh100% (1)

- New Government Accounting System (NGAS) in The PhilippinesDocument24 pagesNew Government Accounting System (NGAS) in The PhilippinesJingRellin100% (1)

- Gov Acc Post TestDocument15 pagesGov Acc Post Test수지No ratings yet

- Governmental Entities: Introduction and General Fund Accounting Chapter 17Document99 pagesGovernmental Entities: Introduction and General Fund Accounting Chapter 17IKRAR AGUNG DEWANTORO 12119072No ratings yet

- Chapter 1 Nature and Scope of NGASDocument26 pagesChapter 1 Nature and Scope of NGASRia BagoNo ratings yet

- GA - Assessment 1Document2 pagesGA - Assessment 1Christel OrugaNo ratings yet

- AC316 Module 8Document5 pagesAC316 Module 8Jaime PalizardoNo ratings yet

- An Introduction An Introduction: Nature and Scope of Accounting For Government and Non-Profit OrganizationsDocument38 pagesAn Introduction An Introduction: Nature and Scope of Accounting For Government and Non-Profit OrganizationsPhrexilyn PajarilloNo ratings yet

- Sec. 1. Legal Basis. The Government Accounting Manual (GAM) Is Prescribed by COADocument3 pagesSec. 1. Legal Basis. The Government Accounting Manual (GAM) Is Prescribed by COAElla Mae TuratoNo ratings yet

- Government Accounting ManualDocument9 pagesGovernment Accounting ManualGabriel PonceNo ratings yet

- Public Sector Accounting: CUAC 406 by ChengeramangaDocument101 pagesPublic Sector Accounting: CUAC 406 by ChengeramangaTanyahl MatumbikeNo ratings yet

- Chapter 1Document68 pagesChapter 1Merrill Ojeda SaflorNo ratings yet

- Government Accounting (AFA-II) : Governmental Entities: Introduction and General Fund AccountingDocument8 pagesGovernment Accounting (AFA-II) : Governmental Entities: Introduction and General Fund AccountingMd. Rejaul Ahsan Chowdhury100% (1)

- Government AccountingDocument13 pagesGovernment AccountingReniella Villondo100% (1)

- Government Accounting Punzalan SolmanDocument4 pagesGovernment Accounting Punzalan SolmanAlarich Catayoc100% (1)

- Acctg For GovernmentDocument12 pagesAcctg For GovernmentNurse NotesNo ratings yet

- On Audit:: Government Accounting Manual (Gam) PointersDocument9 pagesOn Audit:: Government Accounting Manual (Gam) PointersPepsi ColaNo ratings yet

- Chapter 1Document8 pagesChapter 1Adan EveNo ratings yet

- Financial Statements OverviewDocument36 pagesFinancial Statements OverviewIrvin OngyacoNo ratings yet

- 1.maintenance of AccountsDocument32 pages1.maintenance of AccountsShahid ShafiNo ratings yet

- 2, Conceptual FrameworkDocument14 pages2, Conceptual FrameworkkarismaNo ratings yet

- Government Accounting Reviewer Chapter 1: General Provisions, Basic Standards and PoliciesDocument5 pagesGovernment Accounting Reviewer Chapter 1: General Provisions, Basic Standards and PoliciesPatricia GalvezNo ratings yet

- Note 1 - MEC 34Document7 pagesNote 1 - MEC 34S GracsNo ratings yet

- GAS-21 - Accounting for Income, Collections and Related TransactionsDocument21 pagesGAS-21 - Accounting for Income, Collections and Related TransactionsBenzon Agojo OndovillaNo ratings yet

- Chapter 1 Ethiopian Govt AcctingDocument22 pagesChapter 1 Ethiopian Govt AcctingwubeNo ratings yet

- GOVERNMENT ACCOUNTING FUNDAMENTALSDocument22 pagesGOVERNMENT ACCOUNTING FUNDAMENTALSDaniel CalmaNo ratings yet

- Government AccountingDocument93 pagesGovernment Accountingpilonia.donitarosebsa1993No ratings yet

- Chapter 1 Overview of Government AccountingDocument4 pagesChapter 1 Overview of Government AccountingSteffany Roque100% (1)

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- MAS 2023 Module 5 Standard Costing and Variance AnalysisDocument20 pagesMAS 2023 Module 5 Standard Costing and Variance AnalysisDzulija TalipanNo ratings yet

- Principles of TaxationDocument13 pagesPrinciples of TaxationHazel OrtegaNo ratings yet

- MAS 2023 Module3 Cost Volume Profit AnalysisDocument10 pagesMAS 2023 Module3 Cost Volume Profit AnalysisDzulija TalipanNo ratings yet

- Module On SalesDocument17 pagesModule On SalesDzulija TalipanNo ratings yet

- MAS 2023 Module3 Cost Volume Profit AnalysisDocument10 pagesMAS 2023 Module3 Cost Volume Profit AnalysisDzulija TalipanNo ratings yet

- ABC Costing Problem 1Document2 pagesABC Costing Problem 1Dzulija TalipanNo ratings yet

- The Law On Sales Agency and Credit TransDocument5 pagesThe Law On Sales Agency and Credit TransIke100% (1)

- MAS 2023 Module 5 Standard Costing and Variance AnalysisDocument20 pagesMAS 2023 Module 5 Standard Costing and Variance AnalysisDzulija Talipan100% (1)

- AFAR 2303 Cost Accounting-1Document30 pagesAFAR 2303 Cost Accounting-1Dzulija TalipanNo ratings yet

- Job Order Costing ProblemsDocument1 pageJob Order Costing ProblemsDzulija TalipanNo ratings yet

- AFAR 2306 - Home Office, Branch & Agency AcctgDocument5 pagesAFAR 2306 - Home Office, Branch & Agency AcctgDzulija TalipanNo ratings yet

- AFAR 2305 Not-for-Profit OrganizationsDocument14 pagesAFAR 2305 Not-for-Profit OrganizationsDzulija TalipanNo ratings yet

- Consumer Protection ActDocument8 pagesConsumer Protection ActDzulija TalipanNo ratings yet

- Afar2303b Service Cost Allocation Cost AccountingDocument1 pageAfar2303b Service Cost Allocation Cost AccountingDzulija TalipanNo ratings yet

- Case 3 - Wallys Billboard Sign SupplyDocument2 pagesCase 3 - Wallys Billboard Sign SupplyDzulija TalipanNo ratings yet

- IAS 28 Investment in AssociatesDocument7 pagesIAS 28 Investment in AssociatesDzulija TalipanNo ratings yet

- ADVACC 1 AssignDocument3 pagesADVACC 1 AssignDzulija TalipanNo ratings yet

- 5 - FAAC Rules PDFDocument4 pages5 - FAAC Rules PDFDzulija TalipanNo ratings yet

- Advacc1 Accounting For Special Transactions (Advanced Accounting 1)Document21 pagesAdvacc1 Accounting For Special Transactions (Advanced Accounting 1)Dzulija TalipanNo ratings yet

- 5 - FAAC Rules PDFDocument4 pages5 - FAAC Rules PDFDzulija TalipanNo ratings yet

- Advacc1 Accounting For Special Transactions (Advanced Accounting 1)Document24 pagesAdvacc1 Accounting For Special Transactions (Advanced Accounting 1)Dzulija Talipan100% (1)

- ADVACC 1 AssignDocument3 pagesADVACC 1 AssignDzulija TalipanNo ratings yet

- Partial Topics AccountingDocument51 pagesPartial Topics AccountingDzulija Talipan100% (1)

- Clarifying Tax Rules for Homeowners' Association DuesDocument2 pagesClarifying Tax Rules for Homeowners' Association DuesMarieal InotNo ratings yet

- MSC Actuarial Science May2011Document18 pagesMSC Actuarial Science May2011Kalaiarasan GovindarasuNo ratings yet

- 2020-02-29 IFR Asia - UnknownDocument42 pages2020-02-29 IFR Asia - UnknownqbichNo ratings yet

- The Enron Corporation Story Depicts A Company That Reached Dizzying Heights Only To Plummet DramaticallyDocument2 pagesThe Enron Corporation Story Depicts A Company That Reached Dizzying Heights Only To Plummet DramaticallySi Reygie Rojas KoNo ratings yet

- PT Gajah Tunggal Tbk Financial Risk Analysis 2016-2020Document26 pagesPT Gajah Tunggal Tbk Financial Risk Analysis 2016-2020Ananda LukmanNo ratings yet

- SAT exam instructions and questionsDocument11 pagesSAT exam instructions and questionskrishnaNo ratings yet

- Acknowledgement FormDocument3 pagesAcknowledgement FormfafcoNo ratings yet

- Orsted Q3 2023 Investor PresentationDocument44 pagesOrsted Q3 2023 Investor Presentationshen.wangNo ratings yet

- Income Tax Rates PDFDocument1 pageIncome Tax Rates PDFAditi SharmaNo ratings yet

- Ali Asghar Textile Mills LTD: Ratios: TotalDocument7 pagesAli Asghar Textile Mills LTD: Ratios: TotalakhlaqjatoiNo ratings yet

- Emrm5103 (Project Risk Management)Document54 pagesEmrm5103 (Project Risk Management)syahrifendi100% (3)

- Directors Report 2011 12 WCLDocument146 pagesDirectors Report 2011 12 WCLsarvesh.bhartiNo ratings yet

- Essential GST Audit ChecklistDocument3 pagesEssential GST Audit ChecklistBaiju DevNo ratings yet

- Afar ToaDocument22 pagesAfar ToaVanessa Anne Acuña DavisNo ratings yet

- Nick Leeson Barings BankDocument32 pagesNick Leeson Barings Bankdonald.g.white100% (1)

- MCQ 3Document6 pagesMCQ 3Senthil Kumar Ganesan100% (1)

- Compre ExamDocument11 pagesCompre Examena20_paderangaNo ratings yet

- Topic 3 Long-Term Construction Contracts ModuleDocument20 pagesTopic 3 Long-Term Construction Contracts ModuleMaricel Ann BaccayNo ratings yet

- Go.151 Leave Travel Concession-Ltc-RulesDocument3 pagesGo.151 Leave Travel Concession-Ltc-RulesVanagantinaveen Kumar100% (1)

- 21 Republic Vs de GUzman PDFDocument22 pages21 Republic Vs de GUzman PDFShivaNo ratings yet

- Jobberman INV-018126 PDFDocument2 pagesJobberman INV-018126 PDFnfplacideNo ratings yet

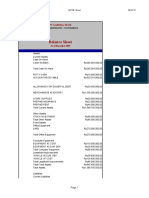

- PT Garuda Tech December 2019 Balance SheetDocument2 pagesPT Garuda Tech December 2019 Balance SheetSMKJTRGNo ratings yet

- PartnershipDocument8 pagesPartnershipOllie WattsNo ratings yet

- Rule 39 Section 9 (B) : Satisfaction by LevyDocument8 pagesRule 39 Section 9 (B) : Satisfaction by LevyLeo Balante Escalante Jr.No ratings yet

- Raw DataDocument28 pagesRaw DataMaya IstiNo ratings yet

- CapstoneDocument29 pagesCapstonelajjo1230% (1)

- Cost of Capital PDFDocument34 pagesCost of Capital PDFMathilda UllyNo ratings yet

- Pivot Point Trading StrategyDocument8 pagesPivot Point Trading StrategyBadrul 'boxer' Hisham50% (4)

- Financing of Constructed FacilitiesDocument24 pagesFinancing of Constructed FacilitiesLyka TanNo ratings yet