You might also like

- PO 200316 - Burdette EngineeringDocument12 pagesPO 200316 - Burdette EngineeringMacon AtkinsonNo ratings yet

- Revised Dell T440 Server ProposalDocument3 pagesRevised Dell T440 Server ProposalJulie Nombra TolosaNo ratings yet

- Facebook India Online Services Pvt. LTD., Purchase Order: SupplierDocument9 pagesFacebook India Online Services Pvt. LTD., Purchase Order: SupplierVamsheeNo ratings yet

- Factura Comercial 8967367614Document2 pagesFactura Comercial 8967367614crazytaino100% (1)

- Top of Form Panel 0 4 None 0 0: Legal Name: Social Security NumberDocument2 pagesTop of Form Panel 0 4 None 0 0: Legal Name: Social Security NumberJason RileyNo ratings yet

- US1099Forms - Form 1099-NEC Copy BDocument2 pagesUS1099Forms - Form 1099-NEC Copy BSaurabh ChandraNo ratings yet

- Sprinturf Po 8373789Document2 pagesSprinturf Po 8373789freestategalNo ratings yet

- Barack Obama Foundation Annual Filing Statement New York 2014Document54 pagesBarack Obama Foundation Annual Filing Statement New York 2014Jerome CorsiNo ratings yet

- Paula Atkins 17881 Thelma Ave Apt A Jupiter, FL 33458 Claimant ID: 226330Document2 pagesPaula Atkins 17881 Thelma Ave Apt A Jupiter, FL 33458 Claimant ID: 226330Natural Beauty LaserNo ratings yet

- New Haven Purchase OrderDocument4 pagesNew Haven Purchase OrderHelen BennettNo ratings yet

- Purchase OrderDocument2 pagesPurchase OrderkheioNo ratings yet

- 31-Jul-2019 GT/PO/072019/5228: PO. No Date Purchase OrderDocument1 page31-Jul-2019 GT/PO/072019/5228: PO. No Date Purchase OrderShiv KannanNo ratings yet

- Title MaxDocument1 pageTitle MaxHumayon MalekNo ratings yet

- Check For InvestigationDocument1 pageCheck For InvestigationWTSP 10No ratings yet

- Earnings StatementDocument1 pageEarnings Statementkrmita OrtizNo ratings yet

- Screenshot 2022-03-09 at 10.35.55 AM PDFDocument2 pagesScreenshot 2022-03-09 at 10.35.55 AM PDFjNo ratings yet

- Rockport Police DepartmentDocument2 pagesRockport Police DepartmentRyan GarzaNo ratings yet

- Fall 2023 - Tax ProjectDocument4 pagesFall 2023 - Tax Projectacwriters123No ratings yet

- Profit or Loss From Business: Schedule C (Form 1040) 09Document2 pagesProfit or Loss From Business: Schedule C (Form 1040) 09Braeylnn bookerNo ratings yet

- A218 DocumentDocument9 pagesA218 DocumentJose AlmonteNo ratings yet

- Windward Fund's 2018 Tax FormsDocument49 pagesWindward Fund's 2018 Tax FormsJoe SchoffstallNo ratings yet

- Pyw223s EeDocument1 pagePyw223s Eedanielman956No ratings yet

- Account # 0302080036: Lifegreen SavingsDocument2 pagesAccount # 0302080036: Lifegreen Savingsstorage mediaNo ratings yet

- U.S. Individual Income Tax Return: Standard DeductionDocument3 pagesU.S. Individual Income Tax Return: Standard DeductionAkNo ratings yet

- Statement For Recipients of Pandemic Unemployment Assistance (Pua) Payments PUA-1099GDocument1 pageStatement For Recipients of Pandemic Unemployment Assistance (Pua) Payments PUA-1099GClifton WilsonNo ratings yet

- Monetary Determination Pandemic Unemployment Assistance: Michael L PresleyDocument3 pagesMonetary Determination Pandemic Unemployment Assistance: Michael L PresleyDylan VanslochterenNo ratings yet

- 1481546265426Document3 pages1481546265426api-370784582No ratings yet

- 21 0008 I OIG Report - CsDocument12 pages21 0008 I OIG Report - CsChris BerinatoNo ratings yet

- CFID 1253 Reseller CertificateDocument2 pagesCFID 1253 Reseller Certificatewaqar chNo ratings yet

- Earnings Statement: Zalena K Mcclenic 11 Sixth ST Westbury, Ny 11590Document1 pageEarnings Statement: Zalena K Mcclenic 11 Sixth ST Westbury, Ny 11590mellishagrant11No ratings yet

- 2021 TaxReturnDocument9 pages2021 TaxReturnTerry ParkerNo ratings yet

- Is in Kind 03-16-09Document1 pageIs in Kind 03-16-09Azi PaybarahNo ratings yet

- No Fear!Document3 pagesNo Fear!mikeNo ratings yet

- 2007 Carl & Ruth Shapiro Family Foundation 990 (Includes Madoff Investment)Document42 pages2007 Carl & Ruth Shapiro Family Foundation 990 (Includes Madoff Investment)jpeppard100% (4)

- Cash FlowDocument1 pageCash Flowpawan_019No ratings yet

- 2020-2021 Financial StatementsDocument51 pages2020-2021 Financial StatementsKyra GillespieNo ratings yet

- 1120 Sample TranscriptDocument3 pages1120 Sample TranscriptEmily KnightNo ratings yet

- 1 5136803172601299942 PDFDocument3 pages1 5136803172601299942 PDFnurulamin00023No ratings yet

- Isucu Tony FulkDocument5 pagesIsucu Tony Fulkkramergeorgec397No ratings yet

- Combo 637648692875701670Document8 pagesCombo 637648692875701670Sanjeev VermaNo ratings yet

- Rounds July FECDocument119 pagesRounds July FECPat PowersNo ratings yet

- 202212-Tax Return Transcript-DARA-104758594023Document7 pages202212-Tax Return Transcript-DARA-104758594023tironatirona455No ratings yet

- Liz Martyr May April 2020 FECDocument26 pagesLiz Martyr May April 2020 FECPat PowersNo ratings yet

- f133 PDFDocument1 pagef133 PDFfaresNo ratings yet

- Standard Form 180Document3 pagesStandard Form 180Nancy CunninghamNo ratings yet

- PayStatement 1000139864Document1 pagePayStatement 1000139864ash.payan123No ratings yet

- Fold Here Cut Along Edge: Please Use The Printed Insurance Cards Below. Please Use The Printed Insurance Cards BelowDocument2 pagesFold Here Cut Along Edge: Please Use The Printed Insurance Cards Below. Please Use The Printed Insurance Cards BelowKim PortantNo ratings yet

- 1013 ALC Quotation ALCSN201029001 20201111080153Document2 pages1013 ALC Quotation ALCSN201029001 20201111080153TRABAJANDIÑO PEREZNo ratings yet

- 3509-27 Page Boulevard - National Register of Historic Places Registration FormDocument45 pages3509-27 Page Boulevard - National Register of Historic Places Registration FormnextSTL.comNo ratings yet

- California Insurance ID Card Effective DDocument1 pageCalifornia Insurance ID Card Effective DD BNo ratings yet

- 1099 G 2018documentdownloadDocument1 page1099 G 2018documentdownloadKristine McVeighNo ratings yet

- Christine Jones Jan. 31, 2014 Arizona Campaign Finance ReportDocument70 pagesChristine Jones Jan. 31, 2014 Arizona Campaign Finance Reportpaul weich100% (1)

- Mund Oct. QuarterlyDocument24 pagesMund Oct. QuarterlyRob PortNo ratings yet

- Financial Statements 1Document19 pagesFinancial Statements 1bhawnaNo ratings yet

- Peaster V McDonalds LawsuitDocument34 pagesPeaster V McDonalds LawsuitRobert GarciaNo ratings yet

- David Crockett High SchoolDocument5 pagesDavid Crockett High SchoolWCYB DigitalNo ratings yet

- 12 SCH B2 Cottonwood MLDocument20 pages12 SCH B2 Cottonwood MLLandon HemsleyNo ratings yet

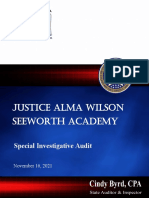

- Seeworth Academy 21 Web FinalDocument52 pagesSeeworth Academy 21 Web FinalKFORNo ratings yet

- CU Free Style Ski Team Investigation ReportDocument7 pagesCU Free Style Ski Team Investigation ReportSarah KutaNo ratings yet

- Gcu Budget Review SD 3Document5 pagesGcu Budget Review SD 3api-606300511No ratings yet

- Public School Security Grant - District AllocationsDocument6 pagesPublic School Security Grant - District AllocationsWZTV Digital StaffNo ratings yet

- Lawsuit: BlueCross BlueShield of Tennessee Denied Workers Religious Exemptions From COVID-19 Vaccine MandateDocument14 pagesLawsuit: BlueCross BlueShield of Tennessee Denied Workers Religious Exemptions From COVID-19 Vaccine MandateDan LehrNo ratings yet

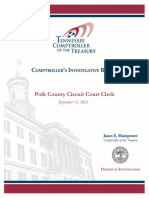

- Polk County Circuit Court Clerk ReportDocument11 pagesPolk County Circuit Court Clerk ReportDan LehrNo ratings yet

- 'Nefarious' Attorneys General Say Popular Clothes Website SHEIN May Be Exploiting Its WorkersDocument4 pages'Nefarious' Attorneys General Say Popular Clothes Website SHEIN May Be Exploiting Its WorkersDan LehrNo ratings yet

- Judge Denies Janet Hinds AppealDocument54 pagesJudge Denies Janet Hinds AppealDan LehrNo ratings yet

- Heart Institute Data LawsuitDocument60 pagesHeart Institute Data LawsuitDan LehrNo ratings yet

- MGT Building Assessment Scores For Hamilton Co. Schools (2019)Document425 pagesMGT Building Assessment Scores For Hamilton Co. Schools (2019)Dan LehrNo ratings yet

- Read: Pilot Error Caused LIFE FORCE Helicopter Crash in March, NTSB Final Report SaysDocument5 pagesRead: Pilot Error Caused LIFE FORCE Helicopter Crash in March, NTSB Final Report SaysDan LehrNo ratings yet

- Padilla Govt BriefDocument16 pagesPadilla Govt BriefDan LehrNo ratings yet

- Lawsuit: Biosolids Transport Company Claims Chattanooga Didn't Live Up To Its ContractDocument26 pagesLawsuit: Biosolids Transport Company Claims Chattanooga Didn't Live Up To Its ContractDan LehrNo ratings yet

- 6 New Changes To TSSAA's Bylaws, Passed July 13th, 2023Document3 pages6 New Changes To TSSAA's Bylaws, Passed July 13th, 2023Dan LehrNo ratings yet

- Chattanooga Biosolids Disposal On Four Farms. 3 in Warren and 1 in Van Buren. NOV and Site Photo Document SignedDocument14 pagesChattanooga Biosolids Disposal On Four Farms. 3 in Warren and 1 in Van Buren. NOV and Site Photo Document SignedDan LehrNo ratings yet

- Release: Hamilton County WWTA To Address 50-Year-Old Sanitary Sewer Problems On Signal MountainDocument1 pageRelease: Hamilton County WWTA To Address 50-Year-Old Sanitary Sewer Problems On Signal MountainDan LehrNo ratings yet

- Read: Pilot Error Caused LIFE FORCE Helicopter Crash in March, NTSB Final Report SaysDocument5 pagesRead: Pilot Error Caused LIFE FORCE Helicopter Crash in March, NTSB Final Report SaysDan LehrNo ratings yet

- Majority Opinion - Benjamin Scott Brewer v. State of Tennessee - E2022-01191-CCA-R3-PCDocument15 pagesMajority Opinion - Benjamin Scott Brewer v. State of Tennessee - E2022-01191-CCA-R3-PCDan LehrNo ratings yet

- Court of AppealsDocument14 pagesCourt of AppealsAnita WadhwaniNo ratings yet

- Map Oakley Catoosa WMA Courtesy The Conservation FundDocument1 pageMap Oakley Catoosa WMA Courtesy The Conservation FundDan LehrNo ratings yet

- Read The Lawsuit: Chattanooga Woman Sues FBI For Failing To Prevent 1979 Death of Her Informant FatherDocument18 pagesRead The Lawsuit: Chattanooga Woman Sues FBI For Failing To Prevent 1979 Death of Her Informant FatherDan LehrNo ratings yet

- Melody Sasser Criminal ComplaintDocument13 pagesMelody Sasser Criminal ComplaintLeigh EganNo ratings yet

- Read: Settlement With US XpressDocument44 pagesRead: Settlement With US XpressDan LehrNo ratings yet

- 2023-306 Winter Storm Elliott After-Action Public Report-FNL2Document15 pages2023-306 Winter Storm Elliott After-Action Public Report-FNL2Dan Lehr100% (1)

- FireworksDocument27 pagesFireworksDan LehrNo ratings yet

- Padilla Defense BriefDocument4 pagesPadilla Defense BriefDan LehrNo ratings yet

- Read: Proposed New Cellphone Policy For Hamilton County SchoolsDocument2 pagesRead: Proposed New Cellphone Policy For Hamilton County SchoolsDan LehrNo ratings yet

- PIT 2023 InfographicDocument1 pagePIT 2023 InfographicDan LehrNo ratings yet

- Menifee Transcript 1Document32 pagesMenifee Transcript 1Dan LehrNo ratings yet

- TN-TWS Position Protection of Wildlife 2023Document1 pageTN-TWS Position Protection of Wildlife 2023Dan LehrNo ratings yet

- Menifee Transcript 1Document32 pagesMenifee Transcript 1Dan LehrNo ratings yet

- Recommended Policy Actions To Reduce Gun Violence in TennesseeDocument4 pagesRecommended Policy Actions To Reduce Gun Violence in TennesseeAnonymous GF8PPILW5No ratings yet

- PIT Count 2023 SnapshotDocument1 pagePIT Count 2023 SnapshotDan LehrNo ratings yet

- Sickness PDFDocument15 pagesSickness PDFpurva maratheNo ratings yet

- Brosur & Harga Perumahan Lavon Swan City 2020Document32 pagesBrosur & Harga Perumahan Lavon Swan City 2020Wahyudi PurnamaNo ratings yet

- Chapter12 Managing and Pricing Deposit ServicesDocument26 pagesChapter12 Managing and Pricing Deposit ServicesTừ Lê Lan HươngNo ratings yet

- SMDP - Project LogisticsDocument15 pagesSMDP - Project LogisticsDimas Arie KusumoNo ratings yet

- Gysum ProjectDocument77 pagesGysum ProjectPrasanta SarmaNo ratings yet

- Double Irish Dutch Sandwich and The Indian Transfer Pricing LawDocument20 pagesDouble Irish Dutch Sandwich and The Indian Transfer Pricing LawRahaMan ShaikNo ratings yet

- Financial ManagementDocument2 pagesFinancial ManagementArun ReddyNo ratings yet

- Alaudin Khilji Market ReformsDocument11 pagesAlaudin Khilji Market ReformsArshita KanodiaNo ratings yet

- Flight Ticket - Hyderabad To Mumbai: Fare Rules & BaggageDocument2 pagesFlight Ticket - Hyderabad To Mumbai: Fare Rules & Baggageanvesh reddyNo ratings yet

- A Study On Consumer Preference Towards Red Label Tea Powder With Reference To Samrat Chowk, SolapurDocument10 pagesA Study On Consumer Preference Towards Red Label Tea Powder With Reference To Samrat Chowk, SolapurVasu ChenniappanNo ratings yet

- CCRIS Request Application and eCCRIS Registration FormDocument4 pagesCCRIS Request Application and eCCRIS Registration FormspermhellNo ratings yet

- Inter 56632 Oil Soft Offer FobDocument8 pagesInter 56632 Oil Soft Offer Fobisam mansouriNo ratings yet

- Rainfed AgricultureDocument4 pagesRainfed AgricultureMatthew Jacobs100% (1)

- Case Digest Chapter 4Document4 pagesCase Digest Chapter 4Marilie TubalinalNo ratings yet

- 13.product and Process Innovation NewDocument20 pages13.product and Process Innovation Newsetiyawanmuktiwijaya160902No ratings yet

- Notice of Related Case: Filed Under SealDocument5 pagesNotice of Related Case: Filed Under Sealmichael.mcsweeneyNo ratings yet

- Innovation and Entrepreneurship Antim PraharDocument15 pagesInnovation and Entrepreneurship Antim PraharHarshit garg100% (1)

- SafariDocument2 pagesSafariMowell MelindaNo ratings yet

- ORGANIZATIONAL CULTURE AutosavedDocument42 pagesORGANIZATIONAL CULTURE AutosavedAayush Niroula OfficialNo ratings yet

- SYAT Bookkeeping TutorialDocument35 pagesSYAT Bookkeeping TutorialJanelle MendozaNo ratings yet

- Shipper's Name and Address Air WaybillDocument2 pagesShipper's Name and Address Air Waybilledwinantony303No ratings yet

- XLSXDocument12 pagesXLSXicadeliciafebNo ratings yet

- Jury Summons Response LetterDocument3 pagesJury Summons Response LetterPaschal James BloiseNo ratings yet

- AX 2012 - ENUS - SMA - 01 - Service ManagementDocument6 pagesAX 2012 - ENUS - SMA - 01 - Service ManagementSubbu_kalNo ratings yet

- Absorption (Total) Costing: A2 Level Accounting - Resources, Past Papers, Notes, Exercises & QuizesDocument4 pagesAbsorption (Total) Costing: A2 Level Accounting - Resources, Past Papers, Notes, Exercises & QuizesAung Zaw HtweNo ratings yet

- Hoffman and Truck Drivers, Helpers & Warehouse Workers Pension Fund 5-15-89, 5-24-89, 6-12-89Document72 pagesHoffman and Truck Drivers, Helpers & Warehouse Workers Pension Fund 5-15-89, 5-24-89, 6-12-89E Frank CorneliusNo ratings yet

- Top Free Construction SoftwareDocument7 pagesTop Free Construction Softwarevenkateswara rao PothinaNo ratings yet

- A4 Business Model CanvasDocument1 pageA4 Business Model CanvasMusic Da LifeNo ratings yet

- Fixed Asset Capitalisation SopDocument3 pagesFixed Asset Capitalisation SopSHARADNo ratings yet

- 2nd Cedric Burl AmpDocument2 pages2nd Cedric Burl AmpCheryl LynnNo ratings yet