You might also like

- Press Release Page 22Document8 pagesPress Release Page 22sab390663No ratings yet

- Hightlights of Economic SurveyDocument8 pagesHightlights of Economic Surveypallavi pattnaikNo ratings yet

- Government of India: Press Information BureauDocument7 pagesGovernment of India: Press Information BureauRavi KumarNo ratings yet

- Pib - Gov.in-Press Information BureauDocument8 pagesPib - Gov.in-Press Information BureauCharlie WillsNo ratings yet

- Crack Grade B: A Brief History of The Economy SurveyDocument28 pagesCrack Grade B: A Brief History of The Economy SurveyShubhendu VermaNo ratings yet

- Economic Survey 2022: Why in News?Document15 pagesEconomic Survey 2022: Why in News?Sourav KumarNo ratings yet

- Press Information Bureau 2Document7 pagesPress Information Bureau 2Raghav StetaNo ratings yet

- Economic Survey 2021-22Document42 pagesEconomic Survey 2021-22bapatlaNo ratings yet

- Press Information BureauDocument7 pagesPress Information BureauCharlie WillsNo ratings yet

- Economic Survey Summary 2022-23 EnglishDocument2 pagesEconomic Survey Summary 2022-23 EnglishKavya KaurNo ratings yet

- Economic Survey 2021 22Document9 pagesEconomic Survey 2021 22ABHAY PARASHARNo ratings yet

- 09 BER 22 en Exe SummaryDocument5 pages09 BER 22 en Exe SummaryNasrin LubnaNo ratings yet

- Bangladesh Economic Review - Chapter 5Document20 pagesBangladesh Economic Review - Chapter 5Md. Abdur RakibNo ratings yet

- Economic Survey Summary2Document8 pagesEconomic Survey Summary2m_vamshikrishna22No ratings yet

- Economic Survey - 2021-22Document2 pagesEconomic Survey - 2021-22Sunil Kumar SalihundamNo ratings yet

- RBI - ANNUAL - REPORT - 2023 by Anuj Jindal - inDocument42 pagesRBI - ANNUAL - REPORT - 2023 by Anuj Jindal - inakverma3226No ratings yet

- Union Budget 2023Document13 pagesUnion Budget 2023RomaNo ratings yet

- Economic Survey 2022-23 HighlightsDocument6 pagesEconomic Survey 2022-23 HighlightsS ShenoyNo ratings yet

- National Budget Memorandum: Department OF Budget AND ManagementDocument6 pagesNational Budget Memorandum: Department OF Budget AND ManagementHallelujer CultNo ratings yet

- Economy Watch October 2021Document26 pagesEconomy Watch October 2021avinash tolaniNo ratings yet

- Economic Outlook April 2022 - v2Document7 pagesEconomic Outlook April 2022 - v2Dev ShahNo ratings yet

- EconomicsDocument21 pagesEconomicsvedha's preparationNo ratings yet

- Economic Survey 2023 Q44 ODocument136 pagesEconomic Survey 2023 Q44 Orambo kunjumonNo ratings yet

- Summary of Economic Survey 2022-23 EnglishDocument18 pagesSummary of Economic Survey 2022-23 EnglishRepublic WorldNo ratings yet

- Union Budget 2022-23 - A Journey Towards Economic RecoveryDocument8 pagesUnion Budget 2022-23 - A Journey Towards Economic Recoveryrvriteshverma13No ratings yet

- Bangladesh FOREXDocument11 pagesBangladesh FOREXJyotika BagNo ratings yet

- TOPIC:Trends of Government Expenditure in India During COVID-19 Pandemic: An OverviewDocument6 pagesTOPIC:Trends of Government Expenditure in India During COVID-19 Pandemic: An OverviewTANISHQNo ratings yet

- SafariDocument13 pagesSafariRohit RoyNo ratings yet

- Financial Stability Report June 2023Document10 pagesFinancial Stability Report June 2023asdfNo ratings yet

- Assingment On Monetory Policy DecisionDocument4 pagesAssingment On Monetory Policy DecisionDebargha SenguptaNo ratings yet

- Union Budget of India: HistoryDocument6 pagesUnion Budget of India: HistoryGOVIND JANGIDNo ratings yet

- EY Economy Watch - November 2022Document29 pagesEY Economy Watch - November 2022Harsha BandarlaNo ratings yet

- Current Affairs A3Document29 pagesCurrent Affairs A3AHSAN ANSARINo ratings yet

- Economy Watch February 2021Document28 pagesEconomy Watch February 2021Avinash GarjeNo ratings yet

- Economic Update March 2024Document11 pagesEconomic Update March 2024Kashf ShabbirNo ratings yet

- Fiscal Policy Statement FY 2023.24 - FinalDocument7 pagesFiscal Policy Statement FY 2023.24 - FinalAnubhav BhattaraiNo ratings yet

- Global Economic Scenario and About State Bank of India Work With Msme SBIDocument21 pagesGlobal Economic Scenario and About State Bank of India Work With Msme SBIkrishnanshu sarafNo ratings yet

- Nepal Macroeconomic Update 202209 PDFDocument30 pagesNepal Macroeconomic Update 202209 PDFRajendra NeupaneNo ratings yet

- Economic Update December 2022Document12 pagesEconomic Update December 2022M A Khan FarazNo ratings yet

- 202112311640944707-Budget Strategy Paper 2022-25Document10 pages202112311640944707-Budget Strategy Paper 2022-25AbdulSalamNo ratings yet

- Economic Review 2023Document31 pagesEconomic Review 202317044 AZMAIN IKTIDER AKASHNo ratings yet

- Market Strategy: February 2021Document19 pagesMarket Strategy: February 2021Harshvardhan SurekaNo ratings yet

- Central Bank of Nigeria Communique No. 143 of The Monetary Policy Committee Meeting Held On Tuesday 19th JULY 2022Document11 pagesCentral Bank of Nigeria Communique No. 143 of The Monetary Policy Committee Meeting Held On Tuesday 19th JULY 2022IbukunNo ratings yet

- Economic Survey 2022 23Document48 pagesEconomic Survey 2022 23Shubham SinghNo ratings yet

- Central Bank of Nigeria Communiqué No. 146 of The Monetary Policy Committee Meeting Held On Monday 23 and Tuesday 24 JANUARY 2023Document70 pagesCentral Bank of Nigeria Communiqué No. 146 of The Monetary Policy Committee Meeting Held On Monday 23 and Tuesday 24 JANUARY 2023QS OH OladosuNo ratings yet

- Economic Review and Inflation Report November 2022Document29 pagesEconomic Review and Inflation Report November 2022Saneliso MotsaNo ratings yet

- Financial Stability Report December 2023 Lyst3567Document13 pagesFinancial Stability Report December 2023 Lyst3567tgtk8xgdx9No ratings yet

- World Bank 2023 India ReportDocument27 pagesWorld Bank 2023 India ReportMithilesh KumarNo ratings yet

- Economy Watch - December 2020Document29 pagesEconomy Watch - December 2020subham mohantyNo ratings yet

- Analysis of Pakistan's EconomyDocument9 pagesAnalysis of Pakistan's Economyserryserry362No ratings yet

- SBP Report Dec-2022Document2 pagesSBP Report Dec-2022usama iqbalNo ratings yet

- Economic Development Monthly Report Analysis of Indian EconomyDocument5 pagesEconomic Development Monthly Report Analysis of Indian EconomyMurali Krishna ReddyNo ratings yet

- Executive Summery - English-2020Document9 pagesExecutive Summery - English-2020M Tariqul Islam MishuNo ratings yet

- National Budget Memorandum No 136Document58 pagesNational Budget Memorandum No 136Mark AllenNo ratings yet

- Economic Survey 2022-23 GistDocument17 pagesEconomic Survey 2022-23 GistAMIT BHARDWAZNo ratings yet

- Group 9 Abdullah 30, Usman Abid 17Document7 pagesGroup 9 Abdullah 30, Usman Abid 17Abdullah CheemaNo ratings yet

- Crux of Economic Survey 2023Document8 pagesCrux of Economic Survey 2023Raja S100% (1)

- Chapter-05 (English-2020) - Monetary Management and Financial MarketDocument21 pagesChapter-05 (English-2020) - Monetary Management and Financial MarketM Tariqul Islam MishuNo ratings yet

- MODULE 7 Advocacy Against CorruptionDocument8 pagesMODULE 7 Advocacy Against Corruptionnewlymade641No ratings yet

- 1460-2820-1-PB (1) (1), ClareteDocument27 pages1460-2820-1-PB (1) (1), ClaretefdizaNo ratings yet

- Eurotech Agency CaseDocument15 pagesEurotech Agency CaseKenzo RodisNo ratings yet

- A Text Book PDFDocument4 pagesA Text Book PDFAqib MalikNo ratings yet

- Orient Freight International v. Keihin-Everett Forwarding G.R. No. 191937, Aug. 9, 2017Document29 pagesOrient Freight International v. Keihin-Everett Forwarding G.R. No. 191937, Aug. 9, 2017Heather LunarNo ratings yet

- Gramt FormatDocument3 pagesGramt Formatwemimosamuel4No ratings yet

- Etil Hexano ASTM D1969Document2 pagesEtil Hexano ASTM D1969Coordinador LaboratorioNo ratings yet

- Financial Highlights: Year Ended December 31, 2020Document8 pagesFinancial Highlights: Year Ended December 31, 2020Muhammad NadeemNo ratings yet

- Case Study - LÓrealDocument4 pagesCase Study - LÓrealAndrea BrozosNo ratings yet

- Published Accounts (Format) Sem Oct 2022 For Students PDFDocument8 pagesPublished Accounts (Format) Sem Oct 2022 For Students PDFNur SyafiqahNo ratings yet

- Open Letter To LMN ChairmanDocument4 pagesOpen Letter To LMN ChairmanMessina04No ratings yet

- MDG Goal 1Document2 pagesMDG Goal 1black_belter789No ratings yet

- Inventory ValuationDocument4 pagesInventory ValuationMary AmoNo ratings yet

- Full Download Test Bank For Mcgraw Hill Connect Resources For Whittington Principles of Auditing and Other Assurance Services 20e PDF Full ChapterDocument36 pagesFull Download Test Bank For Mcgraw Hill Connect Resources For Whittington Principles of Auditing and Other Assurance Services 20e PDF Full Chaptersaturantbruniontvg0100% (24)

- Revised RFBT Quizzer On Special Laws New TopicsDocument48 pagesRevised RFBT Quizzer On Special Laws New Topicslairekk onyotNo ratings yet

- Basics of Bond ValuationDocument6 pagesBasics of Bond Valuationhimanshu AroraNo ratings yet

- Option Trading "The Option Butterfly Spread": by Larry GainesDocument37 pagesOption Trading "The Option Butterfly Spread": by Larry GainesHardyx HeartilyNo ratings yet

- Solved Refer To Figure 10.47. A Flexible Rectangular Area Is S...Document1 pageSolved Refer To Figure 10.47. A Flexible Rectangular Area Is S...Cristian A. GarridoNo ratings yet

- Annual ReportDocument42 pagesAnnual ReportAbdu MohammedNo ratings yet

- A Study On Marketing Mix Strategies and Impact of Consumer Behavior On Piaggio APE Autos and TrucksDocument163 pagesA Study On Marketing Mix Strategies and Impact of Consumer Behavior On Piaggio APE Autos and Trucksveerabhadraswamy100% (5)

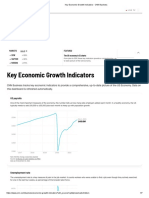

- Key Economic Growth Indicators - CNN BusinessDocument7 pagesKey Economic Growth Indicators - CNN BusinessLNo ratings yet

- Accounting Information Systems - Yola-170-171Document2 pagesAccounting Information Systems - Yola-170-171dindaNo ratings yet

- Acc206 e ExamDocument8 pagesAcc206 e Examm2kxcg4gsxNo ratings yet

- Jack Ma - WikipediaDocument5 pagesJack Ma - WikipediaEko Bayu GiriyantoNo ratings yet

- Explain Origin of Commercial BankingDocument6 pagesExplain Origin of Commercial Bankingዳግማዊ ጌታነህ ግዛው ባይህNo ratings yet

- RMO No. 57-2016 PDFDocument1 pageRMO No. 57-2016 PDFGabriel EdizaNo ratings yet

- Accounting Cycle of A Service BusinessDocument17 pagesAccounting Cycle of A Service BusinessAmie Jane Miranda100% (1)

- Bar Review Material 2019 TaxDocument41 pagesBar Review Material 2019 Taxsam cadley0% (1)

- Elemental Realty - Top 10 Real Estate Entrepreneurs - 2020' - Mr. Arun Kumar Aleti, CEODocument1 pageElemental Realty - Top 10 Real Estate Entrepreneurs - 2020' - Mr. Arun Kumar Aleti, CEOAkhila AdusumilliNo ratings yet

- Instructions:: Candor Cash Flow SolutionDocument1 pageInstructions:: Candor Cash Flow SolutionPirvuNo ratings yet