You might also like

- UntitledDocument1,437 pagesUntitledsalsabila ry1No ratings yet

- Jawaban Chapter 18Document34 pagesJawaban Chapter 18Heltiana Nufriyanti75% (4)

- Chapter 5 AIS PDFDocument4 pagesChapter 5 AIS PDFAnne Rose EncinaNo ratings yet

- Chapter 5 PPT (AIS - James Hall)Document10 pagesChapter 5 PPT (AIS - James Hall)Nur-aima Mortaba50% (2)

- Accounting Information System: Expenditure CycleDocument11 pagesAccounting Information System: Expenditure CycleSophia Marie BesorioNo ratings yet

- Accounting Information Systems, 6: Edition James A. HallDocument40 pagesAccounting Information Systems, 6: Edition James A. HallDianne NolascoNo ratings yet

- AIS ReviewerDocument5 pagesAIS Reviewercamilleorpilla xNo ratings yet

- IT Concepts & Systems AnalysisDocument22 pagesIT Concepts & Systems AnalysisAisah ReemNo ratings yet

- Chapter 5: The Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresDocument7 pagesChapter 5: The Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresAstxilNo ratings yet

- Chapter 5 Expenditure Cycle Part 1Document33 pagesChapter 5 Expenditure Cycle Part 1KRIS ANNE SAMUDIO100% (1)

- Presentation Audit of Acquisition and Payment CycleDocument38 pagesPresentation Audit of Acquisition and Payment CycleSyaffiq UbaidillahNo ratings yet

- Expenditure Cycle NoteDocument2 pagesExpenditure Cycle NoteZara Jane DinhayanNo ratings yet

- Chapter 4 The Revenue Cycle SummaryDocument5 pagesChapter 4 The Revenue Cycle SummaryAngela Erish CastroNo ratings yet

- Module 05 - Accounting and Information SystemsDocument6 pagesModule 05 - Accounting and Information SystemsKaye BabadillaNo ratings yet

- Reviewer 5Document14 pagesReviewer 5Cyrene CruzNo ratings yet

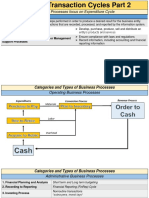

- AT 06-07 Transaction Cycles Part 2Document12 pagesAT 06-07 Transaction Cycles Part 2EeuhNo ratings yet

- Ais Expenditure Activity 2Document3 pagesAis Expenditure Activity 2Precious Anne CantarosNo ratings yet

- Sia - Uas - 2Document29 pagesSia - Uas - 2Cornelita Tesalonika R. K.No ratings yet

- 3) Audit of LiabilitiesDocument6 pages3) Audit of LiabilitiesMaxene Joi PigtainNo ratings yet

- Ch-4 Auditing Principles and Practices-IIDocument26 pagesCh-4 Auditing Principles and Practices-IIfiraolmosisabonkeNo ratings yet

- Kimberly Nicole B. Ledona Bsa 2B: GUIDE QUESTIONS: Report On Revenue CycleDocument3 pagesKimberly Nicole B. Ledona Bsa 2B: GUIDE QUESTIONS: Report On Revenue CycleKimberly NicoleNo ratings yet

- KELOMPOK 04 PPT AUDIT Siklus Perolehan Dan Pembayaran EditDocument39 pagesKELOMPOK 04 PPT AUDIT Siklus Perolehan Dan Pembayaran EditAkuntansi 6511No ratings yet

- Chapter 4Document7 pagesChapter 4Angela Erish CastroNo ratings yet

- AEB15 SM C18 v3Document33 pagesAEB15 SM C18 v3Aaqib Hossain100% (1)

- Chapter FiveDocument58 pagesChapter Fivehasan jabrNo ratings yet

- Quiz 1 Final ExamDocument6 pagesQuiz 1 Final ExamNica Jane MacapinigNo ratings yet

- Gurarsh's Final AssignmentDocument15 pagesGurarsh's Final AssignmentGuntaaj Kaur SranNo ratings yet

- Chapter 5Document70 pagesChapter 5Charles Daniel CatulongNo ratings yet

- The Expenditure Cycle Part 1Document42 pagesThe Expenditure Cycle Part 1CenNo ratings yet

- Chap. 9 Cis Auditing The Revenue CycleDocument68 pagesChap. 9 Cis Auditing The Revenue CycleSergio, JesharelleNo ratings yet

- AIS Chapter 4 Revenue CycleDocument6 pagesAIS Chapter 4 Revenue CycleKate Alvarez100% (1)

- 09 Auditing The Revenue CycleDocument7 pages09 Auditing The Revenue CycleJovie SalvacionNo ratings yet

- Prof BullinaDocument2 pagesProf BullinaAr-Reb AquinoNo ratings yet

- Final Requirement in Auditing in Csis Environment: 1. Create A Data Flow Diagram of The Current SystemDocument3 pagesFinal Requirement in Auditing in Csis Environment: 1. Create A Data Flow Diagram of The Current SystemmaiaaaaNo ratings yet

- IT Concepts & Systems AnalysisDocument28 pagesIT Concepts & Systems AnalysisAisah ReemNo ratings yet

- Reviewer 1Document8 pagesReviewer 1Maria Crista Mae UmaliNo ratings yet

- AUDIT PROGRAM For Cash Disbursements 2Document5 pagesAUDIT PROGRAM For Cash Disbursements 2jezreel dela mercedNo ratings yet

- Revenue Cycle (Part I)Document34 pagesRevenue Cycle (Part I)Rosario TaguinotNo ratings yet

- PDFDocument22 pagesPDFJoy Dhemple LambacoNo ratings yet

- CABINAS FocusNotes PrelimDocument7 pagesCABINAS FocusNotes PrelimJoshua CabinasNo ratings yet

- Chapter 5Document41 pagesChapter 5Gemma RetesNo ratings yet

- Financials For PSX RevisedDocument29 pagesFinancials For PSX RevisedAdnan AhmarNo ratings yet

- Transaction-Related Audit Objective Possible Internal Controls Common Tests of ControlsDocument3 pagesTransaction-Related Audit Objective Possible Internal Controls Common Tests of ControlsJustin DavenportNo ratings yet

- The Expenditure Cycle Part I: Purchases and Cash Disbursements ProceduresDocument28 pagesThe Expenditure Cycle Part I: Purchases and Cash Disbursements ProceduresNicah AcojonNo ratings yet

- Chapter 2Document7 pagesChapter 2Jolina T. OrongNo ratings yet

- Purchases & PayablesDocument12 pagesPurchases & Payablesrsn_surya100% (2)

- Chapter 4 Revenue CyceDocument4 pagesChapter 4 Revenue CyceSAFLOR, Edlyn Mae A.No ratings yet

- Audit of The Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts PayableDocument33 pagesAudit of The Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts Payable김현중No ratings yet

- IC - Review Question - AnsDocument3 pagesIC - Review Question - AnsMERINANo ratings yet

- Case Study - Bell StudioDocument19 pagesCase Study - Bell StudiosheetalsharmaNo ratings yet

- Lecture 9Document33 pagesLecture 9lawlokyiNo ratings yet

- A. Key Internal Control B. Transaction Related Audit Objectives C. Test of Control D. Substantive Test of TransactionDocument5 pagesA. Key Internal Control B. Transaction Related Audit Objectives C. Test of Control D. Substantive Test of TransactionRosanaDíazNo ratings yet

- Accounting Information System Naod Chapter TwoDocument10 pagesAccounting Information System Naod Chapter TwoNaod MekonnenNo ratings yet

- AIS Reviewer AIS Reviewer: Accountancy (The National Teachers College) Accountancy (The National Teachers College)Document13 pagesAIS Reviewer AIS Reviewer: Accountancy (The National Teachers College) Accountancy (The National Teachers College)Aldwin CalambaNo ratings yet

- Chapter 4 The Revenue Cycle SummaryDocument6 pagesChapter 4 The Revenue Cycle SummaryAngela Erish CastroNo ratings yet

- The Expenditure Cycle Part L and LLDocument2 pagesThe Expenditure Cycle Part L and LLloriemiepNo ratings yet

- Davita - Dewardani - 182321069 Tugas Pengauditan KeuanganDocument4 pagesDavita - Dewardani - 182321069 Tugas Pengauditan KeuanganHAHAHA HIHIHINo ratings yet

- Transaction Cycles: Revenue and Receipt CycleDocument4 pagesTransaction Cycles: Revenue and Receipt CycleGraceila P. CalopeNo ratings yet

- The Revenue Cycle: Group 1Document43 pagesThe Revenue Cycle: Group 1Ratih PratiwiNo ratings yet

- Korean Business Dictionary: American and Korean Business Terms for the Internet AgeFrom EverandKorean Business Dictionary: American and Korean Business Terms for the Internet AgeNo ratings yet

- Ge1 PrelimDocument4 pagesGe1 PrelimIexenne FigueroaNo ratings yet

- AE22 Reviewer Chapter 6-8Document7 pagesAE22 Reviewer Chapter 6-8Iexenne FigueroaNo ratings yet

- Ge1 Midterm ReviewerDocument9 pagesGe1 Midterm ReviewerIexenne FigueroaNo ratings yet

- Ge1 Reviewer Part2Document7 pagesGe1 Reviewer Part2Iexenne FigueroaNo ratings yet

- Assignment/ TugasanDocument10 pagesAssignment/ TugasanYung YeeNo ratings yet

- E-Commerce Solutions Benchmark Full EnglishDocument168 pagesE-Commerce Solutions Benchmark Full EnglishmauriciomouraNo ratings yet

- Hexagon Presentation LightDocument15 pagesHexagon Presentation LightManideepVendraNo ratings yet

- System Configuration Guide: Nortel Ethernet Switches 325 and 425 Software Release 3.6Document488 pagesSystem Configuration Guide: Nortel Ethernet Switches 325 and 425 Software Release 3.6Melvin FoongNo ratings yet

- Python BrochureDocument8 pagesPython BrochureSumanth GowdaNo ratings yet

- ISCMDocument3 pagesISCMSyed Jawwad ul hasanNo ratings yet

- Answer:: Free Exam/Cram Practice Materials - Best Exam Practice MaterialsDocument5 pagesAnswer:: Free Exam/Cram Practice Materials - Best Exam Practice MaterialsmrbeanNo ratings yet

- How To Conduct Job Evaluation PDFDocument13 pagesHow To Conduct Job Evaluation PDFZeeshan ch 'Hadi'No ratings yet

- Restaurant Resume PEIDocument2 pagesRestaurant Resume PEIc5t2fnh2hcNo ratings yet

- Software Testing (Manual + Automation) Course ContentDocument4 pagesSoftware Testing (Manual + Automation) Course ContentBinod YadavNo ratings yet

- The Fiery Colourwise M&M Demo: A4 VersionDocument8 pagesThe Fiery Colourwise M&M Demo: A4 VersionSunny SaahilNo ratings yet

- NSS Labs - Advanced Endpoint Protection Test Methodology v4.0Document12 pagesNSS Labs - Advanced Endpoint Protection Test Methodology v4.0Boby JosephNo ratings yet

- Information Systems (IS) Development/ Application Development - Systems ApproachDocument9 pagesInformation Systems (IS) Development/ Application Development - Systems ApproachShaekh Maruf Skder 1912892630No ratings yet

- How To Assign CTCM Status To A Quality Inspection Lot - SAP Q&ADocument2 pagesHow To Assign CTCM Status To A Quality Inspection Lot - SAP Q&AAnkit Garg/TCS/GandhinagarNo ratings yet

- Certified Information Systems Auditor (CISA) - Mock Exam 1Document11 pagesCertified Information Systems Auditor (CISA) - Mock Exam 1Nishant KulshresthaNo ratings yet

- Engineering Management Dissertation IdeasDocument6 pagesEngineering Management Dissertation IdeasCustomizedWritingPaperEugene100% (1)

- GST - Configuration For Vendor Returns ProcessDocument4 pagesGST - Configuration For Vendor Returns ProcessAnand PrakashNo ratings yet

- Kebabangan Northern Hub DevelopmentDocument15 pagesKebabangan Northern Hub Developmentredevils86No ratings yet

- Introduction To Information Storage and Management: © 2009 EMC Corporation. All Rights ReservedDocument21 pagesIntroduction To Information Storage and Management: © 2009 EMC Corporation. All Rights ReservedDeebika KaliyaperumalNo ratings yet

- Finding Orders in The ChaosDocument7 pagesFinding Orders in The ChaosLexs TangNo ratings yet

- Cls 8Document34 pagesCls 8ml assignmentNo ratings yet

- Mastering ASP Net Core Taking Your Skills To The Next LevelDocument11 pagesMastering ASP Net Core Taking Your Skills To The Next LevelHaseeb FarrukhNo ratings yet

- PDFDocument249 pagesPDFOki NurpatriaNo ratings yet

- RBIS User Manual - Encoder v1.0Document41 pagesRBIS User Manual - Encoder v1.0JoyceNo ratings yet

- Begin of Catalogue - in The Catalogue - ZipDocument4 pagesBegin of Catalogue - in The Catalogue - ZipAbdelaly JabbadNo ratings yet

- All India Kisan Sabha - ConferenecDocument3 pagesAll India Kisan Sabha - ConferenecmangeoNo ratings yet

- Primavera P6 Professional Fundamentals Rel 19: Learn ToDocument3 pagesPrimavera P6 Professional Fundamentals Rel 19: Learn ToBuywise shoppingNo ratings yet

- Debenu PDF ToolsDocument1 pageDebenu PDF ToolsMike ShinoderNo ratings yet

- PAYFORT Merchant Integration Guide V 8.7Document175 pagesPAYFORT Merchant Integration Guide V 8.7Woo BodaNo ratings yet