You might also like

- CVDocument2 pagesCVRajesh Kr DasNo ratings yet

- Bu Shivani Report 4Document31 pagesBu Shivani Report 4Shivani AgarwalNo ratings yet

- Internship Report On Electronic Cheque Clearing.Document58 pagesInternship Report On Electronic Cheque Clearing.Sneha Pradhanang100% (2)

- Banking Insurance and Financial Services: Unit 1: Introduction To BANKING (25%)Document13 pagesBanking Insurance and Financial Services: Unit 1: Introduction To BANKING (25%)sunगीत मजे्seNo ratings yet

- Internship Report at UCBL: A Comprehensive OverviewDocument46 pagesInternship Report at UCBL: A Comprehensive Overviewsourov shahaNo ratings yet

- Commodity Market (A Project Report)Document6 pagesCommodity Market (A Project Report)Manish GargNo ratings yet

- Internship Report (1507006)Document59 pagesInternship Report (1507006)Md Byzed AhmedNo ratings yet

- Muhammad Fahad, ID - 1503210108454, Term Paper (BRAC Bank Limited)Document45 pagesMuhammad Fahad, ID - 1503210108454, Term Paper (BRAC Bank Limited)TasmiaNo ratings yet

- Internship Report On UCBL BankDocument66 pagesInternship Report On UCBL BankOmar Faruk100% (1)

- SBL Internship ReportDocument30 pagesSBL Internship ReportPrajwol ThapaNo ratings yet

- Internship Report On Departments and Subsidiaries Branches of ICBDocument37 pagesInternship Report On Departments and Subsidiaries Branches of ICBNafiz FahimNo ratings yet

- Internship Report FormatDocument4 pagesInternship Report FormatMian AhsanNo ratings yet

- Internship Title: Human Resource Perspective at Branch Level of Rupali Bank LimitedDocument43 pagesInternship Title: Human Resource Perspective at Branch Level of Rupali Bank LimitedMounota MandalNo ratings yet

- Internship Report On Nepal Bank Limited: Submitted To: Apex College, Internship Management TeamDocument39 pagesInternship Report On Nepal Bank Limited: Submitted To: Apex College, Internship Management TeamNiraj LamsalNo ratings yet

- Internship Report MBA ACEDocument38 pagesInternship Report MBA ACENabin ShakyaNo ratings yet

- Buyology PresentationDocument13 pagesBuyology PresentationAshooSinghKocharNo ratings yet

- Banking system analysis of NCC Bank's investment portfolioDocument39 pagesBanking system analysis of NCC Bank's investment portfolioaburayhanNo ratings yet

- Internship ReportDocument33 pagesInternship Reportskbinty0% (1)

- National Saving CertificatesDocument11 pagesNational Saving Certificatesaabc12345No ratings yet

- ProposalDocument12 pagesProposalKanwal AwanNo ratings yet

- Report On Performance Analysis of SEBLDocument53 pagesReport On Performance Analysis of SEBLShanu Uddin Rubel80% (10)

- Kathmandu University School of ManagementDocument152 pagesKathmandu University School of Managementram binod yadavNo ratings yet

- Intern Report On Bank AsiaDocument89 pagesIntern Report On Bank Asiaziko777No ratings yet

- RURALDocument21 pagesRURALSrikanth Bhairi100% (2)

- Model Questions Fundamentals of Taxation and Auditing BBS 3rd Year PDFDocument5 pagesModel Questions Fundamentals of Taxation and Auditing BBS 3rd Year PDFShah SujitNo ratings yet

- BBA 15 39 Janib Ali MaharDocument40 pagesBBA 15 39 Janib Ali MaharNisa RizviNo ratings yet

- IntenshipDocument38 pagesIntenshiplovely siva100% (1)

- Internship Report: Profit Maximization and CSR Activities of NCC BankDocument32 pagesInternship Report: Profit Maximization and CSR Activities of NCC BankSiddikur Rahman JibonNo ratings yet

- Unit-9 Compensation ManagementDocument5 pagesUnit-9 Compensation Managementjagannadha raoNo ratings yet

- Accouting, Tax Management & Audit Vouchering UNDER CA ReportDocument95 pagesAccouting, Tax Management & Audit Vouchering UNDER CA ReportsalmanNo ratings yet

- SJIBL Internship ReportDocument101 pagesSJIBL Internship ReportsaminbdNo ratings yet

- Internship Report On Loan and AdvanceDocument72 pagesInternship Report On Loan and AdvanceAsad KhanNo ratings yet

- ReportDocument33 pagesReportKap's KumarNo ratings yet

- SYNOPSIS-A Comparative Study of NPA of Urban Co-Op BanksDocument7 pagesSYNOPSIS-A Comparative Study of NPA of Urban Co-Op BanksJitendra UdawantNo ratings yet

- Internship Report On at Siddhart Bank Limited JanakpurdhamDocument39 pagesInternship Report On at Siddhart Bank Limited JanakpurdhamAshish Kumar100% (1)

- Overall Banking Activities OF Everest Bank Limited: An Internship ReportDocument37 pagesOverall Banking Activities OF Everest Bank Limited: An Internship ReportPEmaa LMNo ratings yet

- Job Analysis of BFSI SectorDocument11 pagesJob Analysis of BFSI SectorHarshada ChavanNo ratings yet

- BBA 8th Sem Regular T 20197112600889969486821Document117 pagesBBA 8th Sem Regular T 20197112600889969486821Torreus AdhikariNo ratings yet

- Management Control Systems of SBIDocument15 pagesManagement Control Systems of SBIyogesh0794No ratings yet

- Financial Statement Analysis Southeast Bank LimitedDocument8 pagesFinancial Statement Analysis Southeast Bank LimitedSharifMahmud50% (4)

- Assignment 3Document16 pagesAssignment 3ShradhaMinkuPradhananga100% (1)

- My Final Internship Report Finalized N Nchecked Allama Iqbal Open University HRM MBADocument60 pagesMy Final Internship Report Finalized N Nchecked Allama Iqbal Open University HRM MBAHaris JamalNo ratings yet

- Practice of Pension in Corporate Sector of BangladeshDocument10 pagesPractice of Pension in Corporate Sector of BangladeshA.M.SyedNo ratings yet

- Internship Report of ADBLDocument41 pagesInternship Report of ADBLconXn Communication & CyberNo ratings yet

- Internship Report On Everest Bank LTDDocument44 pagesInternship Report On Everest Bank LTDSubekshya ShakyaNo ratings yet

- Internship Report On: "Employee Job Satisfaction of First Security Islami Bank Ltd. (FSIBL) : "Document45 pagesInternship Report On: "Employee Job Satisfaction of First Security Islami Bank Ltd. (FSIBL) : "Murshid IqbalNo ratings yet

- Performance Analysis of Standard Bank Limited For Financial Years 2012-13Document16 pagesPerformance Analysis of Standard Bank Limited For Financial Years 2012-13ZerinTasnimeNo ratings yet

- Complete Mba Project 1Document47 pagesComplete Mba Project 1sachingaubaNo ratings yet

- Internship Report on Capital Structure of IBBLDocument47 pagesInternship Report on Capital Structure of IBBLFahimNo ratings yet

- Core Competency - BisleriDocument2 pagesCore Competency - BisleriVipin JoshiNo ratings yet

- Financial Management Narang JainDocument1 pageFinancial Management Narang JainKetan KanoongoNo ratings yet

- Pooja MishraDocument7 pagesPooja MishrasmsmbaNo ratings yet

- BBAs Semester III Taxation Multiple Choice QuestionsDocument36 pagesBBAs Semester III Taxation Multiple Choice QuestionsSom DasNo ratings yet

- Marketing Mix Study at Worldfa ExportsDocument91 pagesMarketing Mix Study at Worldfa ExportsPARVEENNo ratings yet

- Corporate Financial Analysis with Microsoft ExcelFrom EverandCorporate Financial Analysis with Microsoft ExcelRating: 5 out of 5 stars5/5 (1)

- Internship Report at Ray & Ray Chartered AccountantsDocument52 pagesInternship Report at Ray & Ray Chartered AccountantsYashwant ShigwanNo ratings yet

- A Summer Internship Report On: Master of Business AdministrationDocument47 pagesA Summer Internship Report On: Master of Business AdministrationLove GumberNo ratings yet

- BBS-3-Year-Fundamental-of-Taxation-and-AuditingDocument4 pagesBBS-3-Year-Fundamental-of-Taxation-and-AuditingTHE TRICKSTERNo ratings yet

- Course Title: Corporate Tax Planning & Management Course Code: ACCT801 Credit Units:03 Level: PGDocument5 pagesCourse Title: Corporate Tax Planning & Management Course Code: ACCT801 Credit Units:03 Level: PGAkash Singh RajputNo ratings yet

- MPA605 Taxation Course Outline-1Document2 pagesMPA605 Taxation Course Outline-1Aminul Islam Rubel100% (1)

- CAP III-Advanced Audit and Assurance PDFDocument3 pagesCAP III-Advanced Audit and Assurance PDFsubash pandeyNo ratings yet

- Suggested December 2022 CAP III Group IDocument67 pagesSuggested December 2022 CAP III Group Isubash pandeyNo ratings yet

- 1 CAP-III SA Group-I June2022 FinalDocument83 pages1 CAP-III SA Group-I June2022 Finalsubash pandeyNo ratings yet

- Bima Samitte Rating For Non TarriffDocument6 pagesBima Samitte Rating For Non Tarriffsubash pandeyNo ratings yet

- Accounting Cycle - Comprehensive ProblemDocument29 pagesAccounting Cycle - Comprehensive ProblemTooba HashmiNo ratings yet

- 27A1100001972546Document2 pages27A1100001972546Meet Communication ServicesNo ratings yet

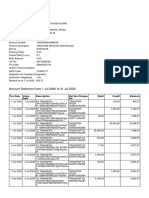

- Account Statement From 1 Jul 2020 To 31 Jul 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument4 pagesAccount Statement From 1 Jul 2020 To 31 Jul 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancepavans25No ratings yet

- An Overview On Digital Payments 4Document12 pagesAn Overview On Digital Payments 4DS DebasisNo ratings yet

- Amount in Words Is Rupees Eleven Thousand Six OnlyDocument1 pageAmount in Words Is Rupees Eleven Thousand Six OnlyGunaganti MaheshNo ratings yet

- Case Digest 2013Document35 pagesCase Digest 2013Jane Flandes Nobleza AbellaNo ratings yet

- AIR CANADA PetitionerDocument4 pagesAIR CANADA Petitionerangelo mendozaNo ratings yet

- Court of Tax AppealsDocument47 pagesCourt of Tax AppealsLady Paul SyNo ratings yet

- Buena Mano Q2-2013 Visayas and Mindanao CatalogDocument25 pagesBuena Mano Q2-2013 Visayas and Mindanao CatalogJay CastilloNo ratings yet

- Release and QuitclaimDocument1 pageRelease and QuitclaimMilli ReyesNo ratings yet

- Apply for Commercial Unit at Paras SquareDocument14 pagesApply for Commercial Unit at Paras SquareSehgal EstatesNo ratings yet

- Cambridge International AS and A Level Accounting Coursebook AnswerDocument5 pagesCambridge International AS and A Level Accounting Coursebook AnswerMopur NELLORENo ratings yet

- Tax EqualizationDocument5 pagesTax EqualizationTaxpert Professionals Private Limited100% (1)

- Cash BudgetDocument3 pagesCash Budgetmanoj kumarNo ratings yet

- Balance StatementDocument5 pagesBalance StatementNayeem RiyazNo ratings yet

- ISO 9001:2015 Certified CompanyDocument1 pageISO 9001:2015 Certified Companyomkar daveNo ratings yet

- GST Registration PDFDocument3 pagesGST Registration PDFRanjit MankuNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument1 pageStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceAdnan sonyNo ratings yet

- Subcontracting ProcessDocument5 pagesSubcontracting ProcessRenu BhasinNo ratings yet

- Meralco v. CBAADocument1 pageMeralco v. CBAAkdescallarNo ratings yet

- Final Tax Review12272022Document3 pagesFinal Tax Review12272022Saphira LuceNo ratings yet

- Boq Notes PDFDocument1 pageBoq Notes PDFJaimin ShahNo ratings yet

- RPH ReportDocument52 pagesRPH ReportElla Mae PalomenoNo ratings yet

- Tachyon Communications PVT LTD: InvoiceDocument1 pageTachyon Communications PVT LTD: InvoiceThe Obnoxious KidNo ratings yet

- Individual Income TaxDocument13 pagesIndividual Income TaxDaniel Dialino100% (1)

- SfsfgegDocument1 pageSfsfgegvishalNo ratings yet

- Important Information About Your Account: WWW - Cignal.tvDocument1 pageImportant Information About Your Account: WWW - Cignal.tvKris ArceoNo ratings yet

- Request Letter For Compromise - KbindustrialDocument1 pageRequest Letter For Compromise - KbindustrialJedah Ibarra VillaflorNo ratings yet

- Application Applicant Information Bank Details: DocumentsDocument2 pagesApplication Applicant Information Bank Details: Documentsednut_ynexNo ratings yet