You might also like

- EIB Working Papers 2018/08 - Debt overhang and investment efficiencyFrom EverandEIB Working Papers 2018/08 - Debt overhang and investment efficiencyNo ratings yet

- What Is A Debt RatioDocument11 pagesWhat Is A Debt RatioshreyaNo ratings yet

- Cas Ii Assignment ON Importance of Liquidity Ratios in The IndustryDocument7 pagesCas Ii Assignment ON Importance of Liquidity Ratios in The IndustrySanchali GoraiNo ratings yet

- Economic, Business and Artificial Intelligence Common Knowledge Terms And DefinitionsFrom EverandEconomic, Business and Artificial Intelligence Common Knowledge Terms And DefinitionsNo ratings yet

- Assignment On: Financial Statement Analysis FIN 4218Document28 pagesAssignment On: Financial Statement Analysis FIN 4218নাফিস ইকবাল আকিলNo ratings yet

- Liquidity Ratio: What Are Liquidity Ratios?Document11 pagesLiquidity Ratio: What Are Liquidity Ratios?Ritesh KumarNo ratings yet

- FSA Chapter 7Document3 pagesFSA Chapter 7Nadia ZahraNo ratings yet

- Liquidity, Asset Utilization, Debt Ratio and Firm Performance: Evidence From EgyptDocument32 pagesLiquidity, Asset Utilization, Debt Ratio and Firm Performance: Evidence From EgyptMsa-Management Sciences JournalNo ratings yet

- Importance of Different Ratios To Different User Groups: Management: Turnover and Operating Performance RatiosDocument4 pagesImportance of Different Ratios To Different User Groups: Management: Turnover and Operating Performance RatiosmirgasaraNo ratings yet

- Leverage RatioDocument5 pagesLeverage RatiopeptideNo ratings yet

- Solvency Ratios: Solvency Ratios Come in A Variety of FormsDocument3 pagesSolvency Ratios: Solvency Ratios Come in A Variety of FormssanskritiNo ratings yet

- Assess Debt Risk with Debt-Equity RatiosDocument3 pagesAssess Debt Risk with Debt-Equity Ratioshafis82No ratings yet

- What Is Ratio AnalysisDocument19 pagesWhat Is Ratio AnalysisMarie Frances Sayson100% (1)

- AssignmentDocument5 pagesAssignmentpankajjaiswal60No ratings yet

- Debt FinancingDocument8 pagesDebt FinancingZuhaib AhmedNo ratings yet

- Impact of Liquidity On ProfitabilityDocument44 pagesImpact of Liquidity On ProfitabilityRavi ShankarNo ratings yet

- Current RatioDocument22 pagesCurrent RatioAsawarNo ratings yet

- Financial LeverageDocument7 pagesFinancial LeverageGeanelleRicanorEsperonNo ratings yet

- A STUDY ON LIQUIDITY - Docx (2) - 1Document111 pagesA STUDY ON LIQUIDITY - Docx (2) - 1Nirmal Raj100% (1)

- Debt To Capital RatioDocument1 pageDebt To Capital RatioJoel FrankNo ratings yet

- Moodys - Sample Questions 3Document16 pagesMoodys - Sample Questions 3ivaNo ratings yet

- Fuad, 7,8,9Document6 pagesFuad, 7,8,9Muhd FiekrieNo ratings yet

- Ratio Analysis: Theory and ProblemsDocument51 pagesRatio Analysis: Theory and ProblemsAnit Jacob Philip100% (1)

- Ratio Analysis PROJECTDocument25 pagesRatio Analysis PROJECTimrataNo ratings yet

- Ratio Analysis Guide: 20 Financial Ratios ExplainedDocument7 pagesRatio Analysis Guide: 20 Financial Ratios ExplainedmgajenNo ratings yet

- Financial Statement Analysis-IIDocument45 pagesFinancial Statement Analysis-IINeelisetty Satya SaiNo ratings yet

- Tata Motors.: Liquidity RatiosDocument11 pagesTata Motors.: Liquidity RatiosAamir ShadNo ratings yet

- Capital StructuringDocument6 pagesCapital StructuringLourene Jauod- GuanzonNo ratings yet

- What Is The Current Ratio?Document10 pagesWhat Is The Current Ratio?Rica Princess MacalinaoNo ratings yet

- FM Analysis November 2019Document13 pagesFM Analysis November 2019Mancit 21No ratings yet

- Accounts Psda 2Document24 pagesAccounts Psda 2Shikhar DabralNo ratings yet

- Quick RatioDocument15 pagesQuick RatioAin roseNo ratings yet

- Principles Based Versus Rules BasedDocument2 pagesPrinciples Based Versus Rules BasedsreelekhaNo ratings yet

- Cost of Goods Sold: 1. Gross Profit MarginDocument10 pagesCost of Goods Sold: 1. Gross Profit MarginYuga ShiniNo ratings yet

- Capital StructureDocument17 pagesCapital StructureVinit Mathur100% (1)

- What Is Debt Equity Ratio & Its Significance?Document2 pagesWhat Is Debt Equity Ratio & Its Significance?bibhav poudelNo ratings yet

- Financial Management - Mba Question AnswersDocument40 pagesFinancial Management - Mba Question AnswersVenkata Narayanarao Kavikondala93% (28)

- Current RatioDocument8 pagesCurrent RatiousamahfsdNo ratings yet

- Ratio Analysis of Life Insurance - IBADocument116 pagesRatio Analysis of Life Insurance - IBANusrat Saragin NovaNo ratings yet

- What Is A Good or Bad Gearing Ratio? PDFDocument8 pagesWhat Is A Good or Bad Gearing Ratio? PDFKainos MuradzikwaNo ratings yet

- Liquidity RatioDocument3 pagesLiquidity RatioJodette Karyl NuyadNo ratings yet

- Financial Analysis Tools ExplainedDocument2 pagesFinancial Analysis Tools ExplainedJohna Mae Dolar EtangNo ratings yet

- Ratio Analysis and Risk Estimation: Submitted To MR - Sheheryar MalikDocument11 pagesRatio Analysis and Risk Estimation: Submitted To MR - Sheheryar MalikHaani ArNo ratings yet

- Ratio Analysis Brief Notes: Prof. Mayur Malviya Ratio AnalysisDocument11 pagesRatio Analysis Brief Notes: Prof. Mayur Malviya Ratio AnalysisravikumardavidNo ratings yet

- Cap StructureDocument4 pagesCap StructureInvisible CionNo ratings yet

- Financial Ratio Cheatsheet PDFDocument33 pagesFinancial Ratio Cheatsheet PDFJanlenn GepayaNo ratings yet

- Two Financial RatiosDocument9 pagesTwo Financial RatiosWONG ZI QINGNo ratings yet

- 1131810 leverage unit 4 fmDocument12 pages1131810 leverage unit 4 fmSHIVANSH ARORANo ratings yet

- Liquidity Ratio-Is Used To Determine A Company's Ability To Pay Its Short-Term Debt ObligationsDocument3 pagesLiquidity Ratio-Is Used To Determine A Company's Ability To Pay Its Short-Term Debt Obligationsjeshelle annNo ratings yet

- Ratio AnalysisDocument38 pagesRatio AnalysisrachitNo ratings yet

- What is a Coverage Ratio and Types to Analyze Financial HealthDocument2 pagesWhat is a Coverage Ratio and Types to Analyze Financial HealthDarlene SarcinoNo ratings yet

- Financial Ratio Analysis IDocument12 pagesFinancial Ratio Analysis IumavensudNo ratings yet

- Financial Leverage and Capital Structure PolicyDocument21 pagesFinancial Leverage and Capital Structure PolicyRashid HussainNo ratings yet

- Gemini Electronic Case StudyDocument9 pagesGemini Electronic Case Studydirshal0% (2)

- Ratios - What Are They?: Category RatioDocument15 pagesRatios - What Are They?: Category Ratiounderwood@eject.co.zaNo ratings yet

- Financial Ratio IntrepretationDocument47 pagesFinancial Ratio IntrepretationRavi Singla100% (1)

- FPT Group's liquidity ratios in 2020Document17 pagesFPT Group's liquidity ratios in 2020Phạm Tuấn HùngNo ratings yet

- Financial RatiosDocument30 pagesFinancial RatiosVenz LacreNo ratings yet

- Clase 1 Article - Inglés - Desarrollo Financiero Crédito Comercial Entre PaísesDocument43 pagesClase 1 Article - Inglés - Desarrollo Financiero Crédito Comercial Entre PaísesAlder RamirezNo ratings yet

- E-Logistics: Omnichannel Strategies During COVID-19Document12 pagesE-Logistics: Omnichannel Strategies During COVID-19Awais AhmedNo ratings yet

- Falcon LogisticsDocument31 pagesFalcon LogisticsAwais AhmedNo ratings yet

- 0008 - Introduction To TaxationDocument6 pages0008 - Introduction To TaxationAwais AhmedNo ratings yet

- ERP System Benefits and Effectiveness in Omani OrganizationsDocument5 pagesERP System Benefits and Effectiveness in Omani OrganizationsAwais AhmedNo ratings yet

- 1695 - Banking, Financial Products and ServicesDocument8 pages1695 - Banking, Financial Products and ServicesAwais AhmedNo ratings yet

- Student Name Registration Number DateDocument12 pagesStudent Name Registration Number DateAwais AhmedNo ratings yet

- HCT Strategic Business PlanDocument12 pagesHCT Strategic Business PlanAwais AhmedNo ratings yet

- Three Valuation MethodsDocument6 pagesThree Valuation MethodsAwais AhmedNo ratings yet

- Cesim Global Challenge - Case DescriptionDocument7 pagesCesim Global Challenge - Case DescriptionAwais AhmedNo ratings yet

- DK Goel SQPDocument8 pagesDK Goel SQPVanshika SinghNo ratings yet

- Review Session 01 MA Concept Review Section2Document20 pagesReview Session 01 MA Concept Review Section2misalNo ratings yet

- Chapter 5 Setting Menu PriceDocument11 pagesChapter 5 Setting Menu PricemeltinaNo ratings yet

- ConsolidatedStatementReport - May2023 2Document116 pagesConsolidatedStatementReport - May2023 2Anupam KumarNo ratings yet

- Chapter 6 Revenue RecognitionDocument41 pagesChapter 6 Revenue Recognitionsamuel hailuNo ratings yet

- ACC117 Project 2Document7 pagesACC117 Project 2Aliamaisara ZahiraNo ratings yet

- Bank Regulatory CapitalDocument9 pagesBank Regulatory CapitalDristi PoddarNo ratings yet

- Open Banking Api Service FactsheetDocument2 pagesOpen Banking Api Service FactsheetswiftcenterNo ratings yet

- Food Production & Distribution Newsletter Q3'23Document19 pagesFood Production & Distribution Newsletter Q3'23Kevin ParkerNo ratings yet

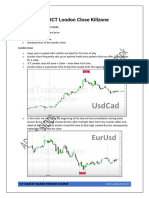

- The ICT London Close KillzoneDocument3 pagesThe ICT London Close Killzonehuda EcharkaouiNo ratings yet

- Barack Home Rental Income Statement and Balance SheetDocument3 pagesBarack Home Rental Income Statement and Balance SheetStephen FrancisNo ratings yet

- DropshippingDocument20 pagesDropshippingdynamicgrowthusNo ratings yet

- Think Marketing First Canadian Edition Canadian 1st Edition Tuckwell Test BankDocument18 pagesThink Marketing First Canadian Edition Canadian 1st Edition Tuckwell Test Bankclitusquanghbz9up100% (21)

- SONIA (Interest Rate)Document2 pagesSONIA (Interest Rate)timothy454No ratings yet

- Accounting Project 2Document63 pagesAccounting Project 2jayeoba oluwaseyiNo ratings yet

- CA Final Test Paper-1Document4 pagesCA Final Test Paper-1anjana2734No ratings yet

- Brand Management AssignmentDocument17 pagesBrand Management AssignmentHiba AnisNo ratings yet

- Reading 11 GARP Code of Conduct - AnswersDocument4 pagesReading 11 GARP Code of Conduct - AnswersPriyadarshini SealNo ratings yet

- BusinessDocument4 pagesBusinessInvincible GokuNo ratings yet

- Practice Questions & AnswersDocument10 pagesPractice Questions & AnswersKomal KothariNo ratings yet

- 10 25 Full Company Update 20230227Document16 pages10 25 Full Company Update 20230227Contra Value BetsNo ratings yet

- Ias 7 Cash Flow Statement ContinuedDocument8 pagesIas 7 Cash Flow Statement ContinuedMichael Bwire100% (1)

- SC 20220816-2022916Document5 pagesSC 20220816-2022916Line XiaoNo ratings yet

- Basics of Financial AnalysisDocument17 pagesBasics of Financial AnalysisRy De VeraNo ratings yet

- Summary #17Document2 pagesSummary #17atika suriNo ratings yet

- Compensation Policy 2020 21Document14 pagesCompensation Policy 2020 21K. NikhilNo ratings yet

- TOC Marketing PlanDocument4 pagesTOC Marketing PlanKarimNo ratings yet

- FMI - PPT - Seminar (Week) 09 (Aug 2023)Document62 pagesFMI - PPT - Seminar (Week) 09 (Aug 2023)Kwan Kwok AsNo ratings yet

- Sanjeev Auto Parts Manufacturers Private Limited-03-03-2017Document6 pagesSanjeev Auto Parts Manufacturers Private Limited-03-03-2017ram shindeNo ratings yet

- Rating Action Moodys Downgrades Limas Rating 26may2023 PR 477088Document6 pagesRating Action Moodys Downgrades Limas Rating 26may2023 PR 477088Diario El Comercio100% (1)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetFrom EverandThe Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetRating: 5 out of 5 stars5/5 (2)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (34)

- Investment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionFrom EverandInvestment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionRating: 5 out of 5 stars5/5 (1)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- How to Measure Anything: Finding the Value of Intangibles in BusinessFrom EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessRating: 3.5 out of 5 stars3.5/5 (4)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Add Then Multiply: How small businesses can think like big businesses and achieve exponential growthFrom EverandAdd Then Multiply: How small businesses can think like big businesses and achieve exponential growthNo ratings yet

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityFrom EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityRating: 4.5 out of 5 stars4.5/5 (4)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorFrom EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorNo ratings yet

- Note Brokering for Profit: Your Complete Work At Home Success ManualFrom EverandNote Brokering for Profit: Your Complete Work At Home Success ManualNo ratings yet