You might also like

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- Codal-Local Power of TaxationDocument7 pagesCodal-Local Power of TaxationKim DyNo ratings yet

- BASTRTAX - Strategic Tax ManagementDocument25 pagesBASTRTAX - Strategic Tax ManagementKyla Shmily GonzagaNo ratings yet

- Basics of Local Finance and Taxation and Responsibilities and Accountabilities of Accountable OfficerDocument16 pagesBasics of Local Finance and Taxation and Responsibilities and Accountabilities of Accountable Officeranne villarinNo ratings yet

- Bolts Training HandoutsDocument649 pagesBolts Training Handoutsgeminailna87% (31)

- Notes On Local Taxation Latest Compilation Base On 2023 Bar SyllabusDocument37 pagesNotes On Local Taxation Latest Compilation Base On 2023 Bar SyllabusCastillo Mike Martin DomiderNo ratings yet

- LOCAL GOVERNMENT TAXATION POWERSDocument136 pagesLOCAL GOVERNMENT TAXATION POWERSJeremae Ann CeriacoNo ratings yet

- B. Section 14 of R.A. 9167 Constitutes An Undue Limitation of The Taxing Power of LgusDocument4 pagesB. Section 14 of R.A. 9167 Constitutes An Undue Limitation of The Taxing Power of LgusNika RojasNo ratings yet

- LGC RPTDocument19 pagesLGC RPTMelissa MarinduqueNo ratings yet

- Local Taxation Part IDocument35 pagesLocal Taxation Part IEmille LlorenteNo ratings yet

- Local Taxation UpdatedDocument71 pagesLocal Taxation UpdatedEmille Llorente100% (1)

- Nature and Source of Local Taxing Power: Grant of Local Taxing Power Under Existing LawDocument6 pagesNature and Source of Local Taxing Power: Grant of Local Taxing Power Under Existing LawFranco David BaratetaNo ratings yet

- Finals Notes LOCAL TAXATION 5.6.23Document13 pagesFinals Notes LOCAL TAXATION 5.6.23Raissa Anjela Carman-JardenicoNo ratings yet

- Tax LGCDocument32 pagesTax LGCFaith JediNo ratings yet

- Local TaxationDocument57 pagesLocal TaxationJesterNo ratings yet

- RA - PrE 418 - EXERCISE IIDocument3 pagesRA - PrE 418 - EXERCISE IIEnnajieee QtNo ratings yet

- Local Government Taxation SDocument5 pagesLocal Government Taxation SDiane UyNo ratings yet

- 03 Local Tax AddendumDocument21 pages03 Local Tax Addendumsmartguy_alecNo ratings yet

- Local Government TaxationDocument5 pagesLocal Government TaxationDiane UyNo ratings yet

- Sources of Income of Barangay and Different Issues in BarangayDocument12 pagesSources of Income of Barangay and Different Issues in BarangayLyndon G TimpugNo ratings yet

- Local Fiscal AdministrationDocument37 pagesLocal Fiscal AdministrationEliza Flores100% (4)

- DE GUZMAN, GRACIELLE ANDREA R. - Pree 418 - EXERCISE IIDocument3 pagesDE GUZMAN, GRACIELLE ANDREA R. - Pree 418 - EXERCISE IIEnnajieee QtNo ratings yet

- Municipal Finance Sources of Revenue (Sections 5-7, Art X) : TaxationDocument8 pagesMunicipal Finance Sources of Revenue (Sections 5-7, Art X) : TaxationKobe Lawrence VeneracionNo ratings yet

- Local Government TaxationDocument7 pagesLocal Government TaxationCeresjudicataNo ratings yet

- PLM Tax II 2016 2017 Local Taxation Local Government Taxation Real Property Taxation Full Notes 09 March 2017Document49 pagesPLM Tax II 2016 2017 Local Taxation Local Government Taxation Real Property Taxation Full Notes 09 March 2017Mark DungoNo ratings yet

- Local TaxesDocument19 pagesLocal TaxesKennethQueRaymundoNo ratings yet

- TAXREV SYLLABUS - LOCAL TAXATION AND REAL PROPERTY TAXATION ATTY CabanDocument6 pagesTAXREV SYLLABUS - LOCAL TAXATION AND REAL PROPERTY TAXATION ATTY CabanPatrick GuetaNo ratings yet

- DELA CRUZ, QUERICO Exercise IIDocument3 pagesDELA CRUZ, QUERICO Exercise IIEnnajieee QtNo ratings yet

- LOCAL TAX 2014 - Atty. DabuDocument12 pagesLOCAL TAX 2014 - Atty. DabuEwendel GatdulaNo ratings yet

- Local TaxationDocument65 pagesLocal TaxationLyndon G TimpugNo ratings yet

- Guide Notes On Local Government TaxationDocument27 pagesGuide Notes On Local Government TaxationNayadNo ratings yet

- Local Government Taxation Powers and LimitationsDocument28 pagesLocal Government Taxation Powers and LimitationsFunnyPearl Adal GajuneraNo ratings yet

- National Power Corp VS City of CabanatuanDocument3 pagesNational Power Corp VS City of CabanatuanEmpty CupNo ratings yet

- Taxing Powers, Scope and Limitations of Nga and LguDocument7 pagesTaxing Powers, Scope and Limitations of Nga and LguArthur MericoNo ratings yet

- Local and RPTaxation CGBP 2017Document221 pagesLocal and RPTaxation CGBP 2017Rodel Cadorniga Jr.No ratings yet

- General Principles of TaxationDocument5 pagesGeneral Principles of Taxationmync89100% (3)

- 2016 Tax Bar ExaminationsDocument19 pages2016 Tax Bar Examinations涛 明 灵No ratings yet

- TaxxxDocument2 pagesTaxxxThomas EdisonNo ratings yet

- LGU Taxation LimitationsDocument80 pagesLGU Taxation LimitationsRuiz, CherryjaneNo ratings yet

- Taxation Digests Pt. 1Document15 pagesTaxation Digests Pt. 1Laurice PocaisNo ratings yet

- Local TaxationDocument60 pagesLocal TaxationWillow Sapphire100% (1)

- Local Fiscal AdministrationDocument12 pagesLocal Fiscal AdministrationJanice Aguila Suarez - Madarang100% (1)

- 04 2019 Up LMT Boc Taxation LawDocument36 pages04 2019 Up LMT Boc Taxation LawMikee PortesNo ratings yet

- Pub Corp Exam ReviewerDocument19 pagesPub Corp Exam Reviewerlicarl benitoNo ratings yet

- Barangay Taxing PowerDocument2 pagesBarangay Taxing PowerNorman CorreaNo ratings yet

- Local Revenue GenerationDocument9 pagesLocal Revenue GenerationIsnihaya I. AbubacarNo ratings yet

- 2023 Locreal TaxDocument25 pages2023 Locreal TaxBogs QuitainNo ratings yet

- TaxationDocument3 pagesTaxationErichWaeschNo ratings yet

- Local Gov't FinanceDocument12 pagesLocal Gov't FinanceLea MonticalboNo ratings yet

- NPC v. CITY OF CABANATUANDocument12 pagesNPC v. CITY OF CABANATUANMuhammadIshahaqBinBenjaminNo ratings yet

- Local Fiscal Administration & Resource Management PresentationDocument39 pagesLocal Fiscal Administration & Resource Management PresentationKen-ken Chua GerolinNo ratings yet

- NPC Liable to Pay Franchise Tax to City of CabanatuanDocument26 pagesNPC Liable to Pay Franchise Tax to City of CabanatuanMirafelNo ratings yet

- Activi: Taxation 219Document14 pagesActivi: Taxation 219Block escapeNo ratings yet

- Local Business Taxes & Real Property Tax: Atty. Vic C. MamalateoDocument78 pagesLocal Business Taxes & Real Property Tax: Atty. Vic C. Mamalateoiris7curl100% (1)

- Tax ReviewerDocument217 pagesTax ReviewerRevz LamosteNo ratings yet

- Local TaxationDocument63 pagesLocal TaxationRolando Mauring ReubalNo ratings yet

- Give at Least 5 Constitutional Provisions /limitations That Directly Affect The Power To Tax of The StateDocument24 pagesGive at Least 5 Constitutional Provisions /limitations That Directly Affect The Power To Tax of The StateAngie JosolNo ratings yet

- Local TaxationDocument47 pagesLocal TaxationjohnisflyNo ratings yet

- Philippine Tax System AssessmentDocument13 pagesPhilippine Tax System Assessmentgblue12100% (1)

- Real PropertyDocument18 pagesReal PropertyRomel AtanacioNo ratings yet

- Notes For Lecture Week 9Document14 pagesNotes For Lecture Week 9Ralph TiempoNo ratings yet

- LW 5B LPC Local Eminent DomainDocument14 pagesLW 5B LPC Local Eminent DomainRalph TiempoNo ratings yet

- Notes For Lecture Week 8Document10 pagesNotes For Lecture Week 8Ralph TiempoNo ratings yet

- LW 2B LPC Power RelationsDocument15 pagesLW 2B LPC Power RelationsRalph TiempoNo ratings yet

- Definition of TermsDocument11 pagesDefinition of TermsRalph TiempoNo ratings yet

- UntitledDocument4 pagesUntitledRalph TiempoNo ratings yet

- Declaration of CompletenessDocument1 pageDeclaration of CompletenessRalph TiempoNo ratings yet

- UntitledDocument1 pageUntitledRalph TiempoNo ratings yet

- Alternative forms of 'R' and 'H' in shorthandDocument14 pagesAlternative forms of 'R' and 'H' in shorthandAnshil SharmaNo ratings yet

- Dhaka Club Areya BaseDocument63 pagesDhaka Club Areya BaseAbu Bakkar Siddiq100% (1)

- Is Participant - Simplified v3Document7 pagesIs Participant - Simplified v3Ajith V0% (1)

- role of the allama iqbal in the creation of pakistanDocument2 pagesrole of the allama iqbal in the creation of pakistandeadson03No ratings yet

- Chapter 7 Audit of LiabilitiesDocument26 pagesChapter 7 Audit of LiabilitiesSteffany Roque100% (2)

- Skripsi: Implementasi Kebijakan Disiplin Pegawai Negeri Sipil Di Distrik Navigasi Kelas I PalembangDocument25 pagesSkripsi: Implementasi Kebijakan Disiplin Pegawai Negeri Sipil Di Distrik Navigasi Kelas I PalembangsichluzNo ratings yet

- BBC Dividends from Unrealized Asset AppreciationDocument1 pageBBC Dividends from Unrealized Asset Appreciationvmanalo16No ratings yet

- 1st Quarter Module 2 - EMPOWERMENT TECHNOLOGYDocument13 pages1st Quarter Module 2 - EMPOWERMENT TECHNOLOGYmichael delinNo ratings yet

- Account activity and balance from 10 Apr to 22 AprDocument2 pagesAccount activity and balance from 10 Apr to 22 AprSRIDHAR allhari0% (1)

- Gstinvoice 0047Document1 pageGstinvoice 0047Kalpatharu OrganicsNo ratings yet

- CC TO BTC Method (Updated September 2020) : Written by @idzsellerDocument7 pagesCC TO BTC Method (Updated September 2020) : Written by @idzsellerStephanie KaitlynNo ratings yet

- Table of CourtsDocument21 pagesTable of CourtsFakhri AzimNo ratings yet

- Government Structure in CanadaDocument4 pagesGovernment Structure in CanadaMichelleLawNo ratings yet

- Reliable Exports Lease DeedDocument27 pagesReliable Exports Lease DeedOkkishoreNo ratings yet

- Corporate Counsel in Omaha NE Resume Jeff AndersonDocument3 pagesCorporate Counsel in Omaha NE Resume Jeff AndersonJeffAndersonNo ratings yet

- Lecture 03 CG TheoriesDocument37 pagesLecture 03 CG TheoriesWILBROAD THEOBARDNo ratings yet

- Election Offenses Omnibus Election CodeDocument12 pagesElection Offenses Omnibus Election CodeRaziele RanesesNo ratings yet

- Chapter 2 Energy and Energy TransferDocument35 pagesChapter 2 Energy and Energy TransferNik Hafiy Hafizi0% (1)

- Dogwhistles, political manipulation analyzedDocument38 pagesDogwhistles, political manipulation analyzedMaria Fernanda Galvis GomezNo ratings yet

- Virtual Weddings Under Philippine Law - PFB.20-08-03Document4 pagesVirtual Weddings Under Philippine Law - PFB.20-08-03Pedro José Fausto BernardoNo ratings yet

- Judicial Interference ComplaintDocument6 pagesJudicial Interference ComplaintNC Policy WatchNo ratings yet

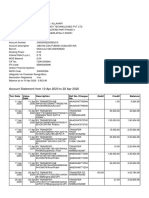

- Statement of Account: Product: Ca-Gen-Pub-Metro/Urban-Inr Currency: INRDocument1 pageStatement of Account: Product: Ca-Gen-Pub-Metro/Urban-Inr Currency: INRAottry MukherjeeNo ratings yet

- Consent Letter Karnataka1Document2 pagesConsent Letter Karnataka1sayeed66No ratings yet

- Results Analysis Method 7, POC Method Based On Project Progress Value Determination - SAP BlogsDocument11 pagesResults Analysis Method 7, POC Method Based On Project Progress Value Determination - SAP BlogsMahesh pvNo ratings yet

- Baybay Elementary School Monthly Accomplishment Report on Anti-Drug ProgramsDocument1 pageBaybay Elementary School Monthly Accomplishment Report on Anti-Drug ProgramsCarinaJoy Ballesteros Mendez DeGuzman100% (1)

- Technical Specification For Fire ProtectionDocument3 pagesTechnical Specification For Fire ProtectionJoeven JagocoyNo ratings yet

- Performance Evaluation of RAK Ceramics & Standard Ceramics.Document24 pagesPerformance Evaluation of RAK Ceramics & Standard Ceramics.Emon HossainNo ratings yet

- UnimportantDocument2 pagesUnimportantapi-78256506No ratings yet

- G.R. No. 181021Document2 pagesG.R. No. 181021Jahbee Tecson Redillas100% (1)

- Vigilantibus Et Non Dormientibus Jura SubveniuntDocument3 pagesVigilantibus Et Non Dormientibus Jura SubveniuntferozekasNo ratings yet