You might also like

- Understanding Financial Statements (Review and Analysis of Straub's Book)From EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Rating: 5 out of 5 stars5/5 (5)

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- The Entrepreneur’S Dictionary of Business and Financial TermsFrom EverandThe Entrepreneur’S Dictionary of Business and Financial TermsNo ratings yet

- Accounting and Finance Formulas: A Simple IntroductionFrom EverandAccounting and Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- A. Calculate Watkins's Value of OperationsDocument20 pagesA. Calculate Watkins's Value of OperationsNarmeen Khan100% (1)

- PARTNERSHIPDocument153 pagesPARTNERSHIPJoen SinamagNo ratings yet

- Investor Diary Expert Stock Analysis Excel (V-3) : How To Use This Spreadsheet?Document76 pagesInvestor Diary Expert Stock Analysis Excel (V-3) : How To Use This Spreadsheet?AkhileshChauhanNo ratings yet

- Ch12 P11 Build A ModelDocument7 pagesCh12 P11 Build A ModelRayudu RamisettiNo ratings yet

- Chapter 13. Tool Kit For Corporate Valuation, Value-Based Management and Corporate GovernanceDocument19 pagesChapter 13. Tool Kit For Corporate Valuation, Value-Based Management and Corporate GovernanceHenry RizqyNo ratings yet

- Ch17-Ppt-Financial Planning and ControlDocument45 pagesCh17-Ppt-Financial Planning and Controlmuhammadosama100% (3)

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Form IEPF-7 - Vedanta - IntDiv2018-19Document70 pagesForm IEPF-7 - Vedanta - IntDiv2018-19james fellow100% (1)

- Is Participant - Simplified v3Document7 pagesIs Participant - Simplified v3Ajith V0% (1)

- FM LMSDocument36 pagesFM LMSJuliana Waniwan100% (1)

- Accountancy Project Class 12 Cash Flow StatementDocument3 pagesAccountancy Project Class 12 Cash Flow StatementKasi Nath0% (5)

- Ch12 Excel ModelDocument23 pagesCh12 Excel ModelDan Johnson50% (2)

- Financial Planning and Control (Chapter 17)Document7 pagesFinancial Planning and Control (Chapter 17)Angelica D. SabenianoNo ratings yet

- Financial PlanningDocument28 pagesFinancial Planningmarina servanNo ratings yet

- MBA 570 Min Case CHP 14 WK 2Document11 pagesMBA 570 Min Case CHP 14 WK 2chastityc2001No ratings yet

- Corporate Valuation and Financial PlanningDocument52 pagesCorporate Valuation and Financial Planningsidra imtiazNo ratings yet

- Chap 12 SolutionDocument15 pagesChap 12 SolutionMarium Raza0% (1)

- CF5e PPT Ch12Document52 pagesCF5e PPT Ch12Thang NguyenNo ratings yet

- Chapter 13. CH 13-11 Build A Model: (Par Plus PIC)Document7 pagesChapter 13. CH 13-11 Build A Model: (Par Plus PIC)AmmarNo ratings yet

- 06 Financial Planning Part ADocument38 pages06 Financial Planning Part Agopika.7mNo ratings yet

- Integrative ProblemDocument3 pagesIntegrative ProblemImelda AngelesNo ratings yet

- 2012-04-13 042436 Finance SandersonicDocument4 pages2012-04-13 042436 Finance SandersonicSai Swaroop MandalNo ratings yet

- CHAPTER II - Financial Analysis and PlanningDocument84 pagesCHAPTER II - Financial Analysis and PlanningTamiratNo ratings yet

- CHAPTER II - Financial Analysis and PlanningDocument84 pagesCHAPTER II - Financial Analysis and PlanningMan TKNo ratings yet

- Chapter 12 Mini Case SolutionsDocument10 pagesChapter 12 Mini Case SolutionsFarhanie NordinNo ratings yet

- Financial Statements, Cash Flow AnalysisDocument41 pagesFinancial Statements, Cash Flow AnalysisMinhaz Ahmed0% (1)

- Business Valuations: Net Asset Value (Nav)Document9 pagesBusiness Valuations: Net Asset Value (Nav)Artwell ZuluNo ratings yet

- 12 Problem: 10: Corporate Valuation and Financial PlanningDocument141 pages12 Problem: 10: Corporate Valuation and Financial PlanningMarium RazaNo ratings yet

- Chapter TwoDocument19 pagesChapter TwoTemesgen LealemNo ratings yet

- Financial Planning and Forecasting Financial Statements: Answers To End-Of-Chapter QuestionsDocument9 pagesFinancial Planning and Forecasting Financial Statements: Answers To End-Of-Chapter QuestionsArpit BhawsarNo ratings yet

- Financial Statement Analysis: Curriculum Designed For Use With The Iowa Electronic MarketsDocument37 pagesFinancial Statement Analysis: Curriculum Designed For Use With The Iowa Electronic MarketsArnab BaruaNo ratings yet

- Ratio Analysis and ExamplesDocument18 pagesRatio Analysis and ExamplesUnique OfficialsNo ratings yet

- FINA 410 Exercises NOV PDFDocument7 pagesFINA 410 Exercises NOV PDFDrSwati BhargavaNo ratings yet

- 05 Test Bank For Business FinanceDocument46 pages05 Test Bank For Business FinanceBabatunde Victor AjalaNo ratings yet

- PART I: Discussion Ques Ons: Submission Date: On or Before Final Examination Total Weight: 30%Document5 pagesPART I: Discussion Ques Ons: Submission Date: On or Before Final Examination Total Weight: 30%jaNo ratings yet

- EFM2e, CH 02, SlidesDocument19 pagesEFM2e, CH 02, SlidesEricLiangtoNo ratings yet

- ExamDocument2 pagesExamAnonymous Uya1CUAqjNo ratings yet

- Financial Forecasting SamarakoonDocument33 pagesFinancial Forecasting SamarakoonEyael ShimleasNo ratings yet

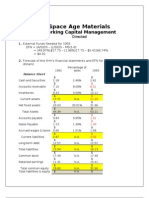

- Space Age Materials: Working Capital ManagementDocument4 pagesSpace Age Materials: Working Capital ManagementChris204267% (3)

- Financial Planning and Forecasting Financial Statements: Answers To End-Of-Chapter QuestionsDocument10 pagesFinancial Planning and Forecasting Financial Statements: Answers To End-Of-Chapter QuestionsBilal RazzaqNo ratings yet

- IFM11 Solution To Ch09 P11 Build A ModelDocument18 pagesIFM11 Solution To Ch09 P11 Build A ModelDiana SorianoNo ratings yet

- Financial Planning Process: ForecastingDocument10 pagesFinancial Planning Process: ForecastingFantayNo ratings yet

- Financial Planning and Forecasting Pro Forma Financial StatementsDocument22 pagesFinancial Planning and Forecasting Pro Forma Financial StatementsCOLONEL ZIKRIA0% (1)

- AAP Q4 2022 Earnings - FinalDocument10 pagesAAP Q4 2022 Earnings - FinalDaniel KwanNo ratings yet

- Exam 1 Fall 19Document9 pagesExam 1 Fall 19April Grace TrinidadNo ratings yet

- Exercise 5 SolutionDocument4 pagesExercise 5 SolutioneyNo ratings yet

- Valuing and Acquiring A Business: Hawawini & Viallet 1Document53 pagesValuing and Acquiring A Business: Hawawini & Viallet 1Kishore ReddyNo ratings yet

- COMM 324 A4 SolutionsDocument6 pagesCOMM 324 A4 SolutionsdorianNo ratings yet

- C. R. Bard, Inc. 2015 Annual ReportDocument20 pagesC. R. Bard, Inc. 2015 Annual ReportRavi HNo ratings yet

- Iefinmt Reviewer For Quiz (#1) : I. Definition of TermsDocument11 pagesIefinmt Reviewer For Quiz (#1) : I. Definition of TermspppppNo ratings yet

- 11Document6 pages11Daud Khan YousafzaiNo ratings yet

- Offices of Bank Holding Company Revenues World Summary: Market Values & Financials by CountryFrom EverandOffices of Bank Holding Company Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- Commercial Bank Revenues World Summary: Market Values & Financials by CountryFrom EverandCommercial Bank Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- T C C (C 11) : HE Ost of Apital HapterDocument11 pagesT C C (C 11) : HE Ost of Apital HapterVARUN MONGANo ratings yet

- Finance Notes - VDocument8 pagesFinance Notes - VVARUN MONGANo ratings yet

- Finance Notes IIIDocument246 pagesFinance Notes IIIVARUN MONGANo ratings yet

- Capbud CFDocument8 pagesCapbud CFVARUN MONGANo ratings yet

- Finance NotesDocument14 pagesFinance NotesVARUN MONGANo ratings yet

- Chapter 13 - Working Capital ManagementDocument38 pagesChapter 13 - Working Capital ManagementAn TuanNo ratings yet

- Evince Textiles LimitedDocument3 pagesEvince Textiles LimitedAnsary LabibNo ratings yet

- Nurul HidayanitaDocument11 pagesNurul HidayanitanurulNo ratings yet

- ETSY - Etsy, IncDocument10 pagesETSY - Etsy, Incdantulo1234No ratings yet

- Accounts Questions Compiler PDFDocument187 pagesAccounts Questions Compiler PDFBrinda RNo ratings yet

- CFAR Time Variation in The Equity Risk PremiumDocument16 pagesCFAR Time Variation in The Equity Risk Premiumpby5145No ratings yet

- Unit 2 Financial PlanningDocument10 pagesUnit 2 Financial PlanningMalde KhuntiNo ratings yet

- Partnership AccountDocument9 pagesPartnership Accountndanujoy180No ratings yet

- 8 Business Purchase and MergerDocument39 pages8 Business Purchase and Mergerprincessaay99No ratings yet

- Kustia Sugar Mills Ltd. Audit Report 2021-2022Document20 pagesKustia Sugar Mills Ltd. Audit Report 2021-2022Prosad DharNo ratings yet

- VIDYA SAGAR Analysis - FR-3Document4 pagesVIDYA SAGAR Analysis - FR-3Dharani SsNo ratings yet

- BBA II Chapter 2 Sale of Partnership ProblemsDocument14 pagesBBA II Chapter 2 Sale of Partnership ProblemsSiddharth SalgaonkarNo ratings yet

- Moniepoint Document 2023-07-28T05 05.xlaDocument42 pagesMoniepoint Document 2023-07-28T05 05.xlacurtispengeleroyNo ratings yet

- GT CAPITAL HOLDINGS, INC. - SEC 17-C - Press Release - 3july23Document5 pagesGT CAPITAL HOLDINGS, INC. - SEC 17-C - Press Release - 3july23Diyo NagamoraNo ratings yet

- 06 0453 0253385 00 - Statement - 2023 02 10Document5 pages06 0453 0253385 00 - Statement - 2023 02 10Bikramjeet SinghNo ratings yet

- IGCSE Accounting - Revision NotesDocument42 pagesIGCSE Accounting - Revision Notesfathimath ahmedNo ratings yet

- 2021-11 Financial Statement - LMS0729sDocument5 pages2021-11 Financial Statement - LMS0729salexgambrel0No ratings yet

- Chapter 5 FMDocument22 pagesChapter 5 FMHananNo ratings yet

- Dwnload Full Financial and Managerial Accounting 4th Edition Wild Test Bank PDFDocument20 pagesDwnload Full Financial and Managerial Accounting 4th Edition Wild Test Bank PDFlanguor.shete0wkzrt100% (13)

- Module 1 Capital MarketDocument6 pagesModule 1 Capital MarketNovelyn Cena100% (1)

- Hots CompanyDocument5 pagesHots CompanySaloni JainNo ratings yet

- Accounting For Business Combination - AssessmentsDocument114 pagesAccounting For Business Combination - AssessmentsArn KylaNo ratings yet

- HomeworkDocument3 pagesHomeworkKressida BanhNo ratings yet

- Cup 2 (Far)Document8 pagesCup 2 (Far)Chan DagaleNo ratings yet

- MGT101 Mcq's Final Term by Vu Topper RMDocument72 pagesMGT101 Mcq's Final Term by Vu Topper RMMuhammad HassanNo ratings yet