You might also like

- Suganya Journal4Document7 pagesSuganya Journal4Subhash CheeliNo ratings yet

- Online Banking Services of India: 2/16/2022 Devanshi ParmarDocument96 pagesOnline Banking Services of India: 2/16/2022 Devanshi ParmarFLEX FFNo ratings yet

- Nisha Rupinder M ServicesinIndia A Study On Mobile Banking and ApplicationsDocument9 pagesNisha Rupinder M ServicesinIndia A Study On Mobile Banking and Applicationskalpesh bhNo ratings yet

- Nitish India Banking 00923009001533Document68 pagesNitish India Banking 00923009001533Ghulam AbbasNo ratings yet

- Main DataDocument59 pagesMain Datachinmay parsekarNo ratings yet

- HDFC Bank ReportDocument43 pagesHDFC Bank ReportAnkit SinhaNo ratings yet

- Prateek Bakliwal ICICIDocument48 pagesPrateek Bakliwal ICICIRajesh TyagiNo ratings yet

- UBI1Document66 pagesUBI1Rudra SinghNo ratings yet

- A Study On Banking System in India - IciciDocument7 pagesA Study On Banking System in India - IcicikizieNo ratings yet

- Bandhan BankDocument13 pagesBandhan Bankkumarshubham65391No ratings yet

- Master of Business Administration Rajasthan Technical University, KOTADocument70 pagesMaster of Business Administration Rajasthan Technical University, KOTAHatim AliNo ratings yet

- Alva'S College, Moodbidri A Unit ofDocument15 pagesAlva'S College, Moodbidri A Unit ofMass N WSNo ratings yet

- Banking Project OrginalfileDocument45 pagesBanking Project OrginalfileSnehal BhorkhadeNo ratings yet

- I.T. in Banking IndustryDocument102 pagesI.T. in Banking Industryshahin14380% (5)

- India Post Payments Bank: Delivering Banking Service at DoorstepDocument24 pagesIndia Post Payments Bank: Delivering Banking Service at DoorstepC K ParjapatiNo ratings yet

- Indian Banking SystemDocument53 pagesIndian Banking SystemConnect Net cafeNo ratings yet

- 2010 Live Project at Imantec: C A B, M P A MNC& N B IDocument15 pages2010 Live Project at Imantec: C A B, M P A MNC& N B Irakesh_raj68No ratings yet

- IPPB's Role in Financial Inclusion and Services OfferedDocument14 pagesIPPB's Role in Financial Inclusion and Services Offeredpavan patelNo ratings yet

- Internet Banking-3Document82 pagesInternet Banking-3urvashiNo ratings yet

- IJCRT2301008Document17 pagesIJCRT2301008hifeztobgglNo ratings yet

- A Study on Rural Banking in IndiaDocument19 pagesA Study on Rural Banking in IndiaMOHAMMED KHAYYUMNo ratings yet

- Icici Rural ExpansionDocument10 pagesIcici Rural ExpansionANiket BharadiyaNo ratings yet

- Tybbi ProjectDocument80 pagesTybbi ProjectSagar KhillareNo ratings yet

- Analysis of 5 Major Banking Institutions of IndiaDocument5 pagesAnalysis of 5 Major Banking Institutions of IndiaShikhar AroraNo ratings yet

- A Study On Customer Perception & Psychology Towards e - Banking With Reference To Mumbra RegionDocument8 pagesA Study On Customer Perception & Psychology Towards e - Banking With Reference To Mumbra RegionPooja Singh SolankiNo ratings yet

- basudev bankimg report 12345Document34 pagesbasudev bankimg report 12345Basudev KumarNo ratings yet

- Awareness and Usage of Payment Banks Among College StudentsDocument21 pagesAwareness and Usage of Payment Banks Among College StudentsMEERA JOSHY 1927436No ratings yet

- Financial Inclusion-Role of Payment Banks in India: IRA-International Journal of Management & Social SciencesDocument6 pagesFinancial Inclusion-Role of Payment Banks in India: IRA-International Journal of Management & Social Sciencesmonica niroliaNo ratings yet

- Effect of Payment Banks on India's Financial SystemDocument6 pagesEffect of Payment Banks on India's Financial SystemNithin JoseNo ratings yet

- 19bbl098, 19bbl110 - Law On Corporate FinanceDocument7 pages19bbl098, 19bbl110 - Law On Corporate FinanceBhumihar Shubham TejasNo ratings yet

- "Satisfaction From E-Banking Services. A Comparative Study of HDFC and ICICI Bank.Document131 pages"Satisfaction From E-Banking Services. A Comparative Study of HDFC and ICICI Bank.bairasiarachana84% (37)

- Shubham Goswami BBADocument43 pagesShubham Goswami BBAUmar ThukarNo ratings yet

- Bank of Maharastra Project ReportDocument33 pagesBank of Maharastra Project ReportBiswakesh Pati100% (1)

- Mobile Banking in IndiaDocument33 pagesMobile Banking in Indiaanir_1986No ratings yet

- v9n2-paper2 (1)Document11 pagesv9n2-paper2 (1)amitmali.armNo ratings yet

- Comparative Analysis of Saving Accounts of Indusind Bank With Different Private BanksDocument63 pagesComparative Analysis of Saving Accounts of Indusind Bank With Different Private Banksramkumar31No ratings yet

- Atm MaintenanceDocument59 pagesAtm MaintenanceRanjeet RajputNo ratings yet

- Online Banking Services by Axis BankDocument51 pagesOnline Banking Services by Axis BankmayurNo ratings yet

- A Comparative Study On Customer Satisfaction Towards Online Banking Services With Reference To Icici and HDFC Bank in LucknowDocument7 pagesA Comparative Study On Customer Satisfaction Towards Online Banking Services With Reference To Icici and HDFC Bank in LucknowChandan Srivastava100% (1)

- Perception of CustomersDocument14 pagesPerception of CustomersChandrika DasNo ratings yet

- Consumer Banking A Tool of Poverty Reduction & Socioeconomic DevelopmentDocument4 pagesConsumer Banking A Tool of Poverty Reduction & Socioeconomic DevelopmentsadiquehakimNo ratings yet

- ATM Services of Public and Private Sector Banks: A Study On Customer SatisfactionDocument5 pagesATM Services of Public and Private Sector Banks: A Study On Customer SatisfactionAsishNo ratings yet

- Rural Banking in India SynopsisDocument20 pagesRural Banking in India SynopsiskizieNo ratings yet

- Customers' Satisfaction On E Banking Services in Indian Banking SectorsDocument7 pagesCustomers' Satisfaction On E Banking Services in Indian Banking SectorsEditor IJTSRDNo ratings yet

- "Mobile Banking" SBI by Komal Sawant: A Project Report ONDocument27 pages"Mobile Banking" SBI by Komal Sawant: A Project Report ONsanket yelaweNo ratings yet

- Marwari CollegeDocument35 pagesMarwari CollegeAvinashNo ratings yet

- Punjab National Bank 1-Amit Kumar SrivastavaDocument66 pagesPunjab National Bank 1-Amit Kumar SrivastavaAwanish Kumar MauryaNo ratings yet

- SBI ATM Cardholders Satisfaction in Udumalpet TalukDocument6 pagesSBI ATM Cardholders Satisfaction in Udumalpet TalukgayathirimcomNo ratings yet

- The India Post Payments BankDocument5 pagesThe India Post Payments Bankanil peralaNo ratings yet

- SBI Mobile BankingDocument46 pagesSBI Mobile BankingAbhishek Tiwari100% (3)

- Daily Current Affairs Today 16th June PDF DownloadDocument16 pagesDaily Current Affairs Today 16th June PDF DownloadV-keyBansalNo ratings yet

- Icici Strategies FinalDocument32 pagesIcici Strategies FinalAjith ReddyNo ratings yet

- Online Banking and Customer Satisfaction in Public and Private Sector Banks: Evidence From IndiaDocument11 pagesOnline Banking and Customer Satisfaction in Public and Private Sector Banks: Evidence From IndiaRamachantran RamachantranNo ratings yet

- My ProjecpoppeeeeeeeeeeeestDocument52 pagesMy ProjecpoppeeeeeeeeeeeestpoppyNo ratings yet

- Blackbook ProjectDocument78 pagesBlackbook ProjectKriti Somani71% (28)

- Role of It in Banking ReportDocument27 pagesRole of It in Banking ReportPrathmesh JambhulkarNo ratings yet

- Role of Branchless Banking in Financial InclusionDocument5 pagesRole of Branchless Banking in Financial Inclusionnishija unnikrishnanNo ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Incubating Indonesia’s Young Entrepreneurs:: Recommendations for Improving Development ProgramsFrom EverandIncubating Indonesia’s Young Entrepreneurs:: Recommendations for Improving Development ProgramsNo ratings yet

- BoA - Deposit Form 05731Document2 pagesBoA - Deposit Form 05731Coy IngramNo ratings yet

- SPEAKING UNIT 10 Lets-Talk-About-MoneyDocument2 pagesSPEAKING UNIT 10 Lets-Talk-About-MoneyDavid Isaac Ruiz ChaconNo ratings yet

- Сommonwealth AUDocument3 pagesСommonwealth AUbefix80880No ratings yet

- Academic Test Report Form ConfirmationDocument4 pagesAcademic Test Report Form ConfirmationkabirNo ratings yet

- Banking Law KSLU Notes Grand FinalDocument83 pagesBanking Law KSLU Notes Grand FinalSherminasNo ratings yet

- SBI empanelment of CA firms as concurrent auditorsDocument33 pagesSBI empanelment of CA firms as concurrent auditorsShadab Malik67% (3)

- Initiate Business Checking: Important Account InformationDocument4 pagesInitiate Business Checking: Important Account InformationWeb TreamicsNo ratings yet

- The Accounting CycleDocument17 pagesThe Accounting Cycleyuvita prasadNo ratings yet

- Your Adv Plus Banking: Account SummaryDocument6 pagesYour Adv Plus Banking: Account SummaryOsvaldo Gómez GarciaNo ratings yet

- 4. application for reopen bank accountDocument6 pages4. application for reopen bank accounttown BoyNo ratings yet

- Q2 Chase CaseDocument2 pagesQ2 Chase CaseAnkur Gautam100% (2)

- Lloyds Bank: StatementDocument2 pagesLloyds Bank: StatementhanhNo ratings yet

- Aud 1&2 - CceDocument6 pagesAud 1&2 - Ccecherish melwinNo ratings yet

- Bank Reconciliation (Practice Quiz)Document4 pagesBank Reconciliation (Practice Quiz)MoniqueNo ratings yet

- RISE ITA Model Paper SolutionDocument15 pagesRISE ITA Model Paper Solutionzaffiii.293No ratings yet

- FNB Payment Reversal FormDocument2 pagesFNB Payment Reversal Formrecruitment SaNo ratings yet

- Cash Handling ProceduresDocument15 pagesCash Handling ProceduresMahabubnubNo ratings yet

- 03 Quiz 1Document9 pages03 Quiz 1Camille MadlangbayanNo ratings yet

- Unit 9 Material WorldDocument9 pagesUnit 9 Material WorldfelipeNo ratings yet

- Banking Services and Activities GuideDocument4 pagesBanking Services and Activities GuideGayatri DWNo ratings yet

- Research EssayDocument13 pagesResearch Essayapi-584024170No ratings yet

- Pre-Intermediate Unit 8 Audio ScriptDocument5 pagesPre-Intermediate Unit 8 Audio Scriptnadin nNo ratings yet

- Student Hostel Fee ReceiptDocument1 pageStudent Hostel Fee ReceiptHarneet KaurNo ratings yet

- Ju 1Document1 pageJu 1lesly malebrancheNo ratings yet

- SOP Credit Card Acceptance HotelsDocument3 pagesSOP Credit Card Acceptance HotelsImee S. YuNo ratings yet

- Students Edition On Cashbook: Capital 15,300 8,200Document5 pagesStudents Edition On Cashbook: Capital 15,300 8,200Geoffrey ObongoNo ratings yet

- Client Application FormDocument2 pagesClient Application FormKarla Jeanne CoNo ratings yet

- AccountingDocument290 pagesAccountingNibash KumuraNo ratings yet

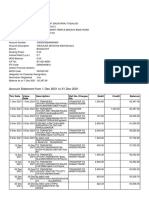

- Account statement for Mr. PRASHANT BASAVARAJ TADALAGIDocument2 pagesAccount statement for Mr. PRASHANT BASAVARAJ TADALAGIprashant tadalagiNo ratings yet

- White Paper The Business Model of Apple Pay and Apple CardDocument15 pagesWhite Paper The Business Model of Apple Pay and Apple CardTBeaver BuilderNo ratings yet