You might also like

- Assignment DMBA104 MBA 1 Set-1 and 2 Jan-Feb 2023Document6 pagesAssignment DMBA104 MBA 1 Set-1 and 2 Jan-Feb 2023Nihar KambleNo ratings yet

- Questions: Indicate Debit and Credit Eff Ects and Normal BalanceDocument11 pagesQuestions: Indicate Debit and Credit Eff Ects and Normal BalanceThiện Vũ100% (1)

- Manarang Auto Repair Shop Journal by The Month of January 2019Document9 pagesManarang Auto Repair Shop Journal by The Month of January 2019Renz MoralesNo ratings yet

- Project HSE PlanDocument33 pagesProject HSE PlanWinnie Eldama100% (2)

- Title of Module: Intermediate Accounting 3 Topic: I. Cash and Accrual Basis Learning ObjectivesDocument21 pagesTitle of Module: Intermediate Accounting 3 Topic: I. Cash and Accrual Basis Learning ObjectivesDenmark Cabaddu100% (1)

- Accounting Error and OmissionsDocument4 pagesAccounting Error and OmissionsDuas and Urdu Dramas/Movies50% (2)

- 5 Trial Balance and Adjustments UDDocument32 pages5 Trial Balance and Adjustments UDERICK MLINGWANo ratings yet

- QM Process Map PDFDocument1 pageQM Process Map PDFghafoorian_khoshgovar148850% (2)

- CZ21A MODEL Answer KeyDocument7 pagesCZ21A MODEL Answer KeymadhuNo ratings yet

- Chapter 1 - Correction of ErrorsDocument3 pagesChapter 1 - Correction of ErrorsHairizal Harun100% (1)

- Class Exercises - Accounting Errors - AnswersDocument4 pagesClass Exercises - Accounting Errors - Answerseshakaur100% (2)

- Rectification of ErrorDocument24 pagesRectification of ErrorPurva ChaudhariNo ratings yet

- L4 - ABFA1163 FA II (Student)Document4 pagesL4 - ABFA1163 FA II (Student)Xue YikNo ratings yet

- 6-Correction of ErrorsDocument8 pages6-Correction of Errorszohaib anwarNo ratings yet

- Chapter 6 The Trial BalanceDocument17 pagesChapter 6 The Trial BalanceENG ZI QINGNo ratings yet

- MGT101 12-15Document62 pagesMGT101 12-15Nasir BashirNo ratings yet

- 1.3 AnswersDocument2 pages1.3 Answersaysilislam528No ratings yet

- Chapter 12 - EDocument10 pagesChapter 12 - EbahuNo ratings yet

- Error of CorrectionDocument8 pagesError of CorrectionTeo Yu XuanNo ratings yet

- Rectification of Errors: Chapter-8Document16 pagesRectification of Errors: Chapter-8Mappiee siddiquieNo ratings yet

- Baf1101 CatDocument7 pagesBaf1101 CatCy RusNo ratings yet

- Accounting For ErrorsDocument10 pagesAccounting For Errorsjacksonkimani3617No ratings yet

- Poa T - 1Document3 pagesPoa T - 1SHEVENA A/P VIJIANNo ratings yet

- Chapter 7Document16 pagesChapter 7Thùy Vân NguyễnNo ratings yet

- 2nd Summative TestDocument2 pages2nd Summative Testje-ann montejoNo ratings yet

- Chapter 02 Correction of Error. (2a)Document33 pagesChapter 02 Correction of Error. (2a)M Kashif QaisraniNo ratings yet

- Acct 4Document6 pagesAcct 4Mopur NELLORENo ratings yet

- Correction of ErrorsDocument3 pagesCorrection of ErrorsHasan ShoaibNo ratings yet

- 7 - Conversion of Single Entry To Double Entry PDFDocument6 pages7 - Conversion of Single Entry To Double Entry PDFmiftah fauzi100% (2)

- Correction of ErrorsDocument5 pagesCorrection of Errorsmuhammad arifNo ratings yet

- Tutorial 2 Q Part 1 - Accounting Cycle For Trade and ServicesDocument8 pagesTutorial 2 Q Part 1 - Accounting Cycle For Trade and ServicesNezelle WongNo ratings yet

- Rectification of ErrorsDocument17 pagesRectification of ErrorsPraveen HaridasNo ratings yet

- Lecture Three - Correction of Accounting Errors, Control, Accounts and Bank Reconciliation StatementDocument45 pagesLecture Three - Correction of Accounting Errors, Control, Accounts and Bank Reconciliation Statementdacosta aboagyeNo ratings yet

- Acc Unit-22-AnswersDocument10 pagesAcc Unit-22-AnswersGeorgeNo ratings yet

- T3 Correction of Errors-R2Document42 pagesT3 Correction of Errors-R2HD DNo ratings yet

- Processing Purchase Invoices - TasksDocument4 pagesProcessing Purchase Invoices - TasksOratwa BlackNo ratings yet

- 00 Readings For Tut 3Document3 pages00 Readings For Tut 3PeiWen TanNo ratings yet

- CH 02 Unit 06Document32 pagesCH 02 Unit 06Saurabh S. VermaNo ratings yet

- Accounts Receivable P 315,300 Less: Allowance For Bad Debts (74,100) Accounts Receivable, Net P 241,200Document2 pagesAccounts Receivable P 315,300 Less: Allowance For Bad Debts (74,100) Accounts Receivable, Net P 241,200Carmella BalboaNo ratings yet

- Errors Suspense AccountDocument21 pagesErrors Suspense AccountShayan KhanNo ratings yet

- 2009 S3 Ase2007Document15 pages2009 S3 Ase2007May CcmNo ratings yet

- Senior High School Department: Quarter 3 - Module 11: Preparing Trial BalanceDocument8 pagesSenior High School Department: Quarter 3 - Module 11: Preparing Trial BalanceJaye RuantoNo ratings yet

- AssignmentDocument3 pagesAssignmentstefhannyhallegado913No ratings yet

- A1 Correction of ErrorsDocument21 pagesA1 Correction of ErrorsdiggywilldoitNo ratings yet

- Financial AccountingDocument25 pagesFinancial AccountingFatuhu Abba dandagoNo ratings yet

- FA (1st) May2018Document3 pagesFA (1st) May2018JahangirNo ratings yet

- Rectification of ErrorsDocument6 pagesRectification of ErrorsPrabir Kumer RoyNo ratings yet

- ACC407 - Chapter 4b - Trial BalanceDocument18 pagesACC407 - Chapter 4b - Trial BalanceA24 Izzah100% (1)

- Senior High School Department: Quarter 3 - Module 5: The Books of AccountsDocument10 pagesSenior High School Department: Quarter 3 - Module 5: The Books of AccountsJaye Ruanto100% (2)

- BBA-1.4-A.D.M Finance 2015 NewDocument3 pagesBBA-1.4-A.D.M Finance 2015 NewAnonymous NSNpGa3T93No ratings yet

- Tutorial 9 & 10 Control Accounts CorrectedDocument4 pagesTutorial 9 & 10 Control Accounts CorrectedGaba RieleNo ratings yet

- DMBA104Document8 pagesDMBA104chetan kansalNo ratings yet

- Green Beige Group Project PresentationDocument16 pagesGreen Beige Group Project PresentationwelchNo ratings yet

- Abm Fabm1 Airs LM q4-m9Document18 pagesAbm Fabm1 Airs LM q4-m9MEDILEN O. BORRESNo ratings yet

- Tutorial 8 Control AccountsDocument4 pagesTutorial 8 Control AccountsKubenderarubban BalachantharNo ratings yet

- FA2 Examiner Report Spet19-Aug20Document6 pagesFA2 Examiner Report Spet19-Aug20Areeb AhmadNo ratings yet

- Acc GR 10 Mid QP 2022-3Document7 pagesAcc GR 10 Mid QP 2022-3LegobjeNo ratings yet

- Turning Black Ink Into Gold: How to increase your company's profitability and market value through excellent financial performance reporting, analysis and controlFrom EverandTurning Black Ink Into Gold: How to increase your company's profitability and market value through excellent financial performance reporting, analysis and controlNo ratings yet

- 2 Standard Vacuum OilDocument5 pages2 Standard Vacuum OilMary Louise R. ConcepcionNo ratings yet

- BAUER Spezialtiefbau GMBH - ImagebrochureDocument0 pagesBAUER Spezialtiefbau GMBH - ImagebrochureagwsNo ratings yet

- Osmena V RamaDocument1 pageOsmena V RamaSuiNo ratings yet

- Dwnload Full Essentials of Management 9th Edition Dubrin Test Bank PDFDocument35 pagesDwnload Full Essentials of Management 9th Edition Dubrin Test Bank PDFisaack4iben100% (12)

- CDC UP Non-Functional Requirements Definition TemplateDocument9 pagesCDC UP Non-Functional Requirements Definition Templategopi_meruguNo ratings yet

- Uh Econ 607 NotesDocument255 pagesUh Econ 607 NotesDamla HacıNo ratings yet

- Cash and Liquidity Optimisation Europe Conference, Partnered With CrowdReviews - Com, Announces Xelix As The Treasury Innovation Fintech WinnerDocument2 pagesCash and Liquidity Optimisation Europe Conference, Partnered With CrowdReviews - Com, Announces Xelix As The Treasury Innovation Fintech WinnerPR.comNo ratings yet

- EnterpreneurshipDocument169 pagesEnterpreneurshipGirish Kumar50% (2)

- Examination Question and Answers, Set C (True or False), Chapter 2 - Analyzing TransactionsDocument2 pagesExamination Question and Answers, Set C (True or False), Chapter 2 - Analyzing TransactionsJohn Carlos DoringoNo ratings yet

- Google NCLDocument152 pagesGoogle NCLPieter Benjamin GrebeNo ratings yet

- Punjab Gramin Bank NotificationDocument9 pagesPunjab Gramin Bank NotificationkslnNo ratings yet

- PROJ Jul23 MBAN MEC901 Final 20230508101130.pdffileDocument3 pagesPROJ Jul23 MBAN MEC901 Final 20230508101130.pdffileUrvasheeNo ratings yet

- Portek Corporate Presentation 2012Document81 pagesPortek Corporate Presentation 2012Nha LuongNo ratings yet

- GE Today's News (1959)Document434 pagesGE Today's News (1959)Ed Palmer100% (1)

- Ohio State-Licensing Lawsuit, July 14, 2017Document35 pagesOhio State-Licensing Lawsuit, July 14, 2017Andrew Welsh-HugginsNo ratings yet

- Ch. 10 Managerial Accounting Ever Green SolutionsDocument18 pagesCh. 10 Managerial Accounting Ever Green Solutionsattique100% (1)

- Environmental Analysis of Textile IndustryDocument6 pagesEnvironmental Analysis of Textile IndustryTanmay Varshney100% (1)

- Liquidation AccountingDocument5 pagesLiquidation AccountingTomy Mathew100% (1)

- MFRS138 Intangible Assets UpdatedDocument76 pagesMFRS138 Intangible Assets UpdatedAnas AjwadNo ratings yet

- Image As A Factor For Enhancing Shopping PDFDocument14 pagesImage As A Factor For Enhancing Shopping PDFKavit BhatiaNo ratings yet

- Labor Week 1 DigestDocument6 pagesLabor Week 1 DigestDenise GordonNo ratings yet

- TPGR Full PresentationDocument25 pagesTPGR Full Presentationprasanna0% (1)

- "Analysis of Indian Sportswear Market": Submitted By: Chander Bhan Kumar M.F.M Sem.-IIDocument9 pages"Analysis of Indian Sportswear Market": Submitted By: Chander Bhan Kumar M.F.M Sem.-IIchandrabhansinghNo ratings yet

- Instruction For The Completion of Income Tax Return For Corporate in IndonesiaDocument51 pagesInstruction For The Completion of Income Tax Return For Corporate in IndonesiaJonathan Bara DiskaPutra KrisnantoNo ratings yet

- COUNTERTRADEDocument8 pagesCOUNTERTRADEaditibrijptlNo ratings yet

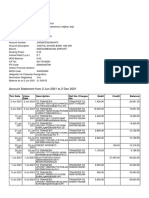

- Account Statement From 2 Jun 2021 To 2 Dec 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument6 pagesAccount Statement From 2 Jun 2021 To 2 Dec 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRavi PallaNo ratings yet

- Wasted: How America Is Losing Up To 40: Percent of Its Food From Farm To Fork To LandfillDocument26 pagesWasted: How America Is Losing Up To 40: Percent of Its Food From Farm To Fork To LandfillpapintoNo ratings yet

- Bba 3rd Semester Project Work A Study of Comparison Between Policy of HDFC Bank and State Bank of IndiaDocument29 pagesBba 3rd Semester Project Work A Study of Comparison Between Policy of HDFC Bank and State Bank of IndiaKARAN TRIPATHINo ratings yet