You might also like

- Solution 742381Document13 pagesSolution 742381GREATER HEIGHTS PUBLIC SCHOOLNo ratings yet

- Class 11 Accountancy Chapter-3 Revision NotesDocument11 pagesClass 11 Accountancy Chapter-3 Revision NotesMohd. Khushmeen KhanNo ratings yet

- Trial Balance: Credit Balances of All Accounts in The Ledger With A View To Test Arithmetical Accuracy of The BooksDocument5 pagesTrial Balance: Credit Balances of All Accounts in The Ledger With A View To Test Arithmetical Accuracy of The BooksPriyanka SharmaNo ratings yet

- Trail BalanceDocument6 pagesTrail BalanceDubai SheikhNo ratings yet

- Solution Manual For Horngrens Financial and Managerial Accounting The Financial Chapters 4Th Edition Nobles Mattison Matsumura 970133255577 0133255573 Full Chapter PDFDocument36 pagesSolution Manual For Horngrens Financial and Managerial Accounting The Financial Chapters 4Th Edition Nobles Mattison Matsumura 970133255577 0133255573 Full Chapter PDFnorman.washington378100% (11)

- Solution Manual For Horngrens Accounting The Financial Chapters 10Th Edition Nobles 0133117561 978013311756 Full Chapter PDFDocument36 pagesSolution Manual For Horngrens Accounting The Financial Chapters 10Th Edition Nobles 0133117561 978013311756 Full Chapter PDFgerard.lopez310100% (11)

- FYJC Book Keeping and Accuntancy Topic Final AccountDocument4 pagesFYJC Book Keeping and Accuntancy Topic Final AccountRavichandraNo ratings yet

- Sample Question Paper IN AccountancyDocument7 pagesSample Question Paper IN AccountancyRahul TyagiNo ratings yet

- Steps in The Accounting Process: Ans:1 Definition of Accounting. 1: The System of Recording and SummarizingDocument9 pagesSteps in The Accounting Process: Ans:1 Definition of Accounting. 1: The System of Recording and SummarizingshamagondalNo ratings yet

- BOOK KEEPING PROCEDURESDocument8 pagesBOOK KEEPING PROCEDURESNagarathna KulkarniNo ratings yet

- Account CHP 4Document9 pagesAccount CHP 4LOW YAN QINNo ratings yet

- FA Assistant Class Notes (Jan-13)Document9 pagesFA Assistant Class Notes (Jan-13)raj shahNo ratings yet

- Accounting For Managers Model Question Paper-1: First Semester MBA Degree ExaminationDocument5 pagesAccounting For Managers Model Question Paper-1: First Semester MBA Degree ExaminationRohan ChauguleNo ratings yet

- Trial balance essentialsDocument13 pagesTrial balance essentialsRahulNo ratings yet

- Solutions Totutorial 1-Fall 2022Document8 pagesSolutions Totutorial 1-Fall 2022chtiouirayyenNo ratings yet

- The Accounting Equation & The Accounting Cycle: Steps 1 - 4: Acct 1A&BDocument5 pagesThe Accounting Equation & The Accounting Cycle: Steps 1 - 4: Acct 1A&BKenneth Christian WilburNo ratings yet

- Weekly Summary For Self Study - Week 4 (Ch7-Receivables) (Rev F23)Document3 pagesWeekly Summary For Self Study - Week 4 (Ch7-Receivables) (Rev F23)That kid 246No ratings yet

- Recording Business TransactionsDocument36 pagesRecording Business Transactionsnorman.washington378100% (10)

- Unit 3 - Trial BalanceDocument11 pagesUnit 3 - Trial Balancegogo chanNo ratings yet

- Fundamentals AccountingDocument5 pagesFundamentals AccountingDennis N. IndigNo ratings yet

- Module 1 Chapter 2 Accounting ProcessDocument116 pagesModule 1 Chapter 2 Accounting ProcessADITYAROOP PATHAKNo ratings yet

- 1 September 2023 Regent - Financial Administartion 102 Presentation 1 September 2024Document36 pages1 September 2023 Regent - Financial Administartion 102 Presentation 1 September 202421620168No ratings yet

- Adjusted Trial BalanceDocument4 pagesAdjusted Trial BalanceMonir HossainNo ratings yet

- Class 11 Accountancy Solutions VPDocument7 pagesClass 11 Accountancy Solutions VPAyush MathiyanNo ratings yet

- Mid Term 2022 (Bsa1)Document4 pagesMid Term 2022 (Bsa1)An KhanhNo ratings yet

- Horngrens Accounting 11th Edition Miller Nobles Solutions ManualDocument26 pagesHorngrens Accounting 11th Edition Miller Nobles Solutions ManualColleenWeberkgsq100% (52)

- 2nd Summative TestDocument2 pages2nd Summative Testje-ann montejoNo ratings yet

- BankingDocument26 pagesBankingbhattag283No ratings yet

- 6 Incomplete RecordsDocument16 pages6 Incomplete Recordssana.ibrahimNo ratings yet

- Prime Academy 34 Session Progress Test - Advanced Accounting No. of Pages: 7 Total Marks: 75 Time Allowed: 2Hrs Part - ADocument46 pagesPrime Academy 34 Session Progress Test - Advanced Accounting No. of Pages: 7 Total Marks: 75 Time Allowed: 2Hrs Part - ALalitha NagarajanNo ratings yet

- Chapter 3the Accounting CycleDocument10 pagesChapter 3the Accounting CycleonakhogxamsheNo ratings yet

- Accounting Concepts and TransactionsDocument6 pagesAccounting Concepts and Transactionsawais awanNo ratings yet

- ACC407 - Chapter 4b - Trial BalanceDocument18 pagesACC407 - Chapter 4b - Trial BalanceA24 Izzah100% (1)

- Abm 005 2Q Week 12 PDFDocument10 pagesAbm 005 2Q Week 12 PDFJoel Vasquez MalunesNo ratings yet

- AdvanceedDocument102 pagesAdvanceedt8616046No ratings yet

- Accounting Recording ProcessDocument56 pagesAccounting Recording ProcessSara Abdelrahim MakkawiNo ratings yet

- 7 - Conversion of Single Entry To Double Entry PDFDocument6 pages7 - Conversion of Single Entry To Double Entry PDFmiftah fauzi100% (2)

- 0 - Anjali Sah AccountancyDocument16 pages0 - Anjali Sah AccountancySushmita BarlaNo ratings yet

- Chap 5 & 6Document46 pagesChap 5 & 6kaleabNo ratings yet

- 46604bosfnd p1 cp2 U1 PDFDocument30 pages46604bosfnd p1 cp2 U1 PDFPrasang GuptaNo ratings yet

- Befa Important Questions For Mid-IiDocument6 pagesBefa Important Questions For Mid-IiSAI PAVANNo ratings yet

- Recording Business TransactionsDocument36 pagesRecording Business Transactionsnorman.washington378100% (10)

- Accounts AnswersDocument12 pagesAccounts AnswersRafiya95z MynirNo ratings yet

- Class11AccountancySolutionsVP (2) (1) (3)Document7 pagesClass11AccountancySolutionsVP (2) (1) (3)visionrajput2005No ratings yet

- DaduDocument33 pagesDaduAnamika VatsaNo ratings yet

- 5125 - BR - Financial AccounitingDocument14 pages5125 - BR - Financial AccounitingjestinaNo ratings yet

- DIFFERENTIATE ERRORS AND FRAUDDocument9 pagesDIFFERENTIATE ERRORS AND FRAUDERICK ABDINo ratings yet

- SAMPURN Accounts Summary NotesDocument97 pagesSAMPURN Accounts Summary Noteszombiesunami007No ratings yet

- 6 Incomplete RecordsDocument16 pages6 Incomplete Recordssana.ibrahimNo ratings yet

- Class 11 Accountancy SolutionsDocument5 pagesClass 11 Accountancy SolutionsNisha SeksariaNo ratings yet

- Chapter 12 Review Updated 11th EdDocument13 pagesChapter 12 Review Updated 11th Edangelsalvador05082006No ratings yet

- Running a Small BusinessDocument20 pagesRunning a Small BusinessJenecil JavierNo ratings yet

- T10 Managing Finance Notes by SeahDocument43 pagesT10 Managing Finance Notes by SeahSeah Chooi KhengNo ratings yet

- CAB AcctDocument9 pagesCAB AcctA.J. ChuaNo ratings yet

- Acc 1 QuizDocument7 pagesAcc 1 QuizAyat MukahalNo ratings yet

- Unit End Questions For All UnitsDocument6 pagesUnit End Questions For All Unitsvenkata sai gireesh pNo ratings yet

- Accounting Books - Journals and LedgersDocument17 pagesAccounting Books - Journals and LedgersJessicaNo ratings yet

- MANUFACTURING AND NON-MANUFACTURING ENTITIES FINAL ACCOUNTSDocument13 pagesMANUFACTURING AND NON-MANUFACTURING ENTITIES FINAL ACCOUNTSRahul NegiNo ratings yet

- Accounting Principles and Practice: The Commonwealth and International Library: Commerce, Economics and Administration DivisionFrom EverandAccounting Principles and Practice: The Commonwealth and International Library: Commerce, Economics and Administration DivisionRating: 2.5 out of 5 stars2.5/5 (2)

- Kerala's Kadalundi Village & Bird SanctuaryDocument23 pagesKerala's Kadalundi Village & Bird SanctuaryMuhammad ZayanNo ratings yet

- Acknowledgement 20141002410Document1 pageAcknowledgement 20141002410Muhammad ZayanNo ratings yet

- Enrolment Intimatiion Letter For BBADocument1 pageEnrolment Intimatiion Letter For BBAMuhammad ZayanNo ratings yet

- Candidate Hall TicketDocument2 pagesCandidate Hall TicketSohil RashidNo ratings yet

- SRM Institute of Science and TechnologyDocument1 pageSRM Institute of Science and TechnologyMuhammad ZayanNo ratings yet

- Prospectives of Kadalundi Island As A Ecotourism DestinationDocument54 pagesProspectives of Kadalundi Island As A Ecotourism DestinationMuhammad ZayanNo ratings yet

- Unit 1Document31 pagesUnit 1Muhammad ZayanNo ratings yet

- Prospectives of Kadalundi Island As A Ecotourism DestinationDocument54 pagesProspectives of Kadalundi Island As A Ecotourism DestinationMuhammad ZayanNo ratings yet

- Prospectives of Kadalundi Island As A Ecotourism DestinationDocument54 pagesProspectives of Kadalundi Island As A Ecotourism DestinationMuhammad ZayanNo ratings yet

- EASY ROUND INCOME TAXESDocument13 pagesEASY ROUND INCOME TAXESCamila Mae AlduezaNo ratings yet

- Ledger Creation AssignmentDocument1 pageLedger Creation AssignmentRajeswari SathishkumarNo ratings yet

- Financial Accounting: Weygandt KimmelDocument82 pagesFinancial Accounting: Weygandt Kimmelclarysage13100% (1)

- Test Bank For Accounting Principles Volume 1 7th Canadian EditionDocument24 pagesTest Bank For Accounting Principles Volume 1 7th Canadian EditionPaigeDiazrmqp98% (48)

- English-Hindi Legal Glossary Part 1Document132 pagesEnglish-Hindi Legal Glossary Part 1Ghalendra Singh RajNo ratings yet

- 9110 - Job Order CostingDocument6 pages9110 - Job Order CostingJosua PagcaliwaganNo ratings yet

- Computer Best Store Accounts Receivable Subsidiary Ledgers: Date Explanation Ref. Debit Credit BalanceDocument60 pagesComputer Best Store Accounts Receivable Subsidiary Ledgers: Date Explanation Ref. Debit Credit BalanceArra StypayhorliksonNo ratings yet

- Training Manual For Union StorekeeperDocument7 pagesTraining Manual For Union StorekeeperTita Hils100% (1)

- Learn To Communicate With Accounting Staff: Cle - Creative Learning ExerciseDocument108 pagesLearn To Communicate With Accounting Staff: Cle - Creative Learning ExercisepasinNo ratings yet

- Practice Questions and Answers in AccounDocument100 pagesPractice Questions and Answers in Accounwalidabdo274No ratings yet

- Accounting Workbook Section 4 AnswersDocument49 pagesAccounting Workbook Section 4 AnswersAhmed Zeeshan100% (22)

- General Journal Page Number 01 Descriptions PR Debit CreditDocument12 pagesGeneral Journal Page Number 01 Descriptions PR Debit CreditKurt SoriaoNo ratings yet

- Trainee'S Record Book: Sibugay Technical Institute Incorporated Lower Taway, Ipil, Zamboanga SibugayDocument15 pagesTrainee'S Record Book: Sibugay Technical Institute Incorporated Lower Taway, Ipil, Zamboanga Sibugayjessica navajaNo ratings yet

- Business DocumentsDocument9 pagesBusiness DocumentsFaraiNo ratings yet

- Corrected File Unit 2 Final AccountDocument19 pagesCorrected File Unit 2 Final AccountUtkarsh SharmaNo ratings yet

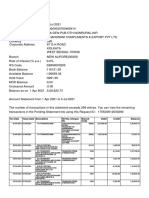

- Account Statement Summary for CHANDRANI COMPLIMENTS & EXPORT PVT LTDDocument12 pagesAccount Statement Summary for CHANDRANI COMPLIMENTS & EXPORT PVT LTDRaju RoyNo ratings yet

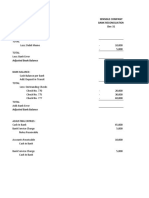

- Bank Reconciliation StatementDocument12 pagesBank Reconciliation StatementBhuvan PrajapatiNo ratings yet

- Class 11 Accounts Half Yearly SPDocument9 pagesClass 11 Accounts Half Yearly SPRakesh AgarwalNo ratings yet

- Oracle AP Training OverviewDocument29 pagesOracle AP Training OverviewMadhu Sudan ReddyNo ratings yet

- Chapter 2 Solutions and ExercisesDocument15 pagesChapter 2 Solutions and ExercisesKashif IshaqNo ratings yet

- Comprehensive Notes F010101T (B) Basic AccountingDocument74 pagesComprehensive Notes F010101T (B) Basic Accountingjyoti.singhNo ratings yet

- Advacc1 Accounting For Special Transactions (Advanced Accounting 1)Document21 pagesAdvacc1 Accounting For Special Transactions (Advanced Accounting 1)Stella SabaoanNo ratings yet

- Yfc Projects PVT Ltd. (New Delhi)Document1 pageYfc Projects PVT Ltd. (New Delhi)jatincasualNo ratings yet

- Ellen Company Cash Bank ReconciliationDocument8 pagesEllen Company Cash Bank ReconciliationShaine PacsonNo ratings yet

- Sensible Company Bank Reconciliation Dec-31Document8 pagesSensible Company Bank Reconciliation Dec-31OwO OwONo ratings yet

- Mechanics of VAT - Zimbabwe Revenue Authority (ZIMRA)Document2 pagesMechanics of VAT - Zimbabwe Revenue Authority (ZIMRA)Tinashe MukukuNo ratings yet

- Activity 3 - TolentinoDocument7 pagesActivity 3 - TolentinoDJazel Tolentino100% (1)

- Voucher TypesDocument4 pagesVoucher Typesshabbir_ahmad100% (1)

- BCLTE Mock Exam ReviewDocument27 pagesBCLTE Mock Exam ReviewXjsajajsja100% (33)

- Administrator: Nicole Roach Marketing Coordinator Bizcentral UsaDocument31 pagesAdministrator: Nicole Roach Marketing Coordinator Bizcentral Usashafie haredNo ratings yet