You might also like

- Controller Powers and FunctionsDocument10 pagesController Powers and Functions18ILB055 Archana YadavNo ratings yet

- JAIIB CAIIB MOCK TESTDocument36 pagesJAIIB CAIIB MOCK TESTrose GuptaNo ratings yet

- Customer Program Details SheetDocument21 pagesCustomer Program Details Sheetmanish yadavNo ratings yet

- Essential Concepts of Mutual FundsDocument51 pagesEssential Concepts of Mutual Fundsgauravmonga15100% (2)

- Malaysian Technical Cooperation Programme Scholarship Endorsement FormDocument1 pageMalaysian Technical Cooperation Programme Scholarship Endorsement FormA'del JummaNo ratings yet

- B.Tech Civil Syllabus AR16 RevisedDocument227 pagesB.Tech Civil Syllabus AR16 Revisedabhiram_23355681No ratings yet

- Csam Qsc2021 SlidesDocument123 pagesCsam Qsc2021 SlidesNurudeen MomoduNo ratings yet

- 2M00733 - Mms Mumbai University Result Sem 3 2023Document887 pages2M00733 - Mms Mumbai University Result Sem 3 2023anammominNo ratings yet

- Reporton Gas Leakage Detection SensorDocument13 pagesReporton Gas Leakage Detection SensorSambram A BNo ratings yet

- Screenshot 2022-03-07 at 10.33.06 PMDocument12 pagesScreenshot 2022-03-07 at 10.33.06 PMYash ChaudhariNo ratings yet

- Subcontracting work order to Go Green Vision SolutionsDocument2 pagesSubcontracting work order to Go Green Vision SolutionsN PiclabNo ratings yet

- 21mca2697 Himanshu Rubrics3Document26 pages21mca2697 Himanshu Rubrics3HimanshuNo ratings yet

- Federal Ministers of Pakistan 2022 - Download PDF List PDFDocument8 pagesFederal Ministers of Pakistan 2022 - Download PDF List PDFiftikhar ahmedNo ratings yet

- MNG201 Revision Q & ADocument60 pagesMNG201 Revision Q & AnevaenaickerNo ratings yet

- Sharad Finial 6Document67 pagesSharad Finial 6diptanshu gaikwadNo ratings yet

- March 2022 TissnetprepDocument42 pagesMarch 2022 TissnetprepVishal Maurya100% (1)

- Goldstar Laryngoscope ManufactureDocument35 pagesGoldstar Laryngoscope ManufactureWasim Bin ArshadNo ratings yet

- Apostila Parte 1 e 2 Ingles BeginnerDocument55 pagesApostila Parte 1 e 2 Ingles BeginnerMarcelo RochaNo ratings yet

- 22-13 OnDocument32 pages22-13 OnMyo MinNo ratings yet

- 1256imguf PlacedStudentsDetails 2018batchDocument21 pages1256imguf PlacedStudentsDetails 2018batchRavindra MeddegodaNo ratings yet

- Smarthands - ButtonDocument2 pagesSmarthands - ButtonhendrawinataNo ratings yet

- Fdocuments - in - Hero-Motocorp-Ltd-55844bb02b8ee (Repaired)Document66 pagesFdocuments - in - Hero-Motocorp-Ltd-55844bb02b8ee (Repaired)HIMANSHU KUMAR TIWARINo ratings yet

- Balaji Viswanathan's Answer To What Is Wrong With The Demolition of Babri Masjid? India's History Is Full of Muslim Invaders Plundering Hindu TemplesDocument15 pagesBalaji Viswanathan's Answer To What Is Wrong With The Demolition of Babri Masjid? India's History Is Full of Muslim Invaders Plundering Hindu TemplesShivangi AgrawalNo ratings yet

- Guide To Alabama's County Officials 2021Document16 pagesGuide To Alabama's County Officials 2021micheal williamNo ratings yet

- 2018 Ambiente Frankfurt ExhibitorsDocument16 pages2018 Ambiente Frankfurt Exhibitorscheng yifangNo ratings yet

- 2023 ADL NATHEALTH Digital ReportDocument35 pages2023 ADL NATHEALTH Digital ReportMoumita Roy ChowdhuryNo ratings yet

- Study Note 3 Preparation of Financial Statement of Profit Oriented OrganisatiosDocument27 pagesStudy Note 3 Preparation of Financial Statement of Profit Oriented Organisatiosnaga naveenNo ratings yet

- Madhya Pradesh MiningDocument20 pagesMadhya Pradesh MiningAnurag Ujjainkar100% (1)

- HSE Competence Training Level 1 2 and 3Document2 pagesHSE Competence Training Level 1 2 and 3wahyuNo ratings yet

- Transition Plan - Plan A and Plan BDocument10 pagesTransition Plan - Plan A and Plan Bapi-631400099No ratings yet

- Counselling Deck - ByJU's CAT - v1.2Document48 pagesCounselling Deck - ByJU's CAT - v1.2Pushparaj kNo ratings yet

- Evolution of the Indian Insurance IndustryDocument19 pagesEvolution of the Indian Insurance IndustrypdabhaadeNo ratings yet

- Fast Food Competition-3-29Document27 pagesFast Food Competition-3-29Thanh Hà TrầnNo ratings yet

- Rubrics 1Document13 pagesRubrics 1HimanshuNo ratings yet

- Arvind Limited Balance Sheet With Common SizeDocument4 pagesArvind Limited Balance Sheet With Common SizeAnkit VermaNo ratings yet

- GRC 16Document6 pagesGRC 16thotaNo ratings yet

- Client Attendance RecordsDocument30 pagesClient Attendance RecordsDexter Multi ServicesNo ratings yet

- Questionnaire 1. Personal DetailsDocument2 pagesQuestionnaire 1. Personal Detailspalash mannaNo ratings yet

- Bank Box Go SpecificationDocument8 pagesBank Box Go Specificationsafe upiNo ratings yet

- Current Account Summery 0 InvestmentsDocument530 pagesCurrent Account Summery 0 InvestmentsKhalid Aman KhanNo ratings yet

- Measuring Customer Satisfaction in BankingDocument81 pagesMeasuring Customer Satisfaction in Bankingsilent readersNo ratings yet

- Citi Group Case Study ReportDocument47 pagesCiti Group Case Study ReportChhin HuiNo ratings yet

- Jaiib Questions and Model Question PaperDocument52 pagesJaiib Questions and Model Question Paperவன்னியராஜாNo ratings yet

- CLASS X POLITICAL SCIENCE IMPORTANT CARTOON BASED QUESTIONS 2020-2021 ExamDocument27 pagesCLASS X POLITICAL SCIENCE IMPORTANT CARTOON BASED QUESTIONS 2020-2021 ExamSumit SinghNo ratings yet

- Interview Material Goa Division 2020 PDFDocument82 pagesInterview Material Goa Division 2020 PDFVasan AmbikaNo ratings yet

- STS1500014-001 Rev 4 HAZID Report For OceanGuard BWMS CompleteDocument71 pagesSTS1500014-001 Rev 4 HAZID Report For OceanGuard BWMS Completele huyNo ratings yet

- UntitledDocument3 pagesUntitledK A R A N M A L H O T R ANo ratings yet

- Kotak Life Insurance Industry and Customer Survey AnalysisDocument37 pagesKotak Life Insurance Industry and Customer Survey AnalysisSimran KaurNo ratings yet

- Complete Project 2023Document69 pagesComplete Project 2023Kirti WajgeNo ratings yet

- Implementation of Secure Authentication Technologies For DFS 1 1 PDFDocument66 pagesImplementation of Secure Authentication Technologies For DFS 1 1 PDFdavidNo ratings yet

- Accounting For Liabilities, Provisions and Contingencies LiabilityDocument13 pagesAccounting For Liabilities, Provisions and Contingencies LiabilitySkyleen Jacy VikeNo ratings yet

- APPRENTICE CONTRACTDocument2 pagesAPPRENTICE CONTRACTdramala69No ratings yet

- A Study On Distribution Practices.: With Reference To FMCG, Paints & Hardware IndustryDocument19 pagesA Study On Distribution Practices.: With Reference To FMCG, Paints & Hardware IndustryAMRUTHA KNo ratings yet

- Success – - GD TopicDocument2 pagesSuccess – - GD Topickhani dhariniNo ratings yet

- Profile DhanikuberjiDocument6 pagesProfile Dhanikuberjihetalahir149No ratings yet

- Usha Thorat Committee's Recommendations On Small Finance BanksDocument12 pagesUsha Thorat Committee's Recommendations On Small Finance BanksanjuNo ratings yet

- Adidas Springblade LawsuitDocument54 pagesAdidas Springblade LawsuitbrendandunneNo ratings yet

- Udkj Iïm A L Ukdlrkh Iy WD Ól N, MeuDocument6 pagesUdkj Iïm A L Ukdlrkh Iy WD Ól N, MeuSUSL 2021No ratings yet

- New FileDocument17 pagesNew FileMobile MediaNo ratings yet

- Heading Functional ProjectDocument6 pagesHeading Functional ProjectTusharJoshiNo ratings yet

- Pension Risk Lifecycles: A Framework for ERMDocument4 pagesPension Risk Lifecycles: A Framework for ERMMuhammad AlkahfiNo ratings yet

- Retirement Income Portfolios - Outcome Based SeriesDocument4 pagesRetirement Income Portfolios - Outcome Based SeriesRandy MarmerNo ratings yet

- Retirement Planning ChecklistDocument3 pagesRetirement Planning ChecklistbvbenhamNo ratings yet

- Active Ageing: Opinion On The Gender Dimension of Active Ageing and Solidarity Between Generations. Synthesis Report. 2011.Document171 pagesActive Ageing: Opinion On The Gender Dimension of Active Ageing and Solidarity Between Generations. Synthesis Report. 2011.Mary McKeonNo ratings yet

- Rufina Patis v. AlusitainDocument11 pagesRufina Patis v. AlusitainBeya AmaroNo ratings yet

- Savings Policy HighlightsDocument12 pagesSavings Policy HighlightsPatio BeeNo ratings yet

- Form 5A Return of Ownership To Be Sent To The Regional Commissioner PFDocument2 pagesForm 5A Return of Ownership To Be Sent To The Regional Commissioner PFRamana Kanth0% (2)

- Foreign Remittances - Inward and OutwardDocument54 pagesForeign Remittances - Inward and OutwardShehabziaNo ratings yet

- Pension RulesDocument7 pagesPension RulesVivek Pal SinghNo ratings yet

- 1996 HammondDocument22 pages1996 HammondTicking DoraditoNo ratings yet

- Agile Retirement Range Guarantees IncomeDocument11 pagesAgile Retirement Range Guarantees IncomeMariusNo ratings yet

- Santos-Vs-Servier-PhilippinesDocument2 pagesSantos-Vs-Servier-PhilippinesAnonymous V0JQmPJc33% (6)

- HBR-investing in A Retirement Plan. Assignment Questions 1. What..Document4 pagesHBR-investing in A Retirement Plan. Assignment Questions 1. What..Sannithi YamsawatNo ratings yet

- Sarla VarmaDocument28 pagesSarla VarmaKajeev KumarNo ratings yet

- Rate of ReturnDocument4 pagesRate of ReturnMichael MarioNo ratings yet

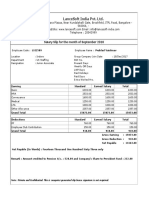

- LanceSoft September Salary SlipDocument1 pageLanceSoft September Salary SlipPRAHLAD VAISHNAV100% (1)

- What We Can Learn From Japanese ManagementDocument14 pagesWhat We Can Learn From Japanese Managementsinan5858No ratings yet

- Seafarers' Employment Agreement: (Written Example)Document7 pagesSeafarers' Employment Agreement: (Written Example)Bitzcomputer TechnologiesNo ratings yet

- Packages Internship Report On I.R Dept, by A HRM, by M.kashif Iqbal 03336866227Document40 pagesPackages Internship Report On I.R Dept, by A HRM, by M.kashif Iqbal 03336866227M Kashif IqbalNo ratings yet

- AFPS 15 Your Scheme ExplainedDocument34 pagesAFPS 15 Your Scheme ExplainedNointingNo ratings yet

- Signature AssignmentDocument15 pagesSignature Assignmentapi-527239212No ratings yet

- Employee Benefits and ServicesDocument9 pagesEmployee Benefits and ServicesAMIT K SINGHNo ratings yet

- Union BugDocument12 pagesUnion BugCasey SeilerNo ratings yet

- China Banking Corp v. HDMFDocument13 pagesChina Banking Corp v. HDMFJoanne CamacamNo ratings yet

- Putnam Individual 401 (K)Document2 pagesPutnam Individual 401 (K)Putnam InvestmentsNo ratings yet

- Ridgecrest TeachersDocument9 pagesRidgecrest TeachersSara ArenasNo ratings yet

- Employer Benefit - Part 2Document9 pagesEmployer Benefit - Part 2Julian Adam PagalNo ratings yet

- Present Value FactorDocument1 pagePresent Value FactorNgan Dang KieuNo ratings yet

- 10 Ways To Make 1 MillionDocument9 pages10 Ways To Make 1 MillionEduardo Salas100% (1)

- Business Finance Q4 Module 3Document21 pagesBusiness Finance Q4 Module 3randy magbudhi80% (15)

- Deduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesFrom EverandDeduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesRating: 3 out of 5 stars3/5 (3)

- What Everyone Needs to Know about Tax: An Introduction to the UK Tax SystemFrom EverandWhat Everyone Needs to Know about Tax: An Introduction to the UK Tax SystemNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesFrom EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesRating: 4 out of 5 stars4/5 (9)

- The Payroll Book: A Guide for Small Businesses and StartupsFrom EverandThe Payroll Book: A Guide for Small Businesses and StartupsRating: 5 out of 5 stars5/5 (1)

- Invested: How I Learned to Master My Mind, My Fears, and My Money to Achieve Financial Freedom and Live a More Authentic Life (with a Little Help from Warren Buffett, Charlie Munger, and My Dad)From EverandInvested: How I Learned to Master My Mind, My Fears, and My Money to Achieve Financial Freedom and Live a More Authentic Life (with a Little Help from Warren Buffett, Charlie Munger, and My Dad)Rating: 4.5 out of 5 stars4.5/5 (43)

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProFrom EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProRating: 4.5 out of 5 stars4.5/5 (43)

- Taxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingFrom EverandTaxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingRating: 5 out of 5 stars5/5 (3)

- How to get US Bank Account for Non US ResidentFrom EverandHow to get US Bank Account for Non US ResidentRating: 5 out of 5 stars5/5 (1)

- Owner Operator Trucking Business Startup: How to Start Your Own Commercial Freight Carrier Trucking Business With Little Money. Bonus: Licenses and Permits ChecklistFrom EverandOwner Operator Trucking Business Startup: How to Start Your Own Commercial Freight Carrier Trucking Business With Little Money. Bonus: Licenses and Permits ChecklistRating: 5 out of 5 stars5/5 (6)

- Bookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessFrom EverandBookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessRating: 5 out of 5 stars5/5 (5)

- The Hidden Wealth Nations: The Scourge of Tax HavensFrom EverandThe Hidden Wealth Nations: The Scourge of Tax HavensRating: 4.5 out of 5 stars4.5/5 (40)

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyFrom EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo ratings yet

- The Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyFrom EverandThe Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyRating: 4 out of 5 stars4/5 (52)

- Tax Accounting: A Guide for Small Business Owners Wanting to Understand Tax Deductions, and Taxes Related to Payroll, LLCs, Self-Employment, S Corps, and C CorporationsFrom EverandTax Accounting: A Guide for Small Business Owners Wanting to Understand Tax Deductions, and Taxes Related to Payroll, LLCs, Self-Employment, S Corps, and C CorporationsRating: 4 out of 5 stars4/5 (1)

- Lower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderFrom EverandLower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderRating: 5 out of 5 stars5/5 (4)

- How To Get IRS Tax Relief: The Complete Tax Resolution Guide for IRS: Back Tax Problems & Settlements, Offer in Compromise, Payment Plans, Federal Tax Liens & Levies, Penalty Abatement, and Much MoreFrom EverandHow To Get IRS Tax Relief: The Complete Tax Resolution Guide for IRS: Back Tax Problems & Settlements, Offer in Compromise, Payment Plans, Federal Tax Liens & Levies, Penalty Abatement, and Much MoreNo ratings yet

- Streetwise Incorporating Your Business: From Legal Issues to Tax Concerns, All You Need to Establish and Protect Your BusinessFrom EverandStreetwise Incorporating Your Business: From Legal Issues to Tax Concerns, All You Need to Establish and Protect Your BusinessNo ratings yet