You might also like

- Ita34 1058123249Document3 pagesIta34 1058123249Bahlakoana NtsasaNo ratings yet

- Get NoticeDocument3 pagesGet NoticeJo anne Jo anneNo ratings yet

- Get NoticeDocument3 pagesGet NoticeLetsoai MalesaNo ratings yet

- Pillay Naidoo 56 Vaalboskat Street Hesteapark Ext 8 Pretoria Noord 0182Document4 pagesPillay Naidoo 56 Vaalboskat Street Hesteapark Ext 8 Pretoria Noord 0182Spoton AutomotiveNo ratings yet

- VV Tinnie 4402 Umnga Crescent Langa 7455: Contact CentreDocument3 pagesVV Tinnie 4402 Umnga Crescent Langa 7455: Contact Centrebra9tee9tiniNo ratings yet

- Richard Pizzey Archive Cra 19 PDFDocument17 pagesRichard Pizzey Archive Cra 19 PDFnancy2handsorNo ratings yet

- Notice of Assessment 2019 04 29 02 32 21 264865Document4 pagesNotice of Assessment 2019 04 29 02 32 21 264865Dennis EnnsNo ratings yet

- Costel Mitrofan, SA Tax Return 1Document2 pagesCostel Mitrofan, SA Tax Return 1Flutur GavrilNo ratings yet

- 2022 T1 Form - CompletedDocument8 pages2022 T1 Form - CompletedARSH GROVERNo ratings yet

- Notice of Assessment - Year Ended 30 June 2023: Miss Sheralie L Shadforth 8 Clabon ST Hillcrest QLD 4118Document2 pagesNotice of Assessment - Year Ended 30 June 2023: Miss Sheralie L Shadforth 8 Clabon ST Hillcrest QLD 4118shadforth1977No ratings yet

- A Guide To Our HMRC Tax Calculation & Tax Year Overview RequirementsDocument7 pagesA Guide To Our HMRC Tax Calculation & Tax Year Overview RequirementsbswaminaNo ratings yet

- IT Return Acknowledgement Slip 6328994Document1 pageIT Return Acknowledgement Slip 6328994waqar100No ratings yet

- Jose AbreuDocument39 pagesJose Abreueddy britoNo ratings yet

- W2 Matthew RussellDocument2 pagesW2 Matthew Russellmatthewrussell661No ratings yet

- 1120s PDFDocument5 pages1120s PDFBreann MorrisNo ratings yet

- Thank You For Paying On-Time: Basic Housing Solutions, IncDocument1 pageThank You For Paying On-Time: Basic Housing Solutions, IncMarcelo AnfoneNo ratings yet

- Tax Credit Certificate 2023 9552312947779Document2 pagesTax Credit Certificate 2023 9552312947779Toni rogers CardosoNo ratings yet

- 34 Wihh 504331 H 0714320240524151104202Document3 pages34 Wihh 504331 H 0714320240524151104202jamelmhunt22No ratings yet

- Profit or Loss From Business: I I I I I I I IDocument1 pageProfit or Loss From Business: I I I I I I I Idolapo BalogunNo ratings yet

- 2019 Tax Year Assessment Ivolpe PDFDocument5 pages2019 Tax Year Assessment Ivolpe PDFLISA VOLPENo ratings yet

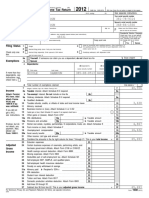

- U.S. Individual Income Tax Return: Filing StatusDocument2 pagesU.S. Individual Income Tax Return: Filing StatusCoen WalterNo ratings yet

- Noa-Iit Ob212020062419132485y PDFDocument1 pageNoa-Iit Ob212020062419132485y PDFilamahizhNo ratings yet

- E0800J3WXBDocument2 pagesE0800J3WXBAhmed Al AdawiNo ratings yet

- Jojoe Agyeman RBC Mar 2022Document2 pagesJojoe Agyeman RBC Mar 2022Ali HassanNo ratings yet

- SGS Technical Services Pvt. LTD.: Attendance Details ValueDocument1 pageSGS Technical Services Pvt. LTD.: Attendance Details Valueshalabh chopraNo ratings yet

- Statement of Account 2 16 Apr 19 To 15 May 19 880757036: Total Amount Due: P1,684.16Document2 pagesStatement of Account 2 16 Apr 19 To 15 May 19 880757036: Total Amount Due: P1,684.16Dat Doria PalerNo ratings yet

- SCAN & PAY Through Paytm Fill Details & Complete: (Authorised Signatory)Document1 pageSCAN & PAY Through Paytm Fill Details & Complete: (Authorised Signatory)ashishNo ratings yet

- Private & Confidential: Re: Your Medical Card ApplicationDocument7 pagesPrivate & Confidential: Re: Your Medical Card ApplicationjulieannagormanNo ratings yet

- Preview 26Document15 pagesPreview 26kakabadzebaiaNo ratings yet

- P45 Part 1A Details of Employee Leaving WorkDocument3 pagesP45 Part 1A Details of Employee Leaving WorkCaleb PriceNo ratings yet

- SCHNEIDERS (00102) Peridic Billing Statement Ending 03.15.2017 - RedactedDocument1 pageSCHNEIDERS (00102) Peridic Billing Statement Ending 03.15.2017 - Redactedlarry-612445No ratings yet

- Account # 0302080036: Lifegreen SavingsDocument2 pagesAccount # 0302080036: Lifegreen Savingsstorage mediaNo ratings yet

- Employee Information Pay Stub InformationDocument1 pageEmployee Information Pay Stub Informationrenato pimentelNo ratings yet

- ShowDocument2 pagesShowBrianna Jean-BaptisteNo ratings yet

- Cash FlowDocument1 pageCash Flowpawan_019No ratings yet

- Payslip Month Ending 30 November 2022Document1 pagePayslip Month Ending 30 November 2022zeppo1234No ratings yet

- Noa-Iit Ob2620150425142233zb4 PDFDocument1 pageNoa-Iit Ob2620150425142233zb4 PDFKanza KhanNo ratings yet

- Statement of Benefits 30 04 2020Document10 pagesStatement of Benefits 30 04 2020Chris MillsNo ratings yet

- Avis 2018 Revenus 2017Document15 pagesAvis 2018 Revenus 2017Arnaud CalisteNo ratings yet

- Statement2023 PDFDocument2 pagesStatement2023 PDFkayrincoddington2424No ratings yet

- Ambulance: VictoriaDocument2 pagesAmbulance: VictoriaJames WearneNo ratings yet

- Tax Return 2023Document2 pagesTax Return 2023jacksonleah313No ratings yet

- Is in Kind 03-16-09Document1 pageIs in Kind 03-16-09Azi PaybarahNo ratings yet

- Agent Appointment FormDocument2 pagesAgent Appointment FormSatyen ChikhliaNo ratings yet

- P45 Part 1A Details of Employee Leaving WorkDocument6 pagesP45 Part 1A Details of Employee Leaving WorkCatalin FandaracNo ratings yet

- RMCL Certioficate of IncorporationDocument3 pagesRMCL Certioficate of IncorporationDr M R aggarwaalNo ratings yet

- Payslip EPay 20231026Document1 pagePayslip EPay 20231026jacksparrow2023mayNo ratings yet

- Hong Thien PhuocBui2018Document6 pagesHong Thien PhuocBui2018Thien BaoNo ratings yet

- Terms and Conditions: Helpdesk - Cbe@actcorp - inDocument2 pagesTerms and Conditions: Helpdesk - Cbe@actcorp - inshibu lijackNo ratings yet

- P 50Document2 pagesP 50Emily DeerNo ratings yet

- A218 DocumentDocument9 pagesA218 DocumentJose AlmonteNo ratings yet

- Tax Year To 5 April 2020 This Is A Printed Copy of An Ep60: To The Employee: Pay and Income Tax DetailsDocument1 pageTax Year To 5 April 2020 This Is A Printed Copy of An Ep60: To The Employee: Pay and Income Tax DetailsNatalino GuterresNo ratings yet

- Payslip Guip47020020112020 PDFDocument1 pagePayslip Guip47020020112020 PDFElena BarsukovaNo ratings yet

- Bill CE Donald Collup 02-07-20 0218 CSDocument6 pagesBill CE Donald Collup 02-07-20 0218 CSMike MarchukNo ratings yet

- PL1 22912 1316456 9776899 Net 30 Days XGT 561083721466Document2 pagesPL1 22912 1316456 9776899 Net 30 Days XGT 561083721466RuodNo ratings yet

- NBR Tin Certificate 499536876199 PDFDocument1 pageNBR Tin Certificate 499536876199 PDFhasan raisNo ratings yet

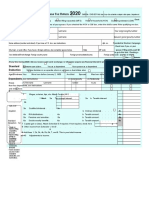

- U.S. Individual Income Tax Return: Filing StatusDocument3 pagesU.S. Individual Income Tax Return: Filing StatuspyatetskyNo ratings yet

- Form 16a - TDS - Blank 16aDocument1 pageForm 16a - TDS - Blank 16aJayNo ratings yet

- Get NoticeDocument4 pagesGet Noticejohn kolokoNo ratings yet

- VV Tinnie 4402 Umnga Crescent Langa Cape Town 7455: Contact CentreDocument3 pagesVV Tinnie 4402 Umnga Crescent Langa Cape Town 7455: Contact Centrebra9tee9tiniNo ratings yet

- Itl152 2024 01 SGDocument118 pagesItl152 2024 01 SGFolaNo ratings yet

- Itl152 2024 01 SGDocument118 pagesItl152 2024 01 SGFolaNo ratings yet

- Annexure 1B PDFDocument1 pageAnnexure 1B PDFFolaNo ratings yet

- Q1C Memo Without MarksDocument1 pageQ1C Memo Without MarksFolaNo ratings yet

- Q1A Memo Without MarksDocument2 pagesQ1A Memo Without MarksFolaNo ratings yet

- Q1A Student TemplateDocument1 pageQ1A Student TemplateFolaNo ratings yet