You might also like

- Accounting - Week 2 - Syndicate 3 - CVP Excel DemoDocument3 pagesAccounting - Week 2 - Syndicate 3 - CVP Excel DemoKrishna Rai0% (1)

- COST3Document7 pagesCOST3Jan Mark CastilloNo ratings yet

- Partnership Accounting - Paula GozunDocument8 pagesPartnership Accounting - Paula GozunPaupauNo ratings yet

- Partnership Operation ExercisesDocument3 pagesPartnership Operation ExercisesArlene Diane OrozcoNo ratings yet

- Partnership Operation ExercisesDocument3 pagesPartnership Operation ExercisesArlene Diane OrozcoNo ratings yet

- Partnership Q6 SolutionDocument4 pagesPartnership Q6 SolutionLorraine Mae RobridoNo ratings yet

- Partnership Q6 SolutionDocument4 pagesPartnership Q6 SolutionLorraine Mae RobridoNo ratings yet

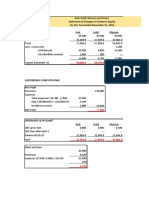

- Red, Gold, Maroon and Green Statement of Changes in Partners' Equity For The Year Ended December 31, 2016Document7 pagesRed, Gold, Maroon and Green Statement of Changes in Partners' Equity For The Year Ended December 31, 2016Vivienne Rozenn LaytoNo ratings yet

- FDNACCT - Quiz #1 - Solutions To PSDocument2 pagesFDNACCT - Quiz #1 - Solutions To PSIchi HasukiNo ratings yet

- Cost AccountingDocument24 pagesCost AccountingJalo NacionNo ratings yet

- Randall Corporation and Sharp Company Consolidation Worksheet December 31, 20X7Document5 pagesRandall Corporation and Sharp Company Consolidation Worksheet December 31, 20X7Diane MagnayeNo ratings yet

- CH 9 ExamplesDocument2 pagesCH 9 ExamplesAisha PatelNo ratings yet

- Advanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FDocument7 pagesAdvanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FJames CantorneNo ratings yet

- Chapter 8 de Leon 2014 PDFDocument4 pagesChapter 8 de Leon 2014 PDFIshan ChuaNo ratings yet

- 100,000 550,000 200,000 50,000 Net Loss: 100,000/.20% 500,000Document3 pages100,000 550,000 200,000 50,000 Net Loss: 100,000/.20% 500,000Alizah BucotNo ratings yet

- Illustrative Problem PayrollDocument23 pagesIllustrative Problem PayrollSophia VistanNo ratings yet

- ACCOUNTING FOR LABOR AND OH LectureDocument13 pagesACCOUNTING FOR LABOR AND OH LectureNah HamzaNo ratings yet

- Income Taxation Answer ExamDocument5 pagesIncome Taxation Answer Examyezaquera100% (1)

- REBYUDocument16 pagesREBYUChi EstrellaNo ratings yet

- Ast Chapter 1 MCPDocument14 pagesAst Chapter 1 MCPElleNo ratings yet

- E5-26A: Cost-Method Consolidation For Majority-Owned SubsidiaryDocument9 pagesE5-26A: Cost-Method Consolidation For Majority-Owned SubsidiaryeryNo ratings yet

- Assignment 9 FARDocument23 pagesAssignment 9 FARcha618717No ratings yet

- AP-5906Q ReceivablesDocument3 pagesAP-5906Q Receivablesjhouvan100% (1)

- Example KPI With GraphsDocument4 pagesExample KPI With GraphsSathesh AustinNo ratings yet

- Equity MethodDocument2 pagesEquity MethodJeane Mae BooNo ratings yet

- ANSWER KEY - FM - Mcom Sem 4 - June 2023Document5 pagesANSWER KEY - FM - Mcom Sem 4 - June 2023Faheem KwtNo ratings yet

- Extra Session 2 (30 Sept 2022) Spreadsheet (CH 3)Document2 pagesExtra Session 2 (30 Sept 2022) Spreadsheet (CH 3)georgius gabrielNo ratings yet

- Final Preboard SolutionDocument74 pagesFinal Preboard SolutionJhedz CartasNo ratings yet

- 2024 Caee BudgetDocument2 pages2024 Caee Budgetapi-201129963No ratings yet

- Assignment in Partnership DissolutionDocument4 pagesAssignment in Partnership DissolutionLalaine Keendra GonzagaNo ratings yet

- StoqnamadruateDocument4 pagesStoqnamadruateDela cruz, Hainrich (Hain)No ratings yet

- Chapter 2Document83 pagesChapter 2Eliza RiveraNo ratings yet

- Answers To Reviewer in Acctg 2Document3 pagesAnswers To Reviewer in Acctg 2Fatima AsprerNo ratings yet

- CH 19Document4 pagesCH 19Nickey DickeyNo ratings yet

- Jawaban PR Ke YgugjhftvfyugjDocument2 pagesJawaban PR Ke YgugjhftvfyugjDidin GstNo ratings yet

- DividendsDocument13 pagesDividendsTrixieNo ratings yet

- Buenaventura, EJ FAR2Document18 pagesBuenaventura, EJ FAR2AnonnNo ratings yet

- Partnership Dissolution ProblemsDocument22 pagesPartnership Dissolution ProblemsMikhaella ZamoraNo ratings yet

- Homework Ch5-Second Week 1Document19 pagesHomework Ch5-Second Week 1api-557133689No ratings yet

- TAX SolutionsDocument24 pagesTAX SolutionsJerome MadrigalNo ratings yet

- EOLA's Equity Distribution - v4Document18 pagesEOLA's Equity Distribution - v4AR-Lion ResearchingNo ratings yet

- Answer Illustration 6Document4 pagesAnswer Illustration 6apokelloNo ratings yet

- B127-Aragon-A No 4Document6 pagesB127-Aragon-A No 4Shaina AragonNo ratings yet

- Income & Expense SummaryDocument18 pagesIncome & Expense SummaryCrestina100% (3)

- Dec 14Document16 pagesDec 14Natasha AzzariennaNo ratings yet

- B, Capital After Admission 480,000: Problem 1 #1Document6 pagesB, Capital After Admission 480,000: Problem 1 #1Alizah BucotNo ratings yet

- Answer c22Document3 pagesAnswer c22Võ Huỳnh BăngNo ratings yet

- Answer 26 Sophia Test 2017Document2 pagesAnswer 26 Sophia Test 2017skye SNo ratings yet

- Acctba2 Units2 3 1Document15 pagesAcctba2 Units2 3 1Anonymous I2lXq5No ratings yet

- TabbelDocument2 pagesTabbelLyra EscosioNo ratings yet

- AnswersDocument3 pagesAnswersRaff LesiaaNo ratings yet

- PRIA FAR - 015 Employee Benefits (PAS 19) Notes and SolutionDocument5 pagesPRIA FAR - 015 Employee Benefits (PAS 19) Notes and SolutionEnrique Hills RiveraNo ratings yet

- USANA Binary Compensation Plan Voted #1 in The Industry: Put It To Work For You! Put It To Work For You!Document12 pagesUSANA Binary Compensation Plan Voted #1 in The Industry: Put It To Work For You! Put It To Work For You!powerbookuserNo ratings yet

- Module 1: Donor'S Taxation Lesson 1 Activities:: Name: Daniel I. Dialino Section: BSA 3-4Document21 pagesModule 1: Donor'S Taxation Lesson 1 Activities:: Name: Daniel I. Dialino Section: BSA 3-4Daniel DialinoNo ratings yet

- MC Solution Pages 2 61 To 2 66Document8 pagesMC Solution Pages 2 61 To 2 66sumagpangkeannecleinNo ratings yet

- Ch09Part02.Home Office and Branch Accounting (Special Problems) PDFDocument2 pagesCh09Part02.Home Office and Branch Accounting (Special Problems) PDFStephanie Ann AsuncionNo ratings yet

- Adjusted Trial Balance To Financial StatementsDocument16 pagesAdjusted Trial Balance To Financial StatementsABM ST.MATTHEW Misa john carloNo ratings yet

- Acccob1 Online Quiz 3 - Solution Guide (Part Iii)Document3 pagesAcccob1 Online Quiz 3 - Solution Guide (Part Iii)Abe Miguel BullecerNo ratings yet

- AFAR1 Operation SolutionDocument4 pagesAFAR1 Operation SolutionMiru YuNo ratings yet

- The Planning Processes Group - Integration ManagementDocument5 pagesThe Planning Processes Group - Integration ManagementRianne NavidadNo ratings yet

- The Planning Processes Group - Stakeholder ManagementdocxDocument3 pagesThe Planning Processes Group - Stakeholder ManagementdocxRianne NavidadNo ratings yet

- Existence in Japanese Sentence PatternDocument44 pagesExistence in Japanese Sentence PatternRianne NavidadNo ratings yet

- Transfer PricingDocument13 pagesTransfer PricingRianne NavidadNo ratings yet

- Ultimate Japanese Verb Conjugation GuideDocument30 pagesUltimate Japanese Verb Conjugation GuideRianne NavidadNo ratings yet

- MAS - CVP AnalysisDocument10 pagesMAS - CVP AnalysisRianne NavidadNo ratings yet

- 2021 Answer Chapter 3 PDFDocument11 pages2021 Answer Chapter 3 PDFRianne NavidadNo ratings yet

- Introduction To Management AccountingDocument12 pagesIntroduction To Management AccountingRianne NavidadNo ratings yet

- 2021 Answer CHAPTER 2 PDFDocument18 pages2021 Answer CHAPTER 2 PDFRianne NavidadNo ratings yet

- 2023 Answer CHAPTER 6 PDFDocument8 pages2023 Answer CHAPTER 6 PDFRianne NavidadNo ratings yet

- 2021 Answer Chapter 5 PDFDocument19 pages2021 Answer Chapter 5 PDFRianne NavidadNo ratings yet

- Afar 2 Practice Test (3rd Year)Document8 pagesAfar 2 Practice Test (3rd Year)Rianne NavidadNo ratings yet

- 2023 Answer CHAPTER 8 PDFDocument8 pages2023 Answer CHAPTER 8 PDFRianne NavidadNo ratings yet

- Adjusting Entries - ProblemDocument1 pageAdjusting Entries - ProblemRianne NavidadNo ratings yet