You might also like

- Quiz For 3rd ExamDocument2 pagesQuiz For 3rd ExamSantiago BuladacoNo ratings yet

- Chapter 4 Caselette Audit of ReceivablesDocument37 pagesChapter 4 Caselette Audit of ReceivablesXXXXXXXXXXXXXXXXXXNo ratings yet

- The Professional CPA Review School - Auditing Problems First Preboard ExamDocument18 pagesThe Professional CPA Review School - Auditing Problems First Preboard ExamRodmae VersonNo ratings yet

- MASTERY CLASS IN AUDITING PROBLEMS Part 1 Prob 1 9Document35 pagesMASTERY CLASS IN AUDITING PROBLEMS Part 1 Prob 1 9Mark Gelo WinchesterNo ratings yet

- AT08 Audit Sampling (PSA 530)Document6 pagesAT08 Audit Sampling (PSA 530)John Paul SiodacalNo ratings yet

- Chapter 11Document45 pagesChapter 11MangoStarr Aibelle VegasNo ratings yet

- Intermediate Acctg A 1 10Document10 pagesIntermediate Acctg A 1 10Leonila RiveraNo ratings yet

- Reviewer 1st PB P1 1920Document7 pagesReviewer 1st PB P1 1920Therese AcostaNo ratings yet

- Prelim Exam - Intermediate Accounting Part 1Document13 pagesPrelim Exam - Intermediate Accounting Part 1Vincent AbellaNo ratings yet

- CDD - Semi Finals Examination - Auditing TheoryDocument14 pagesCDD - Semi Finals Examination - Auditing TheoryFeelingerang MAYoraNo ratings yet

- LagunaDocument8 pagesLagunarandom17341No ratings yet

- Assurance Services FundamentalsDocument10 pagesAssurance Services FundamentalsLysss EpssssNo ratings yet

- Sample Problems On CashDocument9 pagesSample Problems On Cashcriszel4sobejanaNo ratings yet

- Audit of Receivables: Problem No. 1Document6 pagesAudit of Receivables: Problem No. 1Kathrina RoxasNo ratings yet

- Correction of ErrorsDocument5 pagesCorrection of ErrorsJohn Carlo DelorinoNo ratings yet

- CPA Review Code of Ethics for Professional Accountants in the PhilippinesDocument11 pagesCPA Review Code of Ethics for Professional Accountants in the PhilippinesAljur SalamedaNo ratings yet

- Auditing & Assurance 2 Part 6 - Audit of Revenues & A/R - ExercisesDocument6 pagesAuditing & Assurance 2 Part 6 - Audit of Revenues & A/R - ExerciseskmarisseeNo ratings yet

- Advanced Financial Accounting TopicsDocument16 pagesAdvanced Financial Accounting TopicsNhel AlvaroNo ratings yet

- Corporate LiquidationDocument7 pagesCorporate LiquidationAcads PurposesNo ratings yet

- Auditing Problems Midterm - 2021 - DDocument17 pagesAuditing Problems Midterm - 2021 - DjasfNo ratings yet

- Auditing Practice (AP) : #128 Maginhawa ST., Brgy. Teacher's Village East, Quezon City Pinnaclecpareview - PHDocument27 pagesAuditing Practice (AP) : #128 Maginhawa ST., Brgy. Teacher's Village East, Quezon City Pinnaclecpareview - PHWinnie ToribioNo ratings yet

- Assurance Engagement QuizDocument7 pagesAssurance Engagement Quizdave excelleNo ratings yet

- Internal Control Measures: Page 1 of 7Document7 pagesInternal Control Measures: Page 1 of 7Lucy HeartfiliaNo ratings yet

- Quiz 2 AuditingDocument4 pagesQuiz 2 AuditingCrissa Mae Falsis100% (1)

- ACCY 303 Midterm Exam ReviewDocument12 pagesACCY 303 Midterm Exam ReviewCORNADO, MERIJOY G.No ratings yet

- AP-03 Audit of Intangible AssetsDocument11 pagesAP-03 Audit of Intangible AssetsMitch MinglanaNo ratings yet

- AT 04 Practice - Regulation of The ProfessionDocument6 pagesAT 04 Practice - Regulation of The ProfessionPrincesNo ratings yet

- Philippine Standards On Auditing (Psas)Document2 pagesPhilippine Standards On Auditing (Psas)Levi Emmanuel Veloso BravoNo ratings yet

- Total Bills = P 800Coins 10.00 x 50 pieces = P 500 5.00 x 15 pieces = 75 0.25 x 32 pieces = 8Document8 pagesTotal Bills = P 800Coins 10.00 x 50 pieces = P 500 5.00 x 15 pieces = 75 0.25 x 32 pieces = 8Anonymous LC5kFdtcNo ratings yet

- Aud Theo Compilation1Document97 pagesAud Theo Compilation1AiahNo ratings yet

- AT05 Further Audit Procedures (Tests of Controls) PSA 520Document4 pagesAT05 Further Audit Procedures (Tests of Controls) PSA 520John Paul SiodacalNo ratings yet

- Practice Problems Corporate LiquidationDocument2 pagesPractice Problems Corporate LiquidationAllira OrcajadaNo ratings yet

- Financial Accounting and Reporting - ReviewerDocument12 pagesFinancial Accounting and Reporting - ReviewerRonald SaludesNo ratings yet

- Dayag Notes Partnership DissolutionDocument3 pagesDayag Notes Partnership DissolutionGirl Lang AkoNo ratings yet

- Chapter 11 - RR: ConsignmentDocument17 pagesChapter 11 - RR: ConsignmentJane DizonNo ratings yet

- AP Quiz 005 2015 AR and InvestmentsDocument6 pagesAP Quiz 005 2015 AR and InvestmentsGwenneth BachusNo ratings yet

- Accounting For Special Transactions:: Corporate LiquidationDocument28 pagesAccounting For Special Transactions:: Corporate LiquidationKim EllaNo ratings yet

- Corporate Liquidation DFCAMCLPDocument13 pagesCorporate Liquidation DFCAMCLPJessaNo ratings yet

- Module Far1 Unit-1 Part-1bDocument5 pagesModule Far1 Unit-1 Part-1bHazel Jane EsclamadaNo ratings yet

- CHAPTER 03 - Pg.4-6Document4 pagesCHAPTER 03 - Pg.4-6JabonJohnKennethNo ratings yet

- Topic 5 Consignment Sales ModuleDocument4 pagesTopic 5 Consignment Sales ModuleMaricel Ann BaccayNo ratings yet

- Taxation Final Preboard CPAR 92 PDFDocument17 pagesTaxation Final Preboard CPAR 92 PDFomer 2 gerdNo ratings yet

- CL Cup 2018 (AUD, TAX, RFBT)Document4 pagesCL Cup 2018 (AUD, TAX, RFBT)sophiaNo ratings yet

- Answers Managerial Accounting Prelim ExaminationDocument4 pagesAnswers Managerial Accounting Prelim ExaminationRegine ReyesNo ratings yet

- CHAPTER 7 Auditing-Theory-MCQs-by-Salosagcol-with-answersDocument2 pagesCHAPTER 7 Auditing-Theory-MCQs-by-Salosagcol-with-answersMichNo ratings yet

- Problem 1Document4 pagesProblem 1redassdawnNo ratings yet

- CH 17Document32 pagesCH 17Aldrin CabangbangNo ratings yet

- Audit of Investments - Set ADocument4 pagesAudit of Investments - Set AZyrah Mae SaezNo ratings yet

- Impairment of Investment PropertyDocument5 pagesImpairment of Investment PropertyDesiree Nicole ReyesNo ratings yet

- Question: Austral & Company Has A Debt Ratio of 0.5, A Total Assets Turnover Ratio of 0.25, and A Pro ..Document3 pagesQuestion: Austral & Company Has A Debt Ratio of 0.5, A Total Assets Turnover Ratio of 0.25, and A Pro ..Malik AsadNo ratings yet

- Advac SemifinalDocument8 pagesAdvac SemifinalDIVINE VILLENANo ratings yet

- Audit of PPE ExercisesDocument3 pagesAudit of PPE ExercisesMARCUAP Flora Mel Joy H.No ratings yet

- Chapter12 - AnswerDocument26 pagesChapter12 - AnswerAubreyNo ratings yet

- CPAR B94 FAR Final PB Exam - Answers - SolutionsDocument8 pagesCPAR B94 FAR Final PB Exam - Answers - SolutionsJazehl ValdezNo ratings yet

- MS B45 First PB With AnswersDocument13 pagesMS B45 First PB With AnswersSophia RabacalNo ratings yet

- ACCO 30043: Quiz Number 1 (Introduction To Assurance and Audit Services)Document16 pagesACCO 30043: Quiz Number 1 (Introduction To Assurance and Audit Services)pat lanceNo ratings yet

- Far - Team PRTC 1stpb May 2023Document8 pagesFar - Team PRTC 1stpb May 2023Alexander IgotNo ratings yet

- Midterm Exam ADocument16 pagesMidterm Exam ARed YuNo ratings yet

- FARAP 4702 ReceivablesDocument8 pagesFARAP 4702 Receivablesliberace cabreraNo ratings yet

- Receivables Theories and ProblemsDocument5 pagesReceivables Theories and ProblemsMaria Kathreena Andrea AdevaNo ratings yet

- FARAP-4501 (Cash and Cash Equivalents)Document10 pagesFARAP-4501 (Cash and Cash Equivalents)Marya NvlzNo ratings yet

- Farap 4505Document7 pagesFarap 4505Marya NvlzNo ratings yet

- Farap 4504Document8 pagesFarap 4504Marya NvlzNo ratings yet

- Farap 4503Document12 pagesFarap 4503Marya Nvlz100% (1)

- Theory Method Contingent ValuationDocument14 pagesTheory Method Contingent ValuationNugraha Eka SaputraNo ratings yet

- Urbit Data White Paper Details Vision for Transparent Real Estate Marketplace Using BlockchainDocument30 pagesUrbit Data White Paper Details Vision for Transparent Real Estate Marketplace Using BlockchainTessa HallNo ratings yet

- Ipsas Training - Impairement of AssetsDocument49 pagesIpsas Training - Impairement of AssetsNassib Songoro100% (1)

- Eric Woon Kim Thak: Education/QualificationDocument1 pageEric Woon Kim Thak: Education/Qualificationeric woonNo ratings yet

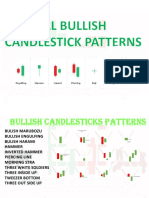

- All Bullish Candlestick Pattern by Optrading00 Telegram Optrading00Document25 pagesAll Bullish Candlestick Pattern by Optrading00 Telegram Optrading00Samitm TamhankarNo ratings yet

- Lesson 4 Earnings ManagementDocument28 pagesLesson 4 Earnings ManagementDerek DadzieNo ratings yet

- Valuing Water: The United Nations World Water Development Report 2021Document206 pagesValuing Water: The United Nations World Water Development Report 2021Is RaelNo ratings yet

- Ejercicios Semana 3 Sesión 1 B (Evaluación de Proyectos)Document3 pagesEjercicios Semana 3 Sesión 1 B (Evaluación de Proyectos)Alison Joyce Herrera Maldonado0% (1)

- Manipulation of Financial Statements V0.1Document17 pagesManipulation of Financial Statements V0.1Aniket RaneNo ratings yet

- Accounting Standard 11Document21 pagesAccounting Standard 11Pranesh KhambeNo ratings yet

- Acctg 105 QuizDocument5 pagesAcctg 105 Quizshin shinNo ratings yet

- Consolidated FM NotesDocument227 pagesConsolidated FM NotesTitus GachuhiNo ratings yet

- Bullet Proof InvestingDocument25 pagesBullet Proof InvestingNiru0% (1)

- The Capital Asset Pricing Model: Some Empirical Tests: Mjensen@Hbs - EduDocument54 pagesThe Capital Asset Pricing Model: Some Empirical Tests: Mjensen@Hbs - EduRdpthNo ratings yet

- Audit of Investment-Ap05-SolutionDocument23 pagesAudit of Investment-Ap05-SolutionmarkNo ratings yet

- 3333 OCW L2-Site Valuation Progress PaymentDocument25 pages3333 OCW L2-Site Valuation Progress PaymentSharifah suuNo ratings yet

- DCF Approach To Valuation PDFDocument8 pagesDCF Approach To Valuation PDFLucky LuckyNo ratings yet

- Innovation and Strategy in The Digital EconomyDocument42 pagesInnovation and Strategy in The Digital EconomyTrixibelle Lyah Allaine100% (1)

- Single 132694674963b77b6ac13faDocument17 pagesSingle 132694674963b77b6ac13faducdungphamNo ratings yet

- Merrill Lynch 2007 Analyst Valuation TrainingDocument74 pagesMerrill Lynch 2007 Analyst Valuation TrainingJose Garcia100% (21)

- Nmims Sep 2019 Solved Assignment 3rd and 4th SemDocument32 pagesNmims Sep 2019 Solved Assignment 3rd and 4th SemRajni KumariNo ratings yet

- Bangalore University MBA FinanceDocument31 pagesBangalore University MBA FinanceRakeshChowdaryKNo ratings yet

- Studi Kelayakan Investasi Pada Proyek Peningkatan JalanDocument18 pagesStudi Kelayakan Investasi Pada Proyek Peningkatan JalanIrma MartaNo ratings yet

- Direct Tax LawsDocument3 pagesDirect Tax LawsDitesh AgarwalNo ratings yet

- CR Progress Test QuestionsDocument9 pagesCR Progress Test QuestionsSophie ChopraNo ratings yet

- SAP MM Interview Questions Level 2 SupportDocument16 pagesSAP MM Interview Questions Level 2 SupportGuru Prasad100% (1)

- Untitled DocumentDocument5 pagesUntitled DocumentArif MelsingNo ratings yet

- Unit 2: Indian Accounting Standard 34: Interim Financial ReportingDocument28 pagesUnit 2: Indian Accounting Standard 34: Interim Financial ReportingvijaykumartaxNo ratings yet

- EMC - Tech M&A MonthlyDocument31 pagesEMC - Tech M&A Monthlyelong3102No ratings yet

- Banyan Tree Holdings RestructuringDocument18 pagesBanyan Tree Holdings RestructuringdfghfiNo ratings yet