You might also like

- SAUDIA vs. REBESENCIODocument12 pagesSAUDIA vs. REBESENCIOHermay BanarioNo ratings yet

- Accession CasesDocument95 pagesAccession CasesMeku DigeNo ratings yet

- Plaintiff-Appellant vs. vs. Respondents-Appellees Solicitor General Meer, Meer & MeerDocument7 pagesPlaintiff-Appellant vs. vs. Respondents-Appellees Solicitor General Meer, Meer & MeerVMNo ratings yet

- Bataan Shipyard & Engineering Co. v. PCGG, G.R. No. L-75885, May 27, 1987, 150 SCRA 181Document54 pagesBataan Shipyard & Engineering Co. v. PCGG, G.R. No. L-75885, May 27, 1987, 150 SCRA 181Joffrey UrianNo ratings yet

- CIR v. BPI, G.R. No. 147375, 2006Document2 pagesCIR v. BPI, G.R. No. 147375, 2006BREL GOSIMATNo ratings yet

- CIR. v. YumexDocument115 pagesCIR. v. YumexPio Vincent BuencaminoNo ratings yet

- UntitledDocument8 pagesUntitledhelen socayenNo ratings yet

- ADR Mod 3 DigestDocument11 pagesADR Mod 3 DigestChristian Jave PagayonNo ratings yet

- Sony Philippines tax disputeDocument12 pagesSony Philippines tax disputeAnisah AquilaNo ratings yet

- Finals ReviewerDocument36 pagesFinals ReviewerAlysa AsidoNo ratings yet

- COMELEC Ruling on Age Requirement for SK ElectionsDocument14 pagesCOMELEC Ruling on Age Requirement for SK ElectionsBestie BushNo ratings yet

- SAUDIA v. CADocument4 pagesSAUDIA v. CAPat NaffyNo ratings yet

- Philippine Supreme Court rules on civil liability in criminal case of estafaDocument11 pagesPhilippine Supreme Court rules on civil liability in criminal case of estafaJUDIE VICTORIANo ratings yet

- Afisco Insurance Corporation, Et. Al. vs. Court of AppealsDocument2 pagesAfisco Insurance Corporation, Et. Al. vs. Court of AppealsJahn Avery Mitchel DatukonNo ratings yet

- Evidence: Hearsay RuleDocument20 pagesEvidence: Hearsay RuleNeil Davis BulanNo ratings yet

- Labor Standards (Transcriptions - Edited)Document14 pagesLabor Standards (Transcriptions - Edited)Antonina ConcepcionNo ratings yet

- NAT RES Case DigestDocument43 pagesNAT RES Case DigestAubrey BalindanNo ratings yet

- GR 254510 2021 Novation Solidary Obligation DivisibleDocument19 pagesGR 254510 2021 Novation Solidary Obligation DivisibleChristine Gel MadrilejoNo ratings yet

- #4. CIR Vs Morgan Bank. FTDocument9 pages#4. CIR Vs Morgan Bank. FTeizNo ratings yet

- Court Sets Aside Dismissal of Complaint, Directs Compliance with Request for Admission Regarding War Damage ClaimDocument1 pageCourt Sets Aside Dismissal of Complaint, Directs Compliance with Request for Admission Regarding War Damage ClaimTet DomingoNo ratings yet

- Banking GNDocument27 pagesBanking GNchan.aNo ratings yet

- Evidence of Uncompleted Road Project Sufficient to Uphold ConvictionDocument3 pagesEvidence of Uncompleted Road Project Sufficient to Uphold ConvictionEnrico DizonNo ratings yet

- Beatingco vs. Gasis - Article 1544 - CorpinDocument2 pagesBeatingco vs. Gasis - Article 1544 - CorpinJemNo ratings yet

- 2015 Q & A in Political LawDocument40 pages2015 Q & A in Political LawCatherine Joy CataminNo ratings yet

- Corporation Law Divina LMTDocument595 pagesCorporation Law Divina LMTjoliwanagNo ratings yet

- Transpo Set 7Document11 pagesTranspo Set 7Jica GulaNo ratings yet

- Caminos, Jr. v. PeopleDocument13 pagesCaminos, Jr. v. PeoplesophiaNo ratings yet

- 10 Estate of Nelson Dulay v. Aboitiz Jebsen Maritime (Capulong)Document2 pages10 Estate of Nelson Dulay v. Aboitiz Jebsen Maritime (Capulong)luis capulongNo ratings yet

- Heirs of Jose Lim vs. Lim 614 Scra 141, March 03, 2010Document3 pagesHeirs of Jose Lim vs. Lim 614 Scra 141, March 03, 2010FranzMordenoNo ratings yet

- OPT, Excise, DST, Tax RemediesDocument11 pagesOPT, Excise, DST, Tax RemediesLou Brad Nazareno IgnacioNo ratings yet

- DIGEST - Remolona v. CSCDocument2 pagesDIGEST - Remolona v. CSCAgatha ApolinarioNo ratings yet

- SSS Death BenefitsDocument2 pagesSSS Death BenefitsTootsie Guzma100% (1)

- Lasam-Vs-SmithDocument2 pagesLasam-Vs-Smithflor100% (1)

- Velasquez v. Lisondra LandDocument10 pagesVelasquez v. Lisondra Landjagabriel616No ratings yet

- Principles of Taxation (BSBA)Document51 pagesPrinciples of Taxation (BSBA)Bernadette LeaNo ratings yet

- Credit Transactions Case DigestsDocument133 pagesCredit Transactions Case DigestsRochel Andag AnactaNo ratings yet

- Capital Insurance Surety Co. vs. Del Monte Motor WorksDocument5 pagesCapital Insurance Surety Co. vs. Del Monte Motor WorksRalf Vincent OcañadaNo ratings yet

- Commercial Law CasesDocument8 pagesCommercial Law CasesMAIMAI CABIGASNo ratings yet

- Tipon Art. 10Document10 pagesTipon Art. 10yeusoff haydn jaafarNo ratings yet

- Evidence Revised Rules (Am-19!08!15-Sc)Document29 pagesEvidence Revised Rules (Am-19!08!15-Sc)Ralph Ronald CatipayNo ratings yet

- Sps. Marano V Pryce Gases Inc.Document8 pagesSps. Marano V Pryce Gases Inc.Neil BorjaNo ratings yet

- Assigned - Digest - Prime White Cement Corporation Vs IacDocument2 pagesAssigned - Digest - Prime White Cement Corporation Vs IacTauMu AcademicNo ratings yet

- Vital-Gozon v. Court of AppealsDocument3 pagesVital-Gozon v. Court of AppealsEarl Anthony ArceNo ratings yet

- GWENDOLYN GARCIA CHALLENGES SANDIGANBAYAN'S AUTHORITY TO ISSUE HOLD DEPARTURE ORDERSDocument3 pagesGWENDOLYN GARCIA CHALLENGES SANDIGANBAYAN'S AUTHORITY TO ISSUE HOLD DEPARTURE ORDERSCezz SerenoNo ratings yet

- INDOPHIL TEXTILE MILL WORKERS UNION Vs CALICA - FERNANDEZDocument2 pagesINDOPHIL TEXTILE MILL WORKERS UNION Vs CALICA - FERNANDEZemmanuel fernandezNo ratings yet

- Mago vs. Sun Power Manufacturing Limited, G.R. No. 210961, January 24, 2018Document25 pagesMago vs. Sun Power Manufacturing Limited, G.R. No. 210961, January 24, 2018Trea CheryNo ratings yet

- 2020 11 Samson V Central AzucareraDocument4 pages2020 11 Samson V Central AzucareraBaltazar LlenosNo ratings yet

- Prosecutor Vs HalilovicDocument309 pagesProsecutor Vs HalilovicSteps RolsNo ratings yet

- DBP Vs LicuananDocument2 pagesDBP Vs Licuanancheryl talisikNo ratings yet

- EMPLOYMENT LAW GUIDE COVERS KEY CONCEPTS LIKE LABOR-ONLY CONTRACTINGDocument61 pagesEMPLOYMENT LAW GUIDE COVERS KEY CONCEPTS LIKE LABOR-ONLY CONTRACTINGAmitaf Napsu100% (1)

- Case No. 6 - POE-VS-COMELECDocument3 pagesCase No. 6 - POE-VS-COMELECgerald quijanoNo ratings yet

- Outline CSCDocument4 pagesOutline CSCNap GonzalesNo ratings yet

- Cir VS SC Johnson and Son IncDocument3 pagesCir VS SC Johnson and Son IncCharmaine Ganancial SorianoNo ratings yet

- PrelimCASE DIGEST Final WorkDocument18 pagesPrelimCASE DIGEST Final WorkHannah Denise BatallangNo ratings yet

- ALTERNATIVE DISPUTE RESOLUTION CASE DIGESTSDocument44 pagesALTERNATIVE DISPUTE RESOLUTION CASE DIGESTScelNo ratings yet

- PEZA Citizen's Charter PDFDocument154 pagesPEZA Citizen's Charter PDFRomer LesondatoNo ratings yet

- People vs. Pentecostes, 844 Scra 610, November 08, 2017Document19 pagesPeople vs. Pentecostes, 844 Scra 610, November 08, 2017Joel Dawn Tumanda SajorgaNo ratings yet

- Constitutional Law (Bill of Rights)Document60 pagesConstitutional Law (Bill of Rights)Ma Angelica Grace AbanNo ratings yet

- Philex Mining Corp Vs CIRDocument2 pagesPhilex Mining Corp Vs CIRWilliam Christian Dela Cruz100% (2)

- Philex Mining v. CIRDocument4 pagesPhilex Mining v. CIRSophiaFrancescaEspinosaNo ratings yet

- 131 Deluao V Casteel YeungDocument5 pages131 Deluao V Casteel YeungJohn YeungNo ratings yet

- 145 - Aguila JR V CADocument2 pages145 - Aguila JR V CAJai HoNo ratings yet

- 151 - Tocao V CADocument2 pages151 - Tocao V CAJai HoNo ratings yet

- 150 - Ortega V CADocument1 page150 - Ortega V CAJai HoNo ratings yet

- 137 - Bourns V CarmanDocument1 page137 - Bourns V CarmanJai HoNo ratings yet

- 127 - Yulo V Yang Chiao SengDocument2 pages127 - Yulo V Yang Chiao SengJai HoNo ratings yet

- SC Rules No Partnership Existed Beyond Scope of AcknowledgmentDocument3 pagesSC Rules No Partnership Existed Beyond Scope of AcknowledgmentJai HoNo ratings yet

- Heirs of Jose Lim Appeal CA Ruling on Elfledo PartnershipDocument3 pagesHeirs of Jose Lim Appeal CA Ruling on Elfledo PartnershipJai HoNo ratings yet

- 136 - Heirs of Tan Eng KeeDocument4 pages136 - Heirs of Tan Eng KeeJai HoNo ratings yet

- 257 Pimentel V AguirreDocument2 pages257 Pimentel V AguirreJai HoNo ratings yet

- 118 - Torres V CADocument2 pages118 - Torres V CAJai HoNo ratings yet

- Local Autonomy Violated by LGSEF EarmarkingDocument3 pagesLocal Autonomy Violated by LGSEF EarmarkingJai HoNo ratings yet

- 118 Berks Broadcasting V CraumerDocument2 pages118 Berks Broadcasting V CraumerJai HoNo ratings yet

- 119 - Lim Tong Lim Vs Phil Fishing GearDocument2 pages119 - Lim Tong Lim Vs Phil Fishing GearJai HoNo ratings yet

- 123 McLaran Vs CrescentDocument2 pages123 McLaran Vs CrescentJai HoNo ratings yet

- Directors Must Prioritize Stockholder Profits Over Charitable GoalsDocument2 pagesDirectors Must Prioritize Stockholder Profits Over Charitable GoalsJai HoNo ratings yet

- Wins Produced CalculationDocument19 pagesWins Produced CalculationJai HoNo ratings yet

- 122 Burk v. Ottawa Gas - ElectricDocument1 page122 Burk v. Ottawa Gas - ElectricJai HoNo ratings yet

- 119 Lich v. US RubberDocument2 pages119 Lich v. US RubberJai HoNo ratings yet

- Lepanto v Nielson dispute over mining management contract dividendsDocument5 pagesLepanto v Nielson dispute over mining management contract dividendsJai HoNo ratings yet

- 120 Keough V St. Paul Milk CoDocument2 pages120 Keough V St. Paul Milk CoJai HoNo ratings yet

- The Great Carmelo DebateDocument9 pagesThe Great Carmelo DebateJai HoNo ratings yet

- Philippine Basketball Association - Air21 Express Player StatisticsDocument1 pagePhilippine Basketball Association - Air21 Express Player StatisticsJai HoNo ratings yet

- Philippine Basketball Association - Alaska Aces Player StatisticsDocument1 pagePhilippine Basketball Association - Alaska Aces Player StatisticsJai HoNo ratings yet

- Philippine Basketball Association - 2010-2011 Governors Cup Overall Player EfficiencyDocument3 pagesPhilippine Basketball Association - 2010-2011 Governors Cup Overall Player EfficiencyJai HoNo ratings yet

- Rebound RateDocument1 pageRebound RateJai HoNo ratings yet

- Philippine Basketball Association - B-Meg Llamados Player StatisticsDocument1 pagePhilippine Basketball Association - B-Meg Llamados Player StatisticsJai HoNo ratings yet

- 58 Petron Vs Talk 'N Text FINALSDocument2 pages58 Petron Vs Talk 'N Text FINALSJai HoNo ratings yet

- Philippine Basketball Association - 2010-2011 Governor's Cup Statistical PointsDocument3 pagesPhilippine Basketball Association - 2010-2011 Governor's Cup Statistical PointsJai HoNo ratings yet

- Home Loan Lap Disbursement ChecklistDocument1 pageHome Loan Lap Disbursement ChecklistJaved QasimNo ratings yet

- Sa Puregold, Always Panalo!: N R D C I NDocument7 pagesSa Puregold, Always Panalo!: N R D C I NTumamudtamud, JenaNo ratings yet

- Intermediate Accounting 1 - InventoriesDocument9 pagesIntermediate Accounting 1 - InventoriesLien LaurethNo ratings yet

- (Circular E), Employer's Tax Guide: Future DevelopmentsDocument49 pages(Circular E), Employer's Tax Guide: Future DevelopmentsJoel PanganibanNo ratings yet

- Major and Minor Programmes 2022-23Document11 pagesMajor and Minor Programmes 2022-23Kelly lamNo ratings yet

- A Simple Explanation of How Money Moves Around The Banking System - Richard Gendal BrownDocument12 pagesA Simple Explanation of How Money Moves Around The Banking System - Richard Gendal BrownAlijaNuhićNo ratings yet

- Analyze Financial Health with Key MetricsDocument12 pagesAnalyze Financial Health with Key Metricsayushi kapoorNo ratings yet

- 7110 w15 Ms 22 PDFDocument9 pages7110 w15 Ms 22 PDFRachel RAMSAMYNo ratings yet

- Quiz #2 exercises - probabilities, distributions, samplingDocument3 pagesQuiz #2 exercises - probabilities, distributions, samplinglouise carino50% (2)

- Policybazaar: Indian Institute of Management RaipurDocument7 pagesPolicybazaar: Indian Institute of Management RaipurKaran SardaNo ratings yet

- The Ultimate SaaS Metrics Cheat SheetDocument2 pagesThe Ultimate SaaS Metrics Cheat SheetTạ Thị Mai - VIVANo ratings yet

- Sample Term SheetDocument9 pagesSample Term SheetSubhash PrajapatNo ratings yet

- Financial ServicesDocument10 pagesFinancial ServicesDinesh Sugumaran100% (4)

- Dynacon Systems Ar 2017 5323650317Document101 pagesDynacon Systems Ar 2017 5323650317murali_pmp1766No ratings yet

- Affidavit Adequate Assurance of Due Performance Ameriquest MortgageDocument5 pagesAffidavit Adequate Assurance of Due Performance Ameriquest MortgageBernie Jones100% (2)

- Corporate FinanceDocument10 pagesCorporate FinancePuteri Nelissa MilaniNo ratings yet

- Optional Riders Provide Critical Illness and Disability CoverageDocument2 pagesOptional Riders Provide Critical Illness and Disability Coverageemaraty khNo ratings yet

- Medical BillDocument27 pagesMedical BillSagarNo ratings yet

- Register Free: Syllabus Revision 20% Guaranteed Score Doubt Solving NasaDocument16 pagesRegister Free: Syllabus Revision 20% Guaranteed Score Doubt Solving NasaKavita SinghNo ratings yet

- 3 - Cash Flow Statement - Indirect Method - QuestionsDocument3 pages3 - Cash Flow Statement - Indirect Method - Questionsmikheal beyber100% (1)

- Fin CH 2 ProblemsDocument9 pagesFin CH 2 Problemsshah118850% (4)

- IIBM Case Study AnswersDocument98 pagesIIBM Case Study AnswersAravind 9901366442 - 990278722422% (9)

- Does Capital Intensity, Inventory Intensity, Firm Size, Firm Risk, and Political Connections Affect Tax Aggressiveness?Document10 pagesDoes Capital Intensity, Inventory Intensity, Firm Size, Firm Risk, and Political Connections Affect Tax Aggressiveness?KurniaNo ratings yet

- HawkinsDocument1 pageHawkinsNatarajNo ratings yet

- Student Budget Worksheet: ExpensesDocument2 pagesStudent Budget Worksheet: ExpensesJo FopNo ratings yet

- Dax PDFDocument64 pagesDax PDFpiyushNo ratings yet

- Generic Ic Disc PresentationDocument55 pagesGeneric Ic Disc PresentationInternational Tax Magazine; David Greenberg PhD, MSA, EA, CPA; Tax Group International; 646-705-2910No ratings yet

- 2076 - Varias, Aizel Ann B - Module 1Document18 pages2076 - Varias, Aizel Ann B - Module 1Aizel Ann VariasNo ratings yet

- Virtual CFO Services for StartupsDocument15 pagesVirtual CFO Services for StartupsKarun GuptaNo ratings yet

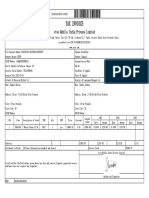

- Tax Invoice: Vivo Mobile India Private LimitedDocument1 pageTax Invoice: Vivo Mobile India Private LimitedRaghav SharmaNo ratings yet