You might also like

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

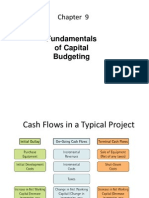

- Typical Cash Flows at The Start: Cost of Machines (200.000, Posses, So On Balance SheetDocument7 pagesTypical Cash Flows at The Start: Cost of Machines (200.000, Posses, So On Balance SheetSylvan EversNo ratings yet

- BEC Notes Chapter 3Document6 pagesBEC Notes Chapter 3cpacfa90% (10)

- Accounting and Finance Formulas: A Simple IntroductionFrom EverandAccounting and Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Solution Manual For Corporate Finance A Focused Approach 6th EditionDocument37 pagesSolution Manual For Corporate Finance A Focused Approach 6th Editionjanetgriffintizze100% (12)

- Incremental Operating Cash Flow CalculationDocument11 pagesIncremental Operating Cash Flow Calculationmehrab1807100% (1)

- (Lecture 3) - Inflation and Capital AllowanceDocument9 pages(Lecture 3) - Inflation and Capital AllowanceAjay Kumar TakiarNo ratings yet

- Tax Income, Sunk Cost and Opportunity Cost: Week 13Document46 pagesTax Income, Sunk Cost and Opportunity Cost: Week 13satryoyu811No ratings yet

- Chapter 5Document34 pagesChapter 5yayobnNo ratings yet

- Acctg FormulasDocument7 pagesAcctg FormulasAira Santos VibarNo ratings yet

- Class Notes: Class: XI Topic: Financial StatementDocument3 pagesClass Notes: Class: XI Topic: Financial StatementRajeev ShuklaNo ratings yet

- Interest: L PinDocument8 pagesInterest: L Pineka putri sri andrianiNo ratings yet

- Financial Concepts: Weighted Average Cost of Capital (WACC)Document6 pagesFinancial Concepts: Weighted Average Cost of Capital (WACC)koshaNo ratings yet

- Cheat Sheet - Financial STDocument2 pagesCheat Sheet - Financial STMohammad DaulehNo ratings yet

- Valuation: Aswath DamodaranDocument100 pagesValuation: Aswath DamodaranhsurampudiNo ratings yet

- Investment Appraisal Taxation, InflationDocument8 pagesInvestment Appraisal Taxation, InflationJiya RajputNo ratings yet

- Fundamentals of Capital Budgeting: FIN 2200 - Corporate Finance Dennis NGDocument31 pagesFundamentals of Capital Budgeting: FIN 2200 - Corporate Finance Dennis NGNyamandasimunyolaNo ratings yet

- LXL Gr12Acc 01 Cash-Flow-Statement 16apr2015Document9 pagesLXL Gr12Acc 01 Cash-Flow-Statement 16apr2015Nezer Byl P. VergaraNo ratings yet

- LXL Gr12Acc 01 Cash-Flow-Statement 16apr2015 PDFDocument9 pagesLXL Gr12Acc 01 Cash-Flow-Statement 16apr2015 PDFNezer Byl P. VergaraNo ratings yet

- Defining Free Cash Flow Top-Down ApproachDocument2 pagesDefining Free Cash Flow Top-Down Approachchuff6675100% (1)

- Free Basic Short Financial Accounting - 2f20dc43 314d 49bf A7e8 F398e2c49e3dDocument32 pagesFree Basic Short Financial Accounting - 2f20dc43 314d 49bf A7e8 F398e2c49e3dCareer and TechnologyNo ratings yet

- Income Statement Revenues - Expenses Net IncomeDocument4 pagesIncome Statement Revenues - Expenses Net IncomeTanishaq bindalNo ratings yet

- DCF in Depth Calculate The Revenue Growth Rate: Forecasting Free Cash FlowsDocument5 pagesDCF in Depth Calculate The Revenue Growth Rate: Forecasting Free Cash FlowsJustBNo ratings yet

- Chapter 2 Buiness FinanxceDocument38 pagesChapter 2 Buiness FinanxceShajeer HamNo ratings yet

- BDHCH 9Document37 pagesBDHCH 9tzsyxxwht100% (1)

- Chapter 3Document5 pagesChapter 3Hal kNo ratings yet

- Notes - An Introduction To Financ, Accouting, Modeling, and ValuationDocument8 pagesNotes - An Introduction To Financ, Accouting, Modeling, and ValuationperNo ratings yet

- DCF Valuation - Aswath DamodaranDocument60 pagesDCF Valuation - Aswath DamodaranUtkarshNo ratings yet

- Fundamentals of Capital BudgetingDocument54 pagesFundamentals of Capital BudgetingLee ChiaNo ratings yet

- Midterm Review - Key ConceptsDocument10 pagesMidterm Review - Key ConceptsGurpreetNo ratings yet

- Unit 4 Earnings Multiplier and EVADocument3 pagesUnit 4 Earnings Multiplier and EVAJaikishan FabyaniNo ratings yet

- Chapter 3 BecDocument11 pagesChapter 3 BecStephen ZhaoNo ratings yet

- Estimation of Project Cash FlowsDocument26 pagesEstimation of Project Cash Flowssupreet2912No ratings yet

- 25 Questions On DCF ValuationDocument4 pages25 Questions On DCF ValuationZain Ul AbidinNo ratings yet

- 02 - Basic Perf MeasuresDocument14 pages02 - Basic Perf MeasureshoalongkiemNo ratings yet

- Financial Statement Analysis For ValuationDocument5 pagesFinancial Statement Analysis For Valuationsanu sayedNo ratings yet

- Minimum Acceptable Rate of ReturnDocument17 pagesMinimum Acceptable Rate of ReturnRalph Galvez100% (1)

- Corporate Valuation: Principles and PracticesDocument12 pagesCorporate Valuation: Principles and PracticesvishalNo ratings yet

- MFM AantekeningenDocument27 pagesMFM AantekeningenabcdefNo ratings yet

- DCF Analysis Forecasting Free Cash FlowsDocument4 pagesDCF Analysis Forecasting Free Cash Flowshamrah1363No ratings yet

- Statement of CashflowsDocument2 pagesStatement of CashflowsLove IslamNo ratings yet

- Effect of Taxat-Wps OfficeDocument10 pagesEffect of Taxat-Wps OfficeZameer DalviNo ratings yet

- Document 26Document2 pagesDocument 26José GómezNo ratings yet

- Statement of Retained Earings and Its Components HandoutDocument12 pagesStatement of Retained Earings and Its Components HandoutRitesh LashkeryNo ratings yet

- Corporate TaxationDocument3 pagesCorporate TaxationRod AnthonyNo ratings yet

- Project Cashflow EstimationDocument11 pagesProject Cashflow EstimationKrishnapriya NairNo ratings yet

- Project Cashflow EstimationDocument11 pagesProject Cashflow EstimationKrishnapriya NairNo ratings yet

- F M S Investment Appraisal: Inancial AnagementDocument50 pagesF M S Investment Appraisal: Inancial AnagementsaadaltafNo ratings yet

- 9 Mas Capital Budgeting Sessions 3 4Document14 pages9 Mas Capital Budgeting Sessions 3 4seya dummyNo ratings yet

- Unit 4: Relative ValuationDocument47 pagesUnit 4: Relative ValuationMadhvendra BhardwajNo ratings yet

- Review SessionDocument25 pagesReview SessionK60 Bùi Phương AnhNo ratings yet

- Advanced Financial Accounting - II CH 1-4Document24 pagesAdvanced Financial Accounting - II CH 1-4TAKELE NEDESANo ratings yet

- Lecture Notes Section 5Document18 pagesLecture Notes Section 5Marc OurfaliNo ratings yet

- How To Calculate Markup PercentageDocument8 pagesHow To Calculate Markup PercentageGilbert AranaNo ratings yet

- FADM Cheat SheetDocument2 pagesFADM Cheat Sheetvarun022084No ratings yet

- International Tax: Dominican Republic Highlights 2019Document4 pagesInternational Tax: Dominican Republic Highlights 2019Juan Enrique GuilianiNo ratings yet

- Capbud CFDocument8 pagesCapbud CFVARUN MONGANo ratings yet

- FINALS - 1ST SEM TER 2021-2022: Valuation, Concepts and MethodsDocument6 pagesFINALS - 1ST SEM TER 2021-2022: Valuation, Concepts and MethodsJoanna MalubayNo ratings yet

- 3 - Income Statement-Without Correction of ExercisesDocument58 pages3 - Income Statement-Without Correction of ExercisesClaire YINo ratings yet

- Soal UAS Startup FinancingDocument6 pagesSoal UAS Startup FinancingNatasha Angelica SusantoNo ratings yet

- 2023 3 Decision Tree AnalysisDocument24 pages2023 3 Decision Tree AnalysisNatasha Angelica SusantoNo ratings yet

- 2023 2 Linear ProgrammingDocument26 pages2023 2 Linear ProgrammingNatasha Angelica SusantoNo ratings yet

- Chapter 4 - Part III NotesDocument1 pageChapter 4 - Part III NotesNatasha Angelica SusantoNo ratings yet