You might also like

- Essential Guide to Operations Management: Concepts and Case NotesFrom EverandEssential Guide to Operations Management: Concepts and Case NotesNo ratings yet

- B PR PracticesDocument24 pagesB PR PracticesAnonymous v6ybIxZFNo ratings yet

- Optimal Control and Optimization of Stochastic Supply Chain SystemsFrom EverandOptimal Control and Optimization of Stochastic Supply Chain SystemsNo ratings yet

- BPRpractices PDFDocument24 pagesBPRpractices PDFsucheta menonNo ratings yet

- An Engineering Approach To An Integrated Value Proposition Design Framework C. Van Der Merwe, A. Van Rensburg & C.S.L. SchutteDocument16 pagesAn Engineering Approach To An Integrated Value Proposition Design Framework C. Van Der Merwe, A. Van Rensburg & C.S.L. SchuttejNo ratings yet

- Maturity AssessmentDocument228 pagesMaturity AssessmentAli ZafarNo ratings yet

- Wang2004 A Methodology To Incorporate Life-CycleDocument9 pagesWang2004 A Methodology To Incorporate Life-Cyclemiguelip01No ratings yet

- Asset Life Cycle ManagementDocument16 pagesAsset Life Cycle ManagementJohan MoraNo ratings yet

- Jurnal WilayahDocument12 pagesJurnal WilayahDevi AgustinaNo ratings yet

- A Review and Evaluation of Circular Business Model Innovation ToolsDocument25 pagesA Review and Evaluation of Circular Business Model Innovation ToolsAlejoCarreraNo ratings yet

- Lean in QsDocument12 pagesLean in QsGimhan GodawatteNo ratings yet

- Design For Utility, Sustainability and Societal Virtues: Developing Product Service SystemsDocument8 pagesDesign For Utility, Sustainability and Societal Virtues: Developing Product Service SystemsEduardo DiestraNo ratings yet

- ScienceDirect SustainableBusinessDesignDocument6 pagesScienceDirect SustainableBusinessDesignTamas TurcsanNo ratings yet

- 7_Root Cause Failure Analysis r2Document11 pages7_Root Cause Failure Analysis r2Raimundo MartínezNo ratings yet

- NewssDocument13 pagesNewssDilaNo ratings yet

- Sustainability 14 07483 v3Document17 pagesSustainability 14 07483 v3Anass CHERRAFINo ratings yet

- Management Accounting and Control SystemDocument15 pagesManagement Accounting and Control Systemflorence bondayiNo ratings yet

- Asset Life Cycle ManagementDocument14 pagesAsset Life Cycle ManagementSheeba Mathew100% (1)

- Life Cycle Engineering: Horst KrasowskiDocument5 pagesLife Cycle Engineering: Horst KrasowskiSundar RathinarajNo ratings yet

- Analisis Del Impacto Politicas de ManttoDocument25 pagesAnalisis Del Impacto Politicas de ManttoAndres Acosta RozoNo ratings yet

- A Meta-Model For Analyzing The Influence of Production-Related Business ProcessesDocument6 pagesA Meta-Model For Analyzing The Influence of Production-Related Business ProcessesWisnu AjiNo ratings yet

- Sciencedirect: A Lean Assessment Tool Based On Systems DynamicsDocument6 pagesSciencedirect: A Lean Assessment Tool Based On Systems DynamicsHadi P.No ratings yet

- Enterprise Architecture Migration Planning Using The Matrix of ChangeDocument5 pagesEnterprise Architecture Migration Planning Using The Matrix of ChangeCecep FahmidinNo ratings yet

- A Lean Approach to Developing Sustainable Supply ChainsDocument33 pagesA Lean Approach to Developing Sustainable Supply Chainsdoddy ChannelNo ratings yet

- Schnetzler IMSDocument8 pagesSchnetzler IMSDipendra ShresthaNo ratings yet

- Hospital Operations Management: An Exploratory Study From Brazil and PortugalDocument10 pagesHospital Operations Management: An Exploratory Study From Brazil and PortugalQuality SaketNo ratings yet

- Sustainability Optimization in Manufacturing Enterprises 2015 Procedia CIRPDocument6 pagesSustainability Optimization in Manufacturing Enterprises 2015 Procedia CIRPMohd TariqNo ratings yet

- IJIMT article explores sustainable supply chain management performanceDocument6 pagesIJIMT article explores sustainable supply chain management performanceparsadNo ratings yet

- Industrial EngineeringDocument6 pagesIndustrial EngineeringJaveria AfzalNo ratings yet

- Sustainability in Performance Measurement and Management Systems For Supply ChainsDocument6 pagesSustainability in Performance Measurement and Management Systems For Supply ChainsMuhammad AliNo ratings yet

- Circular manufacturing literature reviewDocument32 pagesCircular manufacturing literature reviewRabia HassanNo ratings yet

- Governance in The Engineering ContextDocument2 pagesGovernance in The Engineering Contextasim5595No ratings yet

- A Study On Total Quality Management and Lean ManufDocument13 pagesA Study On Total Quality Management and Lean ManufJada CameronNo ratings yet

- Current Issues and Challenges of Supply Chain ManagementDocument6 pagesCurrent Issues and Challenges of Supply Chain ManagementmohsinziaNo ratings yet

- Aggregate Planning and SCM SustainabilityDocument10 pagesAggregate Planning and SCM SustainabilityGouri PNo ratings yet

- Barrier Analysis Producto Service System Usig Interpretive Structural ModelDocument11 pagesBarrier Analysis Producto Service System Usig Interpretive Structural ModelalexandergomezmNo ratings yet

- Ijmrem C013016031 PDFDocument16 pagesIjmrem C013016031 PDFijmremNo ratings yet

- A Study On Total Quality Management and Lean Manufacturing: Through Lean Thinking ApproachDocument12 pagesA Study On Total Quality Management and Lean Manufacturing: Through Lean Thinking Approachhusam-h2252No ratings yet

- A Study On Total Quality Management and Lean Manufacturing: Through Lean Thinking ApproachDocument12 pagesA Study On Total Quality Management and Lean Manufacturing: Through Lean Thinking ApproachDian AndriliaNo ratings yet

- Cost Accounting: Term PaperDocument16 pagesCost Accounting: Term Papervinay_gandhi_2No ratings yet

- Lean Maintenance RoadmapDocument11 pagesLean Maintenance Roadmapreynancs0% (1)

- 1 s2.0 S2212567115001495 MainDocument9 pages1 s2.0 S2212567115001495 MainNicole Louise RiveraNo ratings yet

- Business Process ReengineeringDocument19 pagesBusiness Process ReengineeringErwiin SweenNo ratings yet

- BPR MethodologiesDocument29 pagesBPR MethodologiesOsamah S. Alshaya100% (1)

- Strategic Cost Management and Performance: The Case of Environmental CostsDocument15 pagesStrategic Cost Management and Performance: The Case of Environmental Costsrishu jainNo ratings yet

- How To Foster Sustainable Continuous Improvement A Ca - 2019 - Operations ReseaDocument12 pagesHow To Foster Sustainable Continuous Improvement A Ca - 2019 - Operations ReseaEtetu AbeshaNo ratings yet

- Historical Analysis of Performance Measurement and Management in Operations ManagementDocument13 pagesHistorical Analysis of Performance Measurement and Management in Operations ManagementfanasimNo ratings yet

- Inisiasi 01 MIS in OrganizationDocument7 pagesInisiasi 01 MIS in OrganizationHidayatullah GanieNo ratings yet

- Identification and Prioritization Lean Six Sigma Barriers in MsmesDocument9 pagesIdentification and Prioritization Lean Six Sigma Barriers in MsmesShad AlertNo ratings yet

- Key Performance Indicators On Waste Minimization: A Literature ReviewDocument14 pagesKey Performance Indicators On Waste Minimization: A Literature ReviewdhanarajNo ratings yet

- Engineering Economics GuideDocument6 pagesEngineering Economics Guideabubakar chohaanNo ratings yet

- Activity-Based Costing (ABC) - An Effective Tool For Better ManagementDocument9 pagesActivity-Based Costing (ABC) - An Effective Tool For Better ManagementErica CallosNo ratings yet

- 787-Article Text-4132-6514-10-20190526Document14 pages787-Article Text-4132-6514-10-20190526Bradz TalpoNo ratings yet

- Sustainable Circular Business Model For Transparency and Uncertainty Reduction in Supply Chain ManagementDocument17 pagesSustainable Circular Business Model For Transparency and Uncertainty Reduction in Supply Chain ManagementKetki ChuriNo ratings yet

- Maintenance Management FrameworkDocument12 pagesMaintenance Management FrameworkMauro MLR100% (1)

- Acta Technica NapocensisDocument10 pagesActa Technica NapocensisLakatos SiminaNo ratings yet

- Modeling Concepts For Internal Controls in Business Processes - An Empirically Grounded Extension of BPMNDocument18 pagesModeling Concepts For Internal Controls in Business Processes - An Empirically Grounded Extension of BPMNLilianna KekalihNo ratings yet

- What Is Operation Research? 2.what Is Production Management? 3.what Is The Difference Between Operation Research and Operational Research?Document6 pagesWhat Is Operation Research? 2.what Is Production Management? 3.what Is The Difference Between Operation Research and Operational Research?Justin ReyesNo ratings yet

- Sciencedirect: 26Th Cirp Design ConferenceDocument6 pagesSciencedirect: 26Th Cirp Design ConferenceAbdul Aziz Khan AfridiNo ratings yet

- Articulo Lean Thinking en InglesDocument10 pagesArticulo Lean Thinking en InglesAntonella ParentiniNo ratings yet

- 12-Article Text-27-1-10-20191224Document5 pages12-Article Text-27-1-10-20191224TobNo ratings yet

- 05 00944tdsDocument1 page05 00944tdsTobNo ratings yet

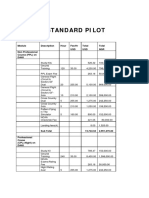

- Fee For Standard Pilot Course: Description Hour Fee/Hr Total Total USD USD NGR Non Professional Course (PPL) On DA40Document3 pagesFee For Standard Pilot Course: Description Hour Fee/Hr Total Total USD USD NGR Non Professional Course (PPL) On DA40TobNo ratings yet

- 01 Mcar Part-1 and IS v2.10Document103 pages01 Mcar Part-1 and IS v2.10TobNo ratings yet

- MalayoDocument39 pagesMalayoRoxanne Datuin UsonNo ratings yet

- Cookery 10Document5 pagesCookery 10Angelica CunananNo ratings yet

- Artificial Intelligence in Practice How 50 Successful CompaniesDocument6 pagesArtificial Intelligence in Practice How 50 Successful CompaniesKaran TawareNo ratings yet

- Videoteca - Daniel Haddad (March 2019)Document8 pagesVideoteca - Daniel Haddad (March 2019)Daniel HaddadNo ratings yet

- Theatre History ProjectDocument5 pagesTheatre History Projectapi-433889391No ratings yet

- Summative Test in MAPEH 10 1st and 2nd QuarterDocument16 pagesSummative Test in MAPEH 10 1st and 2nd QuarterMeljim ReyesNo ratings yet

- 47 Syeda Nida Batool Zaidi-1Document10 pages47 Syeda Nida Batool Zaidi-1Eiman ShahzadNo ratings yet

- Micro-Finance: 16 Principles of Grameen BankDocument5 pagesMicro-Finance: 16 Principles of Grameen BankHomiyar TalatiNo ratings yet

- Question 1 - Adjusting EntriesDocument10 pagesQuestion 1 - Adjusting EntriesVyish VyishuNo ratings yet

- StanadyneDocument1 pageStanadyneJunior IungNo ratings yet

- Experiment No. 2. Frequency Shift Keying (FSK) and Digital CommunicationsDocument15 pagesExperiment No. 2. Frequency Shift Keying (FSK) and Digital CommunicationsAmir Mahmood RehmaniNo ratings yet

- QuestionnaireDocument15 pagesQuestionnaireNaveen GunasekaranNo ratings yet

- Explosive Ordnance Disposal & Canine Group Regional Explosive Ordnance Disposal and Canine Unit 3Document1 pageExplosive Ordnance Disposal & Canine Group Regional Explosive Ordnance Disposal and Canine Unit 3regional eodk9 unit3No ratings yet

- Essay 2Document13 pagesEssay 2Monarch ParmarNo ratings yet

- Operon NotesDocument3 pagesOperon NotesanithagsNo ratings yet

- Summative Test 1 English 9 Q1Document2 pagesSummative Test 1 English 9 Q1Katherine Anne Munar0% (1)

- Speidel, M. O. (1981) - Stress Corrosion Cracking of Stainless Steels in NaCl Solutions.Document11 pagesSpeidel, M. O. (1981) - Stress Corrosion Cracking of Stainless Steels in NaCl Solutions.oozdemirNo ratings yet

- Calculating parameters for a basic modern transistor amplifierDocument189 pagesCalculating parameters for a basic modern transistor amplifierionioni2000No ratings yet

- Tugas B.INGGRIS ALANDocument4 pagesTugas B.INGGRIS ALANAlan GunawanNo ratings yet

- Quality Management and Control in ConstructionDocument22 pagesQuality Management and Control in ConstructionjennyNo ratings yet

- Nelson Olmos introduces himself and familyDocument4 pagesNelson Olmos introduces himself and familyNelson Olmos QuimbayoNo ratings yet

- BRI Divisions and Branches Level ReportDocument177 pagesBRI Divisions and Branches Level ReportCalvin Watulingas100% (1)

- 5S and Visual Control PresentationDocument56 pages5S and Visual Control Presentationarmando.bastosNo ratings yet

- Supercritical CO2 Extraction: A Clean Extraction MethodDocument6 pagesSupercritical CO2 Extraction: A Clean Extraction MethodPrincess Janine CatralNo ratings yet

- Food Safety Culture Webinar SLIDESDocument46 pagesFood Safety Culture Webinar SLIDESAto Kwamena PaintsilNo ratings yet

- Carding: Click To Edit Master Subtitle Style by M. Naveed AkhtarDocument35 pagesCarding: Click To Edit Master Subtitle Style by M. Naveed Akhtarshazliarsahd50% (2)

- God Hates Us All AlbumDocument3 pagesGod Hates Us All AlbumDannyNo ratings yet

- Icon-Architects Executive Profile - For HealthcareDocument14 pagesIcon-Architects Executive Profile - For HealthcareMuhammad Noshad RizviNo ratings yet

- 07 - Toshkov (2016) Theory in The Research ProcessDocument29 pages07 - Toshkov (2016) Theory in The Research ProcessFerlanda LunaNo ratings yet

- 333 Sapugay v. CADocument3 pages333 Sapugay v. CAJoshua Ejeil PascualNo ratings yet

- Working Backwards: Insights, Stories, and Secrets from Inside AmazonFrom EverandWorking Backwards: Insights, Stories, and Secrets from Inside AmazonRating: 4.5 out of 5 stars4.5/5 (14)

- The Goal: A Process of Ongoing Improvement - 30th Aniversary EditionFrom EverandThe Goal: A Process of Ongoing Improvement - 30th Aniversary EditionRating: 4 out of 5 stars4/5 (684)

- PMP Exam Prep: How to pass the PMP Exam on your First Attempt – Learn Faster, Retain More and Pass the PMP ExamFrom EverandPMP Exam Prep: How to pass the PMP Exam on your First Attempt – Learn Faster, Retain More and Pass the PMP ExamRating: 4.5 out of 5 stars4.5/5 (3)

- Self-Discipline: The Ultimate Guide To Beat Procrastination, Achieve Your Goals, and Get What You Want In Your LifeFrom EverandSelf-Discipline: The Ultimate Guide To Beat Procrastination, Achieve Your Goals, and Get What You Want In Your LifeRating: 4.5 out of 5 stars4.5/5 (662)

- The Machine That Changed the World: The Story of Lean Production-- Toyota's Secret Weapon in the Global Car Wars That Is Now Revolutionizing World IndustryFrom EverandThe Machine That Changed the World: The Story of Lean Production-- Toyota's Secret Weapon in the Global Car Wars That Is Now Revolutionizing World IndustryRating: 4.5 out of 5 stars4.5/5 (40)

- Project Planning and SchedulingFrom EverandProject Planning and SchedulingRating: 5 out of 5 stars5/5 (6)

- Process!: How Discipline and Consistency Will Set You and Your Business FreeFrom EverandProcess!: How Discipline and Consistency Will Set You and Your Business FreeRating: 4.5 out of 5 stars4.5/5 (5)

- Working Backwards: Insights, Stories, and Secrets from Inside AmazonFrom EverandWorking Backwards: Insights, Stories, and Secrets from Inside AmazonRating: 4.5 out of 5 stars4.5/5 (44)

- The Supply Chain Revolution: Innovative Sourcing and Logistics for a Fiercely Competitive WorldFrom EverandThe Supply Chain Revolution: Innovative Sourcing and Logistics for a Fiercely Competitive WorldRating: 4 out of 5 stars4/5 (32)

- Kaizen: The Step-by-Step Guide to Success. Adopt a Winning Mindset and Learn Effective Strategies to Productivity Improvement.From EverandKaizen: The Step-by-Step Guide to Success. Adopt a Winning Mindset and Learn Effective Strategies to Productivity Improvement.No ratings yet

- The Red Pill Executive: Transform Operations and Unlock the Potential of Corporate CultureFrom EverandThe Red Pill Executive: Transform Operations and Unlock the Potential of Corporate CultureNo ratings yet

- The Supply Chain Revolution: Innovative Sourcing and Logistics for a Fiercely Competitive WorldFrom EverandThe Supply Chain Revolution: Innovative Sourcing and Logistics for a Fiercely Competitive WorldNo ratings yet

- The Influential Product Manager: How to Lead and Launch Successful Technology ProductsFrom EverandThe Influential Product Manager: How to Lead and Launch Successful Technology ProductsRating: 5 out of 5 stars5/5 (2)

- The Influential Product Manager: How to Lead and Launch Successful Technology ProductsFrom EverandThe Influential Product Manager: How to Lead and Launch Successful Technology ProductsRating: 4.5 out of 5 stars4.5/5 (11)

- Leading Product Development: The Senior Manager's Guide to Creating and ShapingFrom EverandLeading Product Development: The Senior Manager's Guide to Creating and ShapingRating: 5 out of 5 stars5/5 (1)

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItFrom EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItRating: 5 out of 5 stars5/5 (13)

- Execution (Review and Analysis of Bossidy and Charan's Book)From EverandExecution (Review and Analysis of Bossidy and Charan's Book)No ratings yet

- Vibration Basics and Machine Reliability Simplified : A Practical Guide to Vibration AnalysisFrom EverandVibration Basics and Machine Reliability Simplified : A Practical Guide to Vibration AnalysisRating: 4 out of 5 stars4/5 (2)

- Results, Not Reports: Building Exceptional Organizations by Integrating Process, Performance, and PeopleFrom EverandResults, Not Reports: Building Exceptional Organizations by Integrating Process, Performance, and PeopleNo ratings yet