You might also like

- 2020 Q1 Vietnam Quarterly Knowledge Report Industrial Market PDFDocument9 pages2020 Q1 Vietnam Quarterly Knowledge Report Industrial Market PDFLinh MaiNo ratings yet

- Manual de Generadores de Gas SolarDocument49 pagesManual de Generadores de Gas SolarJuvenal Segundo Chavez Acosta100% (7)

- SPAIN Trade Investment Statistical Country NoteDocument10 pagesSPAIN Trade Investment Statistical Country Notelockleong93No ratings yet

- HUNGARY Trade Investment Statistical Country NoteDocument10 pagesHUNGARY Trade Investment Statistical Country NoteDI EGOOOLNo ratings yet

- FDI in Figures April 2021Document12 pagesFDI in Figures April 2021un627331No ratings yet

- Inbound TourismDocument44 pagesInbound Tourismarchit chopraNo ratings yet

- Norway's Economic Profile in 2020Document3 pagesNorway's Economic Profile in 2020ClaudiaNo ratings yet

- FDI Impact on Zimbabwe's Trade BalanceDocument7 pagesFDI Impact on Zimbabwe's Trade BalanceRodwellNo ratings yet

- Wto 2.2Document6 pagesWto 2.2Carol DanversNo ratings yet

- Mgt-201 Assignment International Trade, Trends in World Trade and Overview of India'S TradeDocument21 pagesMgt-201 Assignment International Trade, Trends in World Trade and Overview of India'S TradeGable kaura L-2020 -A-16-BIVNo ratings yet

- JapanDocument4 pagesJapanMaria BuereNo ratings yet

- Leadstar's Macroeconomics Chapter Explains Ethiopia's Economic GrowthDocument24 pagesLeadstar's Macroeconomics Chapter Explains Ethiopia's Economic Growthabey.mulugetaNo ratings yet

- Ditcinf2021d2 enDocument8 pagesDitcinf2021d2 enseafishNo ratings yet

- NESG Manufacturing Policy Brief May 2021Document11 pagesNESG Manufacturing Policy Brief May 2021uchenna joel iconNo ratings yet

- Indonesia Economic Challenges: Raden PardedeDocument38 pagesIndonesia Economic Challenges: Raden PardedeFEBRIZANo ratings yet

- GPIP Green Industrial ParksDocument26 pagesGPIP Green Industrial ParksAlex LiuNo ratings yet

- Monthly Economic Bulletin: January 2011Document15 pagesMonthly Economic Bulletin: January 2011lrochekellyNo ratings yet

- Macroeconomic Analysis For DenmarkDocument8 pagesMacroeconomic Analysis For DenmarkBozinoskaSNo ratings yet

- Individual Problem SET 1Document6 pagesIndividual Problem SET 1Bùi Hoài NhânNo ratings yet

- Pengajar Fakultas Ekonomi Dan Bisnis Universitas Indonesia Fithra FaisalDocument14 pagesPengajar Fakultas Ekonomi Dan Bisnis Universitas Indonesia Fithra FaisalPradiptaAdiPamungkasNo ratings yet

- Pengajar Fakultas Ekonomi Dan Bisnis Universitas Indonesia Fithra FaisalDocument14 pagesPengajar Fakultas Ekonomi Dan Bisnis Universitas Indonesia Fithra FaisalPradiptaAdiPamungkasNo ratings yet

- Global Trade: UpdateDocument8 pagesGlobal Trade: UpdatesanzitNo ratings yet

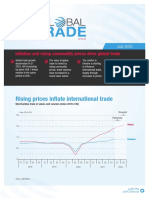

- Rising prices drive global trade values higherDocument11 pagesRising prices drive global trade values higherBekele Guta GemeneNo ratings yet

- General Profile ArubaDocument3 pagesGeneral Profile ArubacayspepeNo ratings yet

- KH 2016 June Investing in Cambodia PDFDocument40 pagesKH 2016 June Investing in Cambodia PDFToan LuongkimNo ratings yet

- Coronavirus (COVID-19) - Economic Impact in IndiaDocument74 pagesCoronavirus (COVID-19) - Economic Impact in IndiaSarvagya GopalNo ratings yet

- Vietnam Economic Update PPT August10Document10 pagesVietnam Economic Update PPT August10chirag ghoshNo ratings yet

- FDI in Tunisia Presentation .Document27 pagesFDI in Tunisia Presentation .Mohamed AboubakrNo ratings yet

- Lucintel: Publisher SampleDocument12 pagesLucintel: Publisher SampleIshna RamosNo ratings yet

- Israel 1Document20 pagesIsrael 1Swati VermaNo ratings yet

- Thailand InvestmentDocument8 pagesThailand Investmentempty87No ratings yet

- Ch4 AES2022Document5 pagesCh4 AES2022Thanh Nguyễn XuânNo ratings yet

- Uzbekistan's Economic Growth and Fiscal Adjustment PathsDocument6 pagesUzbekistan's Economic Growth and Fiscal Adjustment PathsUmidjon MuydinovNo ratings yet

- 2009-08-06 Saxo Bank Research Note - US Q2 GDPDocument8 pages2009-08-06 Saxo Bank Research Note - US Q2 GDPTrading Floor100% (2)

- URUGUAY Trade Competitiveness DiagnosticDocument80 pagesURUGUAY Trade Competitiveness DiagnosticMary RodchenkoNo ratings yet

- Co So Thuc TienDocument3 pagesCo So Thuc TienLan Tô NgọcNo ratings yet

- Situation Analysis and Current Issues of Sri Lankan Economy With Special Emphasis On Fiscal and Debt IssuesDocument34 pagesSituation Analysis and Current Issues of Sri Lankan Economy With Special Emphasis On Fiscal and Debt IssuesuserabhishekNo ratings yet

- Session 16 To 18 International Linkages - Extensions of IS-LM in The Context of International Mobility of GoodsDocument38 pagesSession 16 To 18 International Linkages - Extensions of IS-LM in The Context of International Mobility of GoodsprernaNo ratings yet

- Session 16 To 18 International Linkages - Extensions of IS-LM in The Context of International Mobility of Goods (Fixed Price)Document70 pagesSession 16 To 18 International Linkages - Extensions of IS-LM in The Context of International Mobility of Goods (Fixed Price)prernaNo ratings yet

- Session 16 To 18 International Linkages - Extensions of is-LM in The Context of International Mobility of GoodsDocument61 pagesSession 16 To 18 International Linkages - Extensions of is-LM in The Context of International Mobility of GoodsKartik Kumar PGP 2022-24 BatchNo ratings yet

- General Profile: Tanzania, United Republic ofDocument3 pagesGeneral Profile: Tanzania, United Republic ofPasco NkololoNo ratings yet

- Indian Export Impact on GDPDocument6 pagesIndian Export Impact on GDPSameer ShekharNo ratings yet

- Resilient Economy: Average Economic Decade Wise 2001 - 2010 4.81 %Document2 pagesResilient Economy: Average Economic Decade Wise 2001 - 2010 4.81 %Varshil DesaiNo ratings yet

- 2020 Q2 Knowledge Report DanangDocument11 pages2020 Q2 Knowledge Report DanangLinh HuynhNo ratings yet

- Colombia: Growth Performance, Inequality and Environment Indicators: ColombiaDocument4 pagesColombia: Growth Performance, Inequality and Environment Indicators: ColombiaFelipe MoraNo ratings yet

- Prezentare Ionut DumitruDocument28 pagesPrezentare Ionut DumitruAnonymous c3IPK8No ratings yet

- General Profile AfganistanDocument3 pagesGeneral Profile AfganistancayspepeNo ratings yet

- Canada's Trading PresentationDocument62 pagesCanada's Trading Presentationnxb2pv5scmNo ratings yet

- Bangladesh Trade Profile 2020Document2 pagesBangladesh Trade Profile 2020Rizal KhalidNo ratings yet

- Mankiw8e-Chap06 21 22Document58 pagesMankiw8e-Chap06 21 22Liliane IsabelNo ratings yet

- Ec 038Document4 pagesEc 038suman subediNo ratings yet

- Presentation - India's Relations With SAARC, ASEAN & The EUDocument30 pagesPresentation - India's Relations With SAARC, ASEAN & The EUMeha Lodha100% (3)

- Union Budget 2022: #ConfidentindiaDocument31 pagesUnion Budget 2022: #ConfidentindiaRavi AgarwalNo ratings yet

- Africa Day Presentation VDefDocument30 pagesAfrica Day Presentation VDefBernard BiboumNo ratings yet

- Lucintel: Publisher SampleDocument12 pagesLucintel: Publisher SampleSHARMA TECHNo ratings yet

- Alas John Paul Facon Raul Augustus Macrobite1Document3 pagesAlas John Paul Facon Raul Augustus Macrobite1Raul Augustus D. FACONNo ratings yet

- Q1 - 2023 24 Investor PresentationDocument27 pagesQ1 - 2023 24 Investor PresentationashwinsadvayofficialNo ratings yet

- General Profile AngolaDocument3 pagesGeneral Profile AngolacayspepeNo ratings yet

- 25 Inflation Rate: Exports, Imports and Trade BalanceDocument4 pages25 Inflation Rate: Exports, Imports and Trade BalanceKenjin SaiNo ratings yet

- Reading Lesson 7Document5 pagesReading Lesson 7AnshumanNo ratings yet

- Economic Indicators for East Asia: Input–Output TablesFrom EverandEconomic Indicators for East Asia: Input–Output TablesNo ratings yet

- Cled Case AnalysisDocument2 pagesCled Case AnalysisJake QuakeNo ratings yet

- 92229765297Document2 pages92229765297Jake QuakeNo ratings yet

- General Ledger and Trial Balance - Go Labada-1Document2 pagesGeneral Ledger and Trial Balance - Go Labada-1Jake QuakeNo ratings yet

- Greece Trade and Investment Factsheet 2023-02-17Document17 pagesGreece Trade and Investment Factsheet 2023-02-17Jake QuakeNo ratings yet

- SD WanDocument32 pagesSD WanAbdalrawoof AlsherifNo ratings yet

- What Is Automation: Delegation of Human Control Functions To Technical Equipment Aimed Towards AchievingDocument26 pagesWhat Is Automation: Delegation of Human Control Functions To Technical Equipment Aimed Towards AchievingVeeraperumal ArumugamNo ratings yet

- PreviewpdfDocument32 pagesPreviewpdfAleena HarisNo ratings yet

- Hershey's Milk Shake ProjectDocument20 pagesHershey's Milk Shake ProjectSarvesh MundhadaNo ratings yet

- NBC 2019 - AE Div B - Part 9 PDFDocument62 pagesNBC 2019 - AE Div B - Part 9 PDFviksursNo ratings yet

- Professional GoalsDocument2 pagesProfessional Goalsapi-530115287No ratings yet

- Differential RAID: Rethinking RAID For SSD ReliabilityDocument5 pagesDifferential RAID: Rethinking RAID For SSD ReliabilityRabiul SikderNo ratings yet

- 4x7.1x8.5 Box CulvertDocument1,133 pages4x7.1x8.5 Box CulvertRudra SharmaNo ratings yet

- AMUL TASTE OF INDIADocument39 pagesAMUL TASTE OF INDIAprathamesh kaduNo ratings yet

- 2 Quarter Examination in Tle 8 (Electrical Installation and Maintenance)Document3 pages2 Quarter Examination in Tle 8 (Electrical Installation and Maintenance)jameswisdom javier100% (4)

- Assignment Two: Dennis Wanyoike DIT-035-0022/2009 2/7/2010Document8 pagesAssignment Two: Dennis Wanyoike DIT-035-0022/2009 2/7/2010Dennis WanyoikeNo ratings yet

- Nestle Announcement It Is Pulling The Plug On Eldred TownshipDocument2 pagesNestle Announcement It Is Pulling The Plug On Eldred TownshipDickNo ratings yet

- Compile C/C++ in Atom editorDocument2 pagesCompile C/C++ in Atom editorNishant KeswaniNo ratings yet

- Orientation and TrainingDocument31 pagesOrientation and TrainingSyurga FathonahNo ratings yet

- CvSU Differential Equations SyllabusDocument6 pagesCvSU Differential Equations SyllabusAbegail Jean TangaraNo ratings yet

- Ch. 1 Getting Started W - JavaDocument14 pagesCh. 1 Getting Started W - JavathateggoNo ratings yet

- 04 IPHS Primary Health CentreDocument20 pages04 IPHS Primary Health CentreKailash NagarNo ratings yet

- Prog GuideDocument29 pagesProg GuideOmar L'fataNo ratings yet

- MP Lab04 - LCD PDFDocument11 pagesMP Lab04 - LCD PDFSobia ShakeelNo ratings yet

- ICE Export Catalog 2011Document72 pagesICE Export Catalog 2011Thien BinhNo ratings yet

- Sdoc 09 13 SiDocument70 pagesSdoc 09 13 SiJhojo Tesiorna FalcutilaNo ratings yet

- "GrabCut" - Interactive Foreground Extraction Using Iterated Graph CutsDocument6 pages"GrabCut" - Interactive Foreground Extraction Using Iterated Graph CutsdiegomfagundesNo ratings yet

- Opportunities For Enhanced Lean Construction Management Using Internet of Things StandardsDocument12 pagesOpportunities For Enhanced Lean Construction Management Using Internet of Things StandardsBrahian Roman CabreraNo ratings yet

- String & Math FunctionsDocument38 pagesString & Math FunctionsThanu shreeNo ratings yet

- 22172/pune Humsafar Third Ac (3A)Document2 pages22172/pune Humsafar Third Ac (3A)VISHAL SARSWATNo ratings yet

- 23NM60ND STMicroelectronicsDocument12 pages23NM60ND STMicroelectronicskeisinhoNo ratings yet

- Insurance As A Investment Tool at Icici Bank Project Report Mba FinanceDocument73 pagesInsurance As A Investment Tool at Icici Bank Project Report Mba FinanceBabasab Patil (Karrisatte)No ratings yet

- Valencia v. Sandiganbayan DIGESTDocument2 pagesValencia v. Sandiganbayan DIGESTkathrynmaydevezaNo ratings yet

- ICAP Pakistan Final Exams Business Finance Decisions RecommendationsDocument4 pagesICAP Pakistan Final Exams Business Finance Decisions RecommendationsImran AhmadNo ratings yet