You might also like

- Economic Indicators for East Asia: Input–Output TablesFrom EverandEconomic Indicators for East Asia: Input–Output TablesNo ratings yet

- Greece Trade Investment Statistical Country NoteDocument10 pagesGreece Trade Investment Statistical Country NoteJake QuakeNo ratings yet

- HUNGARY Trade Investment Statistical Country NoteDocument10 pagesHUNGARY Trade Investment Statistical Country NoteDI EGOOOLNo ratings yet

- FDI in Figures April 2021Document12 pagesFDI in Figures April 2021un627331No ratings yet

- IACFM Presentations Feb 2020 PDFDocument51 pagesIACFM Presentations Feb 2020 PDFZack StraussNo ratings yet

- Resilient Economy: Average Economic Decade Wise 2001 - 2010 4.81 %Document2 pagesResilient Economy: Average Economic Decade Wise 2001 - 2010 4.81 %Varshil DesaiNo ratings yet

- Israel 1Document20 pagesIsrael 1Swati VermaNo ratings yet

- Mgt-201 Assignment International Trade, Trends in World Trade and Overview of India'S TradeDocument21 pagesMgt-201 Assignment International Trade, Trends in World Trade and Overview of India'S TradeGable kaura L-2020 -A-16-BIVNo ratings yet

- Ditcinf2021d2 enDocument8 pagesDitcinf2021d2 enseafishNo ratings yet

- 2009-08-06 Saxo Bank Research Note - US Q2 GDPDocument8 pages2009-08-06 Saxo Bank Research Note - US Q2 GDPTrading Floor100% (2)

- GPIP Green Industrial ParksDocument26 pagesGPIP Green Industrial ParksAlex LiuNo ratings yet

- 2020 Q1 Vietnam Quarterly Knowledge Report Industrial Market PDFDocument9 pages2020 Q1 Vietnam Quarterly Knowledge Report Industrial Market PDFLinh MaiNo ratings yet

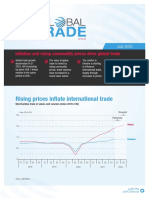

- Rising prices drive global trade values higherDocument11 pagesRising prices drive global trade values higherBekele Guta GemeneNo ratings yet

- CBRE VN - ILS Quarterly Market Update (June 20)Document52 pagesCBRE VN - ILS Quarterly Market Update (June 20)Galih AnggoroNo ratings yet

- JapanDocument4 pagesJapanMaria BuereNo ratings yet

- KH 2016 June Investing in Cambodia PDFDocument40 pagesKH 2016 June Investing in Cambodia PDFToan LuongkimNo ratings yet

- Monthly Economic Bulletin: January 2011Document15 pagesMonthly Economic Bulletin: January 2011lrochekellyNo ratings yet

- The Indian Media & Entertainment Industry 2019: Trends & Analysis - Past, Present & FutureDocument63 pagesThe Indian Media & Entertainment Industry 2019: Trends & Analysis - Past, Present & FutureSharvari ShankarNo ratings yet

- Uzbekistan's Economic Growth and Fiscal Adjustment PathsDocument6 pagesUzbekistan's Economic Growth and Fiscal Adjustment PathsUmidjon MuydinovNo ratings yet

- Alas John Paul Facon Raul Augustus Macrobite1Document3 pagesAlas John Paul Facon Raul Augustus Macrobite1Raul Augustus D. FACONNo ratings yet

- Africa Day Presentation VDefDocument30 pagesAfrica Day Presentation VDefBernard BiboumNo ratings yet

- Industry Growth OutlookDocument1 pageIndustry Growth OutlookPalo Alto SoftwareNo ratings yet

- Bridgewater ReportDocument12 pagesBridgewater Reportw_fibNo ratings yet

- 68 32 Presentasi Perusahaan Fy 2020 Indicative ResultsDocument47 pages68 32 Presentasi Perusahaan Fy 2020 Indicative ResultsIvanNo ratings yet

- The Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureDocument56 pagesThe Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureAnkit TiwariNo ratings yet

- Global Trade: UpdateDocument8 pagesGlobal Trade: UpdatesanzitNo ratings yet

- Coronavirus (COVID-19) - Economic Impact in IndiaDocument74 pagesCoronavirus (COVID-19) - Economic Impact in IndiaSarvagya GopalNo ratings yet

- Compiled Economic Survey English 2019/20Document256 pagesCompiled Economic Survey English 2019/20Hanu ManNo ratings yet

- Pengajar Fakultas Ekonomi Dan Bisnis Universitas Indonesia Fithra FaisalDocument14 pagesPengajar Fakultas Ekonomi Dan Bisnis Universitas Indonesia Fithra FaisalPradiptaAdiPamungkasNo ratings yet

- Pengajar Fakultas Ekonomi Dan Bisnis Universitas Indonesia Fithra FaisalDocument14 pagesPengajar Fakultas Ekonomi Dan Bisnis Universitas Indonesia Fithra FaisalPradiptaAdiPamungkasNo ratings yet

- FDI Impact on Zimbabwe's Trade BalanceDocument7 pagesFDI Impact on Zimbabwe's Trade BalanceRodwellNo ratings yet

- Economic Survey PresentationDocument27 pagesEconomic Survey PresentationcoolkurllaNo ratings yet

- Low Minimum Asset Management Fund Offers Guaranteed Monthly ReturnsDocument5 pagesLow Minimum Asset Management Fund Offers Guaranteed Monthly ReturnsAleksandar DendaNo ratings yet

- Wto 2.2Document6 pagesWto 2.2Carol DanversNo ratings yet

- DRC Tax Revenues Fall Below African AverageDocument2 pagesDRC Tax Revenues Fall Below African AverageDawitNo ratings yet

- CH 04-05-06 Performance AnalysisDocument26 pagesCH 04-05-06 Performance Analysis2021-108960No ratings yet

- 1Q2020 Fullbook enDocument53 pages1Q2020 Fullbook enVincentNo ratings yet

- Solid, Stable and Consistent: BOC Hong Kong (Holdings) LimitedDocument4 pagesSolid, Stable and Consistent: BOC Hong Kong (Holdings) LimitedRalph SuarezNo ratings yet

- 1.are There Productivity Spillovers From Foreign Direct Investment in ChinaDocument34 pages1.are There Productivity Spillovers From Foreign Direct Investment in ChinaAzan RasheedNo ratings yet

- Inbound TourismDocument44 pagesInbound Tourismarchit chopraNo ratings yet

- Thailand InvestmentDocument8 pagesThailand Investmentempty87No ratings yet

- FinalDocument16 pagesFinalUsama malikNo ratings yet

- Equity and Poverty - Global - POVEQ - MYSDocument2 pagesEquity and Poverty - Global - POVEQ - MYSal fatehNo ratings yet

- OECD Report Highlights Low Debt and Fiscal Surpluses in SwitzerlandDocument4 pagesOECD Report Highlights Low Debt and Fiscal Surpluses in SwitzerlandJason del PonteNo ratings yet

- Prezentare Ionut DumitruDocument28 pagesPrezentare Ionut DumitruAnonymous c3IPK8No ratings yet

- Trade Balance of BD in 2018Document11 pagesTrade Balance of BD in 2018shawonNo ratings yet

- FPTS Outlook 2022 No04 KeepFaithDocument16 pagesFPTS Outlook 2022 No04 KeepFaithLinh TRAN Thi AnhNo ratings yet

- INE Monthly Economic Survey July 2021 enDocument14 pagesINE Monthly Economic Survey July 2021 enCatarina SantosNo ratings yet

- Zalando SE - CMD 2021 - Financial Deep DiveDocument16 pagesZalando SE - CMD 2021 - Financial Deep DivehaoNo ratings yet

- The Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureDocument56 pagesThe Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureAnkit TiwariNo ratings yet

- Free Template - BCG MatrixDocument10 pagesFree Template - BCG MatrixEva LianNo ratings yet

- Yardstick Educational Initiatives (FZE) : Information Checklist and Tracker Last Updated On: 11/30/2021Document8 pagesYardstick Educational Initiatives (FZE) : Information Checklist and Tracker Last Updated On: 11/30/2021Dishant KhanejaNo ratings yet

- A1 - Part 1Document18 pagesA1 - Part 1An KhánhhNo ratings yet

- Fin 4150 Week 8 LecturesDocument46 pagesFin 4150 Week 8 LecturesEric McLaughlinNo ratings yet

- Accenture Strategy Digital Disruption Growth Multiplier BrazilDocument12 pagesAccenture Strategy Digital Disruption Growth Multiplier Brazilali fatehiNo ratings yet

- Q1 - 2023 24 Investor PresentationDocument27 pagesQ1 - 2023 24 Investor PresentationashwinsadvayofficialNo ratings yet

- Mckinsey Presentation On Managing The DownturnDocument16 pagesMckinsey Presentation On Managing The DownturnRehan FariasNo ratings yet

- Radico Khaitan Ltd. Earnings Presentation: Q4 and Full Year FY2020Document23 pagesRadico Khaitan Ltd. Earnings Presentation: Q4 and Full Year FY2020UmangNo ratings yet

- It Sector ReportDocument25 pagesIt Sector ReportAryan BhageriaNo ratings yet

- NESG Manufacturing Policy Brief May 2021Document11 pagesNESG Manufacturing Policy Brief May 2021uchenna joel iconNo ratings yet

- US Covered Up Deadly Air Strikes in Syria, New York Times Reports - BBC NewsDocument7 pagesUS Covered Up Deadly Air Strikes in Syria, New York Times Reports - BBC Newslockleong93No ratings yet

- What Are Negative Externalities of ProductionDocument1 pageWhat Are Negative Externalities of Productionlockleong93No ratings yet

- Barriers To Entry - TypesDocument6 pagesBarriers To Entry - Typeslockleong93No ratings yet

- COP26 - Coal Pledge in COP A Huge Step Forward - UN Climate Boss - BBC NewsDocument18 pagesCOP26 - Coal Pledge in COP A Huge Step Forward - UN Climate Boss - BBC Newslockleong93No ratings yet

- Delta Boss Says Climate Change Means Flying Will Cost More - BBC NewsDocument11 pagesDelta Boss Says Climate Change Means Flying Will Cost More - BBC Newslockleong93No ratings yet

- Ship-Load of 'Toxic' Chinese Fertilizer Causes Diplomatic Stink - BBC NewsDocument10 pagesShip-Load of 'Toxic' Chinese Fertilizer Causes Diplomatic Stink - BBC Newslockleong93No ratings yet

- Japan's Former Princess Mako Leaves For New York After Giving Up Title - BBC NewsDocument7 pagesJapan's Former Princess Mako Leaves For New York After Giving Up Title - BBC Newslockleong93No ratings yet

- What The 'Joker Attack' Revealed About Japanese Society - BBC NewsDocument9 pagesWhat The 'Joker Attack' Revealed About Japanese Society - BBC Newslockleong93No ratings yet

- Danny Fenster - Myanmar Court Gives US Journalist 11 Years Jail - BBC NewsDocument8 pagesDanny Fenster - Myanmar Court Gives US Journalist 11 Years Jail - BBC Newslockleong93No ratings yet

- Covid Vaccine Waning Immunity' - How Worried Should I Be - BBC NewsDocument9 pagesCovid Vaccine Waning Immunity' - How Worried Should I Be - BBC Newslockleong93No ratings yet

- COP26 - China and India Must Explain Themselves, Says Sharma - BBC NewsDocument9 pagesCOP26 - China and India Must Explain Themselves, Says Sharma - BBC Newslockleong93No ratings yet

- Belarus Migrants - EU Accuses Lukashenko of Gangster-Style Abuse - BBC NewsDocument10 pagesBelarus Migrants - EU Accuses Lukashenko of Gangster-Style Abuse - BBC Newslockleong93No ratings yet

- China's Xi Jinping Cements His Status With Historic Resolution - BBC NewsDocument8 pagesChina's Xi Jinping Cements His Status With Historic Resolution - BBC Newslockleong93No ratings yet

- Wilbur Smith - Popular Zambian-Born Author Dies Aged 88 - BBC NewsDocument7 pagesWilbur Smith - Popular Zambian-Born Author Dies Aged 88 - BBC Newslockleong93No ratings yet

- COP26 - Climate Talks Into Overtime As Nations Grasp For Deal - BBC NewsDocument16 pagesCOP26 - Climate Talks Into Overtime As Nations Grasp For Deal - BBC Newslockleong93No ratings yet

- COP26 - Temperature Fears As Climate Summit Enters Final Day - BBC NewsDocument7 pagesCOP26 - Temperature Fears As Climate Summit Enters Final Day - BBC Newslockleong93No ratings yet

- Steve Bannon Charged With Contempt of Congress - BBC NewsDocument10 pagesSteve Bannon Charged With Contempt of Congress - BBC Newslockleong93No ratings yet

- California Couple Sue Clinic For Alleged IVF Swap 'Horror' - BBC NewsDocument7 pagesCalifornia Couple Sue Clinic For Alleged IVF Swap 'Horror' - BBC Newslockleong93No ratings yet

- Number of Migrants Crossing Channel To UK Hits New Daily Record - BBC NewsDocument7 pagesNumber of Migrants Crossing Channel To UK Hits New Daily Record - BBC Newslockleong93No ratings yet

- Capitol Riot - Court Temporarily Blocks Release of Trump Files - BBC NewsDocument7 pagesCapitol Riot - Court Temporarily Blocks Release of Trump Files - BBC Newslockleong93No ratings yet

- Climate Change - Human Activity Makes Forests Emit Carbon - BBC NewsDocument9 pagesClimate Change - Human Activity Makes Forests Emit Carbon - BBC Newslockleong93No ratings yet

- COP26 Accused of 'Massive Credibility, Action and Commitment Gap' in New Report - BBC NewsDocument19 pagesCOP26 Accused of 'Massive Credibility, Action and Commitment Gap' in New Report - BBC Newslockleong93No ratings yet

- Belarus Threatens To Cut Off Gas To EU in Border Row - BBC NewsDocument9 pagesBelarus Threatens To Cut Off Gas To EU in Border Row - BBC Newslockleong93No ratings yet

- Covid - Austrians Heading Towards Lockdown For Unvaccinated - BBC NewsDocument7 pagesCovid - Austrians Heading Towards Lockdown For Unvaccinated - BBC Newslockleong93No ratings yet

- Zhang Zhan - US Asks China To Free Jailed Wuhan Citizen Journalist - BBC NewsDocument6 pagesZhang Zhan - US Asks China To Free Jailed Wuhan Citizen Journalist - BBC Newslockleong93No ratings yet

- High-Risk Covid Gene More Common in South Asians - BBC NewsDocument7 pagesHigh-Risk Covid Gene More Common in South Asians - BBC Newslockleong93No ratings yet

- Climate Change - Human Activity Makes Forests Emit Carbon - BBC NewsDocument9 pagesClimate Change - Human Activity Makes Forests Emit Carbon - BBC Newslockleong93No ratings yet

- COP26 - PM Warned Over Aid Cuts Ahead of Climate Summit - BBC NewsDocument7 pagesCOP26 - PM Warned Over Aid Cuts Ahead of Climate Summit - BBC Newslockleong93No ratings yet

- Nagaenthran - Family Prays For Miracle To Halt Execution of Man With Low IQ - BBC NewsDocument11 pagesNagaenthran - Family Prays For Miracle To Halt Execution of Man With Low IQ - BBC Newslockleong93No ratings yet

- CEO Secrets - Rich Lesser of BCG Shares His Advice - BBC NewsDocument9 pagesCEO Secrets - Rich Lesser of BCG Shares His Advice - BBC Newslockleong93No ratings yet

- National Investment Promotional Strategy LaunchedDocument40 pagesNational Investment Promotional Strategy LaunchedFrancis ChikombolaNo ratings yet

- EC 307 Summer Flexi Tutorial 1 - SolutionsDocument6 pagesEC 307 Summer Flexi Tutorial 1 - SolutionsR and R wweNo ratings yet

- The Impact of Banks and Stock Market Development On Economic Growth in South Africa - An ARDL-bounds Testing ApproachDocument17 pagesThe Impact of Banks and Stock Market Development On Economic Growth in South Africa - An ARDL-bounds Testing ApproachNokuthulaNo ratings yet

- Ver2 Updated Vision @2047 IIPADocument79 pagesVer2 Updated Vision @2047 IIPAAbhishek Biswal100% (1)

- Kdem-Usa Road Show - It-Ites GCC BPMDocument40 pagesKdem-Usa Road Show - It-Ites GCC BPMabhimanyu_2927No ratings yet

- Understanding Innovation Policymakers in Vietnam GIPA Scoping StudyDocument31 pagesUnderstanding Innovation Policymakers in Vietnam GIPA Scoping StudyChrist KimNo ratings yet

- ECON 102 Midterm1 SampleDocument5 pagesECON 102 Midterm1 SampleexamkillerNo ratings yet

- ECON1102 Macroeconomics ConceptsDocument4 pagesECON1102 Macroeconomics ConceptsDikshit KashyapNo ratings yet

- 9 - ESCAP PPP Readiness Tool PDFDocument12 pages9 - ESCAP PPP Readiness Tool PDFJulan CastroNo ratings yet

- Traffic Loading & Volume 2022.2023 v1 FinalDocument55 pagesTraffic Loading & Volume 2022.2023 v1 Finalkibiralew DestaNo ratings yet

- Foreign AidDocument3 pagesForeign AidAmna KashifNo ratings yet

- Individual Assignment PAD390Document5 pagesIndividual Assignment PAD390izatul294No ratings yet

- Project Report On KFC PDFDocument60 pagesProject Report On KFC PDFNiraj Vishwakarma100% (1)

- Historical Trends in Savings and Investment in PakistanDocument22 pagesHistorical Trends in Savings and Investment in PakistanAsad BumbiaNo ratings yet

- DP Report 2021 Vol 1 For UploadDocument312 pagesDP Report 2021 Vol 1 For UploadSrushti SatputeNo ratings yet

- Economy Notes 14 Chapters on Key Economic ConceptsDocument85 pagesEconomy Notes 14 Chapters on Key Economic ConceptsvishalNo ratings yet

- PNB MetLife Annual Report 2018-19 - tcm47-69490 PDFDocument191 pagesPNB MetLife Annual Report 2018-19 - tcm47-69490 PDFshuklaNo ratings yet

- The Role of Nutrition and Genetics As Key Determinants of The Positive Height TrendDocument20 pagesThe Role of Nutrition and Genetics As Key Determinants of The Positive Height TrendfakeaccountNo ratings yet

- Boosting investment and SME growth through 2013 BudgetDocument17 pagesBoosting investment and SME growth through 2013 BudgetgombakluangNo ratings yet

- National Income ConceptsDocument15 pagesNational Income Conceptsrinky_trivediNo ratings yet

- 2017 Dec HomefurniDocument12 pages2017 Dec HomefurniAstra CloeNo ratings yet

- Ethiopia Agriculture Seminar Focuses on Role, Policy and Small FarmingDocument16 pagesEthiopia Agriculture Seminar Focuses on Role, Policy and Small FarmingEalshady HoneyBee Work ForceNo ratings yet

- Economic Survey 2020-21 Volume 2Document20 pagesEconomic Survey 2020-21 Volume 2Pallavi JNo ratings yet

- Parallel EconomyDocument8 pagesParallel EconomyAnith GhoshNo ratings yet

- Social Forces 2006 Robison 2009 26Document18 pagesSocial Forces 2006 Robison 2009 26Agne CepinskyteNo ratings yet

- CityAM2011 03 10bookDocument28 pagesCityAM2011 03 10bookCity A.M.No ratings yet

- 英文2021年数字经济报告(en)Document238 pages英文2021年数字经济报告(en)黑氆氇No ratings yet

- Indonesian Embassy in Brussels MagazineDocument30 pagesIndonesian Embassy in Brussels MagazineheruwahyuNo ratings yet

- MCD 2090 Tutorial Questions T5-Wk5Document10 pagesMCD 2090 Tutorial Questions T5-Wk5Leona AriesintaNo ratings yet

- The Third Wave of The Indonesia Family Life Survey (IFLS3) - Strauss Et Al 2000Document88 pagesThe Third Wave of The Indonesia Family Life Survey (IFLS3) - Strauss Et Al 2000dharendraNo ratings yet