You might also like

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- Latest Updates in GST - NovDocument6 pagesLatest Updates in GST - NovVishwanath HollaNo ratings yet

- Goods and Services Tax (GST) Filing Made Easy: Free Software Literacy SeriesFrom EverandGoods and Services Tax (GST) Filing Made Easy: Free Software Literacy SeriesNo ratings yet

- 37 Meeting of The GST Council, Goa 20 September, 2019 Press ReleaseDocument2 pages37 Meeting of The GST Council, Goa 20 September, 2019 Press ReleasePranay SaxenaNo ratings yet

- 37th GST Council Meet Final Press Release GSTPW 20092019Document2 pages37th GST Council Meet Final Press Release GSTPW 20092019AVASTNo ratings yet

- 37th GSTC Meeting - 02Document2 pages37th GSTC Meeting - 02Sahil ShahNo ratings yet

- Cbic Notifies Effective Date For Amendments Under GST Law Made Vide Finance Act 2021 and 2023Document6 pagesCbic Notifies Effective Date For Amendments Under GST Law Made Vide Finance Act 2021 and 2023PradeepkumarNo ratings yet

- Corrigendum 76-2018Document2 pagesCorrigendum 76-2018SivaNo ratings yet

- Hc-Allows-Errros in ITC Availment in Tax Head - Rectification-Of-Gstr-3b-After-Expiry-Of-Statutory-Time-LimitDocument3 pagesHc-Allows-Errros in ITC Availment in Tax Head - Rectification-Of-Gstr-3b-After-Expiry-Of-Statutory-Time-LimitychichghareNo ratings yet

- Overview of GSTDocument74 pagesOverview of GSTsunil patelNo ratings yet

- Cbic Taxes IndiaDocument2 pagesCbic Taxes IndiaReal PlayerNo ratings yet

- Circumstances Which Require ITC Reversal - Taxguru - inDocument3 pagesCircumstances Which Require ITC Reversal - Taxguru - inKaran MNo ratings yet

- Latest Updates in GSTDocument6 pagesLatest Updates in GSTprathNo ratings yet

- Paper-18 Supplementary 180221Document109 pagesPaper-18 Supplementary 180221Srihari SrinivasNo ratings yet

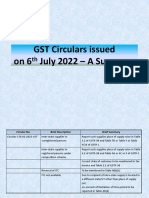

- GST Circulars Issued On 6th July - A SummaryDocument8 pagesGST Circulars Issued On 6th July - A SummaryVijaya ChandNo ratings yet

- Refund in GSTDocument6 pagesRefund in GSTNilesh SoniNo ratings yet

- Press Release 52 GST CouncilDocument6 pagesPress Release 52 GST CouncilCA Thirumalesu ENo ratings yet

- Day 6 & 7Document23 pagesDay 6 & 7PrasanthNo ratings yet

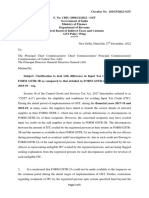

- Circular CGST 197Document5 pagesCircular CGST 197Jaipur-B Gr-2No ratings yet

- Mandatory ISD Provsions - Research PaperDocument3 pagesMandatory ISD Provsions - Research PaperMaunik ParikhNo ratings yet

- Guidance Note-Claim of ITC As Per GSTR 2B - Taxguru - inDocument4 pagesGuidance Note-Claim of ITC As Per GSTR 2B - Taxguru - inpradeepkumarsnairNo ratings yet

- GST NewsletterDocument24 pagesGST NewsletterrkhariNo ratings yet

- GST Amendment SheetDocument31 pagesGST Amendment Sheet10poolcardNo ratings yet

- GST Recap 20.05.2023 To 26.05.2023Document3 pagesGST Recap 20.05.2023 To 26.05.2023blalsteel.pvtltdNo ratings yet

- Circular CGST 193Document4 pagesCircular CGST 193Jaipur-B Gr-2No ratings yet

- Recommendations of GST Council Related To Law &procedureDocument2 pagesRecommendations of GST Council Related To Law &procedurePunit AroraNo ratings yet

- EY Tax Alert: Executive SummaryDocument6 pagesEY Tax Alert: Executive SummaryAjay SinghNo ratings yet

- Circular CGST 123Document4 pagesCircular CGST 123AKSHATANo ratings yet

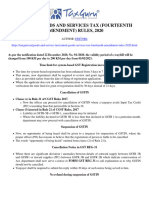

- Central Goods and Services Tax (Fourteenth Amendment) Rules, 2020 - Taxguru - inDocument9 pagesCentral Goods and Services Tax (Fourteenth Amendment) Rules, 2020 - Taxguru - inwaqtkeebaatein12No ratings yet

- Document 1Document2 pagesDocument 1gstceraslmNo ratings yet

- Cir 174 06 2022 CGSTDocument5 pagesCir 174 06 2022 CGSTNM JHANWAR & ASSOCIATESNo ratings yet

- GST LatestAmendments Issues 01072023Document85 pagesGST LatestAmendments Issues 01072023Selvakumar MuthurajNo ratings yet

- Circulars/Notifications: Legal UpdateDocument6 pagesCirculars/Notifications: Legal UpdateAnupam BaliNo ratings yet

- Do You Know GST - July 2022Document17 pagesDo You Know GST - July 2022CA Ranjan MehtaNo ratings yet

- GST UpdatesDocument10 pagesGST Updatesswati.gargchdNo ratings yet

- Taxmann's Analysis - Rule 37A - Navigating Through The Intricacies and GSTN AdvisoryDocument10 pagesTaxmann's Analysis - Rule 37A - Navigating Through The Intricacies and GSTN AdvisoryThouseefNo ratings yet

- Optotax Newletter - March - 2021Document6 pagesOptotax Newletter - March - 2021Atmiya DasNo ratings yet

- Judicial Rulings BY ABHAY DESAIDocument27 pagesJudicial Rulings BY ABHAY DESAIPiyush PatelNo ratings yet

- Faqs On Banking, Insurance and Stock Brokers CbicDocument34 pagesFaqs On Banking, Insurance and Stock Brokers CbicVenkataramana NippaniNo ratings yet

- Indirect Tax Laws 1Document10 pagesIndirect Tax Laws 1GunjanNo ratings yet

- Organised By:: National Conference On GSTDocument19 pagesOrganised By:: National Conference On GSTSunil ShahNo ratings yet

- Aino Communique 111th Edition Jan 2023 PDFDocument14 pagesAino Communique 111th Edition Jan 2023 PDFSwathi JainNo ratings yet

- Highlights of 47th GST Council Meeting - Taxguru - inDocument2 pagesHighlights of 47th GST Council Meeting - Taxguru - inBharath ChootyNo ratings yet

- 61397cajournal Oct2020 28Document4 pages61397cajournal Oct2020 28Anupam BaliNo ratings yet

- Cir 183 15 2022 CGSTDocument5 pagesCir 183 15 2022 CGSTAmritesh RaiNo ratings yet

- Page 1 of 4Document4 pagesPage 1 of 4Sunil ShahNo ratings yet

- AAR - ITC On Capital Goods in Case of Taxable + Exepmt SupplyDocument3 pagesAAR - ITC On Capital Goods in Case of Taxable + Exepmt SupplyJigar MakwanaNo ratings yet

- Comparative Analysis Under GST RegimeDocument5 pagesComparative Analysis Under GST RegimeAmita SinwarNo ratings yet

- Qrmp-Scheme NovDocument2 pagesQrmp-Scheme NovVishwanath HollaNo ratings yet

- Annexure To Form GST Drc-07: 21AAVCS9861M1ZF S.N.S. Industrial Works Private LimitedDocument5 pagesAnnexure To Form GST Drc-07: 21AAVCS9861M1ZF S.N.S. Industrial Works Private LimitedBiswajit MishraNo ratings yet

- Do You Know GST I March 2021 I Ranjan MehtaDocument15 pagesDo You Know GST I March 2021 I Ranjan MehtaCA Ranjan MehtaNo ratings yet

- GST Amendments For June 22 Students by CA Vivek GabaDocument6 pagesGST Amendments For June 22 Students by CA Vivek GabayashNo ratings yet

- GST TDS Applicability QuerryDocument5 pagesGST TDS Applicability QuerryVarun ThukralNo ratings yet

- Bos 56805Document26 pagesBos 56805smartshivenduNo ratings yet

- Tax Connect: Knowledge PartnerDocument15 pagesTax Connect: Knowledge PartnerJosef AnthonyNo ratings yet

- GST 49th Council Meeting 200223Document3 pagesGST 49th Council Meeting 200223Divay PranavNo ratings yet

- Reverse Charge MechanismDocument3 pagesReverse Charge MechanismjaipalmeNo ratings yet

- Summary of Notififcation Dated 26.12.2022Document3 pagesSummary of Notififcation Dated 26.12.2022Akshat MehariaNo ratings yet

- Input Tax Credit: Cma Bibhudatta SarangiDocument3 pagesInput Tax Credit: Cma Bibhudatta SarangihanumanthaiahgowdaNo ratings yet

- Effective GST Changes W.E.F. October 01 2023Document9 pagesEffective GST Changes W.E.F. October 01 2023ravitop2006No ratings yet

- Suggested Answer - Syl12 - June2017 - Paper - 12 Intermediate ExaminationDocument16 pagesSuggested Answer - Syl12 - June2017 - Paper - 12 Intermediate ExaminationDevendra AryaNo ratings yet

- Dormant CompanyDocument6 pagesDormant CompanyDevendra AryaNo ratings yet

- 2.1 Fiscal FunctionsDocument40 pages2.1 Fiscal FunctionsDevendra AryaNo ratings yet

- Striking Off and RestorationDocument9 pagesStriking Off and RestorationDevendra AryaNo ratings yet

- Flowering PlantsDocument7 pagesFlowering PlantsDevendra AryaNo ratings yet

- BiologyDocument23 pagesBiologyDevendra AryaNo ratings yet

- ReproductionDocument80 pagesReproductionDevendra AryaNo ratings yet

- English ClassNotesDocument2 pagesEnglish ClassNotesDevendra AryaNo ratings yet

- Time Allowed: 3 Hours Maximum Mark: 100: Executive ProgrammeDocument18 pagesTime Allowed: 3 Hours Maximum Mark: 100: Executive ProgrammeDevendra AryaNo ratings yet

- Soga Unit 1Document11 pagesSoga Unit 1Devendra AryaNo ratings yet

- Barang Publik: Muhammad Hasyim Ibnu Abbas, S.E.,M.ScDocument15 pagesBarang Publik: Muhammad Hasyim Ibnu Abbas, S.E.,M.ScIsmi AndariNo ratings yet

- Eco Project Chapter 5Document2 pagesEco Project Chapter 5Sanket KumarNo ratings yet

- Ignouassignments - in 9891268050: Assignment OneDocument25 pagesIgnouassignments - in 9891268050: Assignment OneAjay KumarNo ratings yet

- TQM Presentation 1Document17 pagesTQM Presentation 1ammarkhalilNo ratings yet

- Lesson 4 Written Assignment: Every Question)Document8 pagesLesson 4 Written Assignment: Every Question)Uyên Phương Phạm0% (1)

- Crossing of Cheques BankingDocument12 pagesCrossing of Cheques BankingTANAYA KETKARNo ratings yet

- Press Release Aro Granite Industries Limited: Details of Instruments/facilities in Annexure-1Document4 pagesPress Release Aro Granite Industries Limited: Details of Instruments/facilities in Annexure-1Ravi BabuNo ratings yet

- Excel Professional Services, Inc.: Management Firm of Professional Review and Training Center (PRTC)Document3 pagesExcel Professional Services, Inc.: Management Firm of Professional Review and Training Center (PRTC)Mae Angiela TansecoNo ratings yet

- Second Grading ExaminationDocument17 pagesSecond Grading ExaminationAmie Jane MirandaNo ratings yet

- Invoice Receipt: Inovice Number Invoice DateDocument1 pageInvoice Receipt: Inovice Number Invoice DateNazir AzNo ratings yet

- Af101 - Essay IntroductionDocument3 pagesAf101 - Essay IntroductionRosemary FremlinNo ratings yet

- PAC All CAF Mocks With Solutions Compiled by Saboor AhmadDocument128 pagesPAC All CAF Mocks With Solutions Compiled by Saboor AhmadOmair HasanNo ratings yet

- Puravankara AR 2020Document272 pagesPuravankara AR 2020anil1820No ratings yet

- Assignment 1 SCM - 19BBA10015Document3 pagesAssignment 1 SCM - 19BBA10015KartikNo ratings yet

- CTA 8239 (AR Realty) - Excess Input Tax Carry-OverDocument53 pagesCTA 8239 (AR Realty) - Excess Input Tax Carry-OverJerwin DaveNo ratings yet

- Demand Forecasting of Bajaj MotorcyclesDocument20 pagesDemand Forecasting of Bajaj MotorcyclesVipul ManglikNo ratings yet

- Final Accounts of Professionals - 2022-23Document12 pagesFinal Accounts of Professionals - 2022-23Ahishek PrasathNo ratings yet

- Tsinukal BezabihDocument190 pagesTsinukal BezabihSirgut TesfayeNo ratings yet

- Auction Notice Hyderabad Region 1062019 Uploading WebsiteDocument7 pagesAuction Notice Hyderabad Region 1062019 Uploading WebsiteRaviChowdaryNo ratings yet

- Law On Obligations AnswerDocument10 pagesLaw On Obligations AnswerMadduma, Jeromie G.No ratings yet

- First StudentDocument13 pagesFirst StudentWTVCNo ratings yet

- Quality ManagementDocument10 pagesQuality ManagementSweet Iris VillasanNo ratings yet

- Consumer Durable & Lifestyle Products Loan Application: A. PERSONAL DETAILS (Leave Space Between Two Words)Document6 pagesConsumer Durable & Lifestyle Products Loan Application: A. PERSONAL DETAILS (Leave Space Between Two Words)Rohit GuptaNo ratings yet

- GEN ED3 ReviewerDocument3 pagesGEN ED3 ReviewerRishel AlamaNo ratings yet

- Dooly Doughnuts Report Compressed 3Document11 pagesDooly Doughnuts Report Compressed 3Puja ChordiaNo ratings yet

- India Solar Handbook 2016 PDFDocument33 pagesIndia Solar Handbook 2016 PDFalkanm750No ratings yet

- Foreign Exchange Dealers' Association of India: 29th October 2020Document2 pagesForeign Exchange Dealers' Association of India: 29th October 2020Avnish KhuranaNo ratings yet

- Macrs Depreciation: New Smart Phone Calculation AnalysisDocument4 pagesMacrs Depreciation: New Smart Phone Calculation AnalysisErro Jaya RosadyNo ratings yet

- Contoh Format Anggaran BulananDocument1 pageContoh Format Anggaran BulananDedi SukmanaNo ratings yet

- Acct Statement - XX2691 - 26082023Document14 pagesAcct Statement - XX2691 - 26082023rahishsah93No ratings yet

- Money Made Easy: How to Budget, Pay Off Debt, and Save MoneyFrom EverandMoney Made Easy: How to Budget, Pay Off Debt, and Save MoneyRating: 5 out of 5 stars5/5 (1)

- The Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsFrom EverandThe Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsNo ratings yet

- Basic Python in Finance: How to Implement Financial Trading Strategies and Analysis using PythonFrom EverandBasic Python in Finance: How to Implement Financial Trading Strategies and Analysis using PythonRating: 5 out of 5 stars5/5 (9)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassFrom EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNo ratings yet

- The Best Team Wins: The New Science of High PerformanceFrom EverandThe Best Team Wins: The New Science of High PerformanceRating: 4.5 out of 5 stars4.5/5 (31)

- CAPITAL: Vol. 1-3: Complete Edition - Including The Communist Manifesto, Wage-Labour and Capital, & Wages, Price and ProfitFrom EverandCAPITAL: Vol. 1-3: Complete Edition - Including The Communist Manifesto, Wage-Labour and Capital, & Wages, Price and ProfitRating: 4 out of 5 stars4/5 (6)

- Swot analysis in 4 steps: How to use the SWOT matrix to make a difference in career and businessFrom EverandSwot analysis in 4 steps: How to use the SWOT matrix to make a difference in career and businessRating: 4.5 out of 5 stars4.5/5 (4)

- You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantFrom EverandYou Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantRating: 4 out of 5 stars4/5 (104)

- Radically Simple Accounting: A Way Out of the Dark and Into the ProfitFrom EverandRadically Simple Accounting: A Way Out of the Dark and Into the ProfitRating: 4.5 out of 5 stars4.5/5 (9)

- Budget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.From EverandBudget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.Rating: 5 out of 5 stars5/5 (91)

- The 30-Day Money Cleanse: Take Control of Your Finances, Manage Your Spending, and De-Stress Your Money for Good (Personal Finance and Budgeting Self-Help Book)From EverandThe 30-Day Money Cleanse: Take Control of Your Finances, Manage Your Spending, and De-Stress Your Money for Good (Personal Finance and Budgeting Self-Help Book)Rating: 3.5 out of 5 stars3.5/5 (9)

- How To Budget And Manage Your Money In 7 Simple StepsFrom EverandHow To Budget And Manage Your Money In 7 Simple StepsRating: 5 out of 5 stars5/5 (4)

- CDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsFrom EverandCDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsRating: 4 out of 5 stars4/5 (4)

- Minding Your Own Business: A Common Sense Guide to Home Management and IndustryFrom EverandMinding Your Own Business: A Common Sense Guide to Home Management and IndustryRating: 5 out of 5 stars5/5 (1)

- Debt Freedom: A Realistic Guide On How To Eliminate Debt, Including Credit Card Debt ForeverFrom EverandDebt Freedom: A Realistic Guide On How To Eliminate Debt, Including Credit Card Debt ForeverRating: 3 out of 5 stars3/5 (2)

- Personal Finance for Beginners - A Simple Guide to Take Control of Your Financial SituationFrom EverandPersonal Finance for Beginners - A Simple Guide to Take Control of Your Financial SituationRating: 4.5 out of 5 stars4.5/5 (18)

- Money Management: An Essential Guide on How to Get out of Debt and Start Building Financial Wealth, Including Budgeting and Investing Tips, Ways to Save and Frugal Living IdeasFrom EverandMoney Management: An Essential Guide on How to Get out of Debt and Start Building Financial Wealth, Including Budgeting and Investing Tips, Ways to Save and Frugal Living IdeasRating: 4 out of 5 stars4/5 (2)

- Rich Nurse Poor Nurses: The Critical Stuff Nursing School Forgot To Teach YouFrom EverandRich Nurse Poor Nurses: The Critical Stuff Nursing School Forgot To Teach YouRating: 4 out of 5 stars4/5 (2)

- Inflation Hacking: Inflation Investing Techniques to Benefit from High InflationFrom EverandInflation Hacking: Inflation Investing Techniques to Benefit from High InflationRating: 4.5 out of 5 stars4.5/5 (5)