You might also like

- What Is Securitization2Document14 pagesWhat Is Securitization2John Foster100% (2)

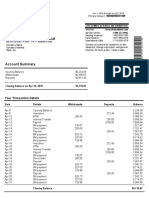

- Account Summary: Your Transaction DetailsDocument1 pageAccount Summary: Your Transaction Detailsdelfa100% (1)

- Features of SecuritizationDocument37 pagesFeatures of Securitizationhakec100% (2)

- International Certificate in WealthDocument388 pagesInternational Certificate in Wealthabhishek210585100% (2)

- Odyssey Private Equity Compensation Report 2023 Candidate Version 1Document42 pagesOdyssey Private Equity Compensation Report 2023 Candidate Version 1RMC123No ratings yet

- Chapter 7 - Fund ManagementDocument23 pagesChapter 7 - Fund ManagementJoiche Itallo Luna100% (2)

- PWC Cryptographic Assets and Related Transactions Accounting Considerations Under IfrsDocument23 pagesPWC Cryptographic Assets and Related Transactions Accounting Considerations Under IfrsJeanPNo ratings yet

- Crypto-Assets - The Global Regulatory PerspectiveDocument20 pagesCrypto-Assets - The Global Regulatory PerspectiveJeremy CorrenNo ratings yet

- Tugas AKMENBIS TM 10 Kel. 5Document4 pagesTugas AKMENBIS TM 10 Kel. 5Dimas Iqbal100% (1)

- Risk Management in BanksDocument107 pagesRisk Management in Bankssmaurya17100% (7)

- Cryptocurrencies and Anti Money Laundering - The Strategic PartnerDocument8 pagesCryptocurrencies and Anti Money Laundering - The Strategic PartnerThe Strategic PartnerNo ratings yet

- Personal Property Securities Act RA 11057Document77 pagesPersonal Property Securities Act RA 11057Ann QuirimitNo ratings yet

- Types of Bank AccountsDocument20 pagesTypes of Bank AccountsNisarg Khamar73% (11)

- Associated Insurance vs. IyaDocument1 pageAssociated Insurance vs. IyaJanlo FevidalNo ratings yet

- Comparative Study On E-Banking of HDFC &Document97 pagesComparative Study On E-Banking of HDFC &NehalNo ratings yet

- Cryptocurrency Held For Own AccountDocument3 pagesCryptocurrency Held For Own AccountKeat 98No ratings yet

- Chapter 21 Cryptocurrency Article (ACCA + IFRS Box)Document8 pagesChapter 21 Cryptocurrency Article (ACCA + IFRS Box)Kelvin Chu JYNo ratings yet

- CASEDocument5 pagesCASEM SameerNo ratings yet

- Accounting For Cryptocurrencies - ACCA Global SBR Exam ArticleDocument6 pagesAccounting For Cryptocurrencies - ACCA Global SBR Exam ArticleMichael DouglasNo ratings yet

- Crypto CurrencyDocument9 pagesCrypto CurrencyMD SAIFUL ISLAMNo ratings yet

- Philippine Interpretations Committee (Pic) Questions and Answers (Q&As)Document11 pagesPhilippine Interpretations Committee (Pic) Questions and Answers (Q&As)CasimirPampoNo ratings yet

- Ey Apply Ifrs Crypto Assets Update October2021Document35 pagesEy Apply Ifrs Crypto Assets Update October2021dab111No ratings yet

- f18 The Recording of Fungible Crypto Assets in Macroeconomic Statistics Background NoteDocument12 pagesf18 The Recording of Fungible Crypto Assets in Macroeconomic Statistics Background NoteRadu-Emil ŞendroiuNo ratings yet

- Accounting For Cryptocurrencies-Dec2016Document12 pagesAccounting For Cryptocurrencies-Dec2016Markie GrabilloNo ratings yet

- RG Introduction To Accounting For Cryptocurrencies May 2018Document24 pagesRG Introduction To Accounting For Cryptocurrencies May 2018Dwi Pamungkas UnggulNo ratings yet

- Perlakuan Akuntansi Atas CryptocurrencyDocument3 pagesPerlakuan Akuntansi Atas CryptocurrencyHerfiyanto WibawaNo ratings yet

- Treatment of Securitized Transactions in Bankruptcy: April 2001Document6 pagesTreatment of Securitized Transactions in Bankruptcy: April 2001Harpott GhantaNo ratings yet

- CRYPTOCURRENCYDocument40 pagesCRYPTOCURRENCYRadhika JaiswalNo ratings yet

- Property Law PSDA - 017 & 059Document6 pagesProperty Law PSDA - 017 & 059Brahm SareenNo ratings yet

- Mt2014 01 Virtual CurrencyDocument5 pagesMt2014 01 Virtual CurrencydinbitsNo ratings yet

- 1647114301financial Instrument - Part 1 (Classification Measurement)Document18 pages1647114301financial Instrument - Part 1 (Classification Measurement)mg21138No ratings yet

- Square Inc. Bitcoin Investment Whitepaper PDFDocument3 pagesSquare Inc. Bitcoin Investment Whitepaper PDFBen AdamteyNo ratings yet

- Accounting & Reporting of Cryptocurrencies: Anirudh Kar 4bcom If 1912705Document4 pagesAccounting & Reporting of Cryptocurrencies: Anirudh Kar 4bcom If 1912705Anirudh Kar 1912705No ratings yet

- IFRS Viewpoint: Accounting For Cryptocurrencies - The BasicsDocument12 pagesIFRS Viewpoint: Accounting For Cryptocurrencies - The BasicsWawa NajwaNo ratings yet

- Litepaper Bonded Sep 29Document13 pagesLitepaper Bonded Sep 29Optimuz OptimuzNo ratings yet

- Case 19-6 Classification of Cryptocurrency Holdings: All Rights ReservedDocument2 pagesCase 19-6 Classification of Cryptocurrency Holdings: All Rights ReservedbalonyNo ratings yet

- Anti-Money Laundering Regulation of Cryptocurrency: U.S. and Global ApproachesDocument14 pagesAnti-Money Laundering Regulation of Cryptocurrency: U.S. and Global ApproachesFiorella VásquezNo ratings yet

- Accounting and Taxation Framework For CryptocurrencyDocument21 pagesAccounting and Taxation Framework For CryptocurrencyBijay ShresthaNo ratings yet

- 3 Micro-Economic Foundations - 978-1-349-20175-4 - 3Document2 pages3 Micro-Economic Foundations - 978-1-349-20175-4 - 3Telmo CabetoNo ratings yet

- K4W WhitepaperDocument36 pagesK4W Whitepaperjoice.publiartNo ratings yet

- Cryptoassets: Accounting For An Emerging Asset Class: Latest ArticlesDocument9 pagesCryptoassets: Accounting For An Emerging Asset Class: Latest ArticlesOng Rii YeeNo ratings yet

- Chapter 21 Financial Instruments (Students)Document49 pagesChapter 21 Financial Instruments (Students)Kelvin Chu JYNo ratings yet

- RG Audit Considerations Related To Cryptocurrency July 2018Document33 pagesRG Audit Considerations Related To Cryptocurrency July 2018Farhan ShaikhNo ratings yet

- AAOIFI - Chapter-1 - Trading in CurrenciesDocument10 pagesAAOIFI - Chapter-1 - Trading in Currencieslegendery_pppNo ratings yet

- Industry Perspectives On Best Practices 1689569356Document29 pagesIndustry Perspectives On Best Practices 1689569356Ramiro Humberto Nova JaimesNo ratings yet

- 69256asb55316 As28Document62 pages69256asb55316 As28GybcNo ratings yet

- Clifford Chance - Distressed CryptoassetsDocument7 pagesClifford Chance - Distressed CryptoassetsAlexNo ratings yet

- A Warranty Is A Promise That A Particular Statement Made Is True at The Date of Contract. ADocument6 pagesA Warranty Is A Promise That A Particular Statement Made Is True at The Date of Contract. AAkshat MehariaNo ratings yet

- Ey Us Cryptocurrency Compliance and Controls Nov 2021Document12 pagesEy Us Cryptocurrency Compliance and Controls Nov 2021Artur MaryahovskyNo ratings yet

- Capital Markets Securities Lending Borrowing and Short Selling Regulations 2017Document7 pagesCapital Markets Securities Lending Borrowing and Short Selling Regulations 2017keithabubakar wangaNo ratings yet

- Article On Issuance of Digital Assets in NigeriaDocument4 pagesArticle On Issuance of Digital Assets in NigeriaNkume DecencyNo ratings yet

- Revised Anti (Updated)Document41 pagesRevised Anti (Updated)Marilyn OhoylanNo ratings yet

- R45 Derivative Markets and InstrumentsDocument24 pagesR45 Derivative Markets and InstrumentsSumair ChughtaiNo ratings yet

- 00 Auditing Crypto-Asset Sector CRCC-CanadaDocument6 pages00 Auditing Crypto-Asset Sector CRCC-CanadaBelen AlonsoNo ratings yet

- CPA Official Ifrs 9 AnsDocument2 pagesCPA Official Ifrs 9 AnsKambi OfficialNo ratings yet

- List of AcronymsDocument10 pagesList of AcronymsMd. Tauhidur Rahman 07-18-45No ratings yet

- Client-Agrement 1607614230105Document50 pagesClient-Agrement 1607614230105NITROIKNo ratings yet

- The Genesis of Cryptocurrency in IslamicDocument11 pagesThe Genesis of Cryptocurrency in IslamicMarco MallamaciNo ratings yet

- AAOIFI-Trading in Currencies Standard No.1Document10 pagesAAOIFI-Trading in Currencies Standard No.1Benett MomoryNo ratings yet

- The Philippines Cryptocurrency OverviewDocument8 pagesThe Philippines Cryptocurrency OverviewCLINT SHEEN CABIASNo ratings yet

- Frequently Asked Questions On Central Bank Digital CurrenciesDocument8 pagesFrequently Asked Questions On Central Bank Digital CurrenciesJOSEPH MARTINEZNo ratings yet

- Crypto-Trading - Supreme Court OrderDocument5 pagesCrypto-Trading - Supreme Court OrderMeghaNo ratings yet

- Membership AgreementDocument7 pagesMembership AgreementsemajamesNo ratings yet

- 1718 - Blockchain Issues For Interactive Entertainment Companies Article 0518Document4 pages1718 - Blockchain Issues For Interactive Entertainment Companies Article 0518Federico AldoNo ratings yet

- Few Acts Banking Regulation Act 1949 BR Act 1949Document13 pagesFew Acts Banking Regulation Act 1949 BR Act 1949Saurabh_K_Bagadi_280No ratings yet

- NSB-PGDM - (Em) - Batch-5 Term-3-2022-24-Blcg-Ppt-5-Law Relating To Negotiable Instruments ActDocument23 pagesNSB-PGDM - (Em) - Batch-5 Term-3-2022-24-Blcg-Ppt-5-Law Relating To Negotiable Instruments ActVij88888No ratings yet

- SummaryDocument4 pagesSummaryNatalie QalanziNo ratings yet

- Long-Term Assets Ii: Investments and IntangiblesDocument43 pagesLong-Term Assets Ii: Investments and IntangiblesGhita Tria MeitinaNo ratings yet

- Crypto Taxation in USA: A Comprehensive Guide to Navigating Digital Assets and TaxationFrom EverandCrypto Taxation in USA: A Comprehensive Guide to Navigating Digital Assets and TaxationNo ratings yet

- Concept of Commercial Banks of NepalDocument2 pagesConcept of Commercial Banks of Nepalvanvun100% (1)

- AE 17 M8 ExercisesDocument46 pagesAE 17 M8 ExercisesKim FloresNo ratings yet

- CARODocument9 pagesCAROSai Lakshmi PNo ratings yet

- FM303 Tutorial Question Week 5Document3 pagesFM303 Tutorial Question Week 5Smriti LalNo ratings yet

- Case Ratios and Financial Planning at EaDocument6 pagesCase Ratios and Financial Planning at EaAgus E. SetiyonoNo ratings yet

- List of Banks, HQS, Heads and Slogans 2016: Public Sector BankDocument2 pagesList of Banks, HQS, Heads and Slogans 2016: Public Sector BankANNENo ratings yet

- Class Work & Home Work Question of Final Account of Banking Conpany 22-23Document23 pagesClass Work & Home Work Question of Final Account of Banking Conpany 22-23DARK KING GamersNo ratings yet

- Survey Questionnaire For UPI PaymentsDocument3 pagesSurvey Questionnaire For UPI PaymentsArun GautamNo ratings yet

- Exercise 3: 1. Initial Capital Investments (Compound Entry) DR CRDocument4 pagesExercise 3: 1. Initial Capital Investments (Compound Entry) DR CRasdfNo ratings yet

- Doug Metcalf EulogyDocument8 pagesDoug Metcalf EulogyWilliam LawtonNo ratings yet

- Accounting 102 Assignment 10Document3 pagesAccounting 102 Assignment 10Cindy YinNo ratings yet

- Financial Markets & Institutions: Lecture Notes #3Document90 pagesFinancial Markets & Institutions: Lecture Notes #3Joan MaduNo ratings yet

- Insurance BusinessDocument23 pagesInsurance BusinessLetsah BrightNo ratings yet

- Auditing A Risk Based-Approach To Conducting A Quality Audit 10th Edition Johnstone Test Bank 1Document30 pagesAuditing A Risk Based-Approach To Conducting A Quality Audit 10th Edition Johnstone Test Bank 1patriciaNo ratings yet

- Notes of Brgy Pulabato .Document9 pagesNotes of Brgy Pulabato .Gier Rizaldo BulaclacNo ratings yet

- MA Dissertation Final-1Document102 pagesMA Dissertation Final-1Ciara PatelNo ratings yet

- Chapter 8 - Pas 1 Statement of Financial PositionDocument33 pagesChapter 8 - Pas 1 Statement of Financial PositionMarriel Fate CullanoNo ratings yet

- Chapter 2 Math For PracticeDocument3 pagesChapter 2 Math For Practiceehratul.bagNo ratings yet

- Prorata Pension DetailsDocument6 pagesProrata Pension Detailsshaunak_srNo ratings yet

- Revision Test 2 (Accounts) XIDocument3 pagesRevision Test 2 (Accounts) XIEshaan GroverNo ratings yet

- FFA Mock Exam AnswersDocument34 pagesFFA Mock Exam AnswersAnnas SaeedNo ratings yet