You might also like

- Commercial Invoice PDFDocument3 pagesCommercial Invoice PDFHerli Perez AltamiranoNo ratings yet

- Basics of Supply Chain ManagementDocument44 pagesBasics of Supply Chain ManagementBoroBethaMoneNo ratings yet

- Simplii Financial Cash Back Visa Card: Your Account at A GlanceDocument4 pagesSimplii Financial Cash Back Visa Card: Your Account at A Glanceclydenjshaw.caNo ratings yet

- Material Ledger ConfigurationDocument3 pagesMaterial Ledger ConfigurationMarcelo Del Canto RodriguezNo ratings yet

- Wecc1963brv1007 PDFDocument1 pageWecc1963brv1007 PDFAnonymous xcKm0DPZNo ratings yet

- Take Home AssignmentDocument2 pagesTake Home AssignmentPravanjan AumcapNo ratings yet

- New- Sheet 3 MPPGCL FinalDocument21 pagesNew- Sheet 3 MPPGCL Finalfilesend681No ratings yet

- Balance Sheet: StandaloneDocument9 pagesBalance Sheet: StandaloneKabita BuragohainNo ratings yet

- Nmims Narsee Monjee Solved Assignments 2Document10 pagesNmims Narsee Monjee Solved Assignments 2Yash MittalNo ratings yet

- Contoh IKAAADocument57 pagesContoh IKAAABintang LestariNo ratings yet

- 17.2. AP by Category (Jun 2023)Document1 page17.2. AP by Category (Jun 2023)susilo liloNo ratings yet

- External Image UrlDocument5 pagesExternal Image Urlrahul sharmaNo ratings yet

- Corporate Finance Profit and Loss AnalysisDocument13 pagesCorporate Finance Profit and Loss AnalysisChaitanya GembaliNo ratings yet

- Table 1 Summary StatisticsDocument2 pagesTable 1 Summary StatisticsLuz Marina ArboledaNo ratings yet

- Analysis FormaetDocument6 pagesAnalysis FormaetGaurav SoniNo ratings yet

- HDFC by IshanDocument14 pagesHDFC by IshanIshan MalikNo ratings yet

- Financial Management Portfolio AnalysisDocument6 pagesFinancial Management Portfolio AnalysisNakulesh VijayvargiyaNo ratings yet

- Ia FinDocument15 pagesIa FinMinh SuyNo ratings yet

- Hole - ID Hill Depth - Fr. Depth - To Interval Z - From Z - ToDocument4 pagesHole - ID Hill Depth - Fr. Depth - To Interval Z - From Z - ToLouis WirdunaNo ratings yet

- Financials of Canara BankDocument14 pagesFinancials of Canara BankSattwik rathNo ratings yet

- Presented by Harichandana Y (2001MBA018) Sanskriti Bharti (2001MBA022) Pragati Upadhya (2001MBA110)Document23 pagesPresented by Harichandana Y (2001MBA018) Sanskriti Bharti (2001MBA022) Pragati Upadhya (2001MBA110)Harichandana YNo ratings yet

- Titan Co LTD (TTAN IN) - LiquidityDocument2 pagesTitan Co LTD (TTAN IN) - LiquiditySambit SarkarNo ratings yet

- BetasDocument1 pageBetaslu acoriNo ratings yet

- Debt FundsDocument38 pagesDebt FundsArmstrong CapitalNo ratings yet

- 3-Year Financial Projections for BusinessDocument6 pages3-Year Financial Projections for BusinessKuljeet SinghNo ratings yet

- Term Paper On Financial Ratio AnalysisDocument15 pagesTerm Paper On Financial Ratio AnalysisFahim XubayerNo ratings yet

- Financial Analysis 2 - ScribdDocument6 pagesFinancial Analysis 2 - ScribdSanjay KumarNo ratings yet

- Analyze Balance Sheets and Profit-Loss Accounts of 5 CompaniesDocument26 pagesAnalyze Balance Sheets and Profit-Loss Accounts of 5 Companiesdheivayani kNo ratings yet

- SHABNAMKHANDocument20 pagesSHABNAMKHANVijay HemwaniNo ratings yet

- Market ResearchDocument22 pagesMarket ResearchBABU ANo ratings yet

- Analysis of OT TA Stock DP CPDocument5 pagesAnalysis of OT TA Stock DP CPWRSAOBUDGETNo ratings yet

- SAI INTERNET Projections of Profitability, Cash Flow & Balance SheetsDocument8 pagesSAI INTERNET Projections of Profitability, Cash Flow & Balance SheetsAkhil JamadarNo ratings yet

- UDC RevisedDocument13 pagesUDC RevisedAbdul QayumNo ratings yet

- Attribute Coeffs S.E. Wald Z P-ValueDocument8 pagesAttribute Coeffs S.E. Wald Z P-Valuesarthak mendirattaNo ratings yet

- Narayana Hrudayalaya RatiosDocument10 pagesNarayana Hrudayalaya RatiosMovie MasterNo ratings yet

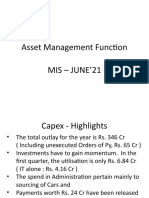

- MFG Asset Mgtpack June 21Document21 pagesMFG Asset Mgtpack June 21muthum44499335No ratings yet

- Impact of Liquidity On Profitability in Telecom Companies: Dr. Mohmad Mushtaq Khan Dr. K. Bhavana RajDocument11 pagesImpact of Liquidity On Profitability in Telecom Companies: Dr. Mohmad Mushtaq Khan Dr. K. Bhavana RajSavy DhillonNo ratings yet

- A Comparative Study Betwe Traditional and Esg Dimensions For Port ConstructionDocument26 pagesA Comparative Study Betwe Traditional and Esg Dimensions For Port ConstructionSiddhesh SheteNo ratings yet

- Case 3Document6 pagesCase 3Dipali SinghNo ratings yet

- Ratios For SugarDocument4 pagesRatios For SugaromairNo ratings yet

- Assignment Brief - Accounting and Finance For Managers - ACC3015Document16 pagesAssignment Brief - Accounting and Finance For Managers - ACC3015AtiqEyashirKanakNo ratings yet

- PSO liquidity and profitabilityDocument9 pagesPSO liquidity and profitabilityKanwal NaazNo ratings yet

- Book 1Document2 pagesBook 1veereshjaiswalNo ratings yet

- Fundcard: Franklin India Smaller Companies FundDocument4 pagesFundcard: Franklin India Smaller Companies FundChiman RaoNo ratings yet

- Financial Analysis of NBFCDocument14 pagesFinancial Analysis of NBFCPKNo ratings yet

- (Monthly %) Freight Loading Position Division Wise As Per FOIS For 13.10.2022Document2 pages(Monthly %) Freight Loading Position Division Wise As Per FOIS For 13.10.2022Rajesh KumarNo ratings yet

- Balance Sheet of ITC: - in Rs. Cr.Document13 pagesBalance Sheet of ITC: - in Rs. Cr.Satyanarayana BodaNo ratings yet

- Data SkripsiDocument52 pagesData SkripsiShafirah AdilahNo ratings yet

- Portfolio July 2005Document10 pagesPortfolio July 2005api-3716002No ratings yet

- Sektor Aneka Industry - Sub ElektronikaDocument3 pagesSektor Aneka Industry - Sub ElektronikaEga PriyatnaNo ratings yet

- Your Holding Details - BAKK1484Document4 pagesYour Holding Details - BAKK1484pandyahitesh6351145099No ratings yet

- Index Today (%) 1 Week (%) 1 Month (%) 6 Months (%) 1 Year (%) YTD (%)Document11 pagesIndex Today (%) 1 Week (%) 1 Month (%) 6 Months (%) 1 Year (%) YTD (%)Violeta TaniNo ratings yet

- Teja WorkDocument12 pagesTeja WorkSiddhant SrivastavaNo ratings yet

- India Cements FADocument154 pagesIndia Cements FARohit KumarNo ratings yet

- ' Ìi'Êü Ì Êì Iê'I Êûiàã Ê Vê V Ýê À Ê Ê ' Ì Àê / Êài Ûiêì Ãê Ì Vi) Êû Ã Ì/ÊDocument8 pages' Ìi'Êü Ì Êì Iê'I Êûiàã Ê Vê V Ýê À Ê Ê ' Ì Àê / Êài Ûiêì Ãê Ì Vi) Êû Ã Ì/ÊArpit MaheshwariNo ratings yet

- RJFInvestment GROUP 4 - Case 4Document57 pagesRJFInvestment GROUP 4 - Case 4dajaNo ratings yet

- Comparison - Ratios - Tyre - DistributionDocument15 pagesComparison - Ratios - Tyre - DistributionParehjuiNo ratings yet

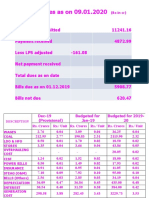

- Power dues as on 09.01.2020 summaryDocument2 pagesPower dues as on 09.01.2020 summaryprasi1010No ratings yet

- BetasDocument7 pagesBetasWendy FernándezNo ratings yet

- Basis and Presumption of The ProjectDocument11 pagesBasis and Presumption of The ProjectVijay HemwaniNo ratings yet

- Linde Bangladesh Limited Balance Sheet: ParticularsDocument16 pagesLinde Bangladesh Limited Balance Sheet: ParticularsShajidul Haq Shahi 173-11-5661No ratings yet

- Company Info - Print FinancialsDocument1 pageCompany Info - Print FinancialsjohnNo ratings yet

- ViTrox's Income and Cash Flow Statements for 2016-2018Document6 pagesViTrox's Income and Cash Flow Statements for 2016-2018Hong JunNo ratings yet

- Irctc: An Assignment ReportDocument12 pagesIrctc: An Assignment ReportAshwani RaiNo ratings yet

- Asia Small and Medium-Sized Enterprise Monitor 2022: Volume I: Country and Regional ReviewsFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2022: Volume I: Country and Regional ReviewsNo ratings yet

- 4.2 Marine InsuranceDocument16 pages4.2 Marine Insurance185Y038 AKSHATA SAWANTNo ratings yet

- CAPE U1 Preparing Financial Statemt IAS 1Document34 pagesCAPE U1 Preparing Financial Statemt IAS 1Nadine DavidsonNo ratings yet

- Development Policies and Agricultural Markets Author(s) - RAMESH CHANDDocument11 pagesDevelopment Policies and Agricultural Markets Author(s) - RAMESH CHANDRegNo ratings yet

- Return and Risk From All Investment DecisionsDocument4 pagesReturn and Risk From All Investment DecisionsAchmad ArdanuNo ratings yet

- Trade Past PapersDocument14 pagesTrade Past PapersMuhammad Ali Khan (AliXKhan)No ratings yet

- Ef4331 Case Study 1Document4 pagesEf4331 Case Study 1Johnny LamNo ratings yet

- History Revision For Garde 7 GMISDocument14 pagesHistory Revision For Garde 7 GMISUtkarsh SandilyaNo ratings yet

- Topic Two Financial Mathematics/Time Value of MoneyDocument43 pagesTopic Two Financial Mathematics/Time Value of Moneysir bookkeeperNo ratings yet

- Receipt BookingDocument1 pageReceipt BookingSultan Gamer 18No ratings yet

- PT BLUE BIRD TBK 2021 Financial ReportDocument111 pagesPT BLUE BIRD TBK 2021 Financial ReportMayyasya UlaNo ratings yet

- Basic Determinants of Exports and ImportsDocument13 pagesBasic Determinants of Exports and ImportsVeer Pratap Singh Jadaun50% (2)

- What Is The Correct Amount of Inventory?: SolutionDocument3 pagesWhat Is The Correct Amount of Inventory?: SolutionSofia LaoNo ratings yet

- FINMAR - Time Value of MoneyDocument2 pagesFINMAR - Time Value of MoneySean Patrick C. WONGNo ratings yet

- Intermediate Accounting 19th Edition Stice Test Bank 1Document40 pagesIntermediate Accounting 19th Edition Stice Test Bank 1pauline100% (45)

- Dry Bulk Cargo - (Import and Export)Document12 pagesDry Bulk Cargo - (Import and Export)Ahmad Fauzi Mehat100% (1)

- Cost Classification (MCQ) SampleDocument3 pagesCost Classification (MCQ) Samplethelkokomg_294988315No ratings yet

- Bacc 4Document16 pagesBacc 4Nhel AlvaroNo ratings yet

- Contemporary World Version 2Document13 pagesContemporary World Version 2Pia Mae LasanasNo ratings yet

- SMEs in Pakistan (Presentation by AZ) 040213Document90 pagesSMEs in Pakistan (Presentation by AZ) 040213zahoor.asad7753No ratings yet

- Frozen Food IndustryDocument9 pagesFrozen Food Industryfms162No ratings yet

- Trade Finance Pricing GuideDocument4 pagesTrade Finance Pricing GuideKhangNo ratings yet

- Airtel Money Statement-19-May-2023 09:41 PM - 620293581Document9 pagesAirtel Money Statement-19-May-2023 09:41 PM - 620293581JamesNo ratings yet

- FINAN204-23A - Tutorial 3Document19 pagesFINAN204-23A - Tutorial 3Xiaohan LuNo ratings yet

- Corporate Finance Chapter 5Document11 pagesCorporate Finance Chapter 5Razan EidNo ratings yet

- Novel and Its HistoryDocument26 pagesNovel and Its HistoryDhruv Singh ShekhawatNo ratings yet