You might also like

- BLACKBOOKDocument98 pagesBLACKBOOKAbhinandan PawarNo ratings yet

- Ms. Priya Raman - 1Document5 pagesMs. Priya Raman - 1priya.08No ratings yet

- 89-The Study On Consumer Awareness Towards Internet Banking Services Provided by Dena BankDocument78 pages89-The Study On Consumer Awareness Towards Internet Banking Services Provided by Dena BankSoham BhurkeNo ratings yet

- A Case Study On Customer Relationship Management Strategy LaveshDocument72 pagesA Case Study On Customer Relationship Management Strategy LaveshNIKHIL SAPKALENo ratings yet

- Screenshot 2024-02-02 at 11.19.18 AMDocument75 pagesScreenshot 2024-02-02 at 11.19.18 AMbkmanoj8363No ratings yet

- Thet Oo Maung (MBF - 70)Document68 pagesThet Oo Maung (MBF - 70)Yar LayNo ratings yet

- Digitalization of Retail Financial ServicesDocument110 pagesDigitalization of Retail Financial ServicesAlaa' Deen ManasraNo ratings yet

- Vicky Project 12Document63 pagesVicky Project 12yashrawas18No ratings yet

- Development and Impact of Mobile Banking in NepalDocument44 pagesDevelopment and Impact of Mobile Banking in NepalSachin JhaNo ratings yet

- NO: Page NoDocument76 pagesNO: Page Nodubeychandan121No ratings yet

- Impact of Digital Banking and Its Role in The Development of Nigeria Banking SystemDocument52 pagesImpact of Digital Banking and Its Role in The Development of Nigeria Banking SystemAFOLABI AZEEZ OLUWASEGUNNo ratings yet

- Impact of Technology in BankingDocument17 pagesImpact of Technology in BankingOliMixNo ratings yet

- Which Bank To Bank With???: A Project by Mr. Rahul IyerDocument78 pagesWhich Bank To Bank With???: A Project by Mr. Rahul IyerRahulprernaNo ratings yet

- Bank of India Project ReportDocument52 pagesBank of India Project Reportashu.01174737667% (6)

- Research Work New - PRNDocument66 pagesResearch Work New - PRNnarayan patelNo ratings yet

- Roll No. 161 (PROJECT REPORT ON "IMPACT OF E-BANKING ON SERVICE QUALITY OF BANKS")Document96 pagesRoll No. 161 (PROJECT REPORT ON "IMPACT OF E-BANKING ON SERVICE QUALITY OF BANKS")Varun Rodi0% (1)

- Supply Chain ProjectDocument62 pagesSupply Chain ProjectreynanutbusterNo ratings yet

- HDFC NetBanking SynopsisDocument5 pagesHDFC NetBanking SynopsisPranavi Paul Pandey100% (1)

- Atef Harb, Mira Thoumy, Michel Yazbeck - 2022Document12 pagesAtef Harb, Mira Thoumy, Michel Yazbeck - 2022Mayang SandyNo ratings yet

- Project 230406173524 f42c00d3 PDFDocument71 pagesProject 230406173524 f42c00d3 PDFJatin sewaniNo ratings yet

- A Report On E-Products of Indian Overseas BankDocument39 pagesA Report On E-Products of Indian Overseas BankThadoi ThangjamNo ratings yet

- Mid-Term ReportDocument16 pagesMid-Term Reportazam bhaiNo ratings yet

- RP 4Document52 pagesRP 4Anuj AgarwalNo ratings yet

- Project ReportDocument38 pagesProject Reportsunidhimishra2375No ratings yet

- BRM Project Under GuidanceDocument25 pagesBRM Project Under GuidancePRUTHIBI PATTANAIKNo ratings yet

- ARINOLADocument41 pagesARINOLATaiwo ArowoloNo ratings yet

- Introduction and Research Design: Chapter - IDocument22 pagesIntroduction and Research Design: Chapter - ISHIVANI chouhanNo ratings yet

- Rahul Jhunjhunwala - Mcom Black BookDocument87 pagesRahul Jhunjhunwala - Mcom Black BookRahul JhunjhunwalaNo ratings yet

- The Evolution of Neobanks in India - 1Document34 pagesThe Evolution of Neobanks in India - 1Ravi BabuNo ratings yet

- 232 Rudrapriya DiwanDocument59 pages232 Rudrapriya DiwanKashish GamreNo ratings yet

- Proposal Mahlet Asefa - Rev NewDocument40 pagesProposal Mahlet Asefa - Rev NewAbdisa GemechuNo ratings yet

- 0158 10 Rohit Soni DissertationDocument43 pages0158 10 Rohit Soni DissertationIshaan JaiswalNo ratings yet

- Project ReportDocument41 pagesProject ReportMahi Singh77% (13)

- IDBI - Retail Banking-Summer InternshipDocument84 pagesIDBI - Retail Banking-Summer InternshipAmol Nagap100% (2)

- Document 2Document69 pagesDocument 2Priyanka SharmaNo ratings yet

- Fere Proposal 1Document30 pagesFere Proposal 1molla fentaye100% (1)

- CONTENTDocument51 pagesCONTENTMuhammed Salim v0% (1)

- Banking SectorDocument54 pagesBanking SectorVicky YadavNo ratings yet

- BRM ISE 1 Groupp PPDocument13 pagesBRM ISE 1 Groupp PPPrajkta ChavanNo ratings yet

- SalimDocument51 pagesSalimMuhammed Salim vNo ratings yet

- Consumer Perception Towards Public SectoDocument24 pagesConsumer Perception Towards Public SectojayNo ratings yet

- Snehal Baikar Rollno 04Document93 pagesSnehal Baikar Rollno 04Akshay ThakurNo ratings yet

- Finance Navya Shenoy M1719042Document85 pagesFinance Navya Shenoy M1719042sanchitkolhe2000No ratings yet

- A Study On Non Performing Assets With Special Reference To Canara BankDocument55 pagesA Study On Non Performing Assets With Special Reference To Canara BankNaveena Shankara100% (1)

- Non Fund Based Activities of BankDocument53 pagesNon Fund Based Activities of BankAKSHAT MAHENDRANo ratings yet

- Customer Satisfaction Regarding Consumer Loan With Specialreference To PUNJAB AND SIND BANKDocument60 pagesCustomer Satisfaction Regarding Consumer Loan With Specialreference To PUNJAB AND SIND BANKSaurabh Mehta0% (1)

- Project On A STUDY ON CONSUMER PERCEPTION OF FEDERAL BANK ATM SERVICES IN VALANCHERY AREADocument57 pagesProject On A STUDY ON CONSUMER PERCEPTION OF FEDERAL BANK ATM SERVICES IN VALANCHERY AREAsalmanulfaris274No ratings yet

- Study of Online Services Offered by BanksDocument34 pagesStudy of Online Services Offered by Bankssarvesh dhatrakNo ratings yet

- Comparative Study of Consumer SatisfactionDocument53 pagesComparative Study of Consumer SatisfactionnikhilNo ratings yet

- FS Project 1Document33 pagesFS Project 1Tarun MishraNo ratings yet

- Rool No 32 BlackBook A Study Related To Consumer Perception Towards Payment Bank and Its Impact On Indian EconomyDocument67 pagesRool No 32 BlackBook A Study Related To Consumer Perception Towards Payment Bank and Its Impact On Indian Economynishanth naikNo ratings yet

- Shubhi RPRDocument82 pagesShubhi RPRSāñyä CháuràsiãNo ratings yet

- A Project Report On Online BankingDocument18 pagesA Project Report On Online BankingSourav PaulNo ratings yet

- Banking and Finance ProjectDocument61 pagesBanking and Finance Projectjustonlyforfun1996No ratings yet

- Online Banking FinalDocument34 pagesOnline Banking FinalSuman Hazra100% (1)

- New Generation Banking in IndiaDocument9 pagesNew Generation Banking in IndiaGanesh TiwariNo ratings yet

- Roshani Raj SinghDocument34 pagesRoshani Raj Singhrupendratripathi2019No ratings yet

- Road Map for Developing an Online Platform to Trade Nonperforming Loans in Asia and the PacificFrom EverandRoad Map for Developing an Online Platform to Trade Nonperforming Loans in Asia and the PacificNo ratings yet

- The Role of Central Bank Digital Currencies in Financial Inclusion: Asia–Pacific Financial Inclusion Forum 2022From EverandThe Role of Central Bank Digital Currencies in Financial Inclusion: Asia–Pacific Financial Inclusion Forum 2022No ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- A Study of Financial Planning and Invest2Document6 pagesA Study of Financial Planning and Invest2Saurav RanaNo ratings yet

- Impact Turn File - MichiganClassic 2013 CTDocument125 pagesImpact Turn File - MichiganClassic 2013 CTmachina07No ratings yet

- Cir vs. Solidbank Corporation2Document1 pageCir vs. Solidbank Corporation2Raquel DoqueniaNo ratings yet

- Strategic Financial Management EssayDocument19 pagesStrategic Financial Management EssayTafadzwa Muza100% (9)

- AASB-16 Sap RefxDocument2 pagesAASB-16 Sap RefxSyed RizwanaNo ratings yet

- Enhanced Consumer Credit Report: Enquiry DetailsDocument9 pagesEnhanced Consumer Credit Report: Enquiry Detailsarcman17100% (1)

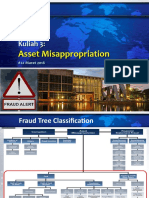

- Asset MisappropriationDocument15 pagesAsset MisappropriationKelas 7-02 D-IV AKTNo ratings yet

- Study of Organisational Structure Syndicate BankDocument48 pagesStudy of Organisational Structure Syndicate BankJissy Shravan50% (2)

- Dawit Final ProposalDocument32 pagesDawit Final ProposalGetu Weyessa0% (1)

- 2012 Ontario Tax FormDocument2 pages2012 Ontario Tax FormHassan MhNo ratings yet

- India Real Estate Residential Office h1 2020 Indian Real Estate Residential Office 7302Document145 pagesIndia Real Estate Residential Office h1 2020 Indian Real Estate Residential Office 7302Venkatesh SankarNo ratings yet

- RG1575748 PDFDocument1 pageRG1575748 PDFJohn BakerNo ratings yet

- Lehman Brothers:: Too Big To Fail?Document13 pagesLehman Brothers:: Too Big To Fail?abbiecdefgNo ratings yet

- Audit of InvestmentDocument70 pagesAudit of InvestmentJoanne RomaNo ratings yet

- Bank RiskPrudential NormsDocument35 pagesBank RiskPrudential Normsdivanshu aroraNo ratings yet

- BIR Provides "Rich Broth" For CorruptionDocument4 pagesBIR Provides "Rich Broth" For Corruptionrico mangawiliNo ratings yet

- Answers For Chapter 4Document3 pagesAnswers For Chapter 4Wan MP WilliamNo ratings yet

- Cif IndividualDocument2 pagesCif IndividualKeyla LumapasNo ratings yet

- MB20202 Corporate Finance Unit V Study MaterialsDocument33 pagesMB20202 Corporate Finance Unit V Study MaterialsSarath kumar CNo ratings yet

- Basics Fundamental AnalysisDocument5 pagesBasics Fundamental AnalysispudiwalaNo ratings yet

- Current Liabilities and Contingencies: True-FalseDocument8 pagesCurrent Liabilities and Contingencies: True-FalseCarlo ParasNo ratings yet

- Ar 2020 BTPN Eng 14 AprilDocument612 pagesAr 2020 BTPN Eng 14 AprilklieindwrNo ratings yet

- #Pvofguaranteedpaymentof10,000In5Years: PV PVDocument7 pages#Pvofguaranteedpaymentof10,000In5Years: PV PVL.E.O.ZNo ratings yet

- Exercise 1 - Balancing The Acctg Equation - v2Document1 pageExercise 1 - Balancing The Acctg Equation - v2Ai MelNo ratings yet

- Barclays U Unity Software Inc. Beat & Raise With $1B EBITDA TargetDocument15 pagesBarclays U Unity Software Inc. Beat & Raise With $1B EBITDA Targetoldman lokNo ratings yet

- Tax 5th Semeter Selected Questions PDFDocument40 pagesTax 5th Semeter Selected Questions PDFAvBNo ratings yet

- CFA III-Asset Allocation关键词清单Document27 pagesCFA III-Asset Allocation关键词清单Lê Chấn PhongNo ratings yet

- 5 (1) - Aggregate Demand and Aggregate Supply PDFDocument8 pages5 (1) - Aggregate Demand and Aggregate Supply PDFBilly Vince AlquinoNo ratings yet

- The Macroeconomic Impact of Remittances in The Philippines: Lecture No. 8Document41 pagesThe Macroeconomic Impact of Remittances in The Philippines: Lecture No. 8bazgukNo ratings yet

- AbstractDocument2 pagesAbstractSakub Amin Sick'L'No ratings yet