You might also like

- TDRIDocument26 pagesTDRIChatis HerabutNo ratings yet

- Introduction To Business Valuation: February 2013Document66 pagesIntroduction To Business Valuation: February 2013Nguyen Hoang Phuong100% (3)

- Ming The Mechanic - The Unknown 20 Trillion Dollar CompanyDocument27 pagesMing The Mechanic - The Unknown 20 Trillion Dollar CompanyJesus BerriosNo ratings yet

- Mckinsey Presentation On Managing The DownturnDocument16 pagesMckinsey Presentation On Managing The DownturnRehan FariasNo ratings yet

- Part 1Document3 pagesPart 1PRETTYKO100% (1)

- 4 Future Telecom TrendsDocument24 pages4 Future Telecom TrendsArtem SmirnovNo ratings yet

- Khối 4 + 5 - TIMO Vòng 2Document33 pagesKhối 4 + 5 - TIMO Vòng 2Nguyen Hoang Phuong100% (3)

- Q S Log Book KenyaDocument25 pagesQ S Log Book KenyaswazsurvNo ratings yet

- India Office MarketView Q1 2019 PuneDocument7 pagesIndia Office MarketView Q1 2019 PuneAbhilash BhatNo ratings yet

- Warehousing Category Dashboard: 30 July 2019Document4 pagesWarehousing Category Dashboard: 30 July 2019Abdul Wassey MehmoodNo ratings yet

- Global Trade: UpdateDocument8 pagesGlobal Trade: UpdatesanzitNo ratings yet

- Kantar Worldpanel Division FMCG Monitor Full Year 2020 EN FinalDocument10 pagesKantar Worldpanel Division FMCG Monitor Full Year 2020 EN FinalvinhtamledangNo ratings yet

- IUMI Stats Report 5c62966a7392dDocument28 pagesIUMI Stats Report 5c62966a7392dPratik ChavanNo ratings yet

- Ditcinf2021d2 enDocument8 pagesDitcinf2021d2 enseafishNo ratings yet

- HDFC Life Presentation - Q1 FY21 FinalDocument59 pagesHDFC Life Presentation - Q1 FY21 FinaljhopadlpNo ratings yet

- JLL India Residential Market Update q1 2020Document17 pagesJLL India Residential Market Update q1 2020Aniket Ranjan (B.A. LLB 16)No ratings yet

- Mgt-201 Assignment International Trade, Trends in World Trade and Overview of India'S TradeDocument21 pagesMgt-201 Assignment International Trade, Trends in World Trade and Overview of India'S TradeGable kaura L-2020 -A-16-BIVNo ratings yet

- Investment Brief SUMMER 2019 FINALDocument16 pagesInvestment Brief SUMMER 2019 FINALMeeraNo ratings yet

- Kantar Worldpanel FMCG Monitor Sep 2018 EN FinalDocument9 pagesKantar Worldpanel FMCG Monitor Sep 2018 EN FinalThao VuNo ratings yet

- India Office MarketView Q1 2019 MumbaiDocument7 pagesIndia Office MarketView Q1 2019 MumbaiAbhilash BhatNo ratings yet

- 2018 q1 Commercial Real Estate Market Survey 09-07-2018Document15 pages2018 q1 Commercial Real Estate Market Survey 09-07-2018National Association of REALTORS®No ratings yet

- NBP Funds Take On Federal Budget FY2021 PDFDocument11 pagesNBP Funds Take On Federal Budget FY2021 PDFWaleed AnsariNo ratings yet

- Air Cargo Market Analysis: Air Cargo Volumes Reached An All-Time High in MarchDocument4 pagesAir Cargo Market Analysis: Air Cargo Volumes Reached An All-Time High in MarchJuan ArcilaNo ratings yet

- 2018 Q4 Jakarta Retail Market Report ColliersDocument10 pages2018 Q4 Jakarta Retail Market Report ColliersNovia PutriNo ratings yet

- The State of The Economy - DR Salami UpdatedDocument21 pagesThe State of The Economy - DR Salami UpdatedEfosa AigbeNo ratings yet

- Rhizome Partners Q2 2020 Investor Letter FinalDocument12 pagesRhizome Partners Q2 2020 Investor Letter FinalAndy HuffNo ratings yet

- Home Purchase Affordability Index: Research ReportDocument13 pagesHome Purchase Affordability Index: Research ReportCelestine DcruzNo ratings yet

- Consumer - Outlook - 3jan22 - JM FinancialDocument14 pagesConsumer - Outlook - 3jan22 - JM FinancialBinoy JariwalaNo ratings yet

- Auto Post COVID-19 - 052920 - tcm9-249607Document10 pagesAuto Post COVID-19 - 052920 - tcm9-249607Bidyut Bhusan PandaNo ratings yet

- Real Estate Market Outlook H1 2020 - RomaniaDocument28 pagesReal Estate Market Outlook H1 2020 - RomaniaAnonymous 4gOYyVfdfNo ratings yet

- Quang Ninh Research Report 2020Document26 pagesQuang Ninh Research Report 2020Architecte UrbanisteNo ratings yet

- GDP 2020 Q1Document34 pagesGDP 2020 Q1Primedia BroadcastingNo ratings yet

- Economic Impact of Covid-19 in The Philippines: Fact File 2020Document26 pagesEconomic Impact of Covid-19 in The Philippines: Fact File 2020Girlee Jhene CadeliñaNo ratings yet

- Mumbai Off 3q15Document3 pagesMumbai Off 3q15Pushkar JadhavNo ratings yet

- WPP 2020 First Quarter Trading Statement PresentationDocument33 pagesWPP 2020 First Quarter Trading Statement PresentationJuan Carlos Garcia SanchezNo ratings yet

- Kantar - Worldpanel Division - FMCG Monitor October 2019 - ENDocument9 pagesKantar - Worldpanel Division - FMCG Monitor October 2019 - ENCuong Chi HuyenNo ratings yet

- ReQ Real Estate Quarterly HighlightsDocument8 pagesReQ Real Estate Quarterly HighlightsVaibhav RaghuvanshiNo ratings yet

- IP - Q2 FY 2020 Affle IndiaDocument15 pagesIP - Q2 FY 2020 Affle IndiaS.Sharique HassanNo ratings yet

- Canada Office and Industrial - CBRE - Q4 2019Document34 pagesCanada Office and Industrial - CBRE - Q4 2019JP & PANo ratings yet

- Nesg G1Document6 pagesNesg G1yahayaNo ratings yet

- US Industrial MarketBeat Q2 2020 PDFDocument7 pagesUS Industrial MarketBeat Q2 2020 PDFRN7 BackupNo ratings yet

- 2018 - Investor - Presentation - Q1-2019 ICICILombard - General - Insurance PDFDocument20 pages2018 - Investor - Presentation - Q1-2019 ICICILombard - General - Insurance PDFRAHUL PANDEYNo ratings yet

- FMCG Infographic June 2020Document1 pageFMCG Infographic June 2020Sanket SharmaNo ratings yet

- Delhi NCR: Industrial Q2 2020Document2 pagesDelhi NCR: Industrial Q2 2020Shivam SharmaNo ratings yet

- Cairo: The Real Estate MarketDocument5 pagesCairo: The Real Estate MarketGamal SalemNo ratings yet

- IFC SlidesDocument10 pagesIFC SlidesducvaNo ratings yet

- Impact of Covid-19 On Banking in IndiaDocument19 pagesImpact of Covid-19 On Banking in IndiaAakash MalhotraNo ratings yet

- Market Update - Transportation - June 2020 PDFDocument24 pagesMarket Update - Transportation - June 2020 PDFVineetNo ratings yet

- KDQTDocument20 pagesKDQTNGỌC NGUYỄN THỊ NHƯNo ratings yet

- CBRE Asia Pacific MarketView Q2 2019Document18 pagesCBRE Asia Pacific MarketView Q2 2019Kenny Huynh100% (1)

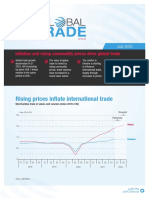

- GL Bal: Rising Prices Inflate International TradeDocument11 pagesGL Bal: Rising Prices Inflate International TradeBekele Guta GemeneNo ratings yet

- Presentation Q4 2018 ResultsDocument47 pagesPresentation Q4 2018 ResultsKỳ Anh TôNo ratings yet

- Investors Presentation-6 June2018Document27 pagesInvestors Presentation-6 June2018tat angNo ratings yet

- Brazil Economic Outlook 4Q18Document27 pagesBrazil Economic Outlook 4Q18joseNo ratings yet

- CECE Annual Economic Report 2020Document18 pagesCECE Annual Economic Report 2020Shantha RaoNo ratings yet

- 2022 Federal Reserve Stress Test Results: June 2022Document66 pages2022 Federal Reserve Stress Test Results: June 2022ZerohedgeNo ratings yet

- 2020.02.03 - Vingroup 4Q2019 Results PDFDocument41 pages2020.02.03 - Vingroup 4Q2019 Results PDFQuach TuNo ratings yet

- Lebanese Economy Off To A Lackluster Start in 2019: April 2019Document8 pagesLebanese Economy Off To A Lackluster Start in 2019: April 2019ismail hotaitNo ratings yet

- Investor PresentationDocument38 pagesInvestor Presentationchaitanya.jNo ratings yet

- India Mumbai Office Q3 2019Document2 pagesIndia Mumbai Office Q3 2019Animesh DharamsiNo ratings yet

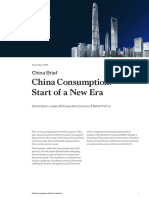

- 中国消费:新时代的开始(英)Document6 pages中国消费:新时代的开始(英)jessica.haiyan.zhengNo ratings yet

- 2017 q4 Commercial Real Estate Market Survey 3-8-2018Document15 pages2017 q4 Commercial Real Estate Market Survey 3-8-2018National Association of REALTORS®No ratings yet

- COVID 19 Outlook For Airlines' Cash BurnDocument12 pagesCOVID 19 Outlook For Airlines' Cash BurnTatiana RokouNo ratings yet

- Monetary Policy 2020 Pakistan PDFDocument20 pagesMonetary Policy 2020 Pakistan PDFiftikharhassanNo ratings yet

- Vietnam Real Estate Market Briefs q1 2017Document7 pagesVietnam Real Estate Market Briefs q1 2017Linh NguyenNo ratings yet

- A New Dawn for Global Value Chain Participation in the PhilippinesFrom EverandA New Dawn for Global Value Chain Participation in the PhilippinesNo ratings yet

- 2007 The Wealth ReportDocument31 pages2007 The Wealth ReportNguyen Hoang PhuongNo ratings yet

- Ligj Për Të Huajt - Nr. 79.2021 - EnglishDocument71 pagesLigj Për Të Huajt - Nr. 79.2021 - EnglishNguyen Hoang PhuongNo ratings yet

- Khối 2 + Khối 3 - TIMO Vòng 2Document31 pagesKhối 2 + Khối 3 - TIMO Vòng 2Nguyen Hoang PhuongNo ratings yet

- CBRE-Global Living - 2020 - FinalDocument48 pagesCBRE-Global Living - 2020 - FinalAyoub LyafNo ratings yet

- 8641 E Outer DriveDocument6 pages8641 E Outer DriveNguyen Hoang PhuongNo ratings yet

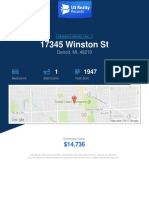

- Winston ReportDocument6 pagesWinston ReportNguyen Hoang PhuongNo ratings yet

- Greek Food & Beverage - Invest in Taste - 032018Document28 pagesGreek Food & Beverage - Invest in Taste - 032018Nguyen Hoang PhuongNo ratings yet

- A Snapshot of The Greek Education SystemDocument16 pagesA Snapshot of The Greek Education SystemNguyen Hoang PhuongNo ratings yet

- Knight Frank - BDS London 2017Document11 pagesKnight Frank - BDS London 2017Nguyen Hoang PhuongNo ratings yet

- Ngoc Tran Thi DISC and MotivatorsDocument10 pagesNgoc Tran Thi DISC and MotivatorsNguyen Hoang PhuongNo ratings yet

- A Guide To Global Citizenship THE 2019 Cbi Index: Special Report August/September 2019Document36 pagesA Guide To Global Citizenship THE 2019 Cbi Index: Special Report August/September 2019ArunNo ratings yet

- Report LI at BSNDocument8 pagesReport LI at BSNSitie Fatima ElaniNo ratings yet

- holdcoPIK FridsonDocument30 pagesholdcoPIK Fridsongbana999No ratings yet

- Qasim ShabbierDocument4 pagesQasim ShabbierAnonymous 1j5KpNNo ratings yet

- Final Report: Submitted By: TAIMOOR RIAZ 13044954-030 Submitted ToDocument65 pagesFinal Report: Submitted By: TAIMOOR RIAZ 13044954-030 Submitted ToSherryMirzaNo ratings yet

- Anurag - Matrimonial DetailsDocument4 pagesAnurag - Matrimonial Detailsmonujeejaji0% (1)

- Factors Influencing Unethical Behavior of Insurance Agents: DR Hasnah HaronDocument1 pageFactors Influencing Unethical Behavior of Insurance Agents: DR Hasnah HaronmaryamfarqNo ratings yet

- DevaluationDocument4 pagesDevaluationYuvraj Vikram singhNo ratings yet

- IB Chapter # 12Document22 pagesIB Chapter # 12Ma Quang ThinhNo ratings yet

- Camposol Holding 3q 2020 Presentation PDFDocument23 pagesCamposol Holding 3q 2020 Presentation PDFJorge Zegarra ValverdeNo ratings yet

- Testbank - Multinational Business Finance - Chapter 12Document15 pagesTestbank - Multinational Business Finance - Chapter 12Uyen Nhi NguyenNo ratings yet

- Behavioral FinanceDocument20 pagesBehavioral FinanceLAZY TWEETYNo ratings yet

- IPP Report PDFDocument296 pagesIPP Report PDFMuhammad ZubairNo ratings yet

- Guidelines For Corporate Strategic Audit ProjectDocument7 pagesGuidelines For Corporate Strategic Audit ProjectMay Cris BondocNo ratings yet

- Professional Code For The Financial Services IndustryDocument21 pagesProfessional Code For The Financial Services IndustryMubarakNo ratings yet

- PGBP - PaperDocument6 pagesPGBP - PapermuskaanNo ratings yet

- WCM EstimationDocument3 pagesWCM Estimationtanya.p23No ratings yet

- FAR 4.3MC Investments in Debt Equity InstrumentsDocument4 pagesFAR 4.3MC Investments in Debt Equity InstrumentsEunice FulgencioNo ratings yet

- Times-Trib 43 MGDocument28 pagesTimes-Trib 43 MGnewspubincNo ratings yet

- The 15th Malaysian Capital Market Summit - ASLI - AgendaDocument3 pagesThe 15th Malaysian Capital Market Summit - ASLI - Agendameor_ayobNo ratings yet

- Unit 5 - Credit Management - Problem 1Document3 pagesUnit 5 - Credit Management - Problem 1Dennis BijuNo ratings yet

- Motilal Oswaal (Q3 Fy23)Document10 pagesMotilal Oswaal (Q3 Fy23)harshbhutra1234No ratings yet

- SCDL BusinessLaw Assignment Oct20Document9 pagesSCDL BusinessLaw Assignment Oct20priyajeejo100% (1)

- Tax Expenditures in Latin America Civil Society Perspective English Ibp 2019Document27 pagesTax Expenditures in Latin America Civil Society Perspective English Ibp 2019Paolo de RenzioNo ratings yet

- Lecture 18 BH CH 9 Stock and Their Valuation Part 2Document23 pagesLecture 18 BH CH 9 Stock and Their Valuation Part 2Alif SultanliNo ratings yet

- FI CIN User Manual V1Document38 pagesFI CIN User Manual V1jagankilariNo ratings yet

- Doctrines Prudential Bank vs. Intermediate Appellate Court, 216 SCRA 257Document5 pagesDoctrines Prudential Bank vs. Intermediate Appellate Court, 216 SCRA 257Bechay PallasigueNo ratings yet