You might also like

- Advanced Financial Management Mock Examination December 2018Document6 pagesAdvanced Financial Management Mock Examination December 2018David LeeNo ratings yet

- Securitization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsFrom EverandSecuritization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsNo ratings yet

- CA-Inter-FM-SM-Q-MTP-2-May-2024-castudynotes-comDocument12 pagesCA-Inter-FM-SM-Q-MTP-2-May-2024-castudynotes-comsaurabhNo ratings yet

- Innovative Infrastructure Financing through Value Capture in IndonesiaFrom EverandInnovative Infrastructure Financing through Value Capture in IndonesiaRating: 5 out of 5 stars5/5 (1)

- MTP 17 53 Questions 1710507531Document9 pagesMTP 17 53 Questions 1710507531janasenalogNo ratings yet

- GTU MBA Semester 2 Financial Management Exam QuestionsDocument3 pagesGTU MBA Semester 2 Financial Management Exam QuestionsAmul PatelNo ratings yet

- Financial Management-P III - Nov 08Document4 pagesFinancial Management-P III - Nov 08gundapolaNo ratings yet

- FM Ca - Zambia - June - 2022 - Q - A-184-208Document25 pagesFM Ca - Zambia - June - 2022 - Q - A-184-208Prince MulengaNo ratings yet

- (l6) Corporate Financial Management2015Document22 pages(l6) Corporate Financial Management2015Moses Mvula100% (2)

- AS Business AnalysisDocument4 pagesAS Business AnalysisLaskar REAZNo ratings yet

- Question PaperDocument3 pagesQuestion PaperAmbrishNo ratings yet

- Financial Management: Acca Revision Mock 3Document13 pagesFinancial Management: Acca Revision Mock 3krishna gopalNo ratings yet

- Financial Management Tutorial QuestionsDocument8 pagesFinancial Management Tutorial QuestionsStephen Olieka100% (2)

- Cfi 5102 Final 2016Document5 pagesCfi 5102 Final 2016MukandionaNo ratings yet

- BAF 2104 Financial Management EssentialsDocument2 pagesBAF 2104 Financial Management EssentialscyrusNo ratings yet

- 7 Corporate Finance - Prof. Gagan SharmaDocument4 pages7 Corporate Finance - Prof. Gagan SharmaVampireNo ratings yet

- Сем 3 (задание 1)Document18 pagesСем 3 (задание 1)Максим НовакNo ratings yet

- Ba Fin430finalDocument4 pagesBa Fin430finalIzzy BbyNo ratings yet

- Financial Management Exam QuestionsDocument12 pagesFinancial Management Exam QuestionsAZLEA BINTI SYED HUSSIN (BG)No ratings yet

- Pyq Merge f9Document90 pagesPyq Merge f9Anonymous gdA3wqWcPNo ratings yet

- June 2014 - OAP CoDocument8 pagesJune 2014 - OAP CoEgyiri FrederickNo ratings yet

- December 2010 Examination: FM12 Financial Management Time: Three Hours Maximum Marks: 100Document5 pagesDecember 2010 Examination: FM12 Financial Management Time: Three Hours Maximum Marks: 100Eashan YadavNo ratings yet

- Business Analysis: (B) What Is An Operating Turnaround Strategy ? 4Document4 pagesBusiness Analysis: (B) What Is An Operating Turnaround Strategy ? 4Davies MumbaNo ratings yet

- CPA 8 - Financial Management - Paper 8Document13 pagesCPA 8 - Financial Management - Paper 8justinorchidsNo ratings yet

- Financial Management Paper F9Document5 pagesFinancial Management Paper F9Nirmal ShresthaNo ratings yet

- Q and As-Corporate Financial Management - June 2010 Dec 2010 and June 2011Document71 pagesQ and As-Corporate Financial Management - June 2010 Dec 2010 and June 2011chisomo_phiri72290% (2)

- 78735bos63031 p6Document44 pages78735bos63031 p6dileepkarumuri93No ratings yet

- Baf2104 Financial Management I, School BasedDocument4 pagesBaf2104 Financial Management I, School BasedLemaronNo ratings yet

- University of Mauritius: Faculty of Law and ManagementDocument10 pagesUniversity of Mauritius: Faculty of Law and Managementmis gunNo ratings yet

- 2016 PaperDocument5 pages2016 PaperumeshNo ratings yet

- Section A: Compulsory: Question 1 (25 Marks)Document10 pagesSection A: Compulsory: Question 1 (25 Marks)mis gunNo ratings yet

- sFikv8tLO3DuTOB3I8bY--4762Document2 pagessFikv8tLO3DuTOB3I8bY--4762dipusharma4200No ratings yet

- MBA 5109 - Financial Management (MBA 2020-2022)Document6 pagesMBA 5109 - Financial Management (MBA 2020-2022)sreekavi19970120No ratings yet

- Gujarat Technological UniversityDocument3 pagesGujarat Technological UniversityAmul PatelNo ratings yet

- It Governance TechnologyDocument5 pagesIt Governance TechnologyIQBAL MAHMUDNo ratings yet

- Question No. 1 Is Compulsory. Attempt Any Four Questions From The Remaining Five Questions. Working Notes Should Form Part of The AnswerDocument5 pagesQuestion No. 1 Is Compulsory. Attempt Any Four Questions From The Remaining Five Questions. Working Notes Should Form Part of The AnswerAyushi GuptaNo ratings yet

- BV 2Document4 pagesBV 2Eshal KhanNo ratings yet

- The Title of KingdomDocument6 pagesThe Title of KingdomKailash RNo ratings yet

- 2017 PaperDocument5 pages2017 PaperumeshNo ratings yet

- D2 Question Answer June 2016Document15 pagesD2 Question Answer June 2016Chisanga ChilubaNo ratings yet

- Paper 10 Financial ManagementDocument10 pagesPaper 10 Financial ManagementJoseph OsakoNo ratings yet

- UntitledDocument5 pagesUntitledbetty KemNo ratings yet

- BFC 3226 Introduction To Financial Management - 5Document3 pagesBFC 3226 Introduction To Financial Management - 5karashinokov siwoNo ratings yet

- CFI5102201412 Advanced Corporate Financial StrategyDocument5 pagesCFI5102201412 Advanced Corporate Financial StrategyFungai MukundiwaNo ratings yet

- TWO (2) Questions From SECTION B in The Answer Booklet Provided. All Question CarryDocument4 pagesTWO (2) Questions From SECTION B in The Answer Booklet Provided. All Question CarrynatlyhNo ratings yet

- AFM Test 1Document3 pagesAFM Test 1Syeda IsmailNo ratings yet

- BSF 1102 - Principles of Finance - November 2022Document6 pagesBSF 1102 - Principles of Finance - November 2022JulianNo ratings yet

- Question Paper Code:: Reg. No.Document26 pagesQuestion Paper Code:: Reg. No.Khanal NilambarNo ratings yet

- Questions For Group 1: S.B.Khatri-FM-AIMDocument6 pagesQuestions For Group 1: S.B.Khatri-FM-AIMAbhishek singhNo ratings yet

- Questions For Group 1: S.B.Khatri-FM-AIMDocument6 pagesQuestions For Group 1: S.B.Khatri-FM-AIMAbhishek singhNo ratings yet

- Financial Management-1Document6 pagesFinancial Management-1chelseaNo ratings yet

- AL Financial Management Nov Dec 2013Document4 pagesAL Financial Management Nov Dec 2013hyp siinNo ratings yet

- GTU MBA Semester II Exam Financial Management QuestionsDocument4 pagesGTU MBA Semester II Exam Financial Management QuestionsVicky ThakkarNo ratings yet

- B1 B4 B5 MergedDocument64 pagesB1 B4 B5 MergedHussein AbdallahNo ratings yet

- ADVANCED-FINANCIAL-MANAGEMENT-may 2016 Icag PDFDocument21 pagesADVANCED-FINANCIAL-MANAGEMENT-may 2016 Icag PDFmohedNo ratings yet

- Bec524 and Bec524e Test 2 October 2022Document5 pagesBec524 and Bec524e Test 2 October 2022Walter tawanda MusosaNo ratings yet

- SFM Q 2Document5 pagesSFM Q 2riyaNo ratings yet

- InvestmentDocument8 pagesInvestmentFrederick GbliNo ratings yet

- Ex.C.BudgetDocument3 pagesEx.C.BudgetGeethika NayanaprabhaNo ratings yet

- Witness Affidavit Motorcycle Installment Purchase DeceptionDocument2 pagesWitness Affidavit Motorcycle Installment Purchase DeceptionFeisty LionessNo ratings yet

- Group 1 SDM Designs by KateDocument8 pagesGroup 1 SDM Designs by KateYATIN BAJAJNo ratings yet

- Strategy and Analysis in Using Net Present Value: Multiple Choice QuestionsDocument12 pagesStrategy and Analysis in Using Net Present Value: Multiple Choice Questionsphantom ceilNo ratings yet

- Infosys - HRM Case StudyDocument25 pagesInfosys - HRM Case StudySAINo ratings yet

- Asme B16-25 1997Document22 pagesAsme B16-25 1997susisaravananNo ratings yet

- Day 3 BootcampDocument55 pagesDay 3 BootcampLissaNo ratings yet

- KFCDocument15 pagesKFCSubham ChakrabortyNo ratings yet

- The Institute of Chartered Accountants of PakistanDocument3 pagesThe Institute of Chartered Accountants of PakistanSuman UroojNo ratings yet

- Exercise 1Document4 pagesExercise 1Musa NgobeniNo ratings yet

- 3 Day Tour Package Costing SheetDocument4 pages3 Day Tour Package Costing SheetRica Marie BarbenNo ratings yet

- Globalization, Slobalization and LocalizationDocument2 pagesGlobalization, Slobalization and LocalizationSadiq NaseerNo ratings yet

- Oracle Identity Cloud ServicesDocument12 pagesOracle Identity Cloud ServicesAlice JohnsonNo ratings yet

- Vertical and Horizantal Analysis of Ultratech CementDocument12 pagesVertical and Horizantal Analysis of Ultratech Cementthamil marpanNo ratings yet

- MGT489 - Final ExamDocument5 pagesMGT489 - Final ExamNahida akter jannat 1712024630No ratings yet

- Acquisitions Incorporated D&D5eDocument226 pagesAcquisitions Incorporated D&D5eLucas Saposnik100% (5)

- Britinnia Cheese: A Class Assignment ReportDocument15 pagesBritinnia Cheese: A Class Assignment ReportAshwani RaiNo ratings yet

- Test Bank For Marketing For Hospitality and Tourism 6Th Edition Kotler Bowen Makens 0132784025 9780132784023 Full Chapter PDFDocument28 pagesTest Bank For Marketing For Hospitality and Tourism 6Th Edition Kotler Bowen Makens 0132784025 9780132784023 Full Chapter PDFjenny.goyco725100% (11)

- AFOMA To Enable Social Impact With Decentralized E-CommerceDocument4 pagesAFOMA To Enable Social Impact With Decentralized E-CommercePR.comNo ratings yet

- Product Recall SOPDocument3 pagesProduct Recall SOPvioletaflora81% (16)

- Anton Kriel Detailed ReviewDocument4 pagesAnton Kriel Detailed ReviewMus'ab Abdullahi Bulale100% (2)

- WerehouseDocument41 pagesWerehouseRamon ColonNo ratings yet

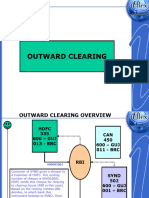

- 5-SETTLEMENT-Outward Clearing 1Document21 pages5-SETTLEMENT-Outward Clearing 1ola.cloudsNo ratings yet

- Bruin Dog Grooming Journals - Rev 15Document40 pagesBruin Dog Grooming Journals - Rev 15Rishab KhandelwalNo ratings yet

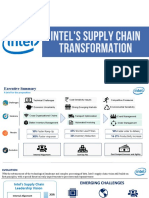

- Intel - FinalDocument6 pagesIntel - FinalChaitanya GuptaNo ratings yet

- Economics - 1.1 The Market System - Igcse EdexcelDocument10 pagesEconomics - 1.1 The Market System - Igcse EdexcelWateen JaberNo ratings yet

- Booklet - Business Immersion Program 2023Document34 pagesBooklet - Business Immersion Program 2023Kenneth ChandrawidjajaNo ratings yet

- Call Centre Investment ProposalDocument3 pagesCall Centre Investment ProposalPredueElleNo ratings yet

- Cleanliness Is Next To Godliness EssayDocument4 pagesCleanliness Is Next To Godliness Essayafabeaida100% (2)

- Synopsis: A Study On Customer Satisfaction AT Nerolac Paints LTD., KadapaDocument5 pagesSynopsis: A Study On Customer Satisfaction AT Nerolac Paints LTD., KadapaAnu GraphicsNo ratings yet

- Volkswagen Emission ScandalDocument5 pagesVolkswagen Emission Scandalavijeetboparai100% (2)