You might also like

- CA Inter Taxation Q MTP 2 May 23Document11 pagesCA Inter Taxation Q MTP 2 May 23sureshstipl sureshNo ratings yet

- UntitledDocument11 pagesUntitleddeepika devsaniNo ratings yet

- Tax (Old) Q Mtp1 Ipc Oct21Document10 pagesTax (Old) Q Mtp1 Ipc Oct21Karan Singh RanaNo ratings yet

- Test Series: March, 2021 Mock Test Paper 1 Intermediate (New) Course Paper - 4: Taxation Time Allowed - 3 Hours Maximum Marks - 100 Section - A: Income Tax Law (60 Marks)Document11 pagesTest Series: March, 2021 Mock Test Paper 1 Intermediate (New) Course Paper - 4: Taxation Time Allowed - 3 Hours Maximum Marks - 100 Section - A: Income Tax Law (60 Marks)M100% (1)

- MTP 10 17 Questions 1694188914Document11 pagesMTP 10 17 Questions 1694188914luvkumar3532No ratings yet

- MTP 12 17 Questions 1696512917Document11 pagesMTP 12 17 Questions 1696512917harshallahotNo ratings yet

- MTP 2 TaxDocument10 pagesMTP 2 TaxPrathmesh JambhulkarNo ratings yet

- Mock Test - 4-2Document16 pagesMock Test - 4-2Deepsikha maitiNo ratings yet

- DT 2 New Question PaperDocument11 pagesDT 2 New Question Paperneha manglaniNo ratings yet

- MCQ CH 12 - Set-Off and Carry Forward of Losses - Nov 23Document10 pagesMCQ CH 12 - Set-Off and Carry Forward of Losses - Nov 23NikiNo ratings yet

- Mock Test - 2-2Document10 pagesMock Test - 2-2Deepsikha maitiNo ratings yet

- Basics & House Property - PaperDocument5 pagesBasics & House Property - PaperLaavanya JainNo ratings yet

- Basics & House Property - PaperDocument5 pagesBasics & House Property - PaperVenkataRajuNo ratings yet

- 71668bos57670 Inter p4q PDFDocument11 pages71668bos57670 Inter p4q PDFmonikaNo ratings yet

- Direct Tax Laws & International Taxation Mock Test Paper SeriesDocument11 pagesDirect Tax Laws & International Taxation Mock Test Paper SeriesDeepsikha maitiNo ratings yet

- 27-3-24... 4110 GR I... Int-3019... Tax Mcq... QueDocument7 pages27-3-24... 4110 GR I... Int-3019... Tax Mcq... Quenikulgauswami9033No ratings yet

- IncomeTax-2Document6 pagesIncomeTax-2Aditya .cNo ratings yet

- Paper7 Syl22 Dec23 Set1Document6 pagesPaper7 Syl22 Dec23 Set1rishabhrai676No ratings yet

- Taxation MTP 1 QuestionsDocument9 pagesTaxation MTP 1 QuestionsVishal Kumar 5504No ratings yet

- Taxation - English Question 27.01.2023Document12 pagesTaxation - English Question 27.01.2023harish jangidNo ratings yet

- Test Series: November, 2021 Mock Test Paper 2 Final (New) Course: Group - Ii Paper - 7: Direct Tax Laws and International TaxaxtionDocument9 pagesTest Series: November, 2021 Mock Test Paper 2 Final (New) Course: Group - Ii Paper - 7: Direct Tax Laws and International TaxaxtionPriyanshu TomarNo ratings yet

- CA Inter N22 - Tax Model QPDocument14 pagesCA Inter N22 - Tax Model QPNAVEEN SURYA MNo ratings yet

- Part - I (MCQS) All Mcqs Are Compulsory: Permission Is Punishable OffenceDocument12 pagesPart - I (MCQS) All Mcqs Are Compulsory: Permission Is Punishable OffenceShashwat SharmaNo ratings yet

- IncomeTax-IIDocument7 pagesIncomeTax-IIAditya .cNo ratings yet

- Test Series: October, 2020 Mock Test Paper Final (Old) Course: Group - Ii Paper - 7: Direct Tax LawsDocument11 pagesTest Series: October, 2020 Mock Test Paper Final (Old) Course: Group - Ii Paper - 7: Direct Tax LawsAnshul JainNo ratings yet

- Final DT 30 QPDocument6 pagesFinal DT 30 QPshivam chaturvediNo ratings yet

- UntitledDocument158 pagesUntitledSakshi KhandelwalNo ratings yet

- CA Inter Taxation Q MTP 1 May 2024 Castudynotes ComDocument15 pagesCA Inter Taxation Q MTP 1 May 2024 Castudynotes Comraghavkanoongo3No ratings yet

- Salary - PaperDocument5 pagesSalary - PaperVenkataRajuNo ratings yet

- Time Allowed: 3 Hours Maximum Mark: 100: Executive ProgrammeDocument18 pagesTime Allowed: 3 Hours Maximum Mark: 100: Executive ProgrammeDevendra AryaNo ratings yet

- Inp 2234 Tax Question PaperDocument11 pagesInp 2234 Tax Question PaperAnshit BahediaNo ratings yet

- Bcom TaxDocument6 pagesBcom TaxAditya .cNo ratings yet

- Bos 59265Document46 pagesBos 59265oproducts96No ratings yet

- Taxation - QuestionsDocument11 pagesTaxation - QuestionsaaaNo ratings yet

- Question Test Paper 2 - NOV 2023Document2 pagesQuestion Test Paper 2 - NOV 2023ABCXYZNo ratings yet

- Adobe Scan 09 Nov 2023Document11 pagesAdobe Scan 09 Nov 2023Sanskruti BarikNo ratings yet

- Term Test 1Document5 pagesTerm Test 1lalshahbaz57No ratings yet

- Sa 2 DT NovDocument9 pagesSa 2 DT NovRishabh GargNo ratings yet

- Test Series: October, 2019 Mock Test Paper 1 Final (New) Course: Group - Ii Paper - 7: Direct Tax Laws and International TaxaxtionDocument12 pagesTest Series: October, 2019 Mock Test Paper 1 Final (New) Course: Group - Ii Paper - 7: Direct Tax Laws and International TaxaxtionANIL JARWALNo ratings yet

- MTP 17 50 Questions 1709941063Document15 pagesMTP 17 50 Questions 1709941063Naveen R HegadeNo ratings yet

- Direct Tax-IDocument21 pagesDirect Tax-Ivivek rajakNo ratings yet

- Test Series - Set 5 - Ay 20-21Document16 pagesTest Series - Set 5 - Ay 20-21Urusi TeklaNo ratings yet

- 64561bos260421 Inter p4Document10 pages64561bos260421 Inter p4GowriNo ratings yet

- MTP Taxation Question Paper 2Document12 pagesMTP Taxation Question Paper 2CursedAfNo ratings yet

- DT Smart WorkDocument15 pagesDT Smart WorkmaacmampadNo ratings yet

- Cim 8682 Taxation Question Paper (Ahemadabad)Document3 pagesCim 8682 Taxation Question Paper (Ahemadabad)Pomi ShiyaNo ratings yet

- CA Final DT Q MTP 2 Nov23 Castudynotes ComDocument10 pagesCA Final DT Q MTP 2 Nov23 Castudynotes ComRajdeep GuptaNo ratings yet

- Ca-Inter Nov.'21 Batch Test of Taxation Topic Covered: PGBPDocument5 pagesCa-Inter Nov.'21 Batch Test of Taxation Topic Covered: PGBPshettymihir9No ratings yet

- MBA193F3: RamaiahDocument4 pagesMBA193F3: Ramaiahvijay shetNo ratings yet

- Paper7 Syl22 Dec23 Set1Document6 pagesPaper7 Syl22 Dec23 Set1Akash AgarwalNo ratings yet

- Paper 4: Taxation Section A: Income Tax Law: Questions and AnswersDocument24 pagesPaper 4: Taxation Section A: Income Tax Law: Questions and AnswersShivani KumariNo ratings yet

- May 23 Tax RTPDocument24 pagesMay 23 Tax RTPShailjaNo ratings yet

- Caf-01 Far-I (Mah SS)Document4 pagesCaf-01 Far-I (Mah SS)Abdullah SaberNo ratings yet

- CA Inter Tax Q MTP 2 May 2024 Castudynotes ComDocument13 pagesCA Inter Tax Q MTP 2 May 2024 Castudynotes ComineffableadityisticNo ratings yet

- Income Tax Law and PracticeDocument4 pagesIncome Tax Law and PracticeShruthi VijayanNo ratings yet

- Test Series: May, 2020 Mock Test Paper 1 Final (Old) Course: Group - Ii Paper - 7: Direct Tax LawsDocument10 pagesTest Series: May, 2020 Mock Test Paper 1 Final (Old) Course: Group - Ii Paper - 7: Direct Tax LawsAnshul JainNo ratings yet

- TaxationDocument24 pagesTaxation1088Anushka SharmaNo ratings yet

- MTP 2 AccountsDocument8 pagesMTP 2 AccountssuzalaggarwalllNo ratings yet

- Income Tax IISep Oct 2022Document15 pagesIncome Tax IISep Oct 2022supritha724No ratings yet

- Adobe Scan Jun 05, 2023Document1 pageAdobe Scan Jun 05, 2023Alok MishraNo ratings yet

- Unacademy TestDocument1 pageUnacademy TestAlok MishraNo ratings yet

- Speed TestDocument11 pagesSpeed TestAlok MishraNo ratings yet

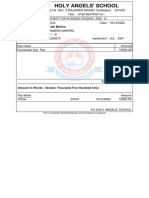

- Fee Receipt For Academic Session: 2020 - 21: Total Rs. 16500.00 Amount in Words: Sixteen Thousand Five Hundred OnlyDocument1 pageFee Receipt For Academic Session: 2020 - 21: Total Rs. 16500.00 Amount in Words: Sixteen Thousand Five Hundred OnlyAlok MishraNo ratings yet

- English 2 ProjectDocument1 pageEnglish 2 ProjectAlok MishraNo ratings yet

- 216 98 The Complete Sentence CDocument5 pages216 98 The Complete Sentence CAlok MishraNo ratings yet

- Projectwork Class XiiDocument2 pagesProjectwork Class XiiBarnali DuttaNo ratings yet

- Counting Your Way To The Sum of Squares Formula: Shailesh A ShiraliDocument13 pagesCounting Your Way To The Sum of Squares Formula: Shailesh A ShiraliAlok MishraNo ratings yet

- Commerce ProjectDocument2 pagesCommerce ProjectAlok MishraNo ratings yet

- Sector Overview: Michael GroosmanDocument17 pagesSector Overview: Michael GroosmanAlok MishraNo ratings yet

- Chapter 15 - Gender Inequality - Norton AugustDocument40 pagesChapter 15 - Gender Inequality - Norton AugustAlok MishraNo ratings yet

- Booking Confirmation On IRCTC, Train: 02225, 14-Nov-2021, 2S, AMH - GZBDocument1 pageBooking Confirmation On IRCTC, Train: 02225, 14-Nov-2021, 2S, AMH - GZBAlok MishraNo ratings yet

- Admission Notice For The Academic Year 2020-21: Post Graduate ProgramsDocument6 pagesAdmission Notice For The Academic Year 2020-21: Post Graduate ProgramsAlok MishraNo ratings yet

- English Grammer Assignment 1Document10 pagesEnglish Grammer Assignment 1Alok MishraNo ratings yet

- English: Unit Test-1 Half YearlyDocument27 pagesEnglish: Unit Test-1 Half YearlyAshwani SharmaNo ratings yet

- ch15 Non-Current LiabilitiesDocument66 pagesch15 Non-Current LiabilitiesDesain KPPN KPHNo ratings yet

- Case Studies EdM404 - TecsonNoesonB.Document15 pagesCase Studies EdM404 - TecsonNoesonB.Noeson TecsonNo ratings yet

- Ketan MehtaDocument5 pagesKetan Mehtasourabh100ravNo ratings yet

- BSTX Reviewer (Midterm)Document7 pagesBSTX Reviewer (Midterm)alaine daphneNo ratings yet

- Needs VS WantsDocument2 pagesNeeds VS WantsMhie RelatorNo ratings yet

- CH 07Document11 pagesCH 07Bhabuk AryalNo ratings yet

- MGT604 Assessment 2.aDocument9 pagesMGT604 Assessment 2.aGoyal PrachiNo ratings yet

- Hayek Money by AmetranoDocument51 pagesHayek Money by AmetranoYousef abachirNo ratings yet

- Toate Subiectele Sunt Obligatorii. Se Acord Timpul Efectiv de Lucru Este de 3 OreDocument2 pagesToate Subiectele Sunt Obligatorii. Se Acord Timpul Efectiv de Lucru Este de 3 OreOliviu ArsenieNo ratings yet

- Assessment of The Perception of Farming Households On Off Farm Activities As A Livelihood Coping Strategy in Wudil Lga of Kano State, NigeriaDocument7 pagesAssessment of The Perception of Farming Households On Off Farm Activities As A Livelihood Coping Strategy in Wudil Lga of Kano State, NigeriaEditor IJTSRDNo ratings yet

- Job CircularDocument28 pagesJob CircularTimeNo ratings yet

- Quizzers On Percentage TaxationDocument10 pagesQuizzers On Percentage Taxation?????No ratings yet

- The 6 Killerapps-NotesDocument6 pagesThe 6 Killerapps-NotesKashifOfflineNo ratings yet

- Famii KarooraDocument9 pagesFamii KarooraIbsa MohammedNo ratings yet

- Form-Loan Express March 2015 PDFDocument3 pagesForm-Loan Express March 2015 PDFJesse Carredo0% (1)

- Compilation of Raw Data - LBOBGDT Group 9Document165 pagesCompilation of Raw Data - LBOBGDT Group 9Romm SamsonNo ratings yet

- Letter of CreditDocument3 pagesLetter of CreditNikita GadeNo ratings yet

- Economic Perspectives On CSRDocument34 pagesEconomic Perspectives On CSRPinkz JanabanNo ratings yet

- Ch17 WagePayDocument14 pagesCh17 WagePaydaNo ratings yet

- Volkswagen Group LogisticsDocument17 pagesVolkswagen Group LogisticsVIPUL TUTEJA100% (1)

- Asisgn. 1 Mod 2 - NCA HELD FOR SALE & DISCONTINUED OPNS.Document5 pagesAsisgn. 1 Mod 2 - NCA HELD FOR SALE & DISCONTINUED OPNS.Kristine Vertucio0% (1)

- Strategic Cost ManagementDocument25 pagesStrategic Cost ManagementPriAnca GuptaNo ratings yet

- Assessment Test Week 6 (ECO 2) - Google FormsDocument3 pagesAssessment Test Week 6 (ECO 2) - Google FormsNeil Jasper CorozaNo ratings yet

- NEGOTIABLE INSTRUMENTonlyDocument97 pagesNEGOTIABLE INSTRUMENTonlyTomSeddyNo ratings yet

- Best Ichimoku Strategy For Quick ProfitsDocument32 pagesBest Ichimoku Strategy For Quick ProfitsNikilesh MekaNo ratings yet

- Managerial Accounting The Cornerstone of Business Decision Making 7Th Edition Mowen Test Bank Full Chapter PDFDocument68 pagesManagerial Accounting The Cornerstone of Business Decision Making 7Th Edition Mowen Test Bank Full Chapter PDFKennethRiosmqoz100% (11)

- PET Tender KMLFDocument47 pagesPET Tender KMLFRAMAKRISHNANNo ratings yet

- SUV Program BrochureDocument4 pagesSUV Program BrochurerahuNo ratings yet

- Services Marketing - Question Paper Set-2 (Semester III) PDFDocument3 pagesServices Marketing - Question Paper Set-2 (Semester III) PDFVikas SinghNo ratings yet

- Solucionario BallouDocument141 pagesSolucionario BallouJuanCarlosRodriguezNo ratings yet