You might also like

- Manual Ford Ranger Complete PDFDocument140 pagesManual Ford Ranger Complete PDFMiguel Angel Perez100% (4)

- New ISO 22519 For Water SystemsDocument2 pagesNew ISO 22519 For Water SystemsChandan Shah100% (1)

- William Cooper-Silent Weapons For Quiet WarsDocument28 pagesWilliam Cooper-Silent Weapons For Quiet WarsMihaita Rosca100% (2)

- MBA Final ProjectDocument48 pagesMBA Final Projecthuitr32No ratings yet

- Microeconomic Analysis of Pharmaceutical IndustryDocument10 pagesMicroeconomic Analysis of Pharmaceutical IndustrySayan MukherjeeNo ratings yet

- Guidance For eCTD Submission - JFDA (Jordan) PDFDocument54 pagesGuidance For eCTD Submission - JFDA (Jordan) PDFChandan Shah100% (1)

- Aurobindo Pharma Limited - 577033 - 062F202F2019 FDADocument7 pagesAurobindo Pharma Limited - 577033 - 062F202F2019 FDAChandan ShahNo ratings yet

- m16 Pitch Deck PDFDocument26 pagesm16 Pitch Deck PDFSarabjeet SinghNo ratings yet

- IR No CE-C1352 Witness to test concrete cubes (compressive strength at 7 days) for containment of pump in DS6. - ف뻵£شDocument1 pageIR No CE-C1352 Witness to test concrete cubes (compressive strength at 7 days) for containment of pump in DS6. - ف뻵£شNassim SabriNo ratings yet

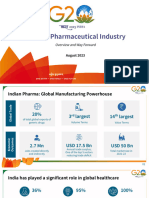

- Indian Pharmaceutical Industry Overview & Way ForwardDocument14 pagesIndian Pharmaceutical Industry Overview & Way Forwardaspinalltom243No ratings yet

- Business PPT Template High EndDocument32 pagesBusiness PPT Template High EndMandeep SinghNo ratings yet

- Financial Analysis of Pharma IndustryDocument82 pagesFinancial Analysis of Pharma IndustrySudheer Gadey100% (2)

- Trends & Opportunities For Indian PharmaDocument24 pagesTrends & Opportunities For Indian PharmaPriyesh BharadNo ratings yet

- Coronavirus Impact On India's Pharma Sector - The Economic TimesDocument2 pagesCoronavirus Impact On India's Pharma Sector - The Economic TimesDevanand DongreNo ratings yet

- Draft Policy PRIPDocument20 pagesDraft Policy PRIPSayani ChakrabortyNo ratings yet

- Pharma Sector UnderstandingDocument6 pagesPharma Sector UnderstandingSrinivas NandikantiNo ratings yet

- Pharmaceutical Industry in IndiaDocument0 pagesPharmaceutical Industry in IndiaBhuvan MalikNo ratings yet

- Financial Management Assignment Final RevDocument50 pagesFinancial Management Assignment Final RevSandesh ShettyNo ratings yet

- Global Pharma Looks To India FinalDocument40 pagesGlobal Pharma Looks To India FinalMeenakshi KhuranaNo ratings yet

- Pharmaceuticals November 2020Document35 pagesPharmaceuticals November 2020jabruNo ratings yet

- McKinsey Pharma 2020 (Highlighted Only)Document29 pagesMcKinsey Pharma 2020 (Highlighted Only)Divyansh GolyanNo ratings yet

- Final Assignment PDFDocument21 pagesFinal Assignment PDFsuruchi100% (1)

- Pharmaceuticals Indian MarketDocument33 pagesPharmaceuticals Indian MarketanshuNo ratings yet

- Marketing Strategies of Different Pharmaceutical Companies: Anil KalotraDocument8 pagesMarketing Strategies of Different Pharmaceutical Companies: Anil KalotraMokshya JaiswalNo ratings yet

- Pharma FebDocument33 pagesPharma FebHarshNo ratings yet

- Indian Pharma IndustryDocument2 pagesIndian Pharma Industrysanskarbarekar789No ratings yet

- Introduction To Pharmaceuticals SectorDocument15 pagesIntroduction To Pharmaceuticals Sectorshadwal naikNo ratings yet

- A Study On Digital Transformation and Its Effectiveness at Pfizer OrganizationDocument11 pagesA Study On Digital Transformation and Its Effectiveness at Pfizer OrganizationAditya NeelNo ratings yet

- ReportDocument67 pagesReportTech NestNo ratings yet

- Pharma - Sector ReportDocument17 pagesPharma - Sector ReportRajendra BhoirNo ratings yet

- ST Report 11Document23 pagesST Report 11Niki PatelNo ratings yet

- Boosting India'S Pharmaceutical Exports: February 2022Document26 pagesBoosting India'S Pharmaceutical Exports: February 2022Akhil SharmaNo ratings yet

- Pharma Industrial AnalysisDocument31 pagesPharma Industrial AnalysisGoel VaibhavNo ratings yet

- Research - Revenue Leakage in PharmaceuticalDocument20 pagesResearch - Revenue Leakage in PharmaceuticalVenkat AgarwalNo ratings yet

- Qualitative Analysis Sun PharmaDocument6 pagesQualitative Analysis Sun Pharmassagr123No ratings yet

- EY FICCI Indian Pharma Report 2021 I Future Is NowDocument172 pagesEY FICCI Indian Pharma Report 2021 I Future Is NowJay JajooNo ratings yet

- IA Grp06Document21 pagesIA Grp06Sanjana SambanaNo ratings yet

- SWOT N PORTER 5 Forces - Indian PahrmaDocument21 pagesSWOT N PORTER 5 Forces - Indian Pahrmabhupendraa97% (35)

- Pharmaceuticals February 20201Document33 pagesPharmaceuticals February 20201whitenagarNo ratings yet

- Global Pharmaceuticals Outlook 2023Document9 pagesGlobal Pharmaceuticals Outlook 2023k60.2113340007No ratings yet

- Pharmaceutical Industry in IndiaDocument10 pagesPharmaceutical Industry in Indiaakshay_bitsNo ratings yet

- Indian Api Industry - Reaching The Full Potential: AprilDocument88 pagesIndian Api Industry - Reaching The Full Potential: AprilStevin GeorgeNo ratings yet

- A Study On The Working Capital Management of Pharmaceutical Industry (A Case Study of Cipla LTD.)Document7 pagesA Study On The Working Capital Management of Pharmaceutical Industry (A Case Study of Cipla LTD.)Harshul BansalNo ratings yet

- Pharmaceuticals September 2021Document34 pagesPharmaceuticals September 2021Daniel JosephNo ratings yet

- Indian Pharmaceutical IndustryDocument19 pagesIndian Pharmaceutical IndustryPankaj GauravNo ratings yet

- Pharma Sector: Mms FinanceDocument8 pagesPharma Sector: Mms Financejignesh143347No ratings yet

- Economics Research PaperDocument7 pagesEconomics Research PaperSunidhiNo ratings yet

- Assignment On I.T & Pharma IndustryDocument11 pagesAssignment On I.T & Pharma IndustryGolu SinghNo ratings yet

- PWC CII Pharma Summit Report 22novDocument64 pagesPWC CII Pharma Summit Report 22novManuj KhuranaNo ratings yet

- Financial Management: Digital Assignment - 2Document24 pagesFinancial Management: Digital Assignment - 2munshiNo ratings yet

- A Study On Impact of Covid - 19 On Indian Pharmaceutical CompaniesDocument9 pagesA Study On Impact of Covid - 19 On Indian Pharmaceutical CompaniesAnonymous CwJeBCAXpNo ratings yet

- Market PotentialDocument61 pagesMarket PotentialSam BhargajeNo ratings yet

- Market SizeDocument4 pagesMarket SizeUbair HamdaniNo ratings yet

- Top 10 Pharmaceutical Companies in India Benchmark Report - Competitive Analysis of The Leading Players in 2013Document21 pagesTop 10 Pharmaceutical Companies in India Benchmark Report - Competitive Analysis of The Leading Players in 2013Akshay 1313No ratings yet

- Introduction To The IndustryDocument21 pagesIntroduction To The IndustrySmeet JasoliyaNo ratings yet

- Pharmaceutical IndustryDocument18 pagesPharmaceutical IndustryKrishna PrasadNo ratings yet

- Indias Pharma SectorDocument22 pagesIndias Pharma SectorAman AgarwalNo ratings yet

- Impact of Make in India Concept-To Face Issues & Challenges in Pharmaceutical Industries ProductivityDocument12 pagesImpact of Make in India Concept-To Face Issues & Challenges in Pharmaceutical Industries ProductivityMunni ChukkaNo ratings yet

- General Profile of The CompanyDocument25 pagesGeneral Profile of The Companyapi-235704876No ratings yet

- Pharmaceuticals September 2020 - IBEFDocument35 pagesPharmaceuticals September 2020 - IBEFGarvita100% (1)

- Sales Final Report CIA 3ADocument37 pagesSales Final Report CIA 3ATRISHNA BHARALI 2128055No ratings yet

- Indian Life SciencesDocument3 pagesIndian Life Sciencesmukesh516No ratings yet

- RBSA Indian PharmaDocument19 pagesRBSA Indian PharmaCorey HuntNo ratings yet

- COVID-19 Impact On Pharmaceuticals SectorDocument6 pagesCOVID-19 Impact On Pharmaceuticals SectorBhargav KumarNo ratings yet

- Model Answer: E-Commerce store launch by Unilever in Sri LankaFrom EverandModel Answer: E-Commerce store launch by Unilever in Sri LankaNo ratings yet

- A New Dawn for Global Value Chain Participation in the PhilippinesFrom EverandA New Dawn for Global Value Chain Participation in the PhilippinesNo ratings yet

- Control of LabelsDocument1 pageControl of LabelsChandan ShahNo ratings yet

- Arvind Resume QADocument3 pagesArvind Resume QAChandan ShahNo ratings yet

- Fe96beed 7a5b 4d7b A5cc C38eecd2b38dDocument1 pageFe96beed 7a5b 4d7b A5cc C38eecd2b38dChandan ShahNo ratings yet

- GuidelinesDocument8 pagesGuidelinesChandan ShahNo ratings yet

- Capa ToolsDocument44 pagesCapa ToolsChandan ShahNo ratings yet

- US FDA 483 - Dr. Reddy's Laboratories Ltd. Unit IIDocument5 pagesUS FDA 483 - Dr. Reddy's Laboratories Ltd. Unit IIChandan ShahNo ratings yet

- "Evolving Critical Documents - Part 3": Session - 5Document29 pages"Evolving Critical Documents - Part 3": Session - 5Chandan ShahNo ratings yet

- 2 2 PPT Managing Oracle InstanceDocument43 pages2 2 PPT Managing Oracle InstancePartho Bora100% (1)

- 1LE7503 2BB03 5AA4 Datasheet enDocument1 page1LE7503 2BB03 5AA4 Datasheet enhafidz.maxonNo ratings yet

- AVS 370 CatalogDocument8 pagesAVS 370 CatalogMohammed OuikhalfanNo ratings yet

- (Questions Only) ME 366 ONLINE REGULAR QUIZ 4 2022 - 2023Document16 pages(Questions Only) ME 366 ONLINE REGULAR QUIZ 4 2022 - 2023somenewguyonthewebNo ratings yet

- Mann Automotive Filter Stock List19052021Document3 pagesMann Automotive Filter Stock List19052021B Sathish BabuNo ratings yet

- Renault ClioDocument2 pagesRenault ClioGeorgian Cranta100% (1)

- 4 ATA 61 PropellerDocument36 pages4 ATA 61 Propellermoabduk1990No ratings yet

- RoBA MultiplierDocument3 pagesRoBA Multipliersai krishna boyapati100% (1)

- ABB VT Outdoor ManualDocument2 pagesABB VT Outdoor ManualSekarNo ratings yet

- XPathDocument50 pagesXPathchhetribharat08No ratings yet

- HVAC & Cooling Towers PDFDocument74 pagesHVAC & Cooling Towers PDFSanket Phatangare0% (1)

- Report 1base Paper On STANDARDIZATION AND INDIGENISATION PDFDocument59 pagesReport 1base Paper On STANDARDIZATION AND INDIGENISATION PDFAjit PatilNo ratings yet

- Technical Data Sheets: Page 1 of 19 210372 Proj. No.: Customer: Proj. Name: 13Document19 pagesTechnical Data Sheets: Page 1 of 19 210372 Proj. No.: Customer: Proj. Name: 13samirNo ratings yet

- Chemical Industry PDFDocument20 pagesChemical Industry PDFJose PriceNo ratings yet

- Unit Iv OcnDocument39 pagesUnit Iv OcnGunasekaran PNo ratings yet

- Self-Cleaning Filter Structur e and PrincipleDocument40 pagesSelf-Cleaning Filter Structur e and PrincipleZ EHNo ratings yet

- PTISDocument7 pagesPTISAdited MlnNo ratings yet

- TU Adv Trans Play Distance Example ENUDocument20 pagesTU Adv Trans Play Distance Example ENULuis FernandoNo ratings yet

- BK 2831D Service ManualDocument26 pagesBK 2831D Service ManualtodorloncarskiNo ratings yet

- Lesson Plan Level 4 TemplateDocument5 pagesLesson Plan Level 4 Templateapi-252213738No ratings yet

- BCMSB Final Poster PresentationDocument1 pageBCMSB Final Poster PresentationQuentin LeitzNo ratings yet

- Designing Effective Powerpoint Presentations: Victor Chen ErauDocument52 pagesDesigning Effective Powerpoint Presentations: Victor Chen ErauEka SubyantaraNo ratings yet

- Driving Management Excellence: Oracle's Enterprise Performance Management SystemDocument12 pagesDriving Management Excellence: Oracle's Enterprise Performance Management SystemganpaNo ratings yet

- Roof Top TowersDocument5 pagesRoof Top TowersYasir JamiNo ratings yet

- 8 To 1Document8 pages8 To 1Andrey Mary RanolaNo ratings yet

- 7 9 13eDocument2 pages7 9 13eprincemmtclNo ratings yet