You might also like

- M20titman254431811finmgtc20 141001085633 Phpapp01Document100 pagesM20titman254431811finmgtc20 141001085633 Phpapp01Cate MasilunganNo ratings yet

- Financial Markets & Risk ManagementDocument48 pagesFinancial Markets & Risk ManagementGabriel Alva AnkrahNo ratings yet

- Nocco Enterprise Risk Management Theory and PracticeDocument33 pagesNocco Enterprise Risk Management Theory and PracticeMichael RitterNo ratings yet

- Investments, Risks and Rates of ReturnsDocument60 pagesInvestments, Risks and Rates of ReturnsJade Berlyn AgcaoiliNo ratings yet

- Chapter 4Document28 pagesChapter 4Diaz CharlotteNo ratings yet

- Part Seven: The Management of Financial InstitutionsDocument39 pagesPart Seven: The Management of Financial InstitutionsManpreet Kaur SekhonNo ratings yet

- Financial Risk ManagementDocument18 pagesFinancial Risk Managementdwimukh360No ratings yet

- CHP 10Document50 pagesCHP 10SUBA NANTINI A/P M.SUBRAMANIAMNo ratings yet

- Financial ManagementDocument21 pagesFinancial ManagementsumanNo ratings yet

- Financial and Business Risk Management 1 PDFDocument75 pagesFinancial and Business Risk Management 1 PDFrochelleandgelloNo ratings yet

- FIN701 Finance AS1744Document17 pagesFIN701 Finance AS1744anurag soniNo ratings yet

- Yyy Yy Yy Y Y Yyy Yyyy Yy Y Y Yyy Yy Y Yyy Y Yyyyyy Yy Y Yycosts of Financial DistressyDocument22 pagesYyy Yy Yy Y Y Yyy Yyyy Yy Y Y Yyy Yy Y Yyy Y Yyyyyy Yy Y Yycosts of Financial DistressyPooja SahooNo ratings yet

- Chapter OneDocument8 pagesChapter OnefdsfsfNo ratings yet

- Corporate Risk ManagementDocument6 pagesCorporate Risk ManagementViral DesaiNo ratings yet

- Enterprise Risk ManagementDocument16 pagesEnterprise Risk ManagementSahil Nagpal100% (1)

- A2b. Gearing ConsiderationsDocument3 pagesA2b. Gearing ConsiderationsVrinda ForbesNo ratings yet

- FINMANDocument29 pagesFINMANViney VillasorNo ratings yet

- BP Amoco CaseDocument37 pagesBP Amoco CaseIlayaraja DhatchinamoorthyNo ratings yet

- Treasury and Risk Management: IntroductionDocument7 pagesTreasury and Risk Management: Introductionmaster of finance and controlNo ratings yet

- Enterprise Risk Management: Theory and Practice: How Does ERM Create Shareholder Value?Document13 pagesEnterprise Risk Management: Theory and Practice: How Does ERM Create Shareholder Value?Pablo Velázquez MéndezNo ratings yet

- Risk Management TermsDocument4 pagesRisk Management TermsJianne Jaycee BorlonganNo ratings yet

- FE Case StudyDocument4 pagesFE Case StudyMohammad Sameer AnsariNo ratings yet

- Financial ManagementDocument11 pagesFinancial ManagementLavesh DixitNo ratings yet

- Unit 6 Foreign Exchange Exposure: Sanjay Ghimire Tu-SomDocument68 pagesUnit 6 Foreign Exchange Exposure: Sanjay Ghimire Tu-SomMotiram paudelNo ratings yet

- 1-2.risk Management IntroductionDocument39 pages1-2.risk Management IntroductionAmitNo ratings yet

- Bench MarkingDocument14 pagesBench MarkingVenkatakrishnan IyerNo ratings yet

- Strategic RiskDocument18 pagesStrategic RiskJonisha JonesNo ratings yet

- Capital Structure Issues: V. VI. V.1 Mergers and Acquisitions Definition and DifferencesDocument26 pagesCapital Structure Issues: V. VI. V.1 Mergers and Acquisitions Definition and Differenceskelvin pogiNo ratings yet

- T1-FRM-2-Ch2-503-20.4-v3 - Practice QuestionsDocument10 pagesT1-FRM-2-Ch2-503-20.4-v3 - Practice QuestionscristianoNo ratings yet

- Answer Key Answer Key: Bansw 1 1 October 2014 5:37 PMDocument40 pagesAnswer Key Answer Key: Bansw 1 1 October 2014 5:37 PMCharbelSaadéNo ratings yet

- 3 - Risk Management and Internal Control System RevisedDocument61 pages3 - Risk Management and Internal Control System RevisedRica RegorisNo ratings yet

- Seminar Report ON Corporate Hedging Process & Techniques Submitted To: Sir. Yasin Zia Submitted By: Zahid Hussain 2009-Ag-65 MBA (R) FinanceDocument12 pagesSeminar Report ON Corporate Hedging Process & Techniques Submitted To: Sir. Yasin Zia Submitted By: Zahid Hussain 2009-Ag-65 MBA (R) FinanceZahid HussainNo ratings yet

- AFM Jan 2024 Tute 5 Risk ManagementDocument9 pagesAFM Jan 2024 Tute 5 Risk Managementpersis.benjamin01No ratings yet

- Lecture-3.2.1 Risk ManagementDocument23 pagesLecture-3.2.1 Risk Managementgsingla802No ratings yet

- What Is Financial Engineering?Document4 pagesWhat Is Financial Engineering?Chandini AllaNo ratings yet

- Introduction To FRMDocument28 pagesIntroduction To FRMThiên HànNo ratings yet

- An Overview of Financial ManagementDocument14 pagesAn Overview of Financial ManagementMariz Julian Pang-aoNo ratings yet

- RAP EMA TemplateDocument8 pagesRAP EMA TemplateShruti GoelNo ratings yet

- Financial Management - Chapter 01Document26 pagesFinancial Management - Chapter 01Joe HizulNo ratings yet

- LN10 EitemanDocument35 pagesLN10 EitemanFong 99No ratings yet

- Assignment: Prepared ByDocument12 pagesAssignment: Prepared ByShamin ArackelNo ratings yet

- Financial Management RiskDocument11 pagesFinancial Management RisknevadNo ratings yet

- Financial Management Chapter OneDocument22 pagesFinancial Management Chapter Onebiko ademNo ratings yet

- Risk Identification Can Be Done byDocument3 pagesRisk Identification Can Be Done bytekalign shalamoNo ratings yet

- Risk Management Solution Manual Chapter 04Document5 pagesRisk Management Solution Manual Chapter 04DanielLam75% (4)

- The Role of Managerial Finance: All Rights ReservedDocument45 pagesThe Role of Managerial Finance: All Rights ReservedRemi SabirNo ratings yet

- 15.997 Practice of Finance: Advanced Corporate Risk ManagementDocument21 pages15.997 Practice of Finance: Advanced Corporate Risk Managementcjsb99No ratings yet

- Chapter 1 - Introduction To Finance: FIN2102 - Financial ManagementDocument21 pagesChapter 1 - Introduction To Finance: FIN2102 - Financial ManagementsatingNo ratings yet

- Why Managa RiskDocument16 pagesWhy Managa RiskMichStevenNo ratings yet

- Special Topics in Financial Management ReviewerDocument4 pagesSpecial Topics in Financial Management ReviewerJoelan AbdulaNo ratings yet

- #02 - The Need For Risk ManagementDocument23 pages#02 - The Need For Risk ManagementLouis BarbierNo ratings yet

- Chapter 14Document9 pagesChapter 14Kimberly LimNo ratings yet

- Alternative Risk TRF e 02Document5 pagesAlternative Risk TRF e 02Vladi B PMNo ratings yet

- Risk ManagementDocument34 pagesRisk ManagementMarky AlmueteNo ratings yet

- Chapter 1 - Version1Document31 pagesChapter 1 - Version1Oktariadie RamadhianNo ratings yet

- FIN 319 - Lecture 06Document30 pagesFIN 319 - Lecture 06Trà MyNo ratings yet

- Strategic Financial Management: Syllabus and IntroductionDocument15 pagesStrategic Financial Management: Syllabus and IntroductionFaizan AnisNo ratings yet

- Board Perspectives On Risk OversightDocument4 pagesBoard Perspectives On Risk OversightJulieNo ratings yet

- GBERMICDocument34 pagesGBERMIC12abm.dinglasandymphnaNo ratings yet

- COBECON Exercise2Document4 pagesCOBECON Exercise2ANo ratings yet

- Worksheet On Symbolic Logic and Consumer MathematicsDocument4 pagesWorksheet On Symbolic Logic and Consumer MathematicsANo ratings yet

- COBECON Exercise1Document6 pagesCOBECON Exercise1ANo ratings yet

- CL WomenGenderPoorDocument1 pageCL WomenGenderPoorANo ratings yet

- DSILYTC Group5 PS5SolutionsDocument7 pagesDSILYTC Group5 PS5SolutionsANo ratings yet

- Advocacy Plan Template: Center For Social Concern and ActionDocument2 pagesAdvocacy Plan Template: Center For Social Concern and ActionANo ratings yet

- STATPRO FINAL PAPERDocument14 pagesSTATPRO FINAL PAPERANo ratings yet

- ACCOB1 EthicsReflectionDocument1 pageACCOB1 EthicsReflectionANo ratings yet

- Li Vs PeopleDocument1 pageLi Vs Peopledjango69No ratings yet

- Dissertation Topic MailDocument57 pagesDissertation Topic MailJothsna ChikkodiNo ratings yet

- Staff Travel PolicyDocument22 pagesStaff Travel PolicyКумуду АрамбевалаNo ratings yet

- All Aluminum Conductor AAC: ApplicationDocument1 pageAll Aluminum Conductor AAC: ApplicationAnonymous 2eA5kc7MWfNo ratings yet

- Course in Real Analysis 1st Junghenn Solution ManualDocument38 pagesCourse in Real Analysis 1st Junghenn Solution Manualmitchellunderwooda4p4d100% (15)

- Business Intelligence GuidebookDocument50 pagesBusiness Intelligence GuidebookElsaNo ratings yet

- Correspondence Between My Friend, The Late Gordon T. "Gordy" Pratt, and Chicago Tribune Reporter Lisa Black and Editor Peter Hernon (Sept/Oct 2009)Document8 pagesCorrespondence Between My Friend, The Late Gordon T. "Gordy" Pratt, and Chicago Tribune Reporter Lisa Black and Editor Peter Hernon (Sept/Oct 2009)Peter M. HeimlichNo ratings yet

- Prosec ResolDocument4 pagesProsec ResolMary Anne Guanzon VitugNo ratings yet

- Accounting at Biovail ReportDocument7 pagesAccounting at Biovail ReportimeldafebrinatNo ratings yet

- Southern National Bank of North Carolina v. Federal Resources Corporation Kenyon Home Furnishings, LTD., and James W. Pearce Elizabeth Contogiannis Steve Palinkas, 911 F.2d 724, 4th Cir. (1990)Document6 pagesSouthern National Bank of North Carolina v. Federal Resources Corporation Kenyon Home Furnishings, LTD., and James W. Pearce Elizabeth Contogiannis Steve Palinkas, 911 F.2d 724, 4th Cir. (1990)Scribd Government DocsNo ratings yet

- 67Document42 pages67Rick DasNo ratings yet

- Module 2Document6 pagesModule 2MonicaMartirosyanNo ratings yet

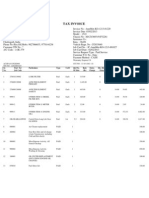

- Tax Invoice: Warranty Expired:NDocument3 pagesTax Invoice: Warranty Expired:NSanjay PatelNo ratings yet

- Original For Recipient: Order Number: RDF15750659Document2 pagesOriginal For Recipient: Order Number: RDF15750659Rajat DawraNo ratings yet

- Uthman Ibn AffanDocument44 pagesUthman Ibn Affanguest_7314No ratings yet

- ST Mary's Academy Vs CarpitanosDocument1 pageST Mary's Academy Vs CarpitanosJune Steve Barredo100% (1)

- Enumerator'S Manual Household Profile Questionnaire (Version Number: 10201301)Document102 pagesEnumerator'S Manual Household Profile Questionnaire (Version Number: 10201301)Mark Vincent LeonesNo ratings yet

- Gospel Humiliation: Ralph Erskine (1685-1752)Document16 pagesGospel Humiliation: Ralph Erskine (1685-1752)Nick_MaNo ratings yet

- Worksheet 3-4 P. 2Document1 pageWorksheet 3-4 P. 2briandmcneillNo ratings yet

- CHENG V GENATODocument2 pagesCHENG V GENATOLaurena ReblandoNo ratings yet

- Rajiv Gandhi National University of Law, PunjabDocument2 pagesRajiv Gandhi National University of Law, PunjabShubham PandeyNo ratings yet

- Palma v. OmelioDocument12 pagesPalma v. OmelioMac SorianoNo ratings yet

- Sant Longowal Institute of Engineering and Technology: Print FormDocument1 pageSant Longowal Institute of Engineering and Technology: Print FormVikash KumarNo ratings yet

- 6.2 Labour Law IIDocument6 pages6.2 Labour Law IIDevvrat garhwalNo ratings yet

- VOL. 12, SEPTEMBER 28, 1964 19: Tady-Y vs. Philippine National BankDocument6 pagesVOL. 12, SEPTEMBER 28, 1964 19: Tady-Y vs. Philippine National BankKris OrenseNo ratings yet

- Geroche Vs People GR No. 179080, November 26, 2014Document6 pagesGeroche Vs People GR No. 179080, November 26, 2014salinpusaNo ratings yet

- Possession FruitsDocument1 pagePossession FruitsJoedhel ApostolNo ratings yet

- Contigent Bill: Code No. Amount Datail of Sub VoucherDocument2 pagesContigent Bill: Code No. Amount Datail of Sub Voucherhyderi photostateNo ratings yet

- Moneymax X Citibank GCash Exclusive Campaign T&CsDocument3 pagesMoneymax X Citibank GCash Exclusive Campaign T&CsProsserfina MinaoNo ratings yet

- F.miklosich - Chronica NestorisDocument258 pagesF.miklosich - Chronica NestorisДжу ХоNo ratings yet