You might also like

- Change Your LifeDocument51 pagesChange Your LifefeevaNo ratings yet

- Cart Eliza Ti OnDocument48 pagesCart Eliza Ti OnGreg PassmoreNo ratings yet

- Ending The Federal ReserveDocument5 pagesEnding The Federal Reserveapi-252760654No ratings yet

- Chesterton Arthur Kenneth Menace of The Money PowerDocument19 pagesChesterton Arthur Kenneth Menace of The Money PowerbandrigNo ratings yet

- Why Banke... R Westley - Mises DailyDocument3 pagesWhy Banke... R Westley - Mises DailysilberksouzaNo ratings yet

- Did You KnowDocument18 pagesDid You KnowAnon Mus100% (1)

- IMF's Epic Plan To Conjure Away Debt and Dethrone BankersDocument5 pagesIMF's Epic Plan To Conjure Away Debt and Dethrone Bankersmonetary-policy-reduxNo ratings yet

- Economics PPT: Group MembersDocument6 pagesEconomics PPT: Group MembersAhmarNo ratings yet

- BWABanking On NeverDocument7 pagesBWABanking On Neverrhawk301No ratings yet

- The History of Money and Banking in the United StatesDocument27 pagesThe History of Money and Banking in the United Statesjaime.bvr7416100% (1)

- A Brief History of UDocument7 pagesA Brief History of UyowNo ratings yet

- 2020-07-20 The US Banking System-Origin, Development, and RegulationDocument6 pages2020-07-20 The US Banking System-Origin, Development, and RegulationD. BushNo ratings yet

- Evoltion of BankDocument8 pagesEvoltion of BankDanny NetkarNo ratings yet

- Smashing the Axis of Financial FraudDocument9 pagesSmashing the Axis of Financial FraudgkeraunenNo ratings yet

- Final Banking Law OutlineDocument95 pagesFinal Banking Law OutlineQuinton JohnsonNo ratings yet

- Evolution of Banking FinalDocument7 pagesEvolution of Banking FinalDouglasNo ratings yet

- Money MastersDocument108 pagesMoney Mastersapanisile14142100% (1)

- The Money ChangersDocument37 pagesThe Money Changerspaliacho77No ratings yet

- Banking in The United States: HistoryDocument5 pagesBanking in The United States: Historysen6aNo ratings yet

- Discharge of Public Debts 2Document39 pagesDischarge of Public Debts 2CK in DC100% (16)

- Avoiding The Next CrisisDocument12 pagesAvoiding The Next CrisisChe VasNo ratings yet

- Ank Otes: Confusing Capitalism With Fractional Reserve BankingDocument11 pagesAnk Otes: Confusing Capitalism With Fractional Reserve BankingMichael HeidbrinkNo ratings yet

- Dr. John Drabik - Money System, Private or PublicDocument2 pagesDr. John Drabik - Money System, Private or PublicGabrielNo ratings yet

- Jackson vs Biddle: The Demise of the Second Bank of the United StatesDocument23 pagesJackson vs Biddle: The Demise of the Second Bank of the United Statesalan orlandoNo ratings yet

- How Canada's Banking System Avoided Financial CrisesDocument8 pagesHow Canada's Banking System Avoided Financial CrisesLore del CastilloNo ratings yet

- Hammond 1947 - Jackson, Biddle, and The Bank of The United StatesDocument24 pagesHammond 1947 - Jackson, Biddle, and The Bank of The United StatesinsightsxNo ratings yet

- Federal Reserve SystemDocument28 pagesFederal Reserve SystemJonathan Yrrizarri100% (2)

- THE BANKRUPTCY OF THE U.S.A. - by James Traficant, Jr. (Speaker-Republican-Ohio)Document7 pagesTHE BANKRUPTCY OF THE U.S.A. - by James Traficant, Jr. (Speaker-Republican-Ohio)extemporaneous100% (3)

- U.S. Money vs. Corporation Currency, "Aldrich Plan.": Wall Street Confessions! Great Bank CombineFrom EverandU.S. Money vs. Corporation Currency, "Aldrich Plan.": Wall Street Confessions! Great Bank CombineNo ratings yet

- The Hazzard Circular: Benjamin S. HeathDocument21 pagesThe Hazzard Circular: Benjamin S. HeathKarel DonkNo ratings yet

- America's Debt-Based Money SystemDocument14 pagesAmerica's Debt-Based Money SystemMaritza GomezNo ratings yet

- Summary: I.O.U.: Review and Analysis of John Lanchester's BookFrom EverandSummary: I.O.U.: Review and Analysis of John Lanchester's BookNo ratings yet

- The Federal Reserve System: Its Purposes and Functions 1939Document33 pagesThe Federal Reserve System: Its Purposes and Functions 1939Trey Sells100% (1)

- Banking QuotesDocument2 pagesBanking QuotesManwisesonNo ratings yet

- Insiders Power December 2015Document41 pagesInsiders Power December 2015InterAnalyst, LLCNo ratings yet

- 378 - Universal Debt Forgiveness and The Imminent Global Debt JubileeDocument2 pages378 - Universal Debt Forgiveness and The Imminent Global Debt JubileeDavid E Robinson100% (2)

- Rev 4 BenDocument5 pagesRev 4 Benapi-317092002No ratings yet

- Federal Reserve ScamDocument31 pagesFederal Reserve ScamSarah Willer100% (4)

- Great Depression Research Paper FinalDocument5 pagesGreat Depression Research Paper FinalmikeNo ratings yet

- JFK EO 11110 and The FedDocument7 pagesJFK EO 11110 and The FedGuy Razer100% (3)

- The Money ChangersDocument27 pagesThe Money Changersanon-881710100% (14)

- Congressman Mcfadden On The Federal Reserve Corporation Remarks in Congress, 1934 An Astounding ExposureDocument22 pagesCongressman Mcfadden On The Federal Reserve Corporation Remarks in Congress, 1934 An Astounding ExposureJason HenryNo ratings yet

- The Economic IssuesDocument9 pagesThe Economic IssuesArya MuraliNo ratings yet

- Dont Cry For Me Argent in ADocument12 pagesDont Cry For Me Argent in AhwaagNo ratings yet

- The Bailout's New Financial OligarchyDocument17 pagesThe Bailout's New Financial OligarchyvanathelNo ratings yet

- Debtor Nation: The History of America in Red InkFrom EverandDebtor Nation: The History of America in Red InkRating: 5 out of 5 stars5/5 (1)

- Thoughts On The Federal ReserveDocument4 pagesThoughts On The Federal Reservelemieuxm327No ratings yet

- National Banknotes As High-Powered MoneyDocument43 pagesNational Banknotes As High-Powered MoneyGeorge SelginNo ratings yet

- Ellen Brown 20012023Document6 pagesEllen Brown 20012023Thuan TrinhNo ratings yet

- The Federal Reserve and Sound Money: National Center For Policy AnalysisDocument4 pagesThe Federal Reserve and Sound Money: National Center For Policy Analysisrichardck61No ratings yet

- Congressman, Louis T. McFadden's RemarksDocument35 pagesCongressman, Louis T. McFadden's RemarksSUPPRESS THIS100% (1)

- Money Management EssentialsDocument6 pagesMoney Management EssentialsTài Chính Nhất ViệtNo ratings yet

- Jurnal tentang ekonomi kreatif di indonesiaDocument16 pagesJurnal tentang ekonomi kreatif di indonesiazahra anisah putriNo ratings yet

- Where Does Money Come From?Document10 pagesWhere Does Money Come From?monetary-policy-redux100% (4)

- The Great Global Debt PrisonDocument4 pagesThe Great Global Debt Prisonjas2maui100% (1)

- The Bankruptcy of The United StatesDocument8 pagesThe Bankruptcy of The United StatesncwazzyNo ratings yet

- The Money Masters PDFDocument31 pagesThe Money Masters PDFvenurao1100% (6)

- Registration Form GreenfieldDocument1 pageRegistration Form GreenfieldJochebed MukandaNo ratings yet

- CharismaDocument19 pagesCharismaJochebed MukandaNo ratings yet

- Gods Word The Miracle SeedDocument101 pagesGods Word The Miracle SeedJochebed MukandaNo ratings yet

- Change Your Questions Change Your LifeDocument10 pagesChange Your Questions Change Your LifeSandeeip Mirajkar100% (1)

- About The Student: JochebedDocument11 pagesAbout The Student: JochebedJochebed MukandaNo ratings yet

- The Secrets To Charisma and Personal Magnetism - Learn A Hidden Energy Tradition To Become Magnetically Attractive and Vitally Alive (Personal Magnetism Series Book 1)Document117 pagesThe Secrets To Charisma and Personal Magnetism - Learn A Hidden Energy Tradition To Become Magnetically Attractive and Vitally Alive (Personal Magnetism Series Book 1)Hendro Santoso82% (11)

- Waco Standard - Community SpecializationDocument2 pagesWaco Standard - Community SpecializationJochebed MukandaNo ratings yet

- Future Diplomats School of Diplomacy Assignment 1Document9 pagesFuture Diplomats School of Diplomacy Assignment 1Jochebed MukandaNo ratings yet

- BeforeYouMeetYourFutureHusband SPDocument41 pagesBeforeYouMeetYourFutureHusband SPJochebed MukandaNo ratings yet

- 10 Points To Remember When Applying For A Nonimmigrant VisaDocument3 pages10 Points To Remember When Applying For A Nonimmigrant VisaJochebed MukandaNo ratings yet

- PALTOK CREDIT COOPERATIVE ACCOUNT VERIFICATIONDocument2 pagesPALTOK CREDIT COOPERATIVE ACCOUNT VERIFICATIONDaenarys VeranoNo ratings yet

- Midxix Prestige Savings FormDocument2 pagesMidxix Prestige Savings FormKartik ShuklaNo ratings yet

- Credit Creation by Commercial BanksDocument19 pagesCredit Creation by Commercial BanksSaumitra RaneNo ratings yet

- Producers Bank vs Excelsa Industries RulingDocument3 pagesProducers Bank vs Excelsa Industries Rulingangelsu04100% (1)

- Central Bank of Sri Lanka: Objectives, Functions & OrganizationDocument32 pagesCentral Bank of Sri Lanka: Objectives, Functions & OrganizationAsiri GunarathnaNo ratings yet

- MIS Ass PrabaDocument12 pagesMIS Ass PrabaPraba VettriveluNo ratings yet

- Secured Transactions and Collateral Registries A Global PerspectiveDocument36 pagesSecured Transactions and Collateral Registries A Global PerspectiveADBI EventsNo ratings yet

- Chapter 1: Mathematics of Investment: Prepared By: Francis Joseph H. CampeñaDocument31 pagesChapter 1: Mathematics of Investment: Prepared By: Francis Joseph H. CampeñaRhay Notorio100% (1)

- Meaning and Definition of Banking-Banking Can Be Defined As The Business Activity ofDocument32 pagesMeaning and Definition of Banking-Banking Can Be Defined As The Business Activity ofPunya KrishnaNo ratings yet

- Navinon Possession NoticeDocument2 pagesNavinon Possession NoticePriyanka ShembekarNo ratings yet

- Determination of Foreign Exchange Chapter 4Document20 pagesDetermination of Foreign Exchange Chapter 4Sazedul Ekab100% (1)

- The Refinancing of Shanghai General MotorsDocument23 pagesThe Refinancing of Shanghai General MotorsAdrija Chakraborty100% (2)

- "Banking Regulation Act 1969": Shreeraj HariharanDocument71 pages"Banking Regulation Act 1969": Shreeraj HariharanVi JayNo ratings yet

- Money and Financial Markets Eurekahow NotesDocument52 pagesMoney and Financial Markets Eurekahow NotesDebajyoti SamajpatiNo ratings yet

- HDFC Bank Freedom Credit CardDocument9 pagesHDFC Bank Freedom Credit CardKuldeep rajakNo ratings yet

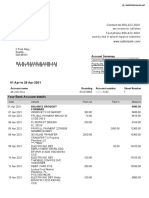

- Bank StatementDocument4 pagesBank StatementKristin BrooksNo ratings yet

- Banking Company Final Accounts: Profit, Loss, Assets, LiabilitiesDocument20 pagesBanking Company Final Accounts: Profit, Loss, Assets, LiabilitiesPaulomi LahaNo ratings yet

- Financial Accounting ProjectDocument12 pagesFinancial Accounting ProjectRishabh ManawatNo ratings yet

- StatementOfAccount 6354576294 02012024 172901Document5 pagesStatementOfAccount 6354576294 02012024 172901sugumarNo ratings yet

- LucerneDocument1 pageLucernerahul venkateshwaranNo ratings yet

- BBC Skillswise E3 Bank MachineDocument1 pageBBC Skillswise E3 Bank MachineMonica ScanlanNo ratings yet

- Dubai Islamic Bank Dubai Islamic Bank Dubai Islamic Bank Dubai Islamic BankDocument2 pagesDubai Islamic Bank Dubai Islamic Bank Dubai Islamic Bank Dubai Islamic BankKhurram MalikNo ratings yet

- Brac Bank StatementDocument1 pageBrac Bank Statementshahid2opu100% (2)

- ICICI Bank SIP Internship Report - Monitoring Marketing Funnel & Improving Customer ExperienceDocument7 pagesICICI Bank SIP Internship Report - Monitoring Marketing Funnel & Improving Customer ExperienceSoumiya BishtNo ratings yet

- Bank account details and contact infoDocument2 pagesBank account details and contact infoNadiia AvetisianNo ratings yet

- Guide Emerging Market Currencies 2010Document128 pagesGuide Emerging Market Currencies 2010ferrarilover2000No ratings yet

- Packing List: Ship-To PartyDocument7 pagesPacking List: Ship-To PartySeb EgnNo ratings yet

- Central Bank - WikipediaDocument21 pagesCentral Bank - WikipediaiazpiazuNo ratings yet

- Class 11 Accountancy Project 1 Comprehensive ProblemDocument21 pagesClass 11 Accountancy Project 1 Comprehensive ProblemSANYAM SINGHALNo ratings yet

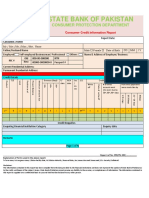

- Consumer Credit Report Format.Document3 pagesConsumer Credit Report Format.Naeem RaoNo ratings yet