You might also like

- Whistle BlowerDocument21 pagesWhistle BlowerVimal SinghNo ratings yet

- Whistleblowing and Death Penalty-Thelma R. VillanuevaDocument75 pagesWhistleblowing and Death Penalty-Thelma R. VillanuevaThelma R. VillanuevaNo ratings yet

- Whistle BlowingDocument24 pagesWhistle BlowingTati Mansur100% (4)

- Whistle Blowing Is of Two TypesDocument5 pagesWhistle Blowing Is of Two TypesmanisandhuNo ratings yet

- Doing the Right Thing Bible Study Participant's Guide: Making Moral Choices in a World Full of OptionsFrom EverandDoing the Right Thing Bible Study Participant's Guide: Making Moral Choices in a World Full of OptionsNo ratings yet

- Ethical FallaciesDocument5 pagesEthical Fallaciesst3792No ratings yet

- WhistleblowerDocument14 pagesWhistleblowerAvinash Kumar100% (2)

- Whistle Blowing Case in InfosysDocument7 pagesWhistle Blowing Case in InfosysMahendhar Reddy PagadalaNo ratings yet

- Whistle BlowingDocument16 pagesWhistle BlowingSakshi Bansal83% (6)

- Secret Service: National Security in an Age of Open InformationFrom EverandSecret Service: National Security in an Age of Open InformationNo ratings yet

- Term Paper On Whistle BlowingDocument14 pagesTerm Paper On Whistle Blowingaayushijain1990100% (1)

- Week 4 Whistle BlowingDocument24 pagesWeek 4 Whistle BlowingPankaj GautamNo ratings yet

- 003 F - MR Alis Bin Puteh Full PaperDocument11 pages003 F - MR Alis Bin Puteh Full PaperastroneNo ratings yet

- Lecture 6Document13 pagesLecture 6Modest DarteyNo ratings yet

- Study On Whistle Blowing: For Ethics & Corporate Governance Assignment SubmissionDocument12 pagesStudy On Whistle Blowing: For Ethics & Corporate Governance Assignment SubmissionNikhil PachNo ratings yet

- Whistle Blowing PDFDocument21 pagesWhistle Blowing PDFAbdul MuqeetNo ratings yet

- A Business Ethic Theory of WhistleblowingDocument14 pagesA Business Ethic Theory of WhistleblowingIlham NurhidayatNo ratings yet

- CASTILLO - Part 02Document2 pagesCASTILLO - Part 02MARIELLE CASTILLONo ratings yet

- Seminar Report ON "Whistle Blowing"Document21 pagesSeminar Report ON "Whistle Blowing"Malika Malhotra100% (2)

- IJRHS_2014_vol02_issue-1Document5 pagesIJRHS_2014_vol02_issue-1lovesuvikashNo ratings yet

- Ulitarian or or Consequentialist Ethics Utilitarianism (Also Called Consequentialism) Is A Moral Theory Developed and Refined in TheDocument2 pagesUlitarian or or Consequentialist Ethics Utilitarianism (Also Called Consequentialism) Is A Moral Theory Developed and Refined in TheAnonymous sQPULpNo ratings yet

- Project ReportDocument49 pagesProject ReportShivani Bansal50% (4)

- Whistle BlowingDocument26 pagesWhistle Blowingsairaali_45No ratings yet

- A Project On Whistle Blowing (Business Ethics)Document14 pagesA Project On Whistle Blowing (Business Ethics)Kiran moreNo ratings yet

- White Collar Crime ExamDocument4 pagesWhite Collar Crime Examjinisha sharmaNo ratings yet

- Ethics at Workplace TheoriesDocument8 pagesEthics at Workplace TheoriesGaurav DevraNo ratings yet

- Descriptive EthicsDocument2 pagesDescriptive EthicsJhazreel BiasuraNo ratings yet

- Whistleblowing Group AssgDocument3 pagesWhistleblowing Group AssgEmellda MANo ratings yet

- Whistleblow IndiaDocument16 pagesWhistleblow IndiaSomashish NaskarNo ratings yet

- Paper Delivered To The National Conference of Whistleblowers Australia "Whistleblowing: Making It Work" September 11 2005, AdelaideDocument20 pagesPaper Delivered To The National Conference of Whistleblowers Australia "Whistleblowing: Making It Work" September 11 2005, AdelaidepurtflintNo ratings yet

- F024 Ishaan Shetty Research PaperDocument10 pagesF024 Ishaan Shetty Research PaperISHAAN SHETTYNo ratings yet

- Torque: Clarity On The US Waterboarding Policy Is Necessary To Combat ImpunityFrom EverandTorque: Clarity On The US Waterboarding Policy Is Necessary To Combat ImpunityNo ratings yet

- Whistleblowing: Presented by Ebad Khan Muhammad Uzair Hassan Asif SahibaDocument12 pagesWhistleblowing: Presented by Ebad Khan Muhammad Uzair Hassan Asif SahibaSahiba FaisalNo ratings yet

- SSRN Id2258296 PDFDocument10 pagesSSRN Id2258296 PDFVed VyasNo ratings yet

- SSRN Id2258296 PDFDocument10 pagesSSRN Id2258296 PDFVed VyasNo ratings yet

- Whistle BlowingDocument18 pagesWhistle BlowingabeerNo ratings yet

- The Bureaucratic Production of Difference: Ethos and Ethics in Migration AdministrationsFrom EverandThe Bureaucratic Production of Difference: Ethos and Ethics in Migration AdministrationsJulia M. EckertNo ratings yet

- Whistle BlowingDocument65 pagesWhistle Blowingtri utariNo ratings yet

- Criminological Theory (Labelling Theory) : Registered Criminologist, Napolcom Passer, Security Staff II, PAGCORDocument6 pagesCriminological Theory (Labelling Theory) : Registered Criminologist, Napolcom Passer, Security Staff II, PAGCORJee AlmanzorNo ratings yet

- Evasive Entrepreneurs and the Future of Governance: How Innovation Improves Economies and GovernmentsFrom EverandEvasive Entrepreneurs and the Future of Governance: How Innovation Improves Economies and GovernmentsNo ratings yet

- What Price the Moral High Ground?: How to Succeed without Selling Your SoulFrom EverandWhat Price the Moral High Ground?: How to Succeed without Selling Your SoulNo ratings yet

- Whistle Blowi NG: Evidence of Illegal Immoral ConductDocument18 pagesWhistle Blowi NG: Evidence of Illegal Immoral Conductdrbrijmohan100% (1)

- Lecture 3Document33 pagesLecture 3Florian Ananias ByarugabaNo ratings yet

- Whistle BlowingDocument34 pagesWhistle BlowingMuskaan ChaudharyNo ratings yet

- Human Rights as Human Independence: A Philosophical and Legal InterpretationFrom EverandHuman Rights as Human Independence: A Philosophical and Legal InterpretationNo ratings yet

- Title of Assignment:: Submitted To: Management Development Institute of Singapore - University of SunderlandDocument9 pagesTitle of Assignment:: Submitted To: Management Development Institute of Singapore - University of SunderlandandiniNo ratings yet

- FRA NotesDocument3 pagesFRA NotesAmit RayNo ratings yet

- Lokpal and Lokayukta: Administrative LawDocument10 pagesLokpal and Lokayukta: Administrative LawZainul AbedeenNo ratings yet

- TermPaper - Whistle BlowingDocument6 pagesTermPaper - Whistle BlowingAnshul GoyalNo ratings yet

- MEH - Combined (1) - 4Document9 pagesMEH - Combined (1) - 4Gandhi Jenny Rakeshkumar BD20029No ratings yet

- TheoriesDocument8 pagesTheoriesAmjad IrshadNo ratings yet

- Share Queenalyssayapbsedmath1bfinalexamDocument12 pagesShare Queenalyssayapbsedmath1bfinalexamCONDADA, FHILIP O.No ratings yet

- Gale Researcher Guide for: The Sociological Study of DevianceFrom EverandGale Researcher Guide for: The Sociological Study of DevianceNo ratings yet

- Name - Riaz Mehadi ID - 1931746042 Section - 8: 1. Explain and Evaluate The Four Critical Principles of EthicsDocument5 pagesName - Riaz Mehadi ID - 1931746042 Section - 8: 1. Explain and Evaluate The Four Critical Principles of EthicsRiaz Mehadi 1931746042No ratings yet

- UtilitarianismDocument6 pagesUtilitarianismRanz GieoNo ratings yet

- Daily InspirationDocument11 pagesDaily InspirationSunday OcheNo ratings yet

- Fund Raising Letter DniDocument2 pagesFund Raising Letter DniSunday OcheNo ratings yet

- Unfair CompetitionDocument9 pagesUnfair CompetitionSunday OcheNo ratings yet

- Unfair CompetitionDocument9 pagesUnfair CompetitionSunday OcheNo ratings yet

- Effects of Leadership Style On Organizational PerfDocument13 pagesEffects of Leadership Style On Organizational PerfEira Del RosarioNo ratings yet

- Fukuhmss19acc0183 Oche Acc 3210Document15 pagesFukuhmss19acc0183 Oche Acc 3210Sunday OcheNo ratings yet

- Bean Game ActivityDocument4 pagesBean Game Activityapi-314402585No ratings yet

- Handbook of Quality Procedures Before EPO enDocument73 pagesHandbook of Quality Procedures Before EPO enaffashNo ratings yet

- BBC Dividends from Unrealized Asset AppreciationDocument1 pageBBC Dividends from Unrealized Asset Appreciationvmanalo16No ratings yet

- LT Tax Advantage FundDocument2 pagesLT Tax Advantage FundDhanashri WarekarNo ratings yet

- Teacher performance certification Titay ZamboangaDocument3 pagesTeacher performance certification Titay ZamboangaJul Abs Salip100% (6)

- Invoice With Finance ChargeDocument1 pageInvoice With Finance ChargeD ¡ a R yNo ratings yet

- CIA Vs Parker Heaxd FinalDocument3 pagesCIA Vs Parker Heaxd Finalإسراء النبريصي50% (2)

- Introduction to Financial Institutions: An OverviewDocument16 pagesIntroduction to Financial Institutions: An OverviewsleshiNo ratings yet

- Earn 5 Unlocks For Every 10 Resources You UploadDocument1 pageEarn 5 Unlocks For Every 10 Resources You UploadHuber Emiro Riascos GomezNo ratings yet

- Baybay Elementary School Monthly Accomplishment Report on Anti-Drug ProgramsDocument1 pageBaybay Elementary School Monthly Accomplishment Report on Anti-Drug ProgramsCarinaJoy Ballesteros Mendez DeGuzman100% (1)

- Reliable Exports Lease DeedDocument27 pagesReliable Exports Lease DeedOkkishoreNo ratings yet

- Lista AuspiciadoresDocument2 pagesLista AuspiciadoresWanda MendezNo ratings yet

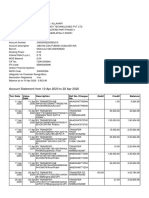

- Account activity and balance from 10 Apr to 22 AprDocument2 pagesAccount activity and balance from 10 Apr to 22 AprSRIDHAR allhari0% (1)

- Pineal Opening - Jigsaw Puzzle - Teal Swan ShopDocument1 pagePineal Opening - Jigsaw Puzzle - Teal Swan ShopBranx VisiNo ratings yet

- Biodesign - The Process of Innovating Medical Technologies - Section 4.1 NotesDocument5 pagesBiodesign - The Process of Innovating Medical Technologies - Section 4.1 NotesMaria JLNo ratings yet

- CRIME SCENE INVESTIGATIONDocument10 pagesCRIME SCENE INVESTIGATIONMel DonNo ratings yet

- Strategic AlliancesDocument20 pagesStrategic Alliancessatyabrat sahoo100% (1)

- Republic Vs de GuzmanDocument2 pagesRepublic Vs de GuzmanAxel Gonzalez100% (1)

- Tbtu MSDS (Tci-B1658) PDFDocument3 pagesTbtu MSDS (Tci-B1658) PDFBigbearBigbearNo ratings yet

- 2019 Os Parent Handbook Final 2Document44 pages2019 Os Parent Handbook Final 2api-573823749No ratings yet

- Accounting for Dividends and Preference SharesDocument16 pagesAccounting for Dividends and Preference Sharesruth san joseNo ratings yet

- SabioDocument2 pagesSabioPrecious TancincoNo ratings yet

- 论公民不服从(小姜老师整理)Document24 pages论公民不服从(小姜老师整理)James JiangNo ratings yet

- Fusion TaskListDocument20 pagesFusion TaskListObulareddy BiyyamNo ratings yet

- SN54273, SN54LS273, SN74273, SN74LS273 Octal D-Type Flip-Flop With ClearDocument8 pagesSN54273, SN54LS273, SN74273, SN74LS273 Octal D-Type Flip-Flop With Clearsas999333No ratings yet

- Tangan Vs CADocument1 pageTangan Vs CAjoyNo ratings yet

- NPA Recruitment Strategy EDITEDDocument55 pagesNPA Recruitment Strategy EDITEDLisha Binong100% (1)

- Indian Stock Market MechanismDocument2 pagesIndian Stock Market Mechanismneo0157No ratings yet

- Human Rights Sarmiento Chap 1Document11 pagesHuman Rights Sarmiento Chap 1nesteamackNo ratings yet

- Bar GlassesDocument31 pagesBar GlassesLyka GazminNo ratings yet