You might also like

- Upwork PDFDocument20 pagesUpwork PDFJP0% (4)

- Notes CA+Inter+Audit+May+24Document280 pagesNotes CA+Inter+Audit+May+24carlsen magNo ratings yet

- Principles of Auditing An Introduction To International Standards On Auditing 3rd Edition Hayes Solu 190402061241Document32 pagesPrinciples of Auditing An Introduction To International Standards On Auditing 3rd Edition Hayes Solu 190402061241Nia100% (2)

- CPA Audit NotesDocument38 pagesCPA Audit NotesDivjot Singh100% (1)

- Bankers Secret ManualDocument75 pagesBankers Secret ManualBZ Riger91% (33)

- Quality Assurance Manual For CpaDocument21 pagesQuality Assurance Manual For CpaJoan FranciscoNo ratings yet

- Auditing TheoryDocument27 pagesAuditing Theorysharielles /No ratings yet

- Uniform CPA Examination Questions May 1980 To November 1981Document260 pagesUniform CPA Examination Questions May 1980 To November 1981Adrienne GonzalezNo ratings yet

- Management Advisory ServicesDocument7 pagesManagement Advisory ServicesMarc Al Francis Jacob40% (5)

- PretestDocument3 pagesPretestDonise Ronadel SantosNo ratings yet

- Lecture 1-Part I: Introduction To Audit and Assurance ServicesDocument65 pagesLecture 1-Part I: Introduction To Audit and Assurance ServicesShueh Yi LimNo ratings yet

- Chapter 1-Overview To AuditingDocument43 pagesChapter 1-Overview To Auditingselman AregaNo ratings yet

- QUIZ001Document2 pagesQUIZ001Anna LomenarioNo ratings yet

- K1 - Jan 2011Document30 pagesK1 - Jan 2011Niki KhorNo ratings yet

- 4introduction To AuditingDocument13 pages4introduction To AuditingFranz CampuedNo ratings yet

- Module 2 - Audit, An OverviewDocument8 pagesModule 2 - Audit, An OverviewMAG MAGNo ratings yet

- Topic # 2: Introdu Ction To Auditin GDocument31 pagesTopic # 2: Introdu Ction To Auditin GRizza OmalinNo ratings yet

- 1498721945audit JoinerDocument70 pages1498721945audit JoinerRockNo ratings yet

- Audit of Overview: Auditing IsDocument26 pagesAudit of Overview: Auditing IsMaria BeatriceNo ratings yet

- Reviewer For AuditingDocument34 pagesReviewer For AuditingKei VenusaNo ratings yet

- Pre1 QuizDocument3 pagesPre1 QuizJessa Gay Cartagena TorresNo ratings yet

- Phases of The Audit ProcessDocument4 pagesPhases of The Audit ProcessChristian Justin MilitanteNo ratings yet

- General Types of AuditDocument39 pagesGeneral Types of AuditRyzeNo ratings yet

- Module 01 - Auditing, Attestation and AssuranceDocument7 pagesModule 01 - Auditing, Attestation and AssuranceMAG MAGNo ratings yet

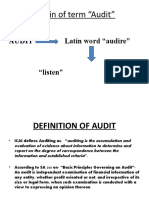

- Origin of Term "Audit": AUDIT Latin Word "Audire"Document17 pagesOrigin of Term "Audit": AUDIT Latin Word "Audire"ranjana7123No ratings yet

- IntroductionDocument44 pagesIntroductionSaiful IslamNo ratings yet

- Difference Between Accounting and AuditingDocument21 pagesDifference Between Accounting and AuditingLaraib SalmanNo ratings yet

- Auditing Assignment 2Document5 pagesAuditing Assignment 2Harshit VaishyaNo ratings yet

- Chap 1 Nature of AuditingDocument32 pagesChap 1 Nature of AuditingAkash Gupta100% (1)

- Auditing: Chapter 1: Introduction To AuditingDocument45 pagesAuditing: Chapter 1: Introduction To AuditingMIR AADILNo ratings yet

- Audit 1 Midterm Exams Part I True or False 50 Points Instruction: Write TRUE If The Statement Is Correct and Write FALSE If TheDocument6 pagesAudit 1 Midterm Exams Part I True or False 50 Points Instruction: Write TRUE If The Statement Is Correct and Write FALSE If Therico mangawiliNo ratings yet

- Aa PDFDocument308 pagesAa PDFTaskin Reza KhalidNo ratings yet

- ACAUD 3149 TOPIC 1 Overview of The Audit ProcessDocument2 pagesACAUD 3149 TOPIC 1 Overview of The Audit ProcessCazia Mei JoverNo ratings yet

- Audtheo Mod1Document4 pagesAudtheo Mod1Christian Arnel Jumpay LopezNo ratings yet

- Nature and Scope of AuditingDocument23 pagesNature and Scope of AuditingPrachi GuptaNo ratings yet

- Introduction To Auditing (Autosaved) 4Document30 pagesIntroduction To Auditing (Autosaved) 4THATONo ratings yet

- Chapter 12 - Assurance & Other Related ServicesDocument5 pagesChapter 12 - Assurance & Other Related ServicesellieNo ratings yet

- IM-01 Overview of Audit and Other Assurance ServicesDocument7 pagesIM-01 Overview of Audit and Other Assurance Servicesharley_quinn11No ratings yet

- Module 2 - Introduction To FS AuditDocument5 pagesModule 2 - Introduction To FS AuditLysss EpssssNo ratings yet

- Audit Practice and Assurance Services - A1.4 PDFDocument94 pagesAudit Practice and Assurance Services - A1.4 PDFFRANCOIS NKUNDIMANANo ratings yet

- Chapter 3 General Types of Audit - PPT 123915218Document32 pagesChapter 3 General Types of Audit - PPT 123915218Clar Aaron Bautista100% (2)

- Lecture OneDocument32 pagesLecture OneNeha LalNo ratings yet

- Nature of AuditingDocument37 pagesNature of Auditinganon_672065362No ratings yet

- Aaa Topic 1Document8 pagesAaa Topic 1Cindy ClollyNo ratings yet

- Audit Problem (Aaconapps2 - Cash and ReceivablesDocument261 pagesAudit Problem (Aaconapps2 - Cash and ReceivablesDawson Dela CruzNo ratings yet

- A6.4 A UNIT 1 & 2 Auditing PracticesDocument27 pagesA6.4 A UNIT 1 & 2 Auditing PracticesGaurav MahajanNo ratings yet

- To Financial Statement Audit: OCTOBER 7, 2021 Auditing TheoryDocument39 pagesTo Financial Statement Audit: OCTOBER 7, 2021 Auditing TheoryJoyce Anne GarduqueNo ratings yet

- Audit OverviewDocument13 pagesAudit OverviewKei VenusaNo ratings yet

- Introduction To Audit STDocument24 pagesIntroduction To Audit STTaha DaudNo ratings yet

- Framework of Philippine Standards On AuditingDocument2 pagesFramework of Philippine Standards On AuditingKaye SyNo ratings yet

- Aud1 & Aud12Document7 pagesAud1 & Aud12Lyka CastroNo ratings yet

- PSBA - Introduction To Assurance and Related ServicesDocument6 pagesPSBA - Introduction To Assurance and Related ServicesephraimNo ratings yet

- Auditing and Assurance PrinciplesDocument19 pagesAuditing and Assurance Principleskanroji1923No ratings yet

- Reviewer Ko HuhuDocument13 pagesReviewer Ko HuhuKei VenusaNo ratings yet

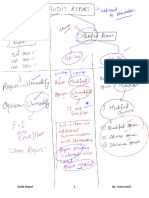

- 48) Audit ReportDocument9 pages48) Audit ReportkasimranjhaNo ratings yet

- Auditing Theory Cabrera 2010 Chapter 03Document8 pagesAuditing Theory Cabrera 2010 Chapter 03Squishy potatoNo ratings yet

- Chapter - 04, Process of Assurance - Evidence and ReportingDocument5 pagesChapter - 04, Process of Assurance - Evidence and Reportingmahbub khanNo ratings yet

- General Types of Audit: Review QuestionsDocument8 pagesGeneral Types of Audit: Review QuestionsUnnamed homosapienNo ratings yet

- AUDIT - An Overview: Kalven Perry T. AgustinDocument17 pagesAUDIT - An Overview: Kalven Perry T. AgustinANGELA THEA BUENVENIDANo ratings yet

- Introduction To Auditing PDFDocument18 pagesIntroduction To Auditing PDFHazel Bianca GabalesNo ratings yet

- Topic I - Demand For Auditing and Assurance ServicesDocument7 pagesTopic I - Demand For Auditing and Assurance ServicesaragonkaycyNo ratings yet

- Talbot SlidesCarnivalDocument38 pagesTalbot SlidesCarnivalLester Glenn LimheyaNo ratings yet

- Review and Audit AssuranceDocument6 pagesReview and Audit AssuranceReg DungcaNo ratings yet

- Chapter 03 AnsDocument7 pagesChapter 03 AnsDave ManaloNo ratings yet

- 2008 Auditing Handbook A180 ISA 600Document5 pages2008 Auditing Handbook A180 ISA 600Nisa Zati JamalNo ratings yet

- Engagement Essentials: Preparation, Compilation, and Review of Financial StatementsFrom EverandEngagement Essentials: Preparation, Compilation, and Review of Financial StatementsNo ratings yet

- 2012-08 CPA Journal AugustDocument84 pages2012-08 CPA Journal AugustshrikantsubsNo ratings yet

- Permintaan Jasa Audit Dan Assurance LainnyaDocument46 pagesPermintaan Jasa Audit Dan Assurance Lainnyafera'sNo ratings yet

- Richard M Young ResumeDocument2 pagesRichard M Young ResumeMorgan SullivanNo ratings yet

- Background Note On Action Plans: Action Plan Developed by Korean Institute of Certified Public Accountants (KICPA)Document28 pagesBackground Note On Action Plans: Action Plan Developed by Korean Institute of Certified Public Accountants (KICPA)radha ramaswamyNo ratings yet

- Slides - Efa - AuditingDocument24 pagesSlides - Efa - Auditinghuangtana13052003No ratings yet

- Chapter 9 PDFDocument17 pagesChapter 9 PDFJasmine LimNo ratings yet

- Arens14e Ch02 PDFDocument36 pagesArens14e Ch02 PDFlaksmitadewiasastaniNo ratings yet

- Integrated AccountingDocument4 pagesIntegrated AccountingJennilou AñascoNo ratings yet

- Syed Waji Ul Hassan Bokhari (FIND)Document3 pagesSyed Waji Ul Hassan Bokhari (FIND)HshhsbsNo ratings yet

- Questions and Answers On Boa Resolution Feb 3Document9 pagesQuestions and Answers On Boa Resolution Feb 3Danilo Pasana Jr.No ratings yet

- Bernadette M. Festin: Province Contact Number: +63945-231-6869Document3 pagesBernadette M. Festin: Province Contact Number: +63945-231-6869Bernadette M. FestinNo ratings yet

- Auditing Investments - A Guide - CPA Hall TalkDocument14 pagesAuditing Investments - A Guide - CPA Hall TalkRhea SimoneNo ratings yet

- Id - 321 - 20160727 - QP BrochureDocument6 pagesId - 321 - 20160727 - QP BrochureJac YuenNo ratings yet

- Final OutputDocument62 pagesFinal OutputJenny Mae AbelinNo ratings yet

- Chapter 3Document57 pagesChapter 3Marco RegunayanNo ratings yet

- Update 87Document40 pagesUpdate 87David BriggsNo ratings yet

- Cpa RepresentationDocument2 pagesCpa RepresentationCloudin Guitabao Catte-GanoNo ratings yet

- Full Download:: Suggested Answers To Discussion QuestionsDocument8 pagesFull Download:: Suggested Answers To Discussion QuestionsIrawatiNo ratings yet

- Accounting Professional: Corporate - Insolvency - CharteredDocument2 pagesAccounting Professional: Corporate - Insolvency - Charteredsamwilson0501No ratings yet

- Auditing Theory Answer Key 1Document197 pagesAuditing Theory Answer Key 1AngelUmayam100% (2)

- Test Bank AISDocument12 pagesTest Bank AISJOCELYN BERDULNo ratings yet

- Ethics QuestionsDocument4 pagesEthics QuestionsShwaibu Sella100% (1)

- AT-20 Part2Document2 pagesAT-20 Part2Edsel TulipasNo ratings yet