You might also like

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Economic and Business Forecasting: Analyzing and Interpreting Econometric ResultsFrom EverandEconomic and Business Forecasting: Analyzing and Interpreting Econometric ResultsNo ratings yet

- Chap 7 - Flexible Budget, Direct Cost Variance and Management Control - Students NoteDocument13 pagesChap 7 - Flexible Budget, Direct Cost Variance and Management Control - Students NoteZulIzzamreeZolkepliNo ratings yet

- CVPDocument8 pagesCVPJessica EntacNo ratings yet

- CH 11 - CF Estimation Mini Case Sols Excel 14edDocument36 pagesCH 11 - CF Estimation Mini Case Sols Excel 14edأثير مخوNo ratings yet

- Z Company Income Statement ComparisonDocument11 pagesZ Company Income Statement ComparisonMohamed RefaayNo ratings yet

- UTECH CVP Income Statement 2010Document8 pagesUTECH CVP Income Statement 2010dcarruciniNo ratings yet

- Chapter 5 6Document8 pagesChapter 5 6Maricar PinedaNo ratings yet

- E22-6 (LO 2) Accounting Changes-DepreciationDocument6 pagesE22-6 (LO 2) Accounting Changes-DepreciationRiana DeztianiNo ratings yet

- E8-29 Segmented Income Statement: Conceptual ConnectionDocument5 pagesE8-29 Segmented Income Statement: Conceptual ConnectionDhiva Rianitha Manurung100% (1)

- Ch8 Additional Practice-AnswersDocument3 pagesCh8 Additional Practice-AnswerstolatillerNo ratings yet

- Budgetary Planning & Control ForumDocument4 pagesBudgetary Planning & Control ForumWindy MartaputriNo ratings yet

- SMCH 13Document47 pagesSMCH 13Lara Lewis AchillesNo ratings yet

- 9-28 Variable and Absorption Costing, Sales, and Operating-Income Changes. Smart SafetyDocument4 pages9-28 Variable and Absorption Costing, Sales, and Operating-Income Changes. Smart SafetyElliot RichardNo ratings yet

- MBA 504 Ch5 SolutionsDocument12 pagesMBA 504 Ch5 SolutionspheeyonaNo ratings yet

- Tutorial 3 - Student AnswerDocument7 pagesTutorial 3 - Student AnswerDâmDâmCôNươngNo ratings yet

- Tutorial 4 SolutionsDocument14 pagesTutorial 4 Solutionss11186706No ratings yet

- Answer Key To Test #3 - ACCT-312 - Fall 2019Document8 pagesAnswer Key To Test #3 - ACCT-312 - Fall 2019Amir ContrerasNo ratings yet

- Variable & Absorption Costing Income Statements with Constant Sales & Variable ProductionDocument17 pagesVariable & Absorption Costing Income Statements with Constant Sales & Variable ProductionApurvAdarshNo ratings yet

- Financial Control - 2 - Variances - Additional Exercises With SolutionDocument9 pagesFinancial Control - 2 - Variances - Additional Exercises With SolutionQuang Nhựt100% (1)

- ACCCOB3Document10 pagesACCCOB3Jenine YamsonNo ratings yet

- Hospital Supply: Alternative Choice Decisions Differential CostingDocument13 pagesHospital Supply: Alternative Choice Decisions Differential Costingksandeep25No ratings yet

- Answers To Questions Answers To Exercises Exercise 1-1 Part A Normal Earnings For Similar Firms ($15,000,000 - $8,800,000) X 15% $930,000Document2 pagesAnswers To Questions Answers To Exercises Exercise 1-1 Part A Normal Earnings For Similar Firms ($15,000,000 - $8,800,000) X 15% $930,000sameerNo ratings yet

- Quiz 17: Flexible Budget Variances for Alloway's FencingDocument2 pagesQuiz 17: Flexible Budget Variances for Alloway's Fencingwarning urgentNo ratings yet

- Far Tutor 3Document4 pagesFar Tutor 3Rian RorresNo ratings yet

- Case 2-1: Solution To Old Turkey MashDocument2 pagesCase 2-1: Solution To Old Turkey MashNeha Wadhwani AhujaNo ratings yet

- Bài tập chương 13Document10 pagesBài tập chương 132021agl12.phamhoangdieumyNo ratings yet

- TUGAS PRIBADI AKUNTANSI KEUANGAN LANJUTAN 1Document9 pagesTUGAS PRIBADI AKUNTANSI KEUANGAN LANJUTAN 1Maulana AmriNo ratings yet

- Chapter 7 Practice QuestionsDocument12 pagesChapter 7 Practice QuestionsZethu JoeNo ratings yet

- AF102 Final Exam Revision PackageDocument22 pagesAF102 Final Exam Revision Packagetb66jfpbrzNo ratings yet

- Fabricare GAAP income statement analysisDocument15 pagesFabricare GAAP income statement analysisRishika RathiNo ratings yet

- Lakeside Jawaban CaseDocument40 pagesLakeside Jawaban CaseDhenayu Tresnadya HendrikNo ratings yet

- Contribution Margin Ratio 0.2: Compute The Break-Even Point in Dollar Sales For Each ProductDocument4 pagesContribution Margin Ratio 0.2: Compute The Break-Even Point in Dollar Sales For Each ProductVõ Triệu VyNo ratings yet

- Chapter 7Document11 pagesChapter 7jake doinog86% (14)

- Acc Tut 12 Final JTDocument21 pagesAcc Tut 12 Final JTxhayyyzNo ratings yet

- Session 4 Practice ProblemsDocument11 pagesSession 4 Practice ProblemsRishika RathiNo ratings yet

- Product Production Units Sales Units: Selling Price Per UnitDocument3 pagesProduct Production Units Sales Units: Selling Price Per UnitKamisiro RizeNo ratings yet

- Key Answer for Assignment + Additional Practice QuestionsDocument19 pagesKey Answer for Assignment + Additional Practice QuestionsNCTNo ratings yet

- Chapter 7 Homework ADocument2 pagesChapter 7 Homework ALong BuiNo ratings yet

- Problem 5-1A:: Selling Prices ($500 X 2.000 Units) $1.000.000Document6 pagesProblem 5-1A:: Selling Prices ($500 X 2.000 Units) $1.000.000Võ Triệu VyNo ratings yet

- Case 16-1 - Hospital Supply, Inc.Document5 pagesCase 16-1 - Hospital Supply, Inc.Ebans Castillo BennettNo ratings yet

- Sol. Man. - Chapter 9 - Interim Financial ReportingDocument6 pagesSol. Man. - Chapter 9 - Interim Financial ReportingAEDRIAN LEE DERECHONo ratings yet

- B326 Final 2017-2018 MGL1Document9 pagesB326 Final 2017-2018 MGL1Shoug SaNo ratings yet

- CH 06Document7 pagesCH 06Gus JooNo ratings yet

- Enigma Corporation Cost of Goods SoldDocument6 pagesEnigma Corporation Cost of Goods SoldEunice CoronadoNo ratings yet

- Manlimos Lyka AssignmentDocument7 pagesManlimos Lyka AssignmentMitch Tokong MinglanaNo ratings yet

- ST ND RD THDocument5 pagesST ND RD THNOVIDANo ratings yet

- Student Q&A on Adjusting EventsTITLESTAR Ltd Financial Statements 2017 TITLESTAR Ltd Statement of Changes in EquityTITLESPSE Annual Reports 2018 Classification TipsDocument3 pagesStudent Q&A on Adjusting EventsTITLESTAR Ltd Financial Statements 2017 TITLESTAR Ltd Statement of Changes in EquityTITLESPSE Annual Reports 2018 Classification TipsAvishchal ChandNo ratings yet

- CH 8 Practice HomeworkDocument11 pagesCH 8 Practice HomeworkNCT100% (1)

- M3 Activity 1Document6 pagesM3 Activity 1Ruffa May GonzalesNo ratings yet

- Group 2 - Answers To QuestionsDocument2 pagesGroup 2 - Answers To QuestionsJr Roque100% (4)

- Problem 1: Cost Volume Profit RelationshipsDocument22 pagesProblem 1: Cost Volume Profit RelationshipsNamir RafiqNo ratings yet

- Hilton CH 8 Select SolutionsDocument9 pagesHilton CH 8 Select SolutionsDebashruti BiswasNo ratings yet

- Solved Problems-Chapter 6 PDFDocument11 pagesSolved Problems-Chapter 6 PDFRoqaia AlwanNo ratings yet

- Operating ExposureDocument27 pagesOperating Exposureashu khetanNo ratings yet

- Analyzing Project Cash Flows: T 0 T 1 Through T 10 AssumptionsDocument45 pagesAnalyzing Project Cash Flows: T 0 T 1 Through T 10 AssumptionsStevin GeorgeNo ratings yet

- FINA 3330 - Notes CH 9Document2 pagesFINA 3330 - Notes CH 9fische100% (1)

- Calculate breakeven point, target sales, and safety margin for contribution margin analysisDocument5 pagesCalculate breakeven point, target sales, and safety margin for contribution margin analysisAbhijit AshNo ratings yet

- Cash Flow Statement SectionsDocument3 pagesCash Flow Statement SectionsTIÊN NGUYỄN LÊ MỸNo ratings yet

- Exhibit 1 Results of Operation - 1985: Ovens Stoves TotalDocument27 pagesExhibit 1 Results of Operation - 1985: Ovens Stoves TotalcandratriutariNo ratings yet

- Key Features of EPF Act 1952Document3 pagesKey Features of EPF Act 1952Fency Jenus67% (3)

- Commerce Questions For PSC ExamsDocument40 pagesCommerce Questions For PSC ExamsShanmuga SubramanianNo ratings yet

- Hku166 PDF EngDocument16 pagesHku166 PDF EngPaodou HuNo ratings yet

- Sabrina SultanaDocument64 pagesSabrina SultanaMohib Ullah YousafzaiNo ratings yet

- Chapter 1 - IBFDocument11 pagesChapter 1 - IBFmariumzehraNo ratings yet

- Horngren Ima16 Tif 17 GEDocument53 pagesHorngren Ima16 Tif 17 GEasem shabanNo ratings yet

- Activity Chapter 1 Actg 111aDocument2 pagesActivity Chapter 1 Actg 111aVergs Valencia100% (3)

- EarlyRetirementNow Side Hustle SWR ToolboxDocument375 pagesEarlyRetirementNow Side Hustle SWR ToolboxJaredNo ratings yet

- 2022 AL Economics Past Paper - English MediumDocument11 pages2022 AL Economics Past Paper - English Mediumcrisgk1234No ratings yet

- Cash Handling FEDocument109 pagesCash Handling FEAsfar KhanNo ratings yet

- Alstom Pursues Asset Sales After Warning On Cash FlowDocument1 pageAlstom Pursues Asset Sales After Warning On Cash FlownelsonashwheelerNo ratings yet

- Economic Growth: Cameroon'SDocument53 pagesEconomic Growth: Cameroon'SFabrice EwoloNo ratings yet

- Fin TechDocument3 pagesFin TechDiana PerezNo ratings yet

- Chase Bank Financial StatementDocument3 pagesChase Bank Financial StatementGo DumpNo ratings yet

- Institute of Business Management: Lms Based Finalexaminations-Summer 2020 Analytical PartDocument3 pagesInstitute of Business Management: Lms Based Finalexaminations-Summer 2020 Analytical PartSafi SheikhNo ratings yet

- Hdssdas 7878Document3 pagesHdssdas 7878vamshiyerrawarNo ratings yet

- Qustion-01 (05+06) Marks (A) :: Bahauddin Zakariya University, Multan Instructions For The ExamDocument2 pagesQustion-01 (05+06) Marks (A) :: Bahauddin Zakariya University, Multan Instructions For The ExamUsman BalochNo ratings yet

- Sumit Singh-Zomato InvoiceDocument1 pageSumit Singh-Zomato InvoiceSumit SinghNo ratings yet

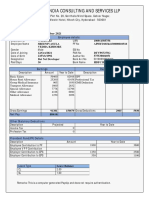

- Purview India Consulting and Services LLPDocument1 pagePurview India Consulting and Services LLPmamatha vemulaNo ratings yet

- Differences Between Forward, Futures and OptionsDocument10 pagesDifferences Between Forward, Futures and OptionsDIANA CABALLERONo ratings yet

- TRS Retirees 05.12.10 Final1Document3 pagesTRS Retirees 05.12.10 Final1Celeste KatzNo ratings yet

- Reviewer On Inter Accounting CH 1 6 1Document19 pagesReviewer On Inter Accounting CH 1 6 1Roseyy Galit43% (7)

- COMM324-03 Investing in Tesla Stock Run-UpDocument2 pagesCOMM324-03 Investing in Tesla Stock Run-UpKendra HalmanNo ratings yet

- Pag-Ibig Mp2 Application FormDocument2 pagesPag-Ibig Mp2 Application Formroy czar pableoNo ratings yet

- Lesson Plan Financial Derivatives MbaiiiDocument5 pagesLesson Plan Financial Derivatives MbaiiiSheg AonNo ratings yet

- Engineering Economics Assignment 2Document6 pagesEngineering Economics Assignment 2balkrishna7621No ratings yet

- EI Fund Transfer Intnl TT Form V3.0Document1 pageEI Fund Transfer Intnl TT Form V3.0Tosin SimeonNo ratings yet

- Axis Card 1Document4 pagesAxis Card 1Om PrakashNo ratings yet

- A Study On Finacial Advisor For Mutual Fund InvestorsDocument53 pagesA Study On Finacial Advisor For Mutual Fund InvestorsPrasanna Belligatti100% (1)

- Branch and Unit BankingDocument1 pageBranch and Unit BankingSheetal Thomas100% (1)