You might also like

- Islamic Financial Transaction TerminologyDocument6 pagesIslamic Financial Transaction Terminologyaries_1984No ratings yet

- BAY' AL INAH AND TAWARRUQ EXPLAINEDDocument8 pagesBAY' AL INAH AND TAWARRUQ EXPLAINEDAisyah SyuhadaNo ratings yet

- Presentation Bba and MurabahahDocument31 pagesPresentation Bba and MurabahahSyharmimi_Shar_6100No ratings yet

- Introduction To Business ManagementDocument24 pagesIntroduction To Business ManagementZintle Mini0% (1)

- U9L4 Activity+Guide+ +Exploring+Two+Columns+ +Unit+9+Lesson+4Document2 pagesU9L4 Activity+Guide+ +Exploring+Two+Columns+ +Unit+9+Lesson+4Rylan Russell0% (1)

- Shlokas and BhajansDocument204 pagesShlokas and BhajansCecilie Ramazanova100% (1)

- Members From The Vietnam Food AssociationDocument19 pagesMembers From The Vietnam Food AssociationMaiquynh DoNo ratings yet

- Chapter 2 - Islamic Contract in The International Trade FinancingDocument19 pagesChapter 2 - Islamic Contract in The International Trade FinancingAisyah AnuarNo ratings yet

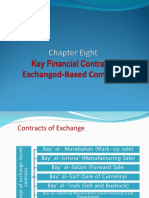

- Chapter 8Document40 pagesChapter 8otaku himeNo ratings yet

- Introduction To Various Major Transactions in Islamic Law: Basic Operation of Interest Banking SystemDocument17 pagesIntroduction To Various Major Transactions in Islamic Law: Basic Operation of Interest Banking SystemZalikha HassimNo ratings yet

- Chapter 6 - Murabahah - Salam - Istisna 2Document42 pagesChapter 6 - Murabahah - Salam - Istisna 2d7gpxg55j9No ratings yet

- CHAPTER 7 APPLICATION of FUNDS Financing Facilities and The Underlying Shariah Concepts Editing PDFDocument122 pagesCHAPTER 7 APPLICATION of FUNDS Financing Facilities and The Underlying Shariah Concepts Editing PDFNURADILAH AHMAD SHAIFUDDINNo ratings yet

- Debt Financing Options in Islamic Finance: Salam, Ijarah, Istisna and Qardhul HassanDocument43 pagesDebt Financing Options in Islamic Finance: Salam, Ijarah, Istisna and Qardhul HassanAmalMdIsaNo ratings yet

- Islamic Banking PrinciplesDocument3 pagesIslamic Banking PrinciplesMd ArqamNo ratings yet

- Chap 3 Part 2Document42 pagesChap 3 Part 2Intan SawalNo ratings yet

- UIB2612 1630 LECTURE 6 MurabahahDocument32 pagesUIB2612 1630 LECTURE 6 MurabahahSyahirah ArifNo ratings yet

- AnOverviewOfShariahContractPractice PDFDocument27 pagesAnOverviewOfShariahContractPractice PDFKuo Hsiung ChongNo ratings yet

- 8th Mode of FinancingDocument30 pages8th Mode of FinancingYaseen IqbalNo ratings yet

- Islamic Banking and Conventional BankingDocument4 pagesIslamic Banking and Conventional BankingSajjad AliNo ratings yet

- Murabaha FinanceDocument36 pagesMurabaha FinancesaadriazNo ratings yet

- Bay' Al-Murabahah: By: Nur Hasanah Ishar Kolej Profesional Baitulmal Kuala LumpurDocument11 pagesBay' Al-Murabahah: By: Nur Hasanah Ishar Kolej Profesional Baitulmal Kuala LumpurNur Hasanah IsharNo ratings yet

- Accounting For Special Transactions: Unit - 1 Bills of Exhange and Promissory NotesDocument31 pagesAccounting For Special Transactions: Unit - 1 Bills of Exhange and Promissory NotesNakul ChaudharyNo ratings yet

- Advanced Islamic Banking and Finance: Murabahah Contracts and Vehicle FinancingDocument20 pagesAdvanced Islamic Banking and Finance: Murabahah Contracts and Vehicle FinancingFBusinessNo ratings yet

- T3 - Salient Features and ContractsDocument49 pagesT3 - Salient Features and Contractsmichael musillaNo ratings yet

- Aitab (Bina Malaysia Bank Berhad)Document9 pagesAitab (Bina Malaysia Bank Berhad)Nur Amin Nor AzmiNo ratings yet

- Aitab (Bina Malaysia Bank Berhad)Document9 pagesAitab (Bina Malaysia Bank Berhad)Nur Amin Nor AzmiNo ratings yet

- Application of Funds - Financing Facilities and The Underlying Shariah ConceptsDocument40 pagesApplication of Funds - Financing Facilities and The Underlying Shariah ConceptsMahyuddin Khalid100% (1)

- Musharakah and key Islamic banking concepts explainedDocument4 pagesMusharakah and key Islamic banking concepts explainedNoha DbnNo ratings yet

- DIMINISHING-MUSHARIKA-14112021-072718pmDocument24 pagesDIMINISHING-MUSHARIKA-14112021-072718pmAwn AqdasNo ratings yet

- Hbl-Islamic Banking (Hbl-Ib) Business ProductsDocument18 pagesHbl-Islamic Banking (Hbl-Ib) Business ProductsNaughty PrinceNo ratings yet

- MTB Yaqeen Hire Purchase Under Shirkatul Milk (HPSM) : (In The Name of Allah, The Merciful, The Compassionate)Document25 pagesMTB Yaqeen Hire Purchase Under Shirkatul Milk (HPSM) : (In The Name of Allah, The Merciful, The Compassionate)ovifinNo ratings yet

- Exercise Chap 3 Isb548Document4 pagesExercise Chap 3 Isb548Atiqah AzmanNo ratings yet

- Islamic Banking Governance and Maybank's AITAB Car FinancingDocument13 pagesIslamic Banking Governance and Maybank's AITAB Car FinancingSHANo ratings yet

- Islamic Finance TermsDocument7 pagesIslamic Finance TermsShahin RahmanNo ratings yet

- Islamic Economics Law: The Concept of Murabaha and Musyarakah MutanaqishahDocument8 pagesIslamic Economics Law: The Concept of Murabaha and Musyarakah MutanaqishahSabita AnjaningNo ratings yet

- Islamic Accounting P 2Document60 pagesIslamic Accounting P 2Abdelnasir HaiderNo ratings yet

- Islamic Financial Systems-2Document17 pagesIslamic Financial Systems-2محمد حسنین رضا قادریNo ratings yet

- Chapter 7: Business Contracts in Islam: 4PM-7PM FST-BK 6.3 Group 5Document23 pagesChapter 7: Business Contracts in Islam: 4PM-7PM FST-BK 6.3 Group 5iman zainuddinNo ratings yet

- Chapter 5 Ijarah 16012022 061036pmDocument12 pagesChapter 5 Ijarah 16012022 061036pmYusra Rehman KhanNo ratings yet

- Islamic Modes of FinancingDocument17 pagesIslamic Modes of FinancingALI SHER HaidriNo ratings yet

- Assignment On MurabahahDocument4 pagesAssignment On Murabahahjazi_4u67% (3)

- Murabahah Parameter PresentDocument49 pagesMurabahah Parameter PresentRabiatul Adawiyah Muhammad FisolNo ratings yet

- Contract MuamalatDocument16 pagesContract MuamalatHarizul RafiqNo ratings yet

- Murabahah and Murabahah For Purchase Orderer: Islamic Financial TransactionsDocument14 pagesMurabahah and Murabahah For Purchase Orderer: Islamic Financial TransactionsSolomon TekalignNo ratings yet

- Islamic FinanceDocument35 pagesIslamic FinanceMuhammed UsmanNo ratings yet

- Investment SideDocument52 pagesInvestment Sideayman FergeionNo ratings yet

- MurabahaDocument28 pagesMurabahaNashaad SardheeyeNo ratings yet

- Murabaha Finanacing in PakistanDocument47 pagesMurabaha Finanacing in Pakistanaamir mumtazNo ratings yet

- Isb540 - MurabahahDocument16 pagesIsb540 - MurabahahMahyuddin Khalid100% (1)

- MIA Tax Treatment On Islamic Finance PDFDocument24 pagesMIA Tax Treatment On Islamic Finance PDFHANISANo ratings yet

- Ch.7 Hire Purchase - Instalment SystemDocument14 pagesCh.7 Hire Purchase - Instalment SystemDeepthi R Tejur100% (1)

- Term Descriptions: Glossary of TermsDocument2 pagesTerm Descriptions: Glossary of TermsabdellaNo ratings yet

- Uqud in Islamic Financial TransactionsDocument40 pagesUqud in Islamic Financial Transactionsmohamed saidNo ratings yet

- AssignmentDocument10 pagesAssignmentmuhammad harisNo ratings yet

- Meezan Bank ReportDocument19 pagesMeezan Bank ReportkashifislamicNo ratings yet

- Islamic Finance Ch2Document16 pagesIslamic Finance Ch2Youssef NabilNo ratings yet

- IjarahDocument20 pagesIjarahRehman TariqNo ratings yet

- Islamic Banking ProductDocument3 pagesIslamic Banking Productput3_waniegurlNo ratings yet

- Islamic Banking: Islamic Modes of FinanceDocument16 pagesIslamic Banking: Islamic Modes of FinanceSoban MamoonNo ratings yet

- Yasaar Glossary of TermsDocument5 pagesYasaar Glossary of TermsFatin MetassanNo ratings yet

- MurabahaDocument31 pagesMurabahaMustafe MohamedNo ratings yet

- Revealed From A Top Realtor: The Fastest Way To Sell Properties Like Crazy In Real Estate - Even If You Are A Complete NewbieFrom EverandRevealed From A Top Realtor: The Fastest Way To Sell Properties Like Crazy In Real Estate - Even If You Are A Complete NewbieNo ratings yet

- StanadyneDocument1 pageStanadyneJunior IungNo ratings yet

- Bohol - Eng5 Q2 WK8Document17 pagesBohol - Eng5 Q2 WK8Leceil Oril PelpinosasNo ratings yet

- Album China RayaDocument12 pagesAlbum China Rayaapitmelodi23No ratings yet

- Consumer BehaviourDocument30 pagesConsumer BehaviourManoj BaghelNo ratings yet

- Aqa Textiles Gcse Coursework Grade BoundariesDocument4 pagesAqa Textiles Gcse Coursework Grade Boundariesrqaeibifg100% (2)

- 2.2 - T - Basic Negotiation Skill Vol. 1Document5 pages2.2 - T - Basic Negotiation Skill Vol. 1Siva 93No ratings yet

- Armenian Question in Tasvir-İ Efkar Between 1914 and 1918Document152 pagesArmenian Question in Tasvir-İ Efkar Between 1914 and 1918Gültekin ÖNCÜNo ratings yet

- Competences Needed in Testing - Handout Manual PDFDocument97 pagesCompetences Needed in Testing - Handout Manual PDFCristina LucaNo ratings yet

- Led PowerpointDocument35 pagesLed PowerpointArunkumarNo ratings yet

- Food Safety Culture Webinar SLIDESDocument46 pagesFood Safety Culture Webinar SLIDESAto Kwamena PaintsilNo ratings yet

- Is 5312 1 2004Document13 pagesIs 5312 1 2004kprasad_56900No ratings yet

- Dividend PolicyDocument16 pagesDividend PolicyJhaden CatudioNo ratings yet

- Activity Sheets in Science VIDocument24 pagesActivity Sheets in Science VIFrauddiggerNo ratings yet

- An Umbrella For Druvi: Author: Shabnam Minwalla Illustrator: Malvika TewariDocument12 pagesAn Umbrella For Druvi: Author: Shabnam Minwalla Illustrator: Malvika TewariKiran Kumar AkulaNo ratings yet

- Ritangle 2018 QuestionsDocument25 pagesRitangle 2018 QuestionsStormzy 67No ratings yet

- LK 2 - Lembar Kerja Refleksi Modul 4 UnimDocument2 pagesLK 2 - Lembar Kerja Refleksi Modul 4 UnimRikhatul UnimNo ratings yet

- News TIA Portal V15 and V15 1 enDocument43 pagesNews TIA Portal V15 and V15 1 enjohanNo ratings yet

- 07 - Toshkov (2016) Theory in The Research ProcessDocument29 pages07 - Toshkov (2016) Theory in The Research ProcessFerlanda LunaNo ratings yet

- Calculating parameters for a basic modern transistor amplifierDocument189 pagesCalculating parameters for a basic modern transistor amplifierionioni2000No ratings yet

- June 10Document16 pagesJune 10rogeliodmngNo ratings yet

- Laughing at Heads in the CloudsDocument2 pagesLaughing at Heads in the Cloudsmatfox2No ratings yet

- Case - History WPC 3790-2013Document2 pagesCase - History WPC 3790-2013Sachin solomonNo ratings yet

- EthicsDocument10 pagesEthicsEssi Chan100% (4)

- The Irish Light 10Document28 pagesThe Irish Light 10Twinomugisha Ndinyenka RobertNo ratings yet

- Alat Studio Dan KomunikasiDocument14 pagesAlat Studio Dan Komunikasiraymon akbarNo ratings yet